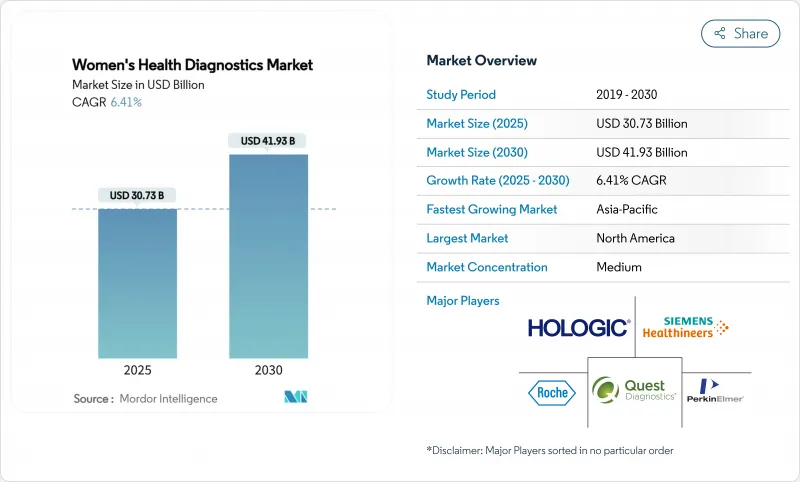

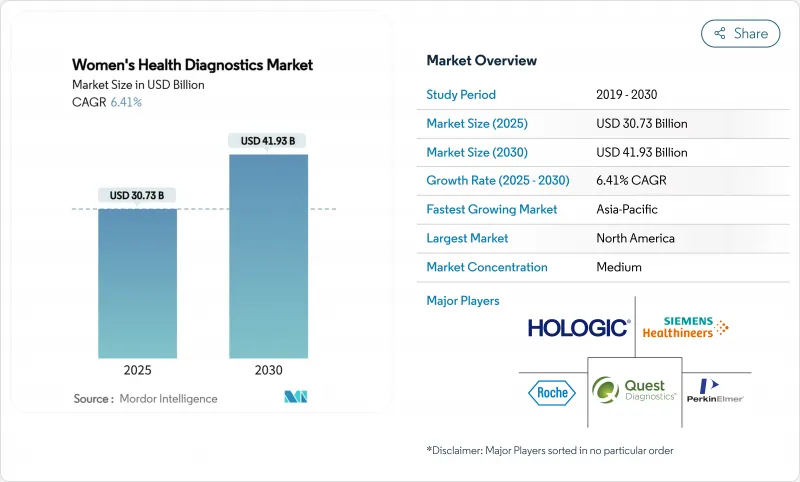

여성 건강 진단 시장 규모는 2025년에 307억 3,000만 달러, 예측기간(2025-2030년) CAGR은 6.41%를 나타내고, 2030년에는 419억 3,000만 달러에 달할 것으로 예측됩니다.

AI를 활용한 스크리닝 툴의 보급, 검사실이 개발한 검사의 합리화, 고용자의 예방급여에 대한 투자 확대로 여성 건강 진단 시장은 10년 후까지 안정된 성장 궤도를 유지합니다. 북미는 2024년 매출액의 38.26%를 차지해 이 분야를 계속 견인하고 있지만 아시아태평양은 인프라 투자와 사회적 인지도 향상 프로그램에 의해 검사 건수가 증가하여 가장 빠르게 성장하고 있습니다. 분자 분석은 유방, 자궁 경부, 감염의 진단 정확도를 높이고 원격 의료를 촉진하는 자기 채취 모델은 기존의 접근 장벽을 깎고 있습니다. 다국적 기기 제조업체가 영상 진단 및 체외 진단 플랫폼에 인공지능을 통합하는 한편, 펨텍의 신흥 기업이 소비자 직접 판매 채널에서 점유율을 획득하고 있기 때문에 경쟁 정보는 격렬함을 늘리고 있습니다.

비만, 당뇨병, 호르몬 관련 암의 세계적인 증가는 증상이 나타나기 전에 질병을 확인할 수 있는 조기 발견 도구 수요 증가로 이어지고 있습니다. 심장 대사 위험 인자는 유방암과 자궁 내막 암에 대한 여성의 취약성을 높이고 임상 의사에게 연령 기준을 넘어선 스크리닝 프로토콜의 확대를 촉구하고 있습니다. 유럽과 북미의 보건부는 현재 고위험 여성에게 유방 조영술과 유전 패널을 결합한 검사를 보험 적용하고 있으며, 병원 네트워크 전체에서 검사 건수를 늘리고 있습니다. 웨어러블 바이오센서는 실시간으로 신진 대사 변화를 감지하고 예측 알고리즘을 위한 신선한 데이터 세트를 생성하는 데 사용됩니다. 여성의 수명이 연장됨에 따라, 만성 질환을 업스트림로부터 관리하는 것이 임상적으로 필수적이 되고, 여성 건강 진단 시장은 계속 추진될 것입니다.

