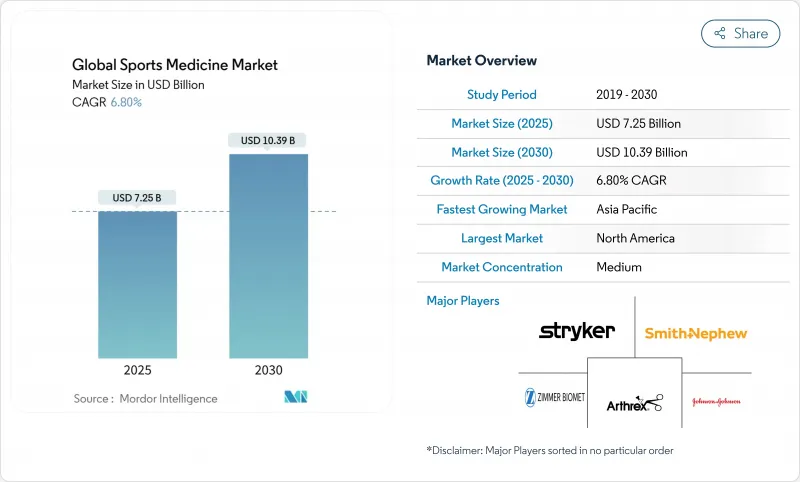

스포츠 의학 시장 규모는 2025년에 72억 5,000만 달러로 추정되고, 2030년에는 100억 9,000만 달러에 이를 전망이며, 2025-2030년 연평균 복합 성장률(CAGR) 6.8%로 성장할 것으로 예측됩니다.

프로스포츠 선수와 레크리에이션 스포츠 선수의 수는 꾸준히 증가하고 있으며, 계속 활동하고 있는 고령화 사회와 더불어 상해 예방, 진단, 치료 솔루션에 대한 수요는 높게 유지되고 있습니다. 재생 성형 생물학적 제형의 채용, 저침습 관절경 검사의 보급, 적절한 치료의 외래수술센터(ASC)로의 전환은 치료 경로를 재구성하고 대응 가능한 양을 확대하고 있습니다. 북미는 충실한 의료 제도와 깊은 스포츠 문화를 배경으로 40%의 수익 기반을 확보하고, 아시아태평양은 확대하는 스포츠 인프라와 의료 투어리즘의 흐름을 배경으로 CAGR 8.1%로 가속하고 있습니다. 기존 기업이 차세대 관절경, 생물학적 제제, 디지털 워크플로 도구로 포트폴리오를 새롭게 하여 더 나은 결과와 총 에피소드 비용 절감을 약속하는 가운데 경쟁이 치열해지고 있습니다.

청소년부터 노인까지 조직된 스포츠에 대한 연간 참가자 수는 증가하고 있지만, 임상적 주의를 요하는 상해의 수는 예방 노력을 능가하고 있습니다. 매년 350만 명 이상의 어린이들이 스포츠 관련 호소로 클리닉을 방문하고, 성인에서는 생산성과 생활의 질을 손상시키는 건증 등의 변성 질환이 증가하고 있습니다. 2024년에는 무릎 외상만으로 41%의 수술을 받았으며, 외과적 자원에 부담을 주는 동시에 조기 개입과 재활 프로그램에 대한 지불자의 관심이 가속화되고 있습니다. 의료 제공업체는 복잡한 어깨와 무릎 사례의 진단 워크플로우에 머신러닝 알고리즘을 통합하여 트리아지 정확도를 향상시키고 최종 치료까지의 시간을 단축하고 있습니다. 각국 정부는 동시에 상해 감시 프로그램을 강화하고 임상의에게 예방 캠페인을 실시하기 위한 풍부한 역학적 데이터를 제공합니다. 이러한 요소는 수술 건수를 유지하고 스포츠 의학 시장 전체의 고급 고정, 이식, 재활 제품에 대한 수요를 강화합니다.

