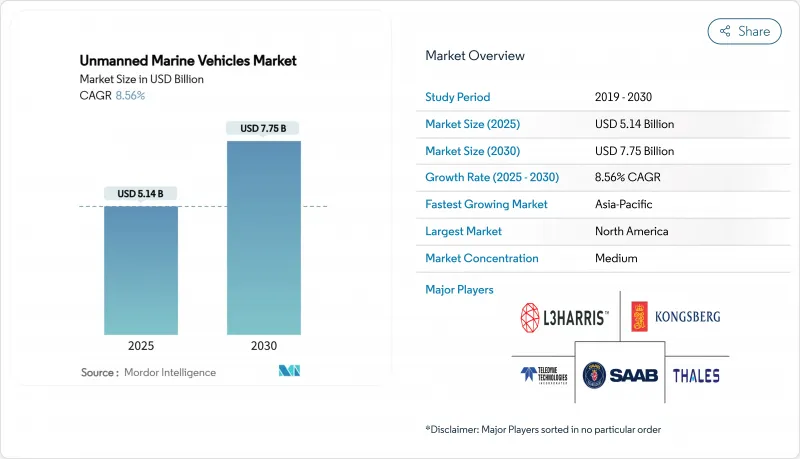

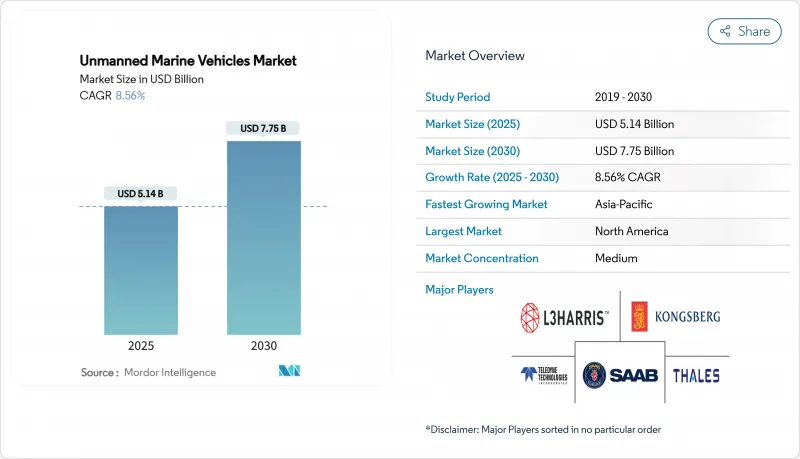

무인 해상 차량 시장 규모는 2025년에 51억 4,000만 달러로 추정되고, 2030년에는 77억 5,000만 달러에 이를 전망이며, CAGR 8.56%로 성장할 것으로 예측됩니다.

이 성장 궤도를 지원하는 것은 해군 근대화 계획의 활성화, 해외 에너지 발자국의 확대, 지속적인 해양 데이터 수집에 대한 수요의 급증입니다. 비클루식 플랫폼은 실험적인 도구에서 방위력의 범위를 넓히고, 석유 및 가스, 풍력 사업자의 검사 비용을 낮추며, 장기적인 기후 변화 미션의 범위를 넓히는 필수적인 자산으로 이행하고 있습니다. 지정학적 갈등이 격화되면 스텔스 해저 시스템의 조달에 박차가 걸려 지속가능성의 의무화에 의해 저배출 가스 파워트레인으로의 축족이 가속합니다. 벤처캐피탈의 지원을 받은 신흥기업은 방위 프라임이 지배하는 분야에 신속한 반복 문화를 주입하고, 보다 신속한 프로토타입 사이클을 가능하게 하고, 보다 소형의 스웜 캐퍼블 크래프트의 2자리수 오더북을 추진합니다. 에코시스템 참가자들은 소프트웨어 오토노미 알고리즘과 데이터 퓨전 엔진이 차세대 함대에 있어 결정적인 차별화 요인이 된다는 견해를 강화하고 있습니다.

