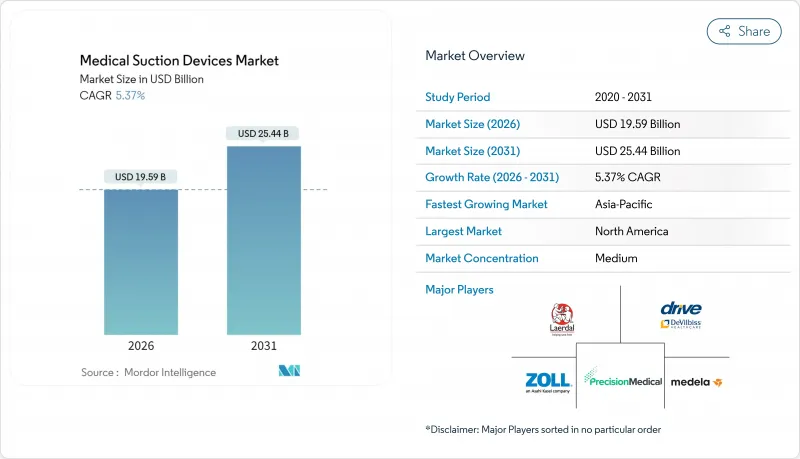

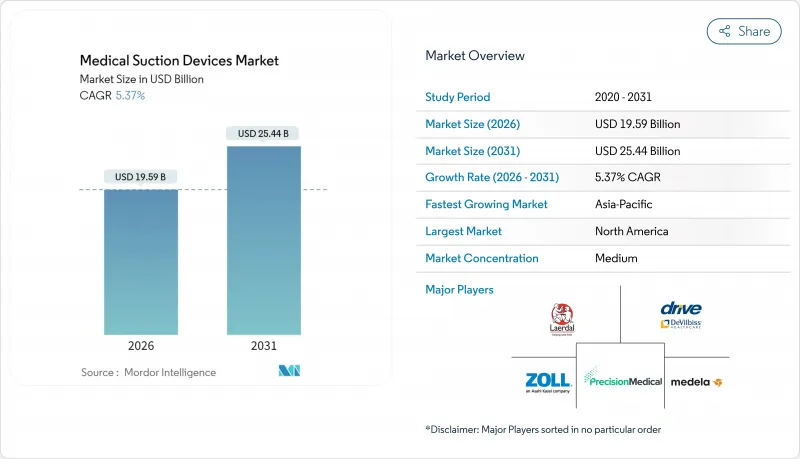

세계의 의료용 흡입 장치 시장 규모는 2026년 195억 9,000만 달러로 추정되고 있으며, 2025년 185억 9,000만 달러에서 성장할 전망입니다. 2031년에는 254억 4,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.37%로 확대될 전망입니다.

응급 의료, 집중 치료 및 수술실에서 기도 관리 솔루션에 대한 견조한 수요가 이러한 확대를 지원합니다. 배터리와 펌프의 효율 향상에 의해 경량화, 정음화 및 고출력화된 휴대형 기기가 실현되어, 외래 진료 센터나 재택 환경으로 케어 이행을 지원하고 있습니다. 북미는 엄격한 품질 기준과 지원적인 상환제도에 힘입어 39.34%의 수익 점유율로 주도적 지위를 유지하고 있습니다. 한편 아시아태평양은 수술 건수 증가와 병원 수용력 확대를 배경으로 6.97%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 기록하고 있습니다. 경쟁의 심각성은 여전히 중간 정도입니다. 세계의 기존 기업들은 소음 억제와 스마트 센서를 통한 제품 차별화를 중시하고 있으며, 지역 업체들은 가격에 민감한 구매자에게 적합한 비용 최적화 제품을 추구하고 있습니다. 일회용 플라스틱 용기에 대한 모니터링 강화는 이미 설계 로드맵을 재사용 가능하거나 재활용할 수 있는 옵션으로 이끌어 왔으며 일부 공급업체는 추가 컴플라이언스 비용이 발생할 수 있습니다.