관절경하 수술은 절개창이 작고, 기능 회복이 빠르며, 감염 위험이 낮기 때문에 관절 수복의 폭넓은 분야에서 선택되는 수술이 되고 있습니다. Arthrex ApolloRF i90과 같은 고주파 어블레이터는 기존 시스템보다 효율적으로 연부 조직을 제거하고 수술 시간 단축과 좋은 시각화를 지원한다는 비교 벤치 테스트에서 확인되었습니다. 외래수술센터에서 이루어지는 어깨, 무릎, 발목 수술은 2024년에는 2자리 성장률로 증가해 지불측 인센티브와 환자 당일 퇴원 지향이 뒷받침되고 있습니다. 장비 공급업체는 소형 타워 시스템, 일회용 시각화 프로브, 기술 효율성을 높이는 AI 강화 이미징을 지원합니다. 이러한 혁신은 스포츠 의학 시장 입원 정형외과의 변화를 강화하고 견고한 장비 업데이트 주기를 지원합니다.

정형 생물학적 주사, 고급 고분자 앵커 및 환자 전용 임플란트는 기존의 대체품을 3-5배 넘는 고가의 정가로 판매되고 있지만, 많은 적응증이 적응외로 남아 있기 때문에 보험사의 보험 적용은 종종 지연되고 있습니다. 가격에 민감한 시장의 의료 제공업체는 자본 지출을 관리하기 위해 경쟁 입찰을 채택하여 공급자 마진에 하향 압력을 가하고 있습니다. 신흥경제국에서는 예산이 제한되어 있어 최첨단 관절경 타워에 대한 접근이 제한되고, 기본 기구에 대한 의존도가 길어지고, 고가의 일회용 기구의 보급이 늦어지고 있습니다. 장비 제조업체는 특히 일괄 지불이 주류인 외래 환자의 상환을 확대하기 위해 의료 경제적 사례를 보여주거나 위험 분담 모델을 제공해야 합니다.

2024년 스포츠 의학 시장에서 정형외과용 임플란트가 35%의 매출을 차지하는 최대 시장이 되었습니다. 하지만 오르토바이오로직스가 가장 급성장하는 궤도를 확보했습니다. 스포츠 의학 재생 성형 생물학적 제형 시장 규모는 2024년 12억 달러에 이르렀고, CAGR 11.5%로 성장할 전망이며, 2030년에는 23억 달러로 확대될 것으로 예측되며, 생물학적 복구에 대한 축족을 강조하고 있습니다. 병원과 외래 센터는 PRP 및 골수 농축액을 위한 요지 관리 시스템을 통합하여 무균성을 유지하면서 치료 시간을 단축합니다. 주요 의료기기 제조업체는 생체 이식편, 콜라겐 스캐폴드, 합성 익스텐더를 자체 임플란트 라인에 추가하고 있으며, 미래 포트폴리오 경쟁력은 금속 고정과 생체 보강의 융합에 달려 있음을 뒷받침하고 있습니다.

절차의 편차는 치료 결과의 재현성을 방해할 수 있기 때문에 외과 의사의 교육은 여전히 중요한 추진력이 되고 있습니다. 주요 대학 센터는 현재 펠로우십 커리큘럼에 생물학적 성형술 모듈을 통합하고 환자의 선택과 표준화된 주입 프로토콜을 강조하고 있습니다. 동시에 헬스케어 지불자는 스포츠 복귀 가속화 및 재수술 감소로 인한 장기 비용 상쇄를 확인하기 위해 레지스트리를 분석합니다. 이러한 데이터가 성숙하면 상환 경로가 명확해지고 스포츠 의학 시장 전체에 생물학적 교정의 침투가 더욱 가속될 것입니다.

북미는 종합적인 보험 적용, 엘리트 선수에 대한 투자, 학술 의료 센터 및 프로 프랜차이즈와의 깊은 협력 관계에 의해 지원되고 있으며, 2024년 세계 매출의 40.0%를 차지했습니다. Johns Hopkins Medicine의 연골 재생 이니셔티브와 US Olympic & Paralympic Committee의 전용 클리닉과 같은 프로그램은 최첨단 연구를 촉진하는 동시에 조사 결과를 일상 진료에 신속하게 반영하고 있습니다. 성과 보상은 기능적 향상이 입증된 임플란트 및 생물학적 제제의 도입을 촉진하고 평균 판매 가격이 높은 환경을 지원합니다. FDA의 510(k) 패스웨이에 의한 규제의 명확화도 지속적인 장치의 반복을 촉진하지만, 생물 제제의 라이선스 신청 규칙에서 성형 생물학적 제제는 보다 엄격한 조사를 받습니다.

