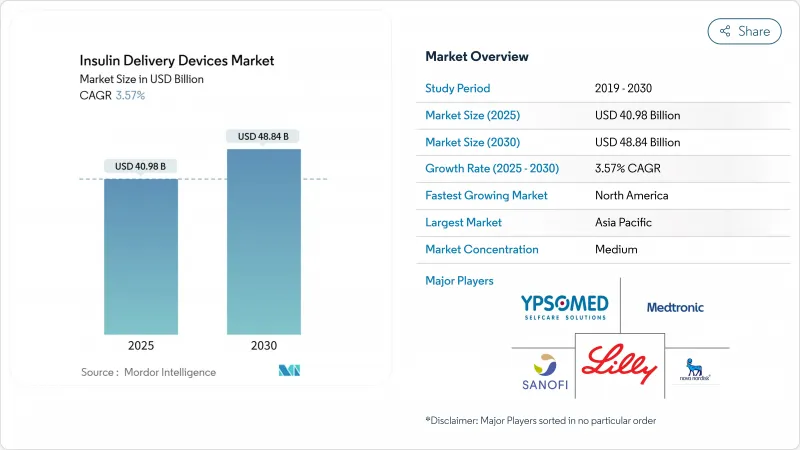

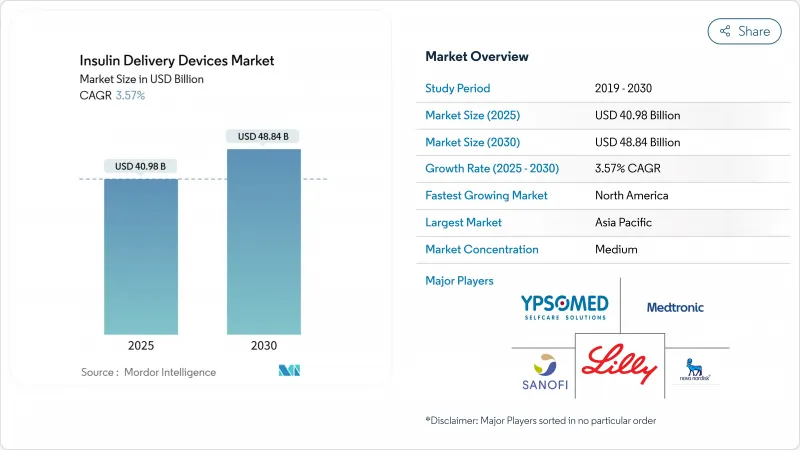

인슐린 투여 기기 시장 규모는 2025년에 409억 8,000만 달러로 추정되고, 2030년에는 488억 4,000만 달러에 이를 전망이며, CAGR 3.57%로 성장할 것으로 예측됩니다.

이러한 완만한 성장은 자동 인슐린 전달 생태계, 스마트 패치 펌프, 앱 대응 투여 지침 플랫폼 등 당뇨병 치료를 혁신하는 급속한 기술 혁신을 배경으로 합니다. 세계 당뇨병 유병률은 1990년의 7%에서 2022년에는 14%로 급상승하고 있으며, 대응 가능한 환자층은 계속 확대되고 있습니다. 한편 CMS는 2026년부터 메디케어 파트D에 35달러의 인슐린 상한을 마련할 것을 제안하고 있으며, 미국 수요는 더욱 확대되고 있습니다. 원격 모니터링이 임상적으로 효과적이고 비용 효율적임이 입증되었으며, 제조업체가 자체 관리가 용이하도록 제품을 조정할 수 있게 됨에 따라 가정 의료가 장비 보급의 축이 되고 있습니다. 북미의 상환 주도권이 신형 시스템의 조기 도입을 지원하고 있지만, 규제 당국이 현지제 펌프와 펜의 인가를 합리화함에 따라 아시아태평양이 가장 빠른 수량 증가에 기여하고 있습니다.

성인 당뇨병 환자 수는 1990년 이후 4배로 증가했으며, 2022년에는 8억 명을 넘었습니다. 역학자들은 이 수치가 2025년에는 13억 1,000만 명에 달할 것으로 예상하고 있으며, 인슐린 투여 기기 시장에 지속적인 수요를 창출하고 있습니다. 2형 당뇨병은 현재 환자의 96%를 차지하고 있으며, 제조업체는 더 용량이 큰 저장소와 후기 경구에서 인슐린으로의 전환에 적합한 간편한 인터페이스를 구축하도록 촉구하고 있습니다. 아시아태평양은 가장 무거운 부담을 겪고 있지만, 중저소득국가는 아직 치료되지 않은 사례의 90%를 차지하고 있으며, 자동화된 저비용 납품 형태에 큰 여백이 있는 것으로 밝혀지고 있습니다. 따라서 장비 제조업체는 변화하기 쉬운 기후, 간헐적인 전력 및 제한된 임상 지원을 견딜 수 있는 신뢰할 수 있는 웨어러블을 선호합니다.