특히, 수술 분야를 청결하게 유지하기 위해 정밀한 체액 배출을 필요로 하는 저침습 접근을 포함하여 선택적 수술 및 외상 수술의 수가 증가하고 있습니다. 로봇 지원 및 컴퓨터 지원 시스템은 현재 많은 척추, 비뇨기, 복부 수술로 주류가 되고 있으며, 그 성공은 카메라 안정성으로 인해 진동이 없는 안정적인 음압을 제공하는 의료용 흡입 장치 시장의 솔루션에 달려 있습니다. 외과의사는 또한 전기 수술 기구와 동기화하는 프로그램 가능한 유량을 요구하며, 이는 연기 및 혈액 오염을 감소시킵니다. 북미 주요 병원의 하이브리드 수술실에서는 이러한 요구에 대응하기 위해 각 타워에 듀얼 고진공 펌프를 표준 장비하고 있습니다. 마찬가지로 아시아태평양의 시설에서는 심혈관 수술실을 재개발할 때 멀티포트 콜렉터를 표준 장비하여 순환기 전문의와 외과의사가 동시에 작업할 수 있도록 하고 있습니다. 따라서 제조업체는 0.1초 이내에 진공도를 조정하는 디지털 컨트롤러를 통합하여 혈행 동태의 가시성을 향상시키고 수술 시간을 단축하고 있습니다.

만성 폐색성 폐질환(COPD), 천식, 기관지 확장증은 여전히 심각한 사망률과 이환율 부담을 초래하여 의료용 흡입 장치 시장 전체 수요를 직접 확대하고 있습니다. 급성 악화는 종종 점액 과분비와 기도 폐색을 일으키고 응급 부문의 첫 번째 관리 방법은 여전히 적극적인 흡입을 포함합니다. 가정에서 분비물 제거 요법도 마찬가지로 중요합니다. 호흡기 전문의는 환자가 자기 관리로 분비물을 제거하고 재입원을 피할 수 있도록 -600mmHg의 흡입력을 가진 휴대용 장치를 처방합니다. 원격 모니터링 프로그램을 시험 도입하고 있는 라틴아메리카의 공적 보험 기관에서는 사용 패턴을 호흡 요법사에게 송신하는 Bluetooth 대응 흡입기의 비용을 현재 상환하고 있습니다. 이러한 데이터 스트림은 임상의가 기관지 확장제의 복용량을 조정하고, 복약 준수의 갭을 검출하는 데 도움이 되며, 흡입 장치를 만성 질환 관리 경로에 추가로 통합할 수 있습니다.

고급 흡입 펌프는 안전한 진공 성능을 유지하기 위해 정기적인 교정, 필터 교환 및 훈련을 받은 기술자의 정기 점검이 필요합니다. 이러한 유지 보수 작업은 장비 수명주기를 통해 초기 구매 가격을 초과하는 지속적인 비용을 발생시키고 소규모 병원 및 지방 클리닉 예산을 압박합니다. 부품이나 숙련된 기술자가 현지에서 입수할 수 없는 경우, 시설은 기기를 도시의 서비스 센터에 보내야 하고, 환자 케어를 중단시키는 다운타임이 발생합니다. 미국 국토 안보부의 평가에서는 휴대형 장치의 보수성에 큰 편차가 인정되었고, 일부 모델에서는 많은 저자원 의료 제공업체가 보유하지 않은 특수 공구가 필요하다고 지적되었습니다. 이러한 장벽에 직면한 관리자들은 보다 단순한 수동식 장치를 선택하거나 업그레이드를 연기하는 경우가 많아 신흥 시장에서 현대 시스템의 보급을 늦추고 의료용 흡입 장치 시장의 성장을 억제하고 있습니다.

2025년 시점에서 AC 전원식 의료용 흡입 장치는 시장 점유율의 44.52%를 차지하며, 수술 및 집중 치료 팀이 가동 시간 제한을 허용할 수 없기 때문에 주도적 지위를 유지하고 있습니다. 인도와 중국에서 뇌신경 수술실을 확충하는 3차 의료기관에서는 설치업체가 -750mmHg의 지속 흡입력을 갖추고 이중 펌프 리던던시를 가지는 벽 콘센트식 유닛을 여전히 선호하고 있습니다. AC 전원 모델의 의료용 흡입 장치 시장 규모는 2025년 82억 7,000만 달러에서 2031년까지 121억 1,000만 달러에 달하고, CAGR 6.55%로 확대될 것으로 예측됩니다. 이것은 보다 진보된 치료가 필요한 병상의 동시적인 정비를 반영한 것입니다.

