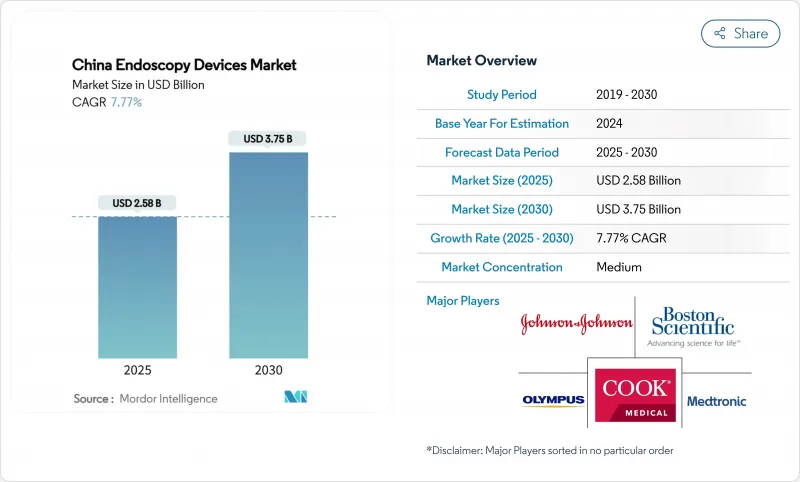

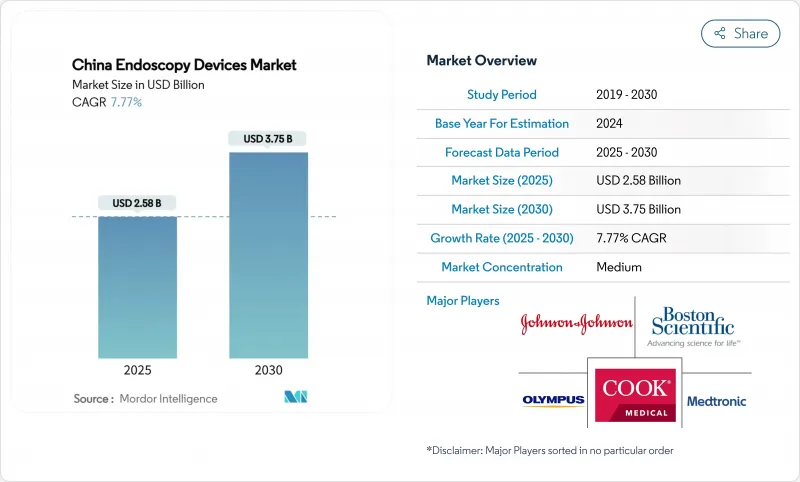

중국의 내시경 검사 기기 시장의 2025년 시장 규모는 25억 8,000만 달러로 추정되고, 2030년에는 37억 5,000만 달러에 이를 전망이며, CAGR 7.77%로 확대될 것으로 예측됩니다.

2050년까지 국민의 26%가 65세 이상이 되는 고령화 사회 및 조기 발견과 폭넓은 검사 접근을 의무화하는 국가적인 암 억제 목표가 성장을 지지하고 있습니다. 4K/3D/AI 가시화 플랫폼의 급속한 보급, 단회 사용 스코프로의 시프트, 저침습 절차에 대한 보험 적용 확대가 수요를 강화하고 있습니다. '메이드 인 차이나 2025'의 국산화 목표에 따라 국내 혁신자들은 생산량을 확대하고 수입 모델의 오랜 우위를 침식하고 있습니다. 3차 병원의 설비투자 및 트레이닝 전용 허브에 대한 투자도 병행하여 이루어져, 수술의 병목이 완화되는 한편, 국가의료제품관리국(NMPA)은 하이테크 시스템의 인가를 가속시키고 있습니다. 중국 내시경 검사 기기 시장에는 하드웨어, 소프트웨어, 애프터 서비스 등 다층 비즈니스 기회가 존재합니다.

소화기 질환은 중국의 인구 역학이 후기 고령자로 이동함에 따라 증가하고 있습니다. 80세 이상의 노인에서는 이미 40.2%가 다질환 합병증을 앓고 있습니다. 정부가 자금을 제공하는 스크리닝의 시험적 이행은 비용 대비 효과 증분비가 1QALY당 1,343달러로 낮고, 대규모의 전개가 재정적으로 가능하다는 것을 확인했습니다. 이러한 경제성은 일반 시민의 의식 향상 캠페인과 함께 중국 내시경 검사 기기 시장 내 대장 내시경 검사 및 EGD 검사실에서 안정적인 처리 능력을 뒷받침하고 있습니다.

