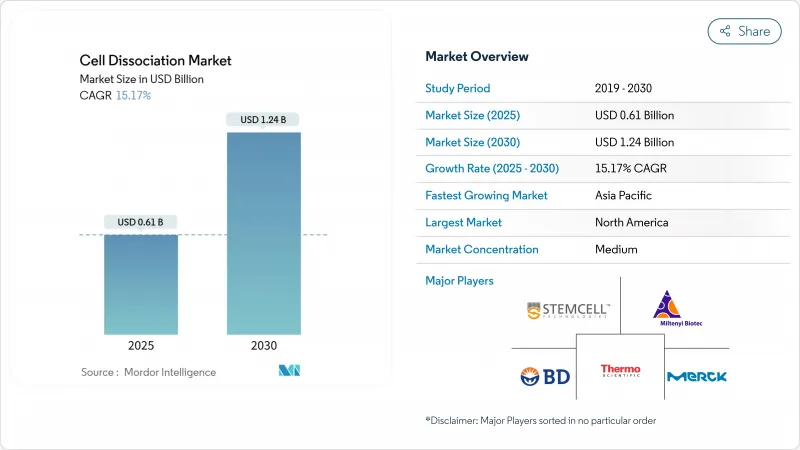

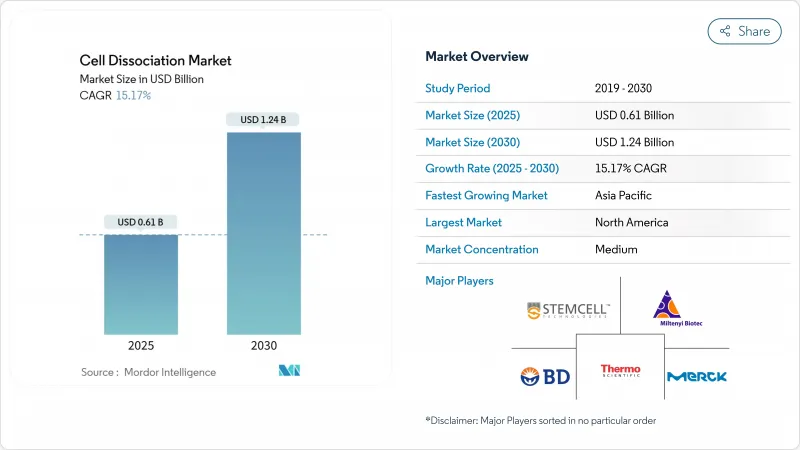

세포 해리 시장 규모는 2025년에 6억 1,000만 달러로 추정되고, 2030년에는 12억 4,000만 달러에 이를 전망이며, CAGR 15.17%로 확대될 것으로 예측됩니다.

이 시장의 상승은 세포 및 유전자 치료 생산, 단일 세포 오믹스, 맞춤형 의료 파이프라인을 가능하게 하는 역할과 연결되어 있습니다. 첨단 치료에 대한 규제 당국의 승인, 자동화의 돌파구, 대규모 공공 생명 공학 자금이 전체로 채용을 가속화하고 있습니다. 제약 회사와 생명 공학 회사는 여전히 주요 구매자이지만 스폰서가 복잡한 작업을 외주함에 따라 개발 업무 수탁 기관(CRO)의 점유율이 증가하고 있습니다. 북미는 확립된 인프라에 의해 리드를 유지하고 있지만, 아시아태평양은 중국, 일본, 인도에서 수십억 달러 규모의 국가 프로그램에 의해 지원되고 급성장하고 있습니다.

2024년에는 7개의 세포 및 유전자 치료제가 FDA의 승인을 취득하고 있으며, FDA는 2025년까지 매년 10-20건의 승인 취득을 전망하고 있습니다. 각 제품에는 첨단 세포 분리 프로토콜이 필요하므로 로트 릴리스 비용을 50% 절감할 수 있는 자동 분리 플랫폼에 대한 수요가 높아지고 있습니다. 고형 종양 및 자가면역 프로그램은 조직 입력을 다양화하고 시약의 품질 및 확장성에 대한 요구를 강화하고 있습니다. 동종이식 포맷은 기증자당 배치량을 더욱 증가시키고 표준화된 GMP 등급 워크플로우의 필요성을 강조합니다.

마이크로플루이딕스 칩은 현재 한 번의 처리로 10만 개 이상의 세포를 처리할 수 있습니다. RNA 무결성을 유지하기 위해 새로운 FixNCut 프로토콜은 해리 전의 가역적 조직 고정을 가능하게 하며 데이터 유출 없이 시료 운송을 용이하게 합니다. 이질성 연구는 생존성이 높은 단세포 현탁액에 의존하기 때문에 종양학 용도에 대한 수요가 대부분을 차지합니다. AI를 활용한 파이프라인은 편차를 최소화하는 표준화된 프로토콜의 추진을 강화하고 있습니다.

완전 자동화된 클로즈드 스위트는 100만 달러를 넘는 경우가 많아 소규모 실험실에서의 도입이 제한됩니다. 세계적인 췌장 효소 부족은 원료 비용과 납기를 더욱 끌어올리고 있습니다. 중국의 CAR-T 현황은 제조 비용 상승이 자기 부담 증가로 이어지는 방법을 보여줍니다.

