북미의 핵의학 시장은 2025년에는 80억 2,000만 달러로 추정되고, 2030년에는 136억 5,000만 달러에 이를 것으로 예측됩니다.

이 확장은 종양학, 순환기학, 신경학에 걸친 정밀 진단 및 표적 치료에서 이 분야가 매우 중요한 역할을 한다는 것을 뒷받침합니다. 방사성 항암제에 대한 지속적인 투자, 보다 광범위한 임상 적응 및 지지적인 상환 정책으로 인해 거시경제적인 압력에도 불구하고 수술 건수는 계속 증가하고 있습니다. 특히 몰리브덴-99와 악티늄-225 공급망의 현지화는 조달 위험을 더욱 줄이고 밸류체인의 강인성을 강화합니다. 기존 기업과 신규 진출기업 간 경쟁 격화는 기술 혁신을 가속화하고 특허 소송은 전략적 포지셔닝을 형성합니다.

암의 이환율은 북미 전역에서 계속 상승하고 있으며, 심혈관계 질환은 여전히 사망 원인의 상위를 차지하고 있기 때문에 정확한 진단 및 치료가 필요한 핵의학 검사에 대한 수요가 높아지고 있습니다. 전립선암, 유방암, 폐암의 유병률이 60세를 넘으면 급격히 상승하기 때문에 인구통계학적 고령화가 이 요구를 증폭시키고 있습니다. 12세 이상의 환자에 대한 루테튬 Lu177 도타테이트의 FDA 승인에 따라 소아에 대한 적응이 확대되고 새로운 대응 가능한 집단이 출현하고 있습니다. 기존의 SPECT에 의한 심장의 볼륨이 감소하는 반면, PET에 의한 심근 관류 영상은 그 특이성의 높이로부터 지지를 모으고 있습니다. 종양학과 순환기학의 용도가 융합됨에 따라 의료 제공업체는 케어 패스를 간소화하고 서비스를 크로스셀할 수 있어 여러 전문가의 수익 기둥이 됩니다.

북미의 헬스케어 시스템에서는 이러한 기술의 채용이 증가하고 있으며, 심장 PET 이미지는 임상 채용 확대 및 2025년 메디케어 & 메디케이드 서비스 센터(Centers for Medicare & Medicaid 서비스) 개혁에 의한 고도 진단용 방사성 의약품에 대한 별도의 지불 경로를 제공하는 상환 프레임워크의 개선에 의해 입증된 바와 같이 미국의 심장 전문의들 사이에서 큰 지지를 얻고 있습니다. GE 헬스케어의 Flyrcado 트레이서는 반감기 109분으로 스트레스 검사의 가능성을 넓혀 외래 심장병 센터를 끌어들입니다. 텔루라이드 카드뮴 아연과 같은 검출기의 진보는 방사선량을 억제하면서 분해능을 향상시키고 임상의와 환자의 안전성에 대응합니다. 인공지능 알고리즘은 병변의 정량화를 자동화하고, 해석의 편차를 줄이며, 보고서의 납기를 가속화합니다.

많은 진단용 아이소토프가 몇 시간 안에 붕괴되기 때문에 저스트-인-타임 물류가 요구됩니다. 불소 18의 반감기는 6시간이므로 배송 지역은 약 200마일로 제한됩니다. 2024년 유럽 원자로의 예기치 않은 다운타임으로 인해 테크네튬-99m가 미국 여러 주에서 50-100% 부족하여 선택적 검사가 지연되었습니다. 콜드체인을 수용하는 데는 비용이 많이 들고, 지역 시설에서는 종종 배송 기한에 맞지 않고 서비스 이용이 제한됩니다. 보다 긴 수명의 구리-64는 부분적인 구제를 가져오지만, 임상으로의 보급은 추가 인프라와 시험 데이터에 달려 있습니다.

진단용 방사성 의약품은 2024년 북미의 핵의학 시장에서 72.70%의 점유율을 유지했으며, 정착된 상환 및 임상의의 익숙성에 의해 지원되고 있습니다. 그러나 루테튬-177 PSMA와 같은 방사성 리간드가 양호한 안전성 프로파일로 진행 전이성 질환에 대응하기 때문에 치료제의 CAGR은 11.45%로 크게 성장할 전망입니다. 치료제의 북미 핵의학 시장 규모는 암 전문의들 사이에서 채용이 가속되고 있음을 반영하여 2030년까지 46억 달러를 넘는 것으로 보입니다. SPECT는 여전히 루틴의 뼈 스캔에서 우위를 유지하고 있지만, PET의 뛰어난 해상도는 신경과와 종양과의 도입을 획득하고 있습니다. 인공지능을 활용한 선량 측정은 치료 정밀도를 향상시켜 고액의 상환 가격에 대한 지불자의 신뢰를 강화합니다.