중국, 인도, 동남아시아 국가들이 스타디움 건설, 선수 트레이닝 센터, 국경을 넘은 의료 관광 허브에 자금을 제공하고 있기 때문에 아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 8.1%로 성장을 지속할 전망입니다. 각국의 스포츠 당국은 아마추어 선수에 대한 보험 적용을 확대해, 진단 및 치료 수요에 박차를 가하고 있습니다. 일본의 클리닉은 현재, 로봇 암에 의한 어시스트와 재생 보조 기구를 조합한 ACL 재건술을, 해외의 환자용으로 당일 판매하게 되어 있습니다. APKASS와 같은 지역의 정형외과학회는 지속적인 의학 교육을 추진하고 모범 사례의 보급을 도와 기술 도입을 가속화하고 있습니다. 투자자들은 이 지역의 관절경 시스템과 생물학적 제형을 위한 강력한 파이프라인을 보여주는 지역 스포츠 기관의 새로운 계약과 연계하여 종종 장비 주문이 급증한다는 것을 관찰합니다.

유럽에서는 GDP 성장이 둔화되었음에도 불구하고 클럽 스포츠가 확립되고 근골격계 연구를 위한 자금이 조정됨에 따라 의미 있는 규모가 유지되고 있습니다. EU 규제하에 국경을 넘은 환자의 이동이 가능하기 때문에 소규모 회원국의 선수도 독일과 프랑스의 일류 시설에 접근할 수 있어 수술 건수를 유지할 수 있습니다. 의료기기 제조업체는 엄격한 임상 증거 요구 사항을 부과하면서도 환자의 안전을 강조하는 변화하는 MDR 상황에 대응합니다. 3대륙의 중심에서 벗어나면 라틴아메리카와 중동은 도시의 병원이 북미의 센터를 모범으로 하는 정형외과 프로그램을 도입하고 있기 때문에 작지만 수요가 증가하고 있습니다. 그럼에도 불구하고 불균등한 인프라 배분이 당면의 규모를 제한하고 있기 때문에 공급업체는 1급 도시와 관민 파트너십 프로젝트에 주력하도록 촉구하고 있습니다.

The sports medicine market size is valued at USD 7.25 billion in 2025 and is forecast to achieve USD 10.09 billion by 2030, advancing at a 6.8% CAGR between 2025 and 2030.

A steadily growing base of professional and recreational athletes, combined with an aging population determined to remain active, is keeping demand high for injury prevention, diagnosis and treatment solutions. Adoption of regenerative orthobiologics, wider use of minimally invasive arthroscopy and the migration of appropriate procedures to ambulatory surgical centers are reshaping care pathways and expanding addressable volumes. North America secures a 40% revenue foothold on the back of well-funded health systems and deep sports culture, while Asia-Pacific is accelerating at an 8.1% CAGR on the strength of expanding sports infrastructure and medical-tourism flows. Competitive intensity is rising as incumbents refresh portfolios with next-generation arthroscopes, biologics and digital workflow tools that promise better outcomes and lower total episode costs.

Annual participation in organized sports is rising among youth and seniors alike, yet the number of injuries requiring clinical attention continues to outpace preventive efforts. More than 3.5 million children present to clinics each year with sports-related complaints, while adults face increasing degenerative conditions such as tendinopathy that compromise productivity and quality of life. Knee trauma alone represented 41% f sports medicine procedures in 2024, stressing surgical resources and accelerating payer interest in earlier intervention and rehabilitation programs. Providers are incorporating machine-learning algorithms into diagnostic workflows for complex shoulder and knee cases, improving triage accuracy and shortening time to definitive care. Governments are simultaneously elevating injury-surveillance programs, giving clinicians richer epidemiological data with which to target prevention campaigns. These elements converge to sustain procedure volumes and bolster demand for advanced fixation, graft and rehabilitation products across the sports medicine market.

Arthroscopy has become the technique of choice for a widening range of joint repairs because it combines smaller incisions with faster functional recovery and lower infection risk. Comparative bench tests confirm that high-frequency ablators such as Arthrex ApolloRF i90 remove soft tissue more efficiently than legacy systems, supporting shorter operative times and better visualization. Outpatient settings are increasingly favored: shoulder, knee and ankle repairs performed in ambulatory surgical centers grew at double-digit rates in 2024, propelled by payer incentives and patient preference for same-day discharge. Equipment suppliers are responding with compact tower systems, disposable visualization probes and AI-enhanced imaging that raise procedural efficiency. These innovations reinforce the sports medicine market's shift away from inpatient orthopedics, underpinning robust capital-equipment replacement cycles.