한편, 배터리 구동 시스템은 현재 규모가 작지만, 인체공학적 개선을 목표로 하는 구급차 사업자로부터 지지를 모으고 있습니다. AIRO 흡입 유닛은 중량 0.9kg이면서 최대 흡입시에도 30분간 가동을 가능하게 하는 충전 성능을 갖추고 있습니다. 응급 의료 기술자는 일회용 소수성 필터로 사용 후 청소를 줄이고 현장 회전율이 24% 향상된 것으로 보고되었습니다. 제조업체는 현재 USB-C 급속 충전 어댑터를 동봉해, 병원 반송중에 기기를 충전할 수 있도록 하고 있습니다. 이것은 배터리 사이클을 기록하는 국제 EMS 자산 추적 프로토콜을 준수합니다.

벽걸이식 시스템은 수술실, 분만센터 및 집중치료실에 대한 임베디드 설치에 의해 2025년 시점에서 의료용 흡입 장치 시장 규모의 45.48%를 유지했습니다. 미국 지역 병원의 리노베이션 프로그램은 아날로그 측정기를 디지털 LED로 업데이트하고 부압이 설정 값 아래로 떨어지면 직원에게 경보를 발합니다. 동시에 환기 전문가가 중앙 대시보드에서 원격으로 유량을 조정하여 환자 수 증가 시 대응력을 강화하고 있습니다.

한편, 핸드헬드 및 휴대용 부문은 2031년까지 연평균 복합 성장률(CAGR) 7.84%로 확대될 것으로 예측되고 있으며, 응급 구명사나 재택치료에서 컴팩트한 기기에 대한 수요를 반영하고 있습니다. NAR 택티컬 흡입 장치는 권총 그립식 펌프로 100mmHg의 흡입력을 발생시켜 무게는 400g 미만이므로 좁은 공간에서도 한 손으로 기도 확보가 가능합니다. 아시아태평양의 인도적 지원 기관은 유지 보수가 최소한으로 전기 부품을 필요로 하지 않기 때문에 재해용 키트에 이러한 장치를 상비하고 있어 사이클론이나 홍수 기간 중 판매 대수 증가 요인이 되고 있습니다.

북미는 39.12%의 수익 점유율로 선두를 유지하고 있습니다. 이것은 모든 중요 침대에서 지속적인 흡입 기능을 확보하도록 의무화하는 엄격한 기준 때문입니다. 메디케어 메디케이드 서비스 센터(CMS)는 공제액 이후 DME 청구액의 80.0%를 상환하기 위해 재택 인공호흡기 사용자에 의한 휴대형 펌프의 이용 기회가 확대되고 있습니다. 연방 보조금에 의한 차량 갱신을 진행하는 미국의 응급 서비스에서는 차재 텔레매틱스와 통합 가능한 리튬 전지식 유닛의 표준화가 진행되어, 지역 내의 설치 대수가 더욱 증가하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 6.91%를 보일 것으로 예측됩니다. 인도의 생산 연동형 장려 제도(PLI)는 국내 흡입 장치에 대해 5-10%의 보조금을 제공하여 안드라 프라데시의 의료기기 산업에서 공장 투자를 촉진하고 있습니다. 중국의 현 레벨 외상 센터에서는 이비인후과 전용 스위트가 추가되어 각 시설에서 이중 진공 레귤레이터가 필요하기 때문에 현지 조립 제조업체의 처리량이 증가하고 있습니다. 일본에서는 급속한 고령화가 진행되고 있습니다. 이 때문에 지방자치단체의 건강보험조합은 재택 COPD 관리용의 휴대형 흡입기를 자금 원조하고 있어 HEPA 배기 기능을 갖춘 고가격 모델을 지원하고 있습니다.

