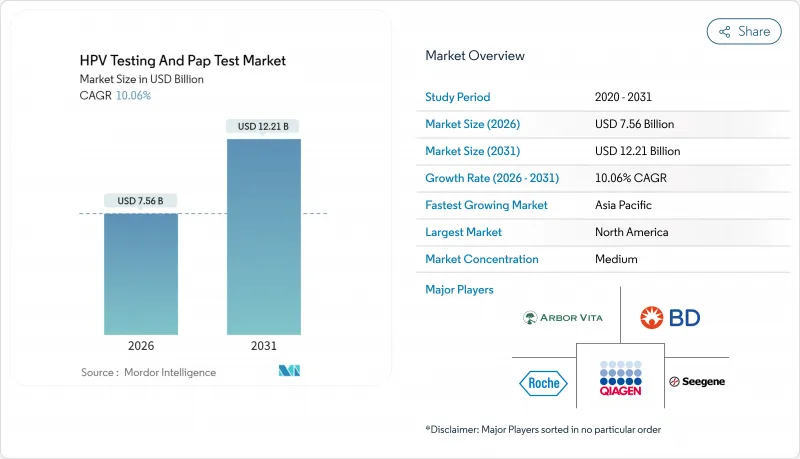

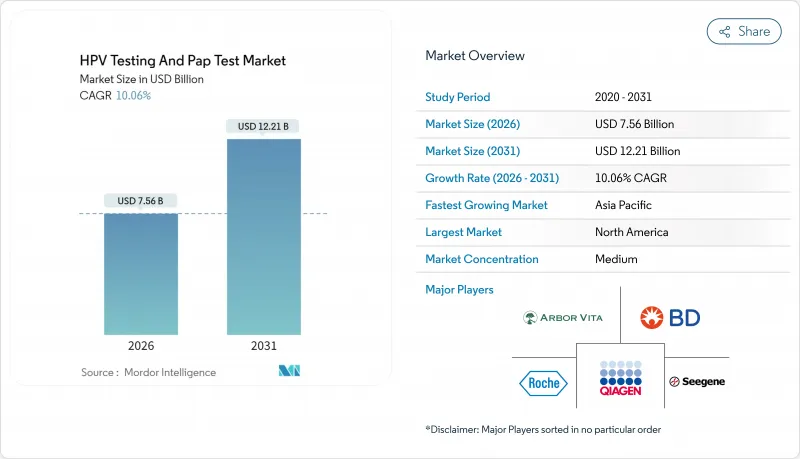

HPV 검사 및 PAP 검사 시장은 2025년에 68억 7,000만 달러로 평가되었고 예측 기간(2026-2031년)동안 CAGR 10.06%로 성장하고, 2026년 75억 6,000만 달러, 2031년까지 122억 1,000만 달러로 성장할 전망입니다.

1차 HPV 스크리닝이 표준치료가 되어, 자기 채취가 규제 당국의 지지를 얻고, 각국 정부가 WHO의 90-70-90 근절 목표에 따라 도입이 가속하고 있습니다. 가이드라인의 급속한 변경, AI를 활용한 세포진단, DNA 메틸화에 의한 트리아지 바이오마커에 의해 검사 정밀도와 검사실 처리 능력이 향상되는 동시에 자원의 제한된 환경에서의 접근 확대를 도모하고 있습니다. HPV 예방접종은 향후 수요의 두드러짐 요인이 될 수 있지만, 많은 지역에서 검진 커버율이 여전히 50% 미만이기 때문에 단기 수요는 여전히 활발합니다. FDA가 2024년에 발표한 실험실 개발 검사(LDT)에 관한 규제는 보다 무거운 컴플라이언스 비용을 부담할 수 있는 벤더를 우대하는 내용이 되어, 업계 재편의 압력이 높아지고 있습니다.

WHO의 2024년 2월 1일자 보도 자료에서는 "2022년 자궁 경부암은 세계에서 66만 1,044건의 신규 사례와 34만 8,186건의 사망을 일으켰다고 명시되어 있습니다. 사하라 이남 아프리카에서는 검진 커버율이 여전히 4%에 그치고, 미치료 환자층이 방대하게 존재하고 있습니다. 중국이 2030년까지 70%의 커버율 달성을 목표로 하는 계획에 따라 4억건의 추가 검사 수요가 발생할 가능성이 있습니다. 인도에서는 2025년에 150만 DALY가 예측되어 연방정부 및 주정부에 의한 검진 시책이 추진되고 있습니다. 이러한 추세는 세포 진단 기반 및 분자진단 분야의 지속적인 수요를 지원합니다.

WHO, ASCCP 및 많은 국가 프로그램은 현재 DNA 기반 HPV 검사를 첫 번째 선택 스크리닝으로 권장합니다. 이는 CIN2에 대한 감도가 95% 이상의 반면, PAP 세포 진단에서는 53%이기 때문입니다. 온타리오에서는 2025년 3월에 팝 검사를 HPV 검사로 대체했습니다. 브리티시컬럼비아 주에서는 2024년 1월 전환 후 몇 개월 동안 2만 5,000건의 자체 스크리닝을 실시했습니다. 이러한 정책 전환은 높은 처리량 PCR 플랫폼에 대한 실험실 투자를 가속화하고 있습니다.

CDC 감시에 따르면 2008년부터 2022년까지 미국 20-24세 여성의 CIN2-3 병변은 79% 감소했습니다. 영국에서는 백신접종군에서 자궁경부암이 83.9% 감소했습니다. 독일에서는 예방접종 후 CIN2 유병률이 51.1% 감소한 것으로 보고되었습니다. 이러한 결과는 특히 고소득 국가에서 장기 검진 대상자 수를 줄였습니다.