포인트 오브 케어 플랫폼은 진단주기를 며칠에서 몇 분으로 단축시켜 합병증이 발생하기 전에 감염을 치료할 수 있도록 도와줍니다. 클라미디아, 임질, 트리코모나스에 대한 최초의 OTC 분자 검사가 2025년 FDA로부터 허가됨으로써 소비자는 집에서 3병원체를 스크리닝하고 30분 내에 결과를 받을 수 있게 되었습니다. 미국의 시골마을에 있는 이동 진료소에서는 골반내 염증성 질환을 당일 관리하기 위한 휴대용 PCR 장치가 배치되어 유럽의 약국에서는 CLIA 면제의 임신 관련 자간전증 검사가 도입되고 있습니다. 신속한 턴어라운드 시간은 후속 손실을 최소화하고, 항균제 스튜어드십을 향상시키고, 지불자가 비용이 많이 드는 후기 개입을 피하는 데 도움이 되며 여성 건강 진단 시장에 대한 호영을 강화하고 있습니다.

MRI 및 고급 초음파 진단 장비의 설비 투자액은 1대당 200만 달러를 초과할 수 있어 신흥국의 병원의 과제가 되고 있습니다. 환율과 수입 관세는 구매 비용을 밀어 올리고, 교체주기를 늦추고 대상 지역을 제한합니다. 벤더의 자금 조달이나 관민 파트너십에 의해 예산의 제약이 완화되고 있다고 해도, 많은 시설에서는 AI에의 대응이 부족한 아날로그 시스템을 운용하고 있습니다. 따라서 소유 비용 상승은 최첨단 모달리티의 단기적인 전개를 억제하고 여성 건강 진단 세계 시장 CAGR의 발판이 되고 있습니다.

진단 검사는 수익의 대부분을 차지하고 2024년 여성 건강 진단 시장의 54.68%를 차지했습니다. 분자 플랫폼은 성 감염, 유전성 암 변이, 출생 전 이상을 1회로 다중 검출할 수 있기 때문에 인기가 높습니다. 샘플 투안서 카트리지가 장착된 고처리량 PCR 시스템은 현재 많은 기준 실험실에서 표준으로 장착되어 있어 작업 시간을 단축하고 당일 치료 시작을 지원합니다. 유전자 패널과 유전체 패널은 CAGR9.24%로 가장 빠르게 확대된 제품 라인으로, 주로 BRCA와 린치 증후군 스크리닝의 보험 적용 범위 확대로 인한 것입니다. 디지털 임신·배란 검사약 수요는 스마트폰과의 제휴에 의한 주기의 추적이나 원격 상담 포털의 제공에 의해 견조하게 추이하고 있습니다.

진단 장비는 나머지 45.32%의 점유율을 차지했으며, 인공지능 대응 유방 조영술, 초음파 및 골밀도 측정 장비가 견인했습니다. 자동 유방 초음파 검사 시스템은 3D 재구성과 밀도 스코어링을 통합하여 스캔 시간과 운영자의 변동을 줄입니다. 생검 도구는 조직 외상을 억제하는 진공 보조 바늘 설계로 업그레이드되었으며 가이드 네비게이션 소프트웨어는 임상의가 mm 이하의 정확도로 병변을 채취 할 수 있도록 지원합니다. 예측 기간 동안 장비와 소프트웨어 번들 판매를 통해 제조업체는 분석 모듈을 교차 셀링하고 여성 건강 진단 시장에서 경상 수익원을 강화할 수 있습니다.

면역검정은 호르몬 검사, 종양 검사, 감염증 검사에 있어서의 범용성이 평가되어 2024년에는 31.93%로 계속해서 가장 중요한 기술 슬라이스가 되었습니다. 화학발광 기질의 지속적인 개선으로 측정 시간이 15분 미만으로 단축되고 응급 상황에서 퇴거 도구로 실용화되었습니다. 한편, AI를 활용한 애널리틱스는 CAGR 8.35%로 급성장하고 있으며, 이는 알고리즘에 의한 유선 밀도와 리스크 스코어링의 FDA 인가에 뒷받침된 것입니다. 클라우드 기반의 머신러닝 파이프라인을 도입하면 소규모 클리닉에서도 On-Premise 무거운 하드웨어 없이 이미지 데이터를 처리할 수 있어 고급 분석에 대한 액세스가 민주화됩니다.