해상 긴장이 증가함에 따라 해군은 분쟁 해역에서 커버 갭을 메우는 고급 무인 함대에 자금을 투입하게 됩니다. 미국 해군은 2025 회계 연도에 무인 시스템에 1억 7,730만 달러의 예산을 계상해, 자율형 해중정의 대량 생산을 목표로 하는 '레플리칸트' 구상을 내세우고 있습니다. 앤드릴의 로드아일랜드 공장은 현재 연간 200대 이상의 Dive-LD를 생산하고 있습니다. 호주 고스트 상어와 인도 XLUVUV 입찰과 같은 동시 프로그램은 여러 지역의 조달 파도를 강화합니다. 프랑스 해군 그룹의 무인 항공기 증명기에는 유럽 연계를 볼 수 있습니다. 흑해 전투 성공 사례는 운영 개념을 검증하고 획득 일정을 단축합니다.

에너지 메이저는 현재 자율형 수중탐사기(AUV)를 도입하고 있어 검사에 드는 경비를 연결식 ROV에 비해 최대 55% 삭감하고 있습니다. TotalEnergies의 원격 조작 로봇의 시험 운영은 오프쇼어 인력을 줄이는 육상 명령 허브로의 이동을 보여줍니다. AUV는 이상 감지를 가속화하고 건조 도크 간격을 줄이며 환경 풋 프린트를 반 줄이기 위해 걸프 운영자와 북해 계약자는 예지 보전을 위해 디지털 트윈을 뒷받침하도록 촉구하고 있습니다. 아랍에미리트(UAE)의 재생에너지로 움직이는 비승조형 수상 선박은 탈탄소화 목표 및 자동화 효율성을 융합시키고 있습니다. DNV의 Solitude와 같은 개념 연구는 완전 무인 부체형 LNG 유닛이 20%의 운영 비용 절감을 실현한다고 가정합니다.

대형 무인 수상 차량의 가격은 선체 1척 당 2억 5,000만 달러에 달하며, 미 해군 XLUV 프로그램만으로도 2025년도에 2,150만 달러의 예산이 됩니다. 수소연료전지 AUV의 컨셉은 배출 가스를 배제하지만 특주 연료 보급이 필요하며 초기 예산이 부풀어 오릅니다. 노티쿠스 로보틱스는 2023년에 5,070만 달러의 손실을 기록해 획기적인 해저 모핑 플랫폼의 투자 회수 기간이 장기화되고 있음을 부각하고 있습니다. Blue Water Autonomy의 1,400만 달러의 시드 자금과 같은 벤처 라운드는 이른 무대의 혁신자가 첫 수익을 얻기 전에 올라가야 하는 어려운 자본 사다리를 강조합니다.

무인 잠수기(UUV)는 2024년 무인 해상 차량 시장 점유율의 54.21%를 유지했고, 2030년까지 연평균 복합 성장률(CAGR) 11.17%로 가장 높은 성장이 전망되며, 이 분야의 성장과 수익의 양륜으로서의 역할을 확고히 하고 있습니다. 수요는 대잠수함전 업그레이드와 심해 인프라 점검에서 솟아오르고 중국 태풍에 강한 '시로나가스 고래'는 30일간의 잠수 내구성 벤치마크를 보여줍니다.

수상 차량은 무인 해상 차량 시장의 밸런스를 흡수하고 있지만, 해안 감시, 기뢰 대책, 물류의 견인역이 되고 있습니다. 미국의 하이브리드 함대 모델은 지속적인 수상 순찰을 활용하여 비밀리의 해중 자산을 보완합니다. 컨버전스 동향은 잠수함 발사형 UAV와, 종래의 미션 닥트린을 바꾸는 수상 및 수중 합동 임무를 나타내고 있습니다.

중형기는 페이로드와 내구성의 균형을 맞춘 프로파일에 의해 2024년 매출의 31.34%를 확보했는데, 초소형기는 군 로봇 공학과 배리어 프리 발사 요건에 밀려 CAGR 10.01%로 약진합니다. 소형 노드는 소모 위험을 최소화하면서 연안 지역을 종합적으로 커버할 수 있습니다.

