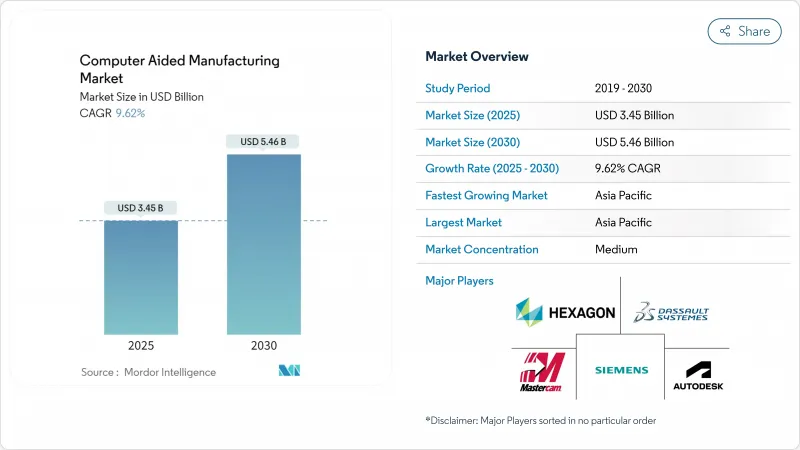

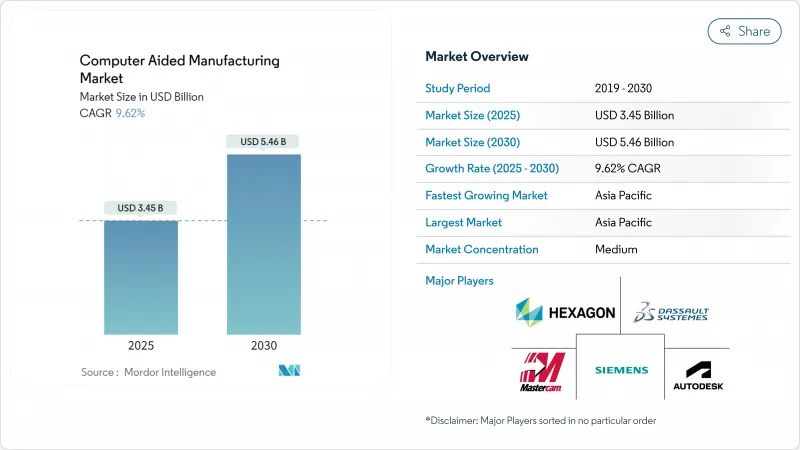

컴퓨터 지원 제조 시장 규모는 2025년에 34억 5,000만 달러, 2030년에는 CAGR 9.62%를 나타내고, 54억 6,000만 달러로 확대될 것으로 예측됩니다.

서브트랙티브+아디티브의 하이브리드 생산 셀로의 시프트, 인공지능과 툴패스 생성의 융합, 국산 반도체 패키징이나 전기자동차 부품을 우대하는 정부의 재쉐어링 우대조치 등이 성장의 요인이 되고 있습니다. 클라우드 네이티브 협업과 On-Premise 보안을 융합할 수 있는 공급업체는 방어 등급의 지적 재산 프로토콜을 존중하면서 여러 대륙에 걸쳐 항공우주 프로그램에서 이익을 얻고 있습니다. Siemens, Autodesk, Dasso Systems는 실시간 기계 분석을 설계부터 제조까지 제품군에 통합하여 순수한 프로그래밍 속도를 뛰어넘는 예지 보전 통찰력을 사용자에게 제공하여 플랫폼 통합을 강화하고 있습니다.

하이브리드 시스템은 레이저 또는 지향성 에너지 증착과 고속 마무리 가공을 하나의 인클로저에 통합하여 2차 계단을 제거하고 원료 낭비를 최대 40% 절감합니다. Siemens NX는 현재 비드 온월 증착 및 마무리 공구 경로를 자동화하고 항공우주 등급의 표면 마감를 달성하기 전에 필요한 부분에만 재료를 증착하여 복잡한 티타늄 부품의 전체 사이클 시간을 25-30% 단축합니다. 실제 롤아웃은 가법적 및 감법적 동작을 마이크로초 단위로 동기화하도록 훈련된 운영자에게 달려 있지만, 이 기술은 대부분의 가공 공장에서 부족합니다.

폐쇄 루프 플랫폼은 CAM 프로그래밍 파라미터를 실시간 스핀들 파워, 진동 및 공구 마모 센서에 연결합니다. 헥사곤의 알고리즘은 15-20분 전에 임박한 공구의 결함을 검출하고 이송 속도를 자동 조정하여 표면 품질을 공차 내에 유지함으로써 깨지기 쉬운 항공우주용 합금의 스크랩을 경감합니다. 이러한 솔루션은 고밀도 센서 네트워크와 높은 처리량 분석을 필요로 하므로 부품 가치가 자본 지출을 정당화하는 공장으로의 도입이 제한됩니다.