분자진단학은 분산형 검사에 적합한 루프 매개 등온증폭법과 CRISPR 기반의 검출형식에 의해 여전히 유력한 분야입니다. 이미지 기술도 멈추지 않았습니다. 공급업체는 낮은 선량으로 이미지의 선명도를 향상시키는 딥러닝 재구성을 추가합니다. 이러한 진보가 결합되어 임상 적응이 확대되고, 처리량이 향상되고, 여성 건강 진단 시장의 기세가 지속되고 있습니다.

북미가 2024년 매출의 38.26%를 차지해 톱이 되었습니다. 이는 탄탄한 상환 정책과 FDA 승인의 꾸준한 쌓아 놓기로 뒷받침되며 혁신을 벤치에서 침대 쪽으로 다른 어떤 지역보다 빠르게 견인하고 있습니다. 미국 보험사는 2024년 유방밀도보고가 의무화된 후 AI지원 유방촬영 보험 적용을 확대했습니다. 캐나다에서는 HPV 자체 채취가 시작되어 충분한 서비스를 받지 못한 그룹에서 자궁 경부 검진의 컴플라이언스가 향상되었습니다.

아시아태평양은 CAGR 9.74%에서 가장 급속히 성장했으며, 지금까지 검진 인프라가 보급되지 않았던 인구가 많은 나라까지 여성 건강 진단 시장이 확대됐습니다. 중국은 농촌의 영상 진단 차량과 유전체 종양 프로파일링에 보조금을 내고 있으며, 일본의 민간보험사는 유선의 밀집한 환자에게 AI 지원 초음파 검사를 적용하고 있습니다. 인도에서는 원격 의료 플랫폼과 포인트 오브 케어 PCR을 통합하여 원격지 마을에 접근하여 도시와 농촌의 검진 격차를 줄이고 있습니다. 싱가포르, 한국, 호주 신흥 기업은 월경 건강 분석 및 생식 능력 평가에 주력하고 제품 파이프라인에 지역 색상을 주입하고 있습니다.

유럽은 확립된 국가 스크리닝 프로그램에 의해 균형 잡힌 위치를 유지하고 검사량을 안정시키고 있습니다. 독일과 영국은 AI 엔진과 연계한 클라우드 기반 PACS를 솔선하여 채택하고 있으며, 프랑스는 공립병원에서 유방암·난소암 유전자 스크리닝을 일괄하여 시험적으로 도입하고 있습니다. 남유럽 국가들은 EU의 체외 진단 규제의 이행을 예상하여 LDT 검증 과정의 조화를 도모하고 환자의 안전을 지키고 신뢰를 유지하고 있습니다. 이러한 이니셔티브는 유럽 전역에서 여성 건강 진단 시장의 장기적인 탄력성을 강화하는 것입니다.

The Women's Health Diagnostics Market size is estimated at USD 30.73 billion in 2025, and is expected to reach USD 41.93 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

Uptake of AI-enabled screening tools, streamlined pathways for laboratory-developed tests, and growing employer investment in preventive benefits will keep the women's health diagnostics market on a steady growth path through the end of the decade. North America continues to anchor the field with 38.26% revenue in 2024, yet Asia-Pacific is advancing fastest as infrastructure spending and public awareness programs lift test volumes. Molecular assays are raising diagnostic accuracy for breast, cervical, and infectious diseases, while tele-health-facilitated self-collection models chip away at traditional access barriers. Competitive intensity is rising as multi-national device makers embed artificial intelligence across imaging and in-vitro platforms, even as fem-tech startups win share in direct-to-consumer channels.

The global growth in obesity, diabetes, and hormone-related cancers is translating into greater demand for early detection tools that can identify disease before symptoms appear. Cardiometabolic risk factors elevate female vulnerability to breast and endometrial cancers, prompting clinicians to widen screening protocols beyond age-based criteria. Health ministries in Europe and North America now reimburse combined mammography and genetic panels for high-risk women, boosting test volumes across hospital networks. Wearable biosensors are being trialed to detect metabolic changes in real time, creating fresh datasets for predictive algorithms. As women's lifespans lengthen, the clinical imperative to manage chronic disease upstream will continue to propel the women's health diagnostics market.

Point-of-care platforms shorten diagnostic cycles from days to minutes, making it easier to treat infections before complications arise. The FDA's 2025 clearance of the first OTC molecular test for chlamydia, gonorrhea, and trichomoniasis allows consumers to perform triple-pathogen screening at home and receive results in 30 minutes. Mobile clinics in rural U.S. counties now deploy portable PCR units for same-day pelvic inflammatory disease management, while European pharmacies have introduced CLIA-waived pregnancy-related preeclampsia assays. Fast turnaround times minimize follow-up loss, improve antimicrobial stewardship, and help payers avoid costly late-stage interventions, reinforcing the positive impact on the women's health diagnostics market.