유럽에서는 PVC 폐기물을 처벌하고 고체화 기능이 있는 폴리프로필렌 캐니스터의 사용을 권장하는 환경 규제로 인해 지속적인 수요가 예상됩니다. 클로즈드 라이너 시스템을 도입한 독일 병원에서는 직원 노출 사고가 23.0% 감소하여 입찰 전환이 가속화되고 있습니다. 영국 NHS 트러스트는 지속가능성을 중시하고 재활용 가능한 하우징과 에너지 절약 대기 모드를 갖춘 펌프를 선호합니다.

중동 및 아프리카에서는 전망이 복합적입니다. 걸프 협력 회의 회원국은 새로운 외상 센터를 위해 높은 사양의 장비를 수입하고 있지만, 사하라 이남의 아프리카에서는 전력 공급의 불안정성을 보완하기 위해 견고하고 배터리가 필요없는 펌프가 우선합니다. 남미에서는 브라질이 중간 정도의 확대를 견인하고 있으며, 관민 제휴에 의해 주립 병원의 외과 수술 능력의 증강에 자금이 투입되어 수동 발 작동식에서 전동식으로 업그레이드가 진행되고 있습니다.

The Medical Suction Devices Market size in 2026 is estimated at USD 19.59 billion, growing from 2025 value of USD 18.59 billion with 2031 projections showing USD 25.44 billion, growing at 5.37% CAGR over 2026-2031.

Robust demand for airway management solutions in emergency medicine, critical care, and operating rooms underpins this expansion. Battery and pump efficiency gains are enabling lighter, quieter, and more powerful portables, supporting the shift of care toward ambulatory centers and the home environment. North America retains leadership with 39.34% revenue share, aided by strict quality standards and supportive reimbursement, while Asia-Pacific posts the fastest growth at 6.97% CAGR on the back of rising surgical volumes and expanded hospital capacity. Competitive intensity remains moderate: global incumbents emphasize product differentiation through noise suppression and smart sensors, and regional manufacturers pursue cost-optimized offerings that suit price-sensitive buyers. Heightened scrutiny of single-use plastic canisters is already steering design roadmaps toward reusable or recyclable options and may create incremental compliance costs for some suppliers.

Expanding elective and trauma surgery volumes, especially minimally invasive approaches that require precise fluid evacuation to keep the field clear. Robotic and computer-assisted systems now dominate many spine, urology, and abdominal procedures, and their success hinges on medical suction devices market solutions that deliver steady negative pressure without vibration for camera stability. Surgeons also request programmable flow rates that synchronize with electrosurgical tools, reducing smoke and blood contamination. Hybrid operating rooms in leading North American hospitals routinely outfit each tower with dual high-vacuum pumps to meet these needs. Asia-Pacific facilities redeveloping cardiovascular theaters similarly standardize on multiport collectors so that perfusionists and surgeons can operate simultaneously. Manufacturers therefore integrate digital controllers that adjust vacuum within 0.1 seconds, improving hemodynamic visibility and shortening operative time.

Chronic obstructive pulmonary disease, asthma, and bronchiectasis continue to exert profound mortality and morbidity burdens directly expanding demand across the medical suction devices market. Acute exacerbations commonly lead to mucus hypersecretion and airway obstruction, and first-line management in emergency departments still includes aggressive suctioning. Home-based clearance regimens are equally critical: pulmonologists prescribe portable devices capable of -600 mmHg vacuum so that patients can self-manage secretions and avoid rehospitalization. Latin American public insurers piloting remote monitoring programs now reimburse for Bluetooth-enabled aspirators that relay usage patterns to respiratory therapists. These data streams help clinicians titrate bronchodilators and detect adherence gaps, further embedding suction equipment into chronic-care pathways.