진단 수익과 치료 수익 사이에는 보강 루프가 존재하며 이미징의 긍정적인 경험은 동반자 치료제에 대한 환자 등록을 촉진합니다. 노발티스의 Pluvicto는 2024년 첫 9개월 동안 미국에서 10억 달러의 매출을 달성하여 고가치 방사선 대체 의료에 대한 상업적 의욕을 입증했습니다. 2025년 CMS 결제 개혁은 630달러 이상의 진단 트레이서에 독립적인 APC를 제공하여 병원 이익률을 개선하고 재고 확대를 촉진했습니다. 북미의 핵의학 업계는 현재 한때 진단제에 집중했던 제조업체들 사이에서 치료 혁신을 주요 차별화 요인으로 자리잡고 있습니다.

종양의 병기 분류 및 치료 모니터링에 있어서 중심적인 역할을 반영하고, 2024년에는 북미의 핵의학 시장의 41.45%를 종양 영역이 차지했습니다. 종양학 용도의 북미 핵의학 시장 규모는 CAGR 11.2%로 성장할 전망이며, 2030년에는 56억 달러 이상에 달할 것으로 예측되고 있습니다. 신경학은 가장 급성장하는 용도로, 아밀로이드와 타우 PET가 알츠하이머병의 진단 정밀도를 높이기 위해 연율 11.78%로 확대될 전망입니다. 2025년 CMS 여행정책의 갱신으로 메디케어 수급자의 자기부담액이 인하되고 스캔 이용이 더욱 촉진됩니다.

신경영상 진단 수요가 증가함에 따라 Neuracaceq 등의 불소 18 트레이서 공급망 조정이 진행되고, Lantheus가 Life Molecular Imaging을 7억 5,000만 달러로 인수함으로써 새롭게 추가되었습니다. 고급 AI 알고리즘을 통해 스캔 당 읽기 시간이 12분에서 4분으로 단축되어 신경 방사선과 의사 부족에 대응하고 있습니다. 순환기 내과는 SPECT의 감소에도 불구하고 2024년에 전년 대비 6% 성장한 PET 관류 이미징에 의해 관련성을 유지합니다. 내분비학은 갑상선 흡수 검사 및 요오드 131 요법이 미국의 주요 학술 센터에서 안정적이고 견조함을 유지합니다.

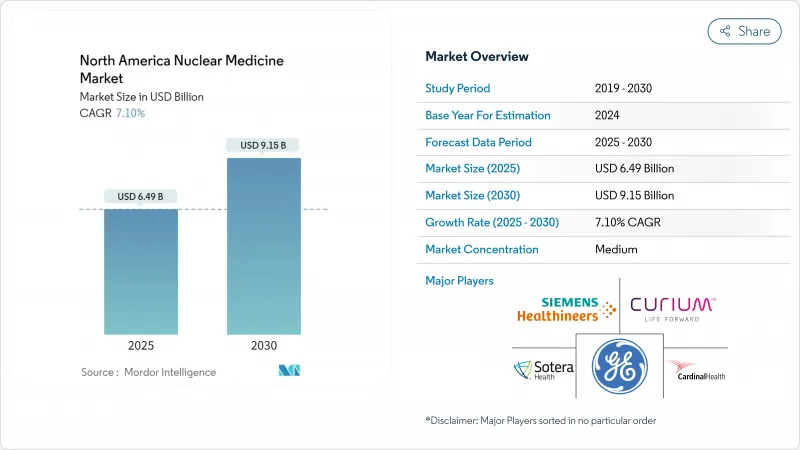

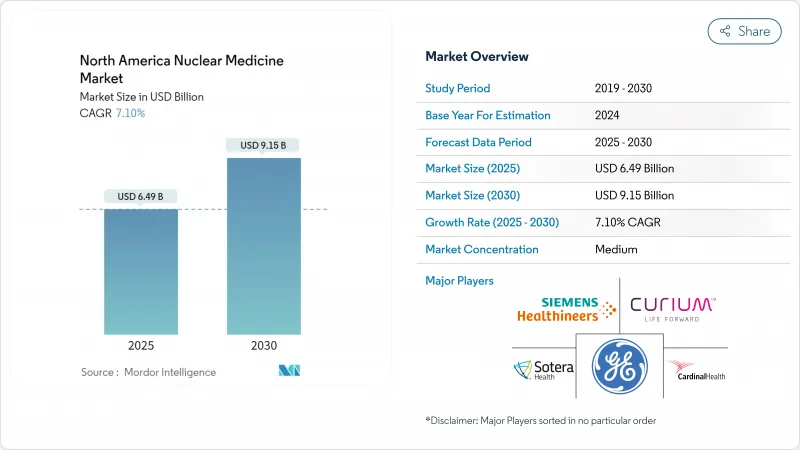

The North America nuclear medicine market stands at USD 8.02 billion in 2025 and is forecast to reach USD 13.65 billion by 2030, translating to an 11.23% CAGR.