FreeCAD PathWorkbench는 현재 라이선스 비용 없이 2.5축 G 코드를 출력할 수 있기 때문에 학교와 마이크로 워크숍 입문 수준의 선택으로 신뢰할 수 있습니다. 상용 벤더는 AI를 활용한 최적화나 클라우드 협업 등 대부분의 커뮤니티 프로젝트의 계산 능력을 뛰어넘는 기능을 번들로 대항하고 있지만, 기본 모듈이 상품화하는 것을 막아야 합니다.

클라우드 호스팅형 스위트는 컴퓨터 지원 제조 시장 전체에서는 아직 소수파이지만, 2030년까지의 CAGR이 10.9%인 것은 돌이킬 수 없는 방향성을 나타내고 있습니다. 3대륙에 공장을 갖춘 항공우주 그룹은 브라우저 기반의 툴패스 편집을 이용하여 야간에 작업을 인도하고 리드타임을 20-25% 단축하고 있습니다. 국방 관련 계약자는 ITAR 규정이 현장에서 데이터 주권을 요구하기 때문에 완전 전환에 저항합니다. 그 결과 클라우드 솔버에 연결된 로컬 포스트 프로세서의 하이브리드 스택이 브리지를 형성합니다. 에지 게이트웨이는 OPC-UA 또는 MTConnect가 없는 구형 머신에 뒷받침함으로써 컨트롤러를 교체하지 않고 암호화된 데이터를 스트리밍할 수 있습니다. 구독 모델은 비용을 자본 예산에서 운영 비용으로 이동시킵니다. 클라우드 분석을 통해 공급업체는 익명화된 함대 전체의 스핀들 사용률을 벤치마킹하고 예기치 않은 다운타임을 줄이는 예측 유지보수 대시보드에 반영할 수 있습니다. 제로 트러스트 아키텍처가 성숙함에 따라 보수적인 섹터조차도 2027년까지 테스트 전환을 계획하고 있으며, 컴퓨터 지원 제조 시장이 다음 예산 주기 내에서 심리적 클라우드 채택 임계값을 초과함을 시사합니다.

그럼에도 불구하고 온 - 프레미스 기반은 에어 갭 네트워크와 독점적 인 합금 배합을 가진 공장에 여전히 필수적입니다. 공급업체는 방화벽 내부에 있는 동안 선택한 메타데이터를 원격지 전문가를 위해 클라우드 저장소에 동기화하는 디지털 스레드 모듈을 라이선싱하여 이러한 계정을 획득했습니다. 이 트윈 트랙 전략은 고객이 하이브리드 분석으로 전환함에 따라 라이선스 갱신을 안정화하는 동시에 경상 수익을 증가시킵니다. 플랫폼 구독 단계가 클라우드 컴퓨팅 크레딧을 켜거나 끌 수 있기 때문에 배포 모드 간의 개별 가격 설정은 시간이 지남에 따라 사라질 수 있습니다. 사이버 보험 보험료는 기계 공구의 네트워크에 대한 노출을 반영하고 CFO는 보안 인증을 총 소유 비용에 반영합니다. 그 결과, Computer-Aided Manufacturing 시장은 클라우드인지 온사이트인지라는 2자 대안이 아니라 유연한 입주 형태로 진화하고 있습니다.

2024년 매출의 36.2%를 차지한 자동차는 보다 광범위한 컴퓨터 지원 제조 시장의 중심 부문입니다. 그러나 내연 기관 부품 가공에서 전기자동차 부품 가공으로의 전환은 오랜 툴패스 라이브러리에 도전을 제기하고 있습니다. 배터리 트레이의 밀링은 높은 실리콘 알루미늄 처리량을 유지하면서 채터를 관리하는 얇은 전략을 필요로 합니다. 한편, 항공우주 및 방위에서는 규모가 작은 것, 5축 가공과 복합재 가공에 프리미엄 라이선스를 요구하고 있습니다. 의료기기 제조업체는 ISO 13485의 추적성을 충족하기 위해 AI 매개 변수 튜닝을 채택하여 수동으로 편집하지 않고 단일 운영자 셀에서 10μm 이하의 공차를 달성 할 수 있습니다. 전자기기나 반도체의 패키징 가공에서는 10만 rpm의 드릴 가공으로 구리의 박리를 방지하기 위해 열을 고려한 드릴 시퀀싱이 필요합니다. 의료기기 제조업체는 항공우주 표면 마감 루틴을 복제하고 자동차 제조업체는 배터리 모듈 웨이퍼 팹의 청정도 프로토콜을 수입하고 컴퓨터 지원 제조의 대응 가능한 시장을 확대하고 있습니다.