HPV 검사는 CAGR 10.88%로 확대되어 세포 진단 검사를 추월할 것으로 예측됩니다. 그러나 2025년 시점에서 PAP 검사는 HPV 검사 및 PAP 검사 시장의 52.78% 점유율을 유지하고 있습니다. HPV 검사 및 PAP 검사 시장 규모는 캐나다, 영국, 호주에서의 정책 의무화에 힘입어 2031년까지 66억 2,000만 달러에 달할 것으로 예측됩니다. 마이그레이션 기간 동안 검사 기관은 이중 워크플로우(동시 검사 및 반사 세포 진단)를 유지합니다.

액체 기반 세포 진단(LBC)은 최소한의 인력 증가로 정확도를 향상시키는 AI 알고리즘의 기반이 되기 때문에 여전히 필수적입니다. PCR 능력이 부족한 자원제약지역에서는 기존 PAP 검사가 계속되지만, 기부금에 의한 PCR 도입 확대에 따라 점감할 전망입니다. 벤더 각 사는 임상가치의 향상과 PAP 검사 건수 감소의 보전을 목적으로 다중 HPV 유전자형 판정 패널을 자리 매김하고 있습니다.

2025년 시점에서 의료 종사자에 의한 자궁경부 검체 채취는 HPV 검사 및 PAP 검사 시장 규모의 68.95%를 차지하고 있지만, 자기 채취는 연률 11.02%로 성장하고 있으며, 2031년까지 같은 수준에 가까워질 가능성이 있습니다. 자기 채취 시장 점유율 확대는 환자의 강한 선호도와 건강 격차 시정의 목표에 지지되고 있습니다.

소변 검체 채취는 원격지역에서의 잠재력을 나타내지만, 임상적 검증은 계속되고 있습니다. 혈액 기반 혈청학 검사는 여전히 틈새 지역이며 주로 역학 연구에 사용됩니다. 의료 제공업체는 우송 검체 채취의 물류, 원격 의료에 의한 동의 취득, 자동 결과 포털을 통합해, 자기 검체 채취의 확대를 지원하고 있습니다.

The HPV Testing and Pap Test market was valued at USD 6.87 billion in 2025 and estimated to grow from USD 7.56 billion in 2026 to reach USD 12.21 billion by 2031, at a CAGR of 10.06% during the forecast period (2026-2031).

Uptake accelerates as primary HPV screening becomes the standard of care, self-collection gains regulatory backing, and governments align with the WHO 90-70-90 elimination targets. Rapid guideline shifts, AI-enabled cytology, and DNA-methylation triage biomarkers improve test accuracy and laboratory throughput while widening access in low-resource settings. HPV vaccination generates future volume headwinds, yet near-term demand remains buoyant because screening coverage in many regions is still below 50%. Consolidation pressure is mounting after the FDA's 2024 rule on laboratory-developed tests, which favors vendors able to shoulder heavier compliance costs.

WHO's February 1, 2024 press release explicitly states: "In 2022, cervical cancer accounted for 661,044 new cases and 348,186 deaths globally. Screening coverage is still 4% in sub-Saharan Africa, creating a large untreated population base. China's plan to reach 70% coverage by 2030 could generate 400 million additional tests. India faces 1.5 million DALYs in 2025, spurring federal and state screening initiatives. These dynamics underpin sustained demand for both cytology-based and molecular diagnostics.

WHO, ASCCP, and many national programs now endorse DNA-based HPV tests as first-line screening because sensitivity exceeds 95% for CIN2+ versus 53% for Pap cytology. Ontario replaced Pap tests with HPV testing in March 2025. British Columbia saw 25,000 self-screens in months after its January 2024 switch. These policy moves accelerate laboratory investment in high-throughput PCR platforms.

CDC surveillance shows CIN2-3 lesions plummeted 79% among U.S. women aged 20-24 between 2008 and 2022. England observed an 83.9% cervical-cancer reduction in vaccinated cohorts. Germany reports a 51.1% drop in CIN2+ prevalence post-immunization. These successes shrink long-term screening pools, especially in high-income countries.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

HPV testing is forecast to grow at an 10.88% CAGR, overtaking cytology even though Pap tests still held 52.78% HPV Testing and Pap Test market share in 2025. The HPV Testing and Pap Test market size for HPV assays is projected to reach USD 6.62 billion by 2031, supported by policy mandates in Canada, U.K., and Australia. Laboratories retain dual workflows, co-testing and reflex cytology, during the transition.

Liquid-based cytology (LBC) remains integral because LBC slides feed AI algorithms that raise accuracy with minimal staffing increases. Conventional Paps persist in resource-constrained geographies lacking PCR capacity but will gradually decline as donor-funded PCR initiatives expand. Vendors position multiplex HPV genotyping panels to increase clinical value and offset falling Pap volumes.

Clinician-collected cervical samples captured 68.95% of HPV Testing and Pap Test market size in 2025, but self-collection is growing 11.02% annually and could approach parity by 2031. The HPV Testing and Pap Test market share for self-collection is buoyed by strong patient preference scores and health-equity objectives.

Urine-based sampling shows promise for remote communities though clinical validation remains ongoing. Blood-based serology is still niche, used primarily in epidemiology. Providers are integrating mail-order logistics, telehealth consent, and automated result portals to support self-sampling scale-up.

The HPV Testing and Pap Test Market Report is Segmented by Test Type (HPV Testing, Pap Test), Sample Collection Method (Clinician-Collected Cervical Sample, and More), Product & Service (Instruments & Analyzers, and More), Application (Cervical Cancer Screening, and More), End User (Hospitals & Surgical Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).