인공지능 엔진은 수작업에 의한 독영에 비해 병변 검출을 95.9%까지 높이면서 캡슐 독영 시간을 89.3% 단축하고 있습니다. MONARCH 플랫폼과 같은 로봇 기관지경 시스템은 말초 결절까지 도달 범위를 넓히고 치료 적응을 확대합니다. 통합형 3D 4K 형광 유닛은 깊은 지각, 초고화질, 실시간 관류 평가를 결합하여 종양 단단을 개선합니다. 실험적인 라만 대응 범위는 생검 없이 조직학 수준의 인사이트를 약속하고 정밀 진단의 다음 프론티어를 보여줍니다. 이러한 혁신은 임상 기대를 높이고 중국 내시경 검사 기기 시장 전체의 장비 업데이트 사이클을 가속화합니다.

로봇과 형광 유닛의 자본 가격은 여전히 높습니다. 한 대형 멀티포트 수술용 로봇은 보급을 촉진하기 위해 할인되었지만 연간 도입 대수는 30% 가까이 감소했습니다. 연간 서비스 계약, 수리비, 집중적인 트레이닝 등, 보이지 않는 경비가 부피, 예산에 제약이 있는 병원은 도입에 밟히지 않습니다. 현지 신흥 벤더의 경쟁력 있는 가격 설정이 장벽을 낮추고 있지만, 국제적인 비용 구조에 대한 완전한 수렴은 중국의 내시경 검사 기기 시장에서 여전히 수년간 앞서 있습니다.

2024년 매출 점유율은 플렉서블 기기가 48%를 차지했으며, 일상적인 소화기, 기관지, 이비인후과 수술을 통해 중국 내시경 검사 기기 시장을 지원합니다. 하지만 로봇 지원 시스템은 2030년까지 연평균 복합 성장률(CAGR)이 14.7%로 가장 빠른 성장을 보일 전망입니다. 고해상도 이미지, 촉각 피드백, 클라우드 분석은 특히 말초 폐 결절과 복잡한 비뇨기 병변으로 인해 일찍의 실험 프로토타입을 일상 사용 자산으로 바꾸고 있습니다.

각 제조업체는 형광, 3D 시각화 및 딥러닝에 의한 병리 예측을 로봇 암에 직접 통합하여 진단 및 치료 사이클을 단축하고 있습니다. 기도 관리를 위한 단일 사용 플렉서블 로봇도 평가 중이며 감염 제어의 장점과 기계적 안정성을 결합합니다. 이러한 기술 혁신이 진행됨에 따라 로봇 플랫폼의 중국 내시경 검사 기기 시장 규모는 기존의 카테고리를 능가하게 될 것이지만, 일회용 스코프에 의한 에코시스템은 대량의 환자를 진료하는 호흡기 클리닉에서는 불가결한 존재로 계속될 것으로 보입니다.

소화기 영역은 2024년 시장 규모의 42%를 차지했으며, 여전히 중국 내시경 검사 기기 시장의 핵심을 이루는 절차입니다. 그러나 호흡기 케어는 가장 급 곡선을 그려 대기 오염에 의한 COPD와 폐암 검진의 의무화를 배경으로 호흡기 내과용 기기는 CAGR 10.2%로 상승할 것으로 예측되고 있습니다. 병원은 기관지경 검사 능력을 확장하고 말초 종양에 대한 내시경 지침에 의존하는 마이크로파 절제 카테터를 채택합니다.

정형외과 센터는 관절경에 의한 스포츠 의학 프로그램을 확대하고, 인터벤셔널 심장병학은 판막 검사를 위한 마이크로내시경을 시험하고 있습니다. 이비인후과 클리닉은 음성 장애에 대한 의식이 높아지는 가운데 후두경에 대한 안정적인 수요를 유지하고 있습니다. 산부인과 및 뇌신경 수술은 4K 3D 뷰가 중요한, 작지만 복잡한 틈새 분야입니다. 이러한 다양한 파이프라인은 전체 임상 사이클에서 중국 내시경 검사 기기 시장의 탄력성을 강화하고 있습니다.

The China endoscopy devices market is valued at USD 2.58 billion in 2025 and is forecast to reach USD 3.75 billion by 2030, expanding at a 7.77% CAGR.