This expansion underscores the segment's pivotal role in precision diagnostics and targeted therapy across oncology, cardiology, and neurology. Sustained investment in radiotheranostics, broader clinical indications, and supportive reimbursement policies continue to lift procedure volumes despite macro-economic pressures. Supply chain localization, particularly for molybdenum-99 and actinium-225, further reduces procurement risk and strengthens value-chain resilience. Intensifying competition among incumbents and new entrants accelerates innovation while patent litigation shapes strategic positioning.

Cancer incidence continues to climb across North America, with cardiovascular disease remaining the leading cause of mortality, sustaining demand for accurate diagnostic and therapeutic nuclear medicine procedures. Demographic aging amplifies this need as prostate, breast, and lung cancer prevalence rises sharply beyond age 60. Pediatric indications now grow following FDA approval of lutetium Lu 177 dotatate for patients aged 12 and above, opening new addressable populations. While traditional SPECT cardiac volumes ebb, PET myocardial perfusion imaging gains favor for its higher specificity. The convergence of oncology and cardiology applications enables providers to streamline care pathways and cross-sell services, anchoring multi-specialty revenue streams.

North American healthcare systems increasingly adopt these technologies, with cardiac PET imaging gaining significant traction among US cardiologists as demonstrated by expanding clinical adoption and improved reimbursement frameworks under Centers for Medicare & Medicaid Services reforms in 2025 that provide separate payment pathways for advanced diagnostic radiopharmaceuticals. GE HealthCare's Flyrcado tracer, with a 109-minute half-life, broadens stress testing feasibility and attracts outpatient cardiology centers. Detector advances such as cadmium zinc telluride improve resolution while trimming radiation dose, addressing clinician and patient safety. Artificial intelligence algorithms automate lesion quantification, reducing interpretation variability and accelerating report turnaround.

Many diagnostic isotopes decay within hours, demanding just-in-time distribution. Fluorine-18's 6-hour half-life restricts shipment zones to roughly 200 miles. In 2024, unexpected European reactor downtime created 50-100% shortages in technetium-99m across multiple U.S. states, delaying elective scans. Cold-chain compliance adds cost, and rural sites often cannot meet delivery windows, limiting service availability. Longer-lived copper-64 offers partial relief, though widespread clinical adoption hinges on additional infrastructure and trial data.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Diagnostic radiopharmaceuticals retained 72.70% share of the North America nuclear medicine market in 2024, supported by entrenched reimbursement and entrenched clinician familiarity. Therapeutic agents, however, are growing much faster at an 11.45% CAGR as radioligands like lutetium-177 PSMA address advanced metastatic disease with favorable safety profiles. The North America nuclear medicine market size for therapeutics is set to surpass USD 4.6 billion by 2030, reflecting accelerating adoption among oncologists. SPECT remains dominant in routine bone scans, while PET's superior resolution wins neurology and oncology referrals. Artificial intelligence-driven dosimetry improves treatment precision, reinforcing payer confidence in premium reimbursement tiers.

A reinforcing loop exists between diagnostic and therapeutic revenues: positive imaging experiences facilitate patient enrollment in companion therapeutics. Novartis's Pluvicto reached USD 1 billion in U.S. sales during the first nine months of 2024, validating commercial appetite for high-value radiotheranostics. CMS payment reform in 2025 created a separate APC for diagnostic tracers above USD 630, improving hospital margins and encouraging inventory expansion. The North America nuclear medicine industry now positions therapeutic innovation as a primary differentiator among manufacturers that once concentrated on diagnostic agents.

Oncology represented 41.45% of the North America nuclear medicine market in 2024, reflecting its central role in tumor staging and therapy monitoring. The North America nuclear medicine market size for oncology applications is forecast to cross USD 5.6 billion in 2030 at an 11.2% CAGR. Neurology is the fastest-growing application, expanding 11.78% annually as amyloid and tau PET increase Alzheimer's diagnostic accuracy. CMS travel policy updates in 2025 lowered out-of-pocket costs for Medicare beneficiaries, further encouraging scan uptake.

Neuroimaging demand spurs supply chain adjustments for fluorine-18 tracers like Neuraceq, recently added through Lantheus's USD 750 million acquisition of Life Molecular Imaging. Advanced AI algorithms shorten interpretation time from 12 minutes to 4 minutes per scan, addressing neuroradiologist shortages. Cardiology maintains relevance through PET perfusion imaging, which grew 6% year-over-year in 2024 despite SPECT declines. Endocrinology remains steady, with thyroid uptake studies and iodine-131 therapy stable across major U.S. academic centers.

The North America Nuclear Medicine Market Report is Segmented by Product Type (Diagnostic Radiopharmaceuticals, Therapeutic Radiopharmaceuticals), Application (Oncology, Cardiology, Neurology, and More), Radioisotope (Tc-99m, F-18, I-131, Lu-177, Y-90, Ga-68, Ac-225, Others), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (US, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).