모듈 디자인은 규모에 맞지 않는 섀시를 실현하고 해상에서 미션 팩을 교체하여 크기 경계를 모호하게 만듭니다. 소프트 머티리얼 슬러스터와 압전 액추에이션이 좁은 파이프라인과 암초의 틈새에서의 조종성을 연마합니다. 사이프러스의 스웜 기반 인공 산호초 모니터링은 한 달 동안 무인 전개를 검증하고 조사선을 전세하지 않고 생물 다양성에 대한 인사이트를 넓혔습니다.

북미는 2024년 매출의 33.27%를 차지했으며, 국방부의 수십억 달러 규모의 선대 재편과 150피트의 마로다 무인정찰기를 제조하는 살로닉의 루이지애나 조선소와 같은 벤처 자금에 의한 스케일 업에 지지되고 있습니다. 캐나다의 북극권 프로그램과 멕시코의 심해 캄페체 검사는 수요 루프를 증가시킵니다. 이 지역은 성숙한 방위 산업 기반, 인공지능 인적 자원 수영장, 조기 어댑터 규제의 샌드 박스화로 혜택을 받고 있습니다.

아시아태평양은 중국의 함대 증강, 호주 AUKUS와 연동한 Ghost Shark의 프로토타입, 인도가 해상 영역 인식을 확장하는 12대의 XLUV의 입찰을 실시함으로써 10.40%의 연평균 복합 성장률(CAGR)을 기록했습니다. 우크라이나에서 USV를 공동 생산하는 노르웨이의 결정을 포함한 공동 프로젝트는 더 넓은 인도 태평양 사분 엔 전체에 기술의 분산이 증가하고 있음을 보여줍니다.

유럽은 통합 조선 클러스터와 통합된 연구 개발 자금을 활용하여 자율 시험의 견고한 파이프라인을 유지하고 있습니다. EU의 AI법은 규제 측면에서 선행자 이익을 초래할 수 있는 하모나이제이션의 선례를 보여줍니다. 영국은 기뢰소해 패키지에 대한 Kongsberg Vanguard 마더십을 평가하고 프랑스의 Naval Group은 대구경선형에서 대륙의 전문지식을 정착시킵니다.

The unmanned marine vehicles market size is estimated at USD 5.14 billion in 2025 and is expected to reach USD 7.75 billion by 2030, advancing at an 8.56% CAGR.

Heightened naval modernization programs, an expanding offshore energy footprint, and surging demand for persistent ocean-data collection underpin this growth trajectory. Uncrewed platforms are shifting from experimental tools to indispensable assets that extend the reach of defense forces, lower inspection costs for oil, gas, and wind operators, and widen the scope of long-duration climate missions. Intensifying geopolitical flashpoints spur procurement of stealthy undersea systems, while sustainability mandates accelerate the pivot toward low-emission powertrains. Venture-capital-backed start-ups inject rapid-iteration culture into a field dominated by defense primes, enabling faster prototype cycles and driving double-digit order books for smaller, swarm-capable craft. Ecosystem participants increasingly view software-autonomy algorithms and data-fusion engines as the decisive differentiator for next-generation fleets.

Escalating maritime tensions drive navies to bankroll sophisticated unmanned fleets that plug coverage gaps in contested waters. The US Navy budgeted USD 177.3 million for uncrewed systems in fiscal 2025, with the Replicator initiative targeting mass production of autonomous undersea craft. Anduril's Rhode Island plant can now roll out more than 200 Dive-LD vehicles annually. Parallel programs such as Australia's Ghost Shark and India's XLUUV tender reinforce a multi-regional procurement wave. European alignment is visible in France's Naval Group drone demonstrators, underpinning future cooperative under-ice operations. Combat success stories from the Black Sea validate operational concepts and compress acquisition timelines, while Taiwan and Norway expand indigenous production to address local threat matrices.