블루투스 모듈, 모바일 앱, 미스 도즈 경고를 갖춘 스마트 펜은 환자가 매일 루틴에 맞는 눈에 띄지 않는 도구를 요구하게 되어 주류가 되고 있습니다. 메드트로닉의 2024년 FDA가 승인한 InPen 업그레이드에서는 수정 투여가 권장되고 볼러스가 자동으로 기록됩니다. 이러한 기술 혁신은 GLP-1 수용체 작용제가 인슐린을 빼고 약국에서 3번째로 많이 처방되는 당뇨병 치료제가 되었을 때 관찰된 복약 준수의 저하에 대항하는 것입니다. 의료 제공자는 앱 연동 펜을 펌프 요법을 망설이는 2형 환자를 위한 실용적인 브리지 역할로 간주하고 있으며, 성숙 시장에서도 신흥 시장에서도 판매량을 가속화하고 있습니다.

펌프 시스템은 소모품을 포함하면 연간 10,000달러를 초과할 수 있으며 주사기 기반 요법을 능가하고 가격에 민감한 경제권에서의 보급을 제한하고 있습니다. 메디케어에서는 일회용 패치 시스템이 파트D로 처리되지만, 내구성 있는 펌프는 파트B로 분류되기 때문에 액세스 격차가 발생합니다. 중국에서는 인슐린 양에 따른 조달로 약가가 떨어졌지만 하드웨어에는 적용되지 않고 선진 의료기기 가격은 평균 가계를 크게 웃돌고 있습니다. 지불자는 가치 기반 계약을 테스트하고 있지만 채택은 완만하며 가격은 중기적으로 인슐린 투여 기기 시장의 발판이 되었습니다.

인슐린 펌프는 2024년의 매출 점유율 44.56%를 차지했으며, 인슐린 투여 기기 시장의 최대 슬라이스가 되고 있습니다. 그러나 스마트 패치 펌프는 튜브를 없애고 미용적인 매력을 높이기 위해 2030년까지 CAGR 5.67%로 성장할 전망입니다. 펌프로 인한 인슐린 투여 기기 시장 규모는 하이브리드 폐쇄 루프 알고리즘이 표준화됨에 따라 더욱 확대될 것으로 예측됩니다. 이와 병행하여, 재사용 가능한 펜은 복용량 포착 팁을 통합하고, 제트 주사기는 주사 바늘을 싫어하는 사용자를 수용하며 장치의 다양성을 유지합니다.

첨단 웨어러블은 기본 조정을 자동화하고 식사 시의 볼싱을 간소화함으로써 사용자의 신뢰성을 높입니다. Embecta사의 FDA 승인 300단위 일회용 패치는 고용량 2형 처방용 전용 설계를 나타내고, Tandem사의 t:slim X2는 성인 코호트에서 86%의 만족도를 보고하고 있습니다. MDPI가 발표한 임상시험에서는 자동펌프 플랫폼과 센서 부착 펜을 비교했을 경우, 펌프를 사용하는 쪽이 투여 가능한 시간이 긴 것이 확인되고 있어, 의사는 치료의 초기 단계에서 펌프를 추천하게 되어 있습니다.

2024년 인슐린 투여 기기 시장 점유율의 62.45%를 딜리버리 하드웨어가 차지했는데, 소모품은 2030년까지 연평균 복합 성장률(CAGR) 5.45%로 성장을 가속할 전망입니다. 주입 세트, 저장소, 바늘 카트리지는 투자자에게 매력적인 연금과 같은 수익원을 형성합니다. 또한 항균 코팅은 감염 위험을 줄입니다.

제조업체 각사는 소모품 포트폴리오를 활용해 고객과의 관계를 견고하게 하고 있습니다. 인슬릿은 현재 판매의 대부분을 옴니팟 컨트롤러 전용으로 하는 포드의 정기적인 출하에서 얻고 있습니다. 패치 펌프는 리저버와 캐뉼라를 하나의 유닛에 통합하여 컨트롤러의 선행 가격이 하락하더라도 환자 1인당 소모품 지출을 확대합니다. ScienceDirect에 게재된 재료 과학의 진보는 긴 장착 기간 동안 탄력성을 유지하는 실리콘 하이드로겔 블렌드를 보여 주며 일회용 의료에서의 혁신을 강조하고 있습니다.