Growth is underpinned by an aging population-26% of citizens will be at least 65 years old by 2050-together with national cancer-control goals that mandate earlier detection and wider procedural access. Rapid uptake of 4K/3D/AI visualization platforms, a shift toward single-use scopes, and wider insurance coverage for minimally invasive techniques are reinforcing demand. Domestic innovators are scaling output under the "Made in China 2025" localization target, eroding the longstanding dominance of imported models. Parallel investments in tertiary-hospital capacity and dedicated training hubs are easing procedural bottlenecks, while the National Medical Products Administration (NMPA) is accelerating approvals for high-technology systems. Collectively, these forces are creating multi-layered opportunities across hardware, software, and after-sales services inside the China endoscopy devices market.

Gastrointestinal disorders are climbing in tandem with China's demographic shift toward later-life morbidity. Among citizens aged 80 and over, multimorbidity already affects 40.2% of individuals. Government-funded screening pilots show incremental cost-effectiveness ratios as low as USD 1,343 per QALY, confirming fiscal viability for large-scale roll-outs. These economics, combined with public awareness campaigns, drive steady throughput in colonoscopy and EGD suites inside the China endoscopy devices market.

Artificial-intelligence engines now cut capsule-review time by 89.3% while boosting lesion detection to 95.9% versus manual reads. Robotic bronchoscopy systems such as the MONARCH platform extend reach to peripheral nodules, broadening therapeutic indications. Integrated 3D 4K fluorescence units combine depth perception, ultra-high definition, and real-time perfusion assessment to improve oncologic margins. Experimental Raman-enabled scopes promise histology-level insight without biopsies, signalling the next frontier in precision diagnostics. These breakthroughs collectively elevate clinical expectations, accelerating capital-equipment replacement cycles throughout the China endoscopy devices market.

Capital prices for robotics and fluorescence units remain steep. A leading multi-port surgical robot, now discounted to spur uptake, still saw annual installations fall by nearly 30%. Annual service contracts, repair outlays, and intensive training add invisible overheads, discouraging budget-constrained hospitals. Competitive pricing by emerging local vendors is lowering the barrier, but full convergence with international cost structures is still several years away in the China endoscopy devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flexible instruments commanded a 48% revenue share in 2024, anchoring the China endoscopy devices market through routine GI, bronchial, and ENT work. Robot-assisted systems, however, represent the fastest CAGR at 14.7% through 2030, driven by demand for sub-millimeter control and integrated AI navigation. High-definition imaging, haptic feedback, and cloud analytics are converting once-experimental prototypes into daily-use assets, particularly for peripheral lung nodules and complex urologic lesions.

Manufacturers are layering fluorescence, 3D visualization, and deep-learning pathology prediction directly into robotic arms, compressing diagnostic and therapeutic cycles. Single-use flexible robots for airway management are also under evaluation, pairing infection-control benefits with mechanical stability. As these innovations roll out, the China endoscopy devices market size for robot platforms is set to outpace legacy categories, although disposable scope ecosystems will remain indispensable in high-volume respiratory clinics.

Gastrointestinal indications held 42% of 2024 value and remain the procedural backbone of the China endoscopy devices market. Yet respiratory care shows the steepest curve, with pulmonology devices forecast to rise at 10.2% CAGR on the back of air-pollution-induced COPD and lung-cancer screening mandates. Hospitals are expanding bronchoscopy capacities and adopting microwave ablation catheters that rely on endoscopic guidance for peripheral tumors.

Orthopedic centers are scaling arthroscopic sports-medicine programs, while interventional cardiology is experimenting with micro-endoscopes for valve inspection. ENT clinics maintain consistent demand for laryngoscopes amid rising voice-disorder awareness. Gynecology and neurosurgery remain smaller but high-complexity niches where 4K 3D views are critical. This diversified pipeline reinforces the resilience of the China endoscopy devices market across clinical cycles.

The China Endoscopy Devices Market Report is Segmented by Device Type (Endoscopes [Flexible Endoscope, and More], Endoscopic Operative Devices, and More), Application (Gastroenterology, Pulmonology, Orthopedic Surgery, and More), End User (Class III Hospitals, Specialty Clinics, and More), Hygiene (Reusable Endoscopes, and More), Technology (HD Imaging, and More). The Market Forecasts are Provided in Terms of Value (USD).