Orthobiologic injections, advanced polymer anchors and patient-specific implants carry premium list prices that can exceed traditional alternatives by 3-5X, yet insurer coverage often lags because many indications remain off-label. Providers in price-sensitive markets adopt competitive bidding to manage capital outlays, thereby placing downward pressure on supplier margins. In emerging economies, constrained budgets limit access to cutting-edge arthroscopic towers, perpetuating reliance on basic instrumentation and slowing penetration of higher-value disposables. Device manufacturers must demonstrate strong health-economic cases or offer risk-sharing models to broaden reimbursement, particularly in outpatient settings where bundled payments dominate.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Orthopedic implants contributed the largest 35% revenue portion of the sports medicine market in 2024 because surgeons remain reliant on screws, plates and suture anchors for durable mechanical fixation. Nevertheless, orthobiologics secured the steepest growth trajectory, aided by expanding clinical proof points and higher reimbursement adoption. The sports medicine market size for regenerative orthobiologics is projected to rise from USD 1.2 billion in 2024 to USD 2.3 billion by 2030 at an 11.5% CAGR, highlighting the pivot toward biologically driven repair. Hospitals and outpatient centers are integrating point-of-care preparation systems for PRP and bone-marrow concentrates, reducing procedure times while maintaining sterility. Larger device firms are adding biologic grafts, collagen scaffolds and synthetic extenders to their implant lines, confirming that future portfolio competitiveness hinges on blending metal fixation with biologic augmentation.

Surgeon education remains a crucial enabler because technique variation can hamper outcome reproducibility. Leading academic centers now include orthobiologic modules in fellowship curricula, emphasizing patient selection and standardized injection protocols. Simultaneously, healthcare payers analyze registries to confirm long-term cost offsets from faster return-to-sport and reduced re-operations. Such data, once mature, will clarify reimbursement pathways and further accelerate orthobiologic penetration across the sports medicine market.

The Sports Medicine Market Report is Segmented by Product Type (Orthopedic Implants, Arthroscopy Devices, Orthobiologics, Braces & Supports, and More), Application (Knee Injuries, Shoulder Injuries, Foot & Ankle Injuries, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 40.0% of global revenue in 2024, sustained by comprehensive insurance coverage, elite athlete investment and deep collaboration between academic medical centers and professional franchises. Programs such as Johns Hopkins Medicine's cartilage-regeneration initiative and the U.S. Olympic & Paralympic Committee's dedicated sports medicine clinics foster leading-edge research while translating findings rapidly into everyday practice. Pay-for-performance reimbursement encourages uptake of implants and biologics that boast proven functional gains, supporting a high average selling price environment. Regulatory clarity under the FDA 510(k) pathway also facilitates continuous device iteration, although orthobiologics face tighter scrutiny under biologics license application rules.

Asia-Pacific is tracking the fastest 8.1% CAGR through 2030 as China, India and Southeast Asian nations fund stadium construction, athlete-training centers and cross-border medical-tourism hubs. National sport authorities are extending insurance cover for amateur athletes, spurring diagnostic and therapeutic demand. Japanese clinics now market same-day ACL reconstruction packages to international patients, combining robotic-arm assistance with regenerative adjuncts. Regional orthopedic societies such as APKASS promote continuing medical education, helping disseminate best practices and accelerating technology adoption. Investors observe that device orders often jump in tandem with new provincial sports-institute contracts, indicating a strong pipeline for arthroscopy systems and biologics in the region.

Europe preserves meaningful scale despite slower GDP growth, thanks to well-established club sports and coordinated funding for musculoskeletal research. Cross-border patient mobility under EU regulations allows athletes from smaller member states to access leading German and French centers, sustaining procedure volumes. Device companies navigate a shifting MDR landscape that imposes stringent clinical-evidence requirements but also underscores patient safety. Outside the tri-continental core, Latin America and the Middle East generate modest but rising demand as urban hospitals model their orthopedic programs on North American centers. Nonetheless, unequal infrastructure distribution limits near-term scale, prompting suppliers to focus on tier-one cities and public-private partnership projects.