자동차 제조의 다양화도 마찬가지로 심각합니다. 구조 부품의 기가 캐스팅은 수십 개의 프레스 부품을 제거하지만 알루미늄 다이 캐스트의 대규모 CNC 마감재를 도입하여 높은 재료 제거율과 견고한 공구 수명 모델을 필요로합니다. 이러한 셀에 투자하는 공급업체는 20 시간 무인 이동으로 공구 마모 드리프트를 자동 보정하는 소프트웨어를 요구합니다. 대조적으로, 틈새 하이퍼커 제조 업체는 탄소섬유 트림에 중점을두고 생산 사이클마다 5 축 라우터와 프로브 기반 경로 업데이트를 사용합니다. 이러한 괴리는 하나의 업종이 여러 CAM 라이선스 계층에 걸쳐 있는 것을 의미하며, 자동차의 총 생산 대수가 평평해져도 컴퓨터 지원 제조 시장이 두께를 유지할 수 있도록 합니다.

아시아태평양의 점유율 47.1%는 제조업의 힘을 강조하고 있지만, 이 지역은 플러그 앤 플레이의 상호 운용성을 복잡하게 하는 CNC 프로토콜의 분단과 아직 격투하고 있습니다. 중국 정책은 자국제 컨트롤러와 연계된 자국제 CAM 알고리즘을 선호하고 있으며 세계 벤더가 2개 언어 포스트프로세서와 오픈 API 툴 라이브러리를 통해 다리를 해야 하는 병렬 생태계에 박차를 가하고 있습니다. 일본의 기계 OEM은 CAM을 제어 펌웨어에 직접 통합하여 툴 패스의 로딩 시간을 단축하고 있지만 고객은 자체 스택에 갇혀 있습니다. 인도의 Production Linked Incentive(생산 연동형 장려금) 제도는 노동력의 스킬업에 연결되면 CAM 라이선스를 보조하는 것으로, 벤더는 2030년까지 기존의 대기업에 필적할 수 있는 신흥 중견 시장에 대한 발판을 얻을 수 있습니다.

북미 유저가 클라우드 도입으로 선도하고 있는 이유는 CHIPS법이 520억 달러를 투입하기 때문입니다. 유럽은 에너지 효율적인 가공을 지지하고 압축공기 절감과 공구 재사용을 의무화하고 있으며, CAM 전략 시뮬레이터는 현재 부품당 킬로와트 시에 모델화하고 있습니다. 데이터 주권 규칙이 마찰을 낳고 있지만, Tier One 공급업체는 공장을 가로지르는 최적화 알고리즘을 대신하여 현지화된 데이터 레이크를 수용합니다. 이러한 지역 뉘앙스의 차이로 인해 컴퓨터 지원 제조 시장은 광범위한 다양화를 유지하고 지역적 침체에 대비할 수 있도록 합니다.

The Computer Aided Manufacturing market size reached USD 3.45 billion in 2025 and is forecast to expand to USD 5.46 billion by 2030, registering a 9.62% CAGR.

Growth stems from the shift to hybrid subtractive-plus-additive production cells, the fusion of artificial intelligence with tool-path generation, and government re-shoring incentives that favor domestic semiconductor packaging and electric-vehicle components. Vendors able to blend cloud-native collaboration with on-premises security benefit from aerospace programs that span multiple continents while respecting defense-grade intellectual-property protocols. Platform consolidation is intensifying as Siemens, Autodesk, and Dassault Systemes embed real-time machine analytics inside their design-to-manufacturing suites, giving users predictive maintenance insight that trumps pure programming speed.

Hybrid systems integrate laser or directed-energy deposition with high-speed finishing inside one enclosure, eliminating secondary setups and cutting raw-material waste by up to 40%. Siemens NX now automates bead-on-wall deposition and finishing toolpaths so manufacturers deposit material only where needed before achieving aerospace-grade surface finish, reducing overall cycle time for complex titanium parts by 25-30%. Real-world rollouts still hinge on operators trained to synchronize additive and subtractive motions within microsecond windows, a skill set in short supply across most job shops.

Closed-loop platforms connect CAM programming parameters to real-time spindle power, vibration, and tool-wear sensors. Hexagon algorithms detect impending tool failure 15-20 minutes in advance and auto-adjust feed rates to hold surface quality within tolerance, mitigating scrap on fragile aerospace alloys. These solutions require dense sensor networks and high-throughput analytics, restricting adoption to plants where part value justifies the capital outlay.