효소 시약은 2024년에 58.76%의 점유율을 유지했으며, Clostridium histolyticum 유래의 세균성 콜라게나아제가 특이성에서 진중해지고 있습니다. 트립신은 일상적인 계대 배양을 지배하며, 디스파제와 엘라스타제는 틈새 용도 분야에 사용됩니다. 비효소 제제는 단일 세포 워크플로우가 프로테아제 노출을 경원하는 동안 CAGR로 가장 빠른 17.67%로 성장을 지속하고 있습니다. ATCC의 킬레이트제 기반 용액과 재조합 TrypLE는 이러한 규제 친화적인 이동의 예입니다. 자동 조직 해리 장치는 현재 시약 카트리지와 함께 설치되어 운영자의 변동을 최소화합니다.

2024년 시장 점유율은 북미가 38.78%를 차지하였고, FDA에 의한 첨단 치료제의 패스트 트랙 패스가 이를 뒷받침하고 있습니다. 뉴욕의 4억 3,000만 달러의 바이오제네시스 파크는 1,530명의 고용과 새로운 GMP 스위트를 추가했습니다. 캐나다의 STEMCELL Technologies에 2,250만 달러가 투자되어 국내 시약 생산 능력이 확보됩니다. 잘트리우스와 지멘스, 로트 릴리스 시간을 단축하는 디지털 트윈 오토메이션으로 협업하고 있습니다.

아시아태평양은 중국의 41억 7,000만 달러의 바이오파크 계획에 견인되어 CAGR 16.56%로 전진하고 있습니다. 일본의 스타트업 개발 5개년 계획과 고령화 사회의 요구가, 2030년까지 15조 엔의 바이오 테크놀로지 성장을 뒷받침할 전망입니다. 인도의 BioE3 정책은 미국 바이오보안법을 준수하는 공급망의 다양화를 예측하여 지역 CDMO를 세계 공급업체로 자리매김하는 것을 목표로 합니다.

유럽은 7,200억 유로 세계 시장 진입 확대를 목표로 하는 EU 생명공학 전략의 혜택을 누리고 있습니다. 세포 기반 제품에 대한 EMA 지침과 새로운 유럽 약전의 QC 장은 규정을 명확히 합니다. 론자의 네덜란드 공장은 버텍스 사를 위해 CASGEVY를 제조하고 있으며 대량 수탁 제조의 허브로서 유럽의 관련성을 강조하고 있습니다.

The cell dissociation market size is valued at USD 0.61 billion in 2025 and is projected to reach USD 1.24 billion by 2030, expanding at a 15.17% CAGR.

The market's ascent is tied to its enabling role in cell and gene therapy production, single-cell omics, and personalized-medicine pipelines. Regulatory approvals for advanced therapies, automation breakthroughs, and large-scale public biotechnology funding collectively accelerate adoption. Pharmaceutical and biotechnology firms remain the primary purchasers, yet contract research organizations (CROs) capture rising share as sponsors outsource complex tasks. North America keeps the lead owing to established infrastructure, while Asia-Pacific posts the fastest growth backed by multibillion-dollar national programs in China, Japan, and India.

Seven cell and gene therapies secured FDA approval in 2024, and the agency expects 10-20 clearances annually through 2025. Each product requires sophisticated cell-isolation protocols, elevating demand for automated dissociation platforms that can cut lot-release costs by 50%. Solid-tumor and autoimmune programs diversify tissue inputs, intensifying reagent-quality and scalability requirements. Allogeneic formats further raise batch volumes per donor, underscoring the need for standardized, GMP-grade workflow.

Microfluidic chips now process upward of 100,000 cells per run, a step-change from prior capacities. To preserve RNA integrity, new FixNCut protocols enable reversible tissue fixation before dissociation, easing sample transport without data loss. Oncology applications dominate demand as heterogeneity studies rely on high-viability single-cell suspensions. AI-augmented pipelines intensify the push for standardized protocols that minimize variability.

Closed, fully automated suites frequently exceed USD 1 million, limiting adoption among smaller labs. The global pancreatic-enzyme shortage further inflates raw-material costs and delivery times. China's CAR-T landscape shows how high production costs can shift most payments out-of-pocket.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Enzymatic reagents retained 58.76% share in 2024, with bacterial collagenase from Clostridium histolyticum prized for specificity. Trypsin dominates routine passaging, while dispase and elastase service niche applications. Non-enzymatic formulations post the fastest 17.67% CAGR as single-cell workflows shy away from protease exposure. ATCC's chelator-based solution and recombinant TrypLE exemplify this regulatory-friendly shift. Automated tissue dissociators now come bundled with reagent cartridges to minimize operator variability.

The Cell Dissociation Market Report is Segmented by Product (Enzymatic Dissociation Products, and More), Tissue (Connective Tissue, Epithelial Tissue, Muscular Tissue, and More), End-User (Pharmaceutical & Biotechnology Companies, Research & Academic Institutes, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America held 38.78% of market share in 2024, buoyed by FDA fast-track pathways for advanced therapies. New York's USD 430 million BioGenesis Park adds 1,530 jobs and new GMP suites. Canada's USD 22.5 million investment in STEMCELL Technologies ensures domestic reagent capacity. Sartorius and Siemens collaborate on digital-twin automation that trims lot-release time.

Asia-Pacific advances at 16.56% CAGR, led by China's USD 4.17 billion biopark program. Japan's Startup Development Five-Year Plan and aging-society needs push biotech growth toward ¥15 trillion by 2030. India's BioE3 policy aims to position local CDMOs as global suppliers in anticipation of supply-chain diversification from U.S. Biosecure Act compliance.

Europe benefits from the EU biotechnology strategy targeting greater participation in the EUR 720 billion global market. EMA guidelines for cell-based products and new European Pharmacopoeia QC chapters provide regulatory clarity. Lonza's Dutch plant produces CASGEVY for Vertex, underscoring Europe's relevance as a high-volume contract-manufacturing hub.