Capital expenditure for MRI and advanced ultrasound can exceed USD 2 million per unit, a figure that challenges hospitals in emerging economies. Currency depreciation and import tariffs inflate acquisition costs, slowing replacement cycles and limiting geographic coverage. Although vendor financing and public-private partnerships are easing budget constraints, many facilities still operate analog systems that lack AI readiness. Elevated ownership costs thus temper the near-term rollout of cutting-edge modalities, creating a moderate drag on the global women's health diagnostics market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Diagnostic tests generated the majority of revenue, accounting for 54.68% of the women's health diagnostics market in 2024. Molecular platforms are popular because they deliver multiplex detection of sexually transmitted infections, hereditary cancer mutations, and prenatal anomalies in a single run. High-throughput PCR systems equipped with sample-to-answer cartridges are now standard in many reference labs, reducing hands-on time and supporting same-day therapy initiation. Genetic and genomic panels represent the quickest-expanding product line at a 9.24% CAGR, mainly due to broader insurance coverage for BRCA and Lynch syndrome screening. Demand for digital pregnancy and ovulation tests remains steady, as smartphone linkages offer cycle tracking and tele-consultation portals.

Diagnostic devices held the remaining 45.32% share, led by AI-capable mammography, ultrasound, and bone densitometry equipment. Automated breast ultrasound systems integrate 3D reconstruction and density scoring, cutting scan time and operator variability. Biopsy tools are upgrading to vacuum-assisted needle designs that limit tissue trauma, and guided navigation software helps clinicians sample lesions with sub-millimeter precision. Over the forecast window, bundled device-and-software sales will allow manufacturers to cross-sell analytics modules, reinforcing their recurring revenue streams within the women's health diagnostics market.

Immunoassays remained the most significant technology slice at 31.93% in 2024, valued for their versatility in hormone, oncology, and infectious disease testing. Continuous improvements in chemiluminescent substrates have shortened assay times to under 15 minutes, making them practical triage tools in emergency settings. Meanwhile, AI-enabled analytics is climbing fastest with an 8.35% CAGR, propelled by FDA clearances for algorithmic breast density and risk scoring. Deployment of cloud-based machine learning pipelines lets small clinics process imaging data without heavy on-premises hardware, democratizing access to advanced analytics.

Molecular diagnostics remains a powerhouse segment, thanks to loop-mediated isothermal amplification and CRISPR-based detection formats suited for decentralized testing. Imaging technology is not standing still: vendors are adding deep-learning reconstruction that improves image clarity at lower radiation doses. Together, these advances are widening clinical indications and boosting throughput, sustaining momentum in the women's health diagnostics market.

The Women's Health Diagnostics Market Report is Segmented by Product Type (Diagnostic Devices, Diagnostic Tests), Technology (Immunoassay, Molecular Diagnostics, Imaging, AI-Enabled Analytics), Application (Breast Cancer, and More), End User (Hospitals & Diagnostic Centres, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 38.26% of 2024 revenue, underpinned by robust reimbursement policies and a steady cadence of FDA approvals that pull innovation from bench to bedside faster than any other region. United States insurers expanded coverage for AI-assisted mammography after mandated breast density reporting took effect in 2024. Canada's HPV self-collection launch is lifting cervical screening compliance among underserved groups.

Asia-Pacific posted the quickest regional climb at a 9.74% CAGR, extending the women's health diagnostics market into populous countries that previously lacked widespread screening infrastructure. China subsidizes rural imaging vans and genomic tumor-profiling grants, and Japan's top private insurers now cover AI-assisted ultrasound for dense-breast patients. India is leveraging telemedicine platforms integrated with point-of-care PCR to reach remote villages, narrowing the urban-rural detection gap. Startups across Singapore, South Korea, and Australia are focusing on menstrual health analytics and fertility assessment, injecting local flavor into product pipelines.

Europe maintains a balanced position with established national screening programs that keep test volumes steady. Germany and the United Kingdom are leading adopters of cloud-based PACS linked to AI engines, while France is piloting bundled breast and ovarian cancer genetic screening in public hospitals. Southern European countries are harmonizing LDT validation processes in anticipation of the EU In-Vitro Diagnostic Regulation transition, protecting patient safety and sustaining trust. Together, these initiatives reinforce the long-term resilience of the women's health diagnostics market across the continent.