FreeCAD PathWorkbench now outputs 2.5-axis G-code at no license cost, making it a credible entry-level choice for schools and micro-workshops. Commercial vendors counter by bundling AI-driven optimization and cloud collaboration, features that exceed the computing means of most community projects, yet must guard against basic modules edging toward commoditization.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud-hosted suites still represent a minority of the overall Computer Aided Manufacturing market, but their 10.9% CAGR through 2030 underscores an irreversible direction. Aerospace groups with plants on three continents rely on browser-based toolpath editing to hand off jobs overnight, trimming lead times by 20-25%. Defense contractors resist full migration because ITAR rules demand onsite data sovereignty; consequently, hybrid stacks local post-processors linked to cloud solvers form the bridge. Edge gateways retrofit older machines lacking OPC-UA or MTConnect, letting them stream encrypted data without controller replacement. Subscription models shift costs from capital budgets to operating expenses, a boon for small shops that previously deferred software upgrades. Cloud analytics also enable vendors to benchmark spindle utilization across an anonymized fleet, feeding predictive-maintenance dashboards that slash unscheduled downtime. As zero-trust architectures mature, even conservative sectors plan pilot migrations by 2027, suggesting the Computer Aided Manufacturing market will cross a psychological cloud-adoption threshold within the next budget cycle.

The on-premises base nevertheless remains indispensable for plants with air-gapped networks and proprietary alloy formulations. Vendors court these accounts by licensing digital-thread modules that reside behind the firewall yet sync selected metadata to a cloud vault for remote experts. This twin-track strategy stabilizes license renewals while boosting recurring revenue as customers graduate to hybrid analytics. Over time, discrete pricing between deployment modes may vanish as platform subscription tiers simply toggle cloud compute credits on or off. With cyber-insurance premiums now reflecting machine-tool network exposure, CFOs increasingly factor security accreditation into total cost of ownership. Consequently, the Computer-Aided Manufacturing market is evolving toward flexible tenancy rather than binary cloud-versus-on-site choices.

Automotive held 36.2% revenue in 2024, making it the anchor segment of the broader Compute Aided Manufacturing market. Yet the shift from internal-combustion machining to electric-vehicle parts challenges long-standing toolpath libraries. Battery tray milling demands thin-wall strategies that manage chatter while sustaining throughput in high-silicon aluminum. Meanwhile, aerospace and defense, though smaller, command premium licenses for 5-axis and composite machining. Medical-device firms adopt AI-assisted parameter tuning to meet ISO 13485 traceability, letting single-operator cells hit sub-10 µm tolerances without manual edits. Electronics and semiconductor packaging operators require thermal-aware drill sequencing to prevent copper delamination during 100,000-rpm via drilling, a niche that the latest CAM modules fulfill through physics solvers. Cross-pollination is rising: medical device shops replicate aerospace surface-finish routines, while automotive tiers import wafer-fab cleanliness protocols for battery modules, expanding the total addressable market of Computer Aided Manufacturing.

Diversification inside automaking is equally profound. Gigacasting of structural components eliminates dozens of stamped parts, but introduces massive CNC finishing of die-cast aluminum, requiring high material-removal rates and robust tool-life models. Suppliers investing in these cells demand software that auto-compensates for tool-wear drift across 20-hour unmanned shifts. In contrast, niche hypercar builders focus on carbon-fiber trim, using 5-axis routers and probe-based path updates each production cycle. Such divergence means one vertical now spans multiple CAM license tiers, ensuring that the Computer Aided Manufacturing market retains depth even if overall car volumes level off.

The Computer Aided Manufacturing Market Report is Segmented by Deployment Model (On-Premises, and Cloud-Based), End-User Industry (Aerospace and Defense, Automotive, Medical Devices, and More), Component (Software, and Services), Manufacturing Process (Milling, Turning, Drilling, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's 47.1% share underscores its manufacturing heft, yet the region still wrestles with CNC protocol fragmentation that complicates plug-and-play interoperability. Chinese policy favors indigenous CAM algorithms tied to homegrown controllers, spurring parallel ecosystems that global vendors must bridge through dual-language post-processors and open-API tool libraries. Japan's machine OEMs integrate CAM directly into control firmware, shortening toolpath load times but locking customers into proprietary stacks. India's Production Linked Incentive schemes subsidize CAM licenses if tied to workforce upskilling, giving vendors a foothold in an emerging mid-market that could rival traditional giants by 2030.

North American users lead in cloud adoption, partly because the CHIPS Act funnels USD 52 billion into regional fabs that require distributed programming sooner than brick-and-mortar capacity is completed. Europe champions energy-efficient machining, mandating compressed-air reduction and tool reuse targets that CAM strategy simulators now model in kilowatt-hours per part. Data-sovereignty rules add friction, but tier-one suppliers accept localized data lakes in exchange for cross-plant optimization algorithms. These regional nuances ensure the Computer Aided Manufacturing market maintains broad diversification, cushioning it against localized downturns.