Energy majors now deploy autonomous underwater vehicles (AUVs) that slice inspection outlays by up to 55% compared with tethered ROVs. TotalEnergies' pilot of remotely controlled robots illustrates the shift toward onshore command hubs that cut offshore headcount. AUVs accelerate anomaly detection, shorten dry-dock intervals, and halve environmental footprints, prompting Gulf operators and North Sea contractors to retrofit digital twins for predictive maintenance. Renewable-powered uncrewed surface vessels in the UAE merge decarbonization goals with automation efficiencies. Conceptual studies such as DNV's Solitude envisage fully unmanned floating LNG units realizing 20% operating-cost savings.

Price tags for large uncrewed surface vehicles reach USD 250 million per hull, while the US Navy's XLUUV program alone will draw USD 21.5 million in FY 2025. Hydrogen-fuel-cell AUV concepts eliminate emissions but demand bespoke bunkering and inflate upfront budgets. Nauticus Robotics posted a USD 50.7 million loss in 2023, underscoring the protracted payback period for breakthrough subsea morphing platforms. Venture rounds such as Blue Water Autonomy's USD 14 million seed highlight the steep capital ladder that early-stage innovators must climb before first revenue.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Unmanned underwater vehicles (UUVs) retained 54.21% of the unmanned marine vehicles market share in 2024 while also logging the highest 11.17% CAGR through 2030, cementing their role as the sector's dual growth and revenue engine. Demand springs from anti-submarine warfare upgrades and deep-water infrastructure inspection, with China's typhoon-proof Blue Whale illustrating 30-day submerged endurance benchmarks.

Surface vehicles absorb the balance of the unmanned marine vehicles market but gain traction for coastal surveillance, mine countermeasures, and logistics. The United States' hybrid fleet model exploits persistent surface patrols to complement covert undersea assets. Convergence trends show submarine-launched UAVs and joint surface-subsurface tasking that rewrite traditional mission doctrines.

Medium craft secured 31.34% of 2024 revenue thanks to balanced payload-endurance profiles, yet micro vehicles sprint ahead at 10.01% CAGR, propelled by swarm robotics and barrier-free launch requirements. Compact nodes enable blanket coverage of littoral zones while minimizing attrition risk.

The modular design allows a scale-agnostic chassis where mission packs swap in at sea, blurring size boundaries. Soft-material thrusters and piezoelectric actuation sharpen maneuverability in confined pipelines and reef crevices. Swarm-based artificial reef monitoring in Cyprus validates month-long untended deployments, expanding biodiversity insights without research-vessel charters.

The Unmanned Marine Vehicles Market Report is Segmented by Vehicle Type (Unmanned Surface Vehicles (USVs), and Unmanned Underwater Vehicles (UUVs)), Vehicle Size (Micro, Small, and More), Propulsion (Diesel, Electric, and More), Control Type (Remotely Operated and Autonomous), Application (Defense and Security, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 33.27% of 2024 revenue, underpinned by the Pentagon's multi-billion-dollar fleet recapitalization and venture-financed scale-ups such as Saronic's Louisiana shipyard producing 150-foot Marauder drones. Canada's Arctic programs and Mexico's deep-water Campeche inspections add incremental demand loops. The region benefits from a mature defense industrial base, AI talent pools, and early-adopter regulatory sandboxing.

Asia-Pacific registers the steepest 10.40% CAGR thanks to China's fleet buildup, Australia's AUKUS-linked Ghost Shark prototypes, and India's tender for 12 XLUUVs that extend maritime domain awareness. Collaborative projects, including Norway's decision to co-produce USVs in Ukraine, signal rising technology dispersion throughout the wider Indo-Pacific quadrant.

Europe leverages integrated shipbuilding clusters and cohesive R&D funding to sustain a robust pipeline of autonomous trials. The EU AI Act sets harmonization precedents that may translate into first-mover regulatory advantages. The United Kingdom evaluates Kongsberg Vanguard motherships for mine-hunting packages, while France's Naval Group anchors continental expertise in large-diameter hull forms.