Advanced suction pumps require routine calibration, filter replacement, and periodic servicing by trained technicians to keep vacuum performance within safe limits. These maintenance steps add recurring costs that can exceed the original purchase price over the equipment's life cycle, straining budgets in small hospitals and rural clinics. When parts or skilled labor are unavailable locally, facilities must ship devices to urban service centers, causing downtime that interrupts patient care. A U.S. Department of Homeland Security evaluation found wide variation in maintainability among portable units and noted that some models demand specialized tools that many low-resource providers do not possess. Faced with these hurdles, administrators often choose simpler manual devices or postpone upgrades, slowing penetration of modern systems in emerging markets and moderating growth of the medical suction devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The AC-powered class generated 44.52% of the medical suction devices market share in 2025, retaining primacy because surgical and intensive-care teams cannot tolerate runtime limits. In tertiary hospitals expanding neurosurgical suites across India and China, installers continue to favor wall-outlet units rated to -750 mmHg sustained vacuum with dual-pump redundancy. The medical suction devices market size for AC-powered models is projected to grow from USD 8.27 billion in 2025 to USD 12.11 billion by 2031 at 6.55% CAGR, reflecting the parallel construction of higher-acuity beds.

Battery-powered systems, while smaller today, are winning preference among ambulance operators aiming for ergonomic upgrades. The AIRO Suction Unit weighs 0.9 kg yet holds charge for 30 minutes of peak draw. Emergency medical technicians note 24% faster scene turnover because disposable hydrophobic filters reduce post-use cleanup. Manufacturers now bundle USB-C fast-charge adaptors so devices recharge during transfer to hospitals, aligning with international EMS asset-tracking protocols that log battery cycles.

Wall-mounted systems maintained 45.48% of the medical suction devices market size in 2025 owing to embedded installation across operating rooms, birthing centers, and ICUs. Retrofit programs in U.S. community hospitals are upgrading analog gauges to digital LEDs that alert staff when negative pressure dips below set points. Simultaneously, ventilation specialists adjust flows remotely from central dashboards, enhancing responsiveness during high census periods.

Conversely, the hand-held/portable segment is forecast to post an 7.84% CAGR through 2031, reflecting paramedic and home-care demand for compact tools. The NAR Tactical Suction Device produces 100 mmHg vacuum via pistol-grip pump and weighs under 400 g, facilitating single-handed airway clearance in confined spaces. Asia-Pacific humanitarian agencies routinely keep such devices in disaster kits due to minimal maintenance requirements and absence of electrical components, a factor accelerating unit sales during cyclone and flood seasons.

The Medical Suction Devices Market Report is Segmented by Type (AC-Powered, Battery-Powered, and More), Portability (Hand-Held/Portable, Wall-Mounted, and Trolley/Cart-Mounted), Application (Airway Clearance, Surgical Applications, and More), End User (Hospitals, Home Healthcare Settings, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America leads with 39.12% revenue thanks to rigorous standards that require continuous suction availability at every critical bed. Centers for Medicare & Medicaid Services reimburse 80.0% of DME invoice amounts after deductibles, widening access to portable pumps for home ventilator users. U.S. ambulance services upgrading fleets under federal grants are standardizing on lithium-battery units that integrate with onboard telematics, further expanding the regional installed base.

Asia-Pacific is projected to record a 6.91% CAGR through 2031. The Indian Production Linked Incentive scheme offers 5%-10% subsidies on domestic suction equipment, spurring plant investments in Andhra Pradesh MedTech. China's county-level trauma centers add dedicated ENT suites, each requiring dual vacuum regulators, boosting volume throughput for local assemblers. Japan faces rapidly aging demographics; municipal health insurers thus fund portable aspirators for at-home COPD management, supporting premium-priced models with HEPA exhaust.

Europe maintains strong demand, driven by environmental regulation that penalizes PVC waste and encourages polypropylene canisters with integrated solidifiers. German hospitals adopting closed-liner systems reduced staff exposure incidents by 23.0%, accelerating tender conversions. United Kingdom NHS trusts emphasize sustainability, favoring pumps with recyclable housings and energy-saving standby modes.

Middle East & Africa offers mixed prospects: Gulf Cooperation Council states import high-specification devices for new trauma centers, while sub-Saharan regions prioritize rugged battery-free pumps to offset grid unreliability. South America's moderate expansion is led by Brazil, where public-private partnerships fund surgical capacity growth in state hospitals, driving upgrades from manual foot-operated to electric units.