북미는 2024년에 35.78%의 점유율을 획득했으며, 지역별로 가장 높은 매출을 기록했습니다. 2026년에 도래할 CMS의 인슐린 상한은 접근을 확대할 것으로 예상되며, 인슐릿, 탠덤, 메드트로닉은 각각 2025년에 2자리 단위 성장을 달성했습니다. 캐나다의 1인 친구제는 전국적인 CGM 전개에 자금을 제공하고, 멕시코의 세그로 파퓰러 개혁은 일부 인슐린 펜을 환불해, 대륙의 유저 베이스를 서서히 확대하고 있습니다.

유럽에서는 독일, 프랑스 및 북유럽 상환 기관이 하이브리드 폐쇄 루프 시스템을 승인했기 때문에 한 자리 대 중반의 견조한 확대를 보이고 있습니다. Inslett의 Omnipod 5는 2025년 이탈리아, 덴마크, 핀란드, 노르웨이, 스웨덴에 도입되어 멀티센서 호환성이 보급을 가속화하는 방법을 보여줍니다. EMA에 의한 범유럽 정합화는 임상 증거 제출을 간소화하고, 제조업체는 예측 가능한 일정으로 시장 출시를 어긋나게 할 수 있습니다. 예방의료의 의무화로 임상의사는 저혈당의 긴급 사태를 줄이는 결과 지향의 기술을 채용하게 되어, 인슐린 투여 기기 시장에서는 상호 운용 가능한 생태계에 대한 수요가 높아집니다.

아시아태평양은 CAGR 4.67%로 세계에서 가장 빠르게 진행되고 있으며, 중국, 인도, 일본이 스크리닝 및 치료 프로그램을 강화하고 있습니다. 중국의 NMPA는 2024년에 전년대비 11% 증가한 61개의 혁신적인 의료기기를 승인하고 정책 기세를 나타내고 있지만, 중국의 1형 환자에서의 펌프의 보급률은 비용면에서의 우려로 인해 11.4%에 그쳤습니다. 인도에서는 고용주 보험 확대 및 인슐린 펜의 현지 조립으로 가격이 인하되었습니다. 일본의 가이드라인에서는 소아 환자에게 하이브리드 클로즈드 루프의 도입을 추천하게 되어, 페이어에 의한 상환이 개시되어, 견조한 판매 대수의 성장을 지지하고 있습니다. 그럼에도 불구하고, 소득의 현저한 분산과 분단된 배송 인프라가 여전히 농촌 지역에서의 균일한 보급을 방해하고 있으며, 눈앞의 판매 개수에 상한을 부과하고 있습니다.

The insulin delivery devices market size generated USD 40.98 billion in revenue in 2025 and is projected to reach USD 48.84 billion by 2030, advancing at a 3.57% CAGR.

This moderate headline growth conceals rapid technological change fueled by automated insulin delivery ecosystems, smart patch pumps, and app-enabled dose-guidance platforms that together reframe diabetes therapy. A sharp rise in global diabetes prevalence-from 7% in 1990 to 14% in 2022-continues to widen the addressable patient pool, while CMS's proposed USD 35 insulin cap for Medicare Part D from 2026 further expands U.S. demand. Home-based care now anchors device adoption as remote monitoring proves clinically effective and cost-efficient, prompting manufacturers to tailor products for easy self-management. North American reimbursement leadership sustains early uptake of novel systems, but Asia-Pacific contributes the fastest incremental volumes as regulatory agencies streamline approvals for locally made pumps and pens.

Adult diabetes cases quadrupled since 1990 to exceed 800 million in 2022, and epidemiologists expect the figure to climb to 1.31 billion by 2025, creating sustained demand for the insulin delivery devices market. Type 2 diabetes now represents 96% of cases, prompting manufacturers to build higher-capacity reservoirs and simplified interfaces that suit late-stage oral-to-insulin transitions. Asia-Pacific bears the heaviest burden, yet low- and middle-income countries still account for 90% of untreated cases, revealing significant white-space for automated and low-cost delivery formats. Device makers therefore prioritize reliable wearables that tolerate variable climates, intermittent electricity, and limited clinical support.

Smart pens equipped with Bluetooth modules, mobile apps, and missed-dose alerts have moved mainstream as patients seek discreet tools that fit daily routines. Medtronic's 2024 FDA-cleared InPen upgrade now recommends corrective doses and records boluses automatically. Such innovations counter adherence declines observed when GLP-1 receptor agonists overtook insulin as the third most-dispensed diabetes medication in pharmacies. Healthcare providers view app-linked pens as a pragmatic bridge for type 2 patients hesitant to adopt pump therapy, accelerating unit volumes in both mature and emerging markets.

Fully featured pump systems can exceed USD 10,000 per year when disposables are included, dwarfing syringe-based regimens and limiting uptake in price-sensitive economies. Insurance coverage remains patchy; Medicare treats disposable patch systems under Part D but classifies durable pumps under Part B, causing access disparities. China's volume-based insulin procurement lowered drug prices yet has not extended to hardware, leaving advanced devices priced well above average household health budgets. Payers are testing value-based contracts but adoption is gradual, keeping price a medium-term drag on the insulin delivery devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Insulin pumps held 44.56% revenue share in 2024, anchoring the largest slice of the insulin delivery devices market. However, smart patch pumps are on track for a 5.67% CAGR to 2030 as they eliminate tubing and boost cosmetic appeal. The insulin delivery devices market size attributable to pumps is poised to widen further as hybrid closed-loop algorithms become standard. In parallel, reusable pens integrate dose-capture chips, and jet injectors court needle-averse users, preserving device plurality.

Advanced wearables strengthen user confidence by automating basal adjustments and simplifying mealtime bolusing. Embecta's FDA-cleared 300-unit disposable patch illustrates purpose-built engineering for high-dose type 2 regimens, while Tandem's t:slim X2 reports 86% satisfaction across adult cohorts. Clinical trials published by MDPI confirm greater time-in-range with automated pump platforms versus sensor-augmented pens, prompting physicians to recommend pumps earlier in therapy journeys.

Delivery hardware accounted for 62.45% of insulin delivery devices market share in 2024, yet consumables will accelerate at a 5.45% CAGR through 2030. Infusion sets, reservoirs, and needle cartridges form an annuity-like revenue stream attractive to investors. Extended-wear cannulas reduce insertion frequency, lifting adherence and lowering total cost of care, while antimicrobial coatings cut infection risk.

Manufacturers leverage consumables portfolios for sticky customer relationships; Insulet now derives a majority of sales from recurring pod shipments that pair exclusively with Omnipod controllers. Patch pumps integrate reservoir and cannula in one unit, expanding per-patient consumable spend even as upfront controller prices moderate. Material-science advances profiled in ScienceDirect show silicone-hydrogel blends that maintain elasticity over longer wear periods, underscoring innovation in disposables.

The Insulin Delivery Devices Market Report is Segmented by Device Type (Insulin Pumps, Insulin Pens, and More), Component (Delivery Devices and Consumables), End-User (Hospitals & Clinics, and More), Distribution Channel (Hospital Pharmacies, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated the highest regional revenue with 35.78% share in 2024 as broad insurance coverage, early technology adoption, and sophisticated clinical pathways underpin rapid pump and CGM uptake. The CMS insulin cap arriving in 2026 is expected to widen access, while Insulet, Tandem, and Medtronic each delivered double-digit unit growth in 2025. Canada's single-payer structure funds national CGM rollouts, and Mexico's Seguro Popular reforms now reimburse select insulin pens, incrementally enlarging the continent's user base.

Europe shows solid mid-single-digit expansion as reimbursement agencies in Germany, France, and the Nordics approve hybrid closed-loop systems. Insulet's Omnipod 5 entered Italy, Denmark, Finland, Norway, and Sweden in 2025, illustrating how multi-sensor compatibility accelerates adoption. Pan-European harmonization through EMA simplifies clinical evidence filings, letting manufacturers stagger market launches with predictable timelines. Preventive-care mandates push clinicians to adopt outcome-oriented technologies that reduce hypoglycemia emergencies, reinforcing demand for interoperable ecosystems in the insulin delivery devices market.

Asia-Pacific is advancing at a 4.67% CAGR, the fastest worldwide, as China, India, and Japan ramp screening and treatment programs. China's NMPA approved 61 innovative medical devices in 2024, up 11% year-on-year, signaling policy momentum, though pump penetration among Chinese type 1 patients remains 11.4% due to cost concerns. India benefits from expanding employer insurance and local assembly of insulin pens, trimming prices. Japanese guidelines now recommend hybrid closed-loop adoption for pediatric patients, unlocking payer reimbursement, and supporting robust volume growth. Nevertheless, marked income dispersion and fragmented delivery infrastructure still hinder uniform adoption across rural zones, imposing a ceiling on near-term unit sales.