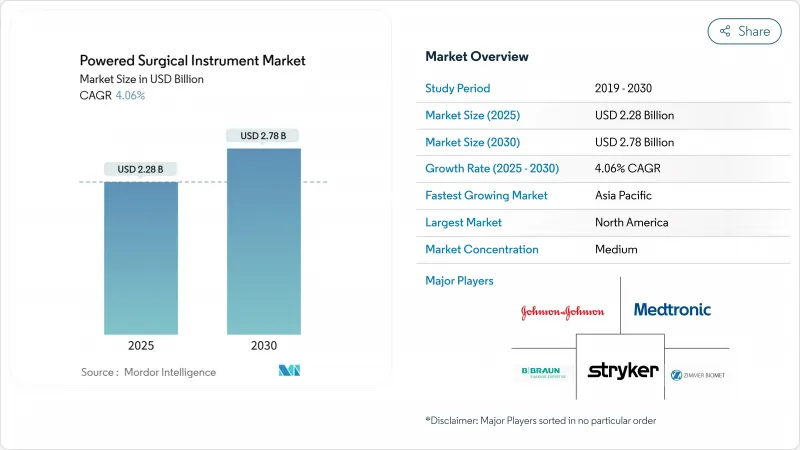

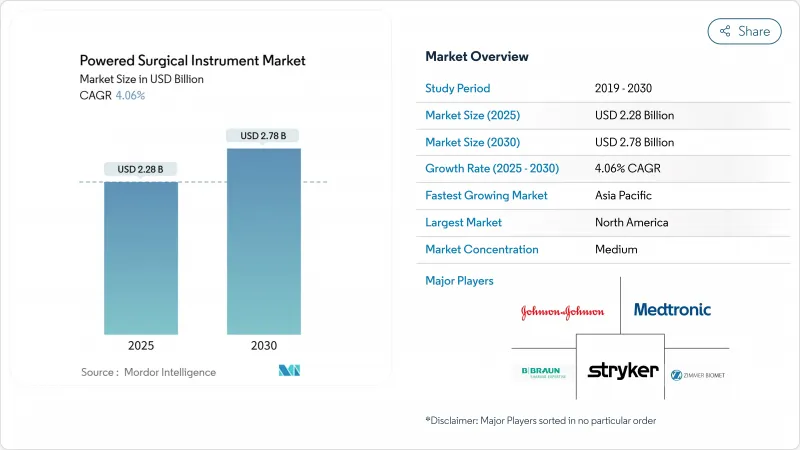

전동 수술기구 시장 규모는 2025년에 22억 8,000만 달러, 2030년에는 27억 8,000만 달러에 이르고, CAGR은 4.06%를 나타낼 전망입니다.

고령화, 수술 건수 증가, 단계적인 기술 향상이 초기 채택 단계 이후의 성장을 지원하고 있습니다. 수요는 낮은 침습 절차의 선호에 의해 강화되는 반면, 표준 멸균을 위한 규제의 움직임은 기존 공급업체에게 유리합니다. 병원은 또한 가치 기반 의료 지표를 충족하기 위해 통합 장비 플랫폼을 선호하고 프리미엄 가격을 지원합니다. 아시아태평양의 인프라 정비 및 당일치기 수술 전문센터의 상승은 전동 수술기구 시장에서 북미의 현재 수익 리더십과 균형을 이루는 지리적 변화를 지원하고 있습니다.

신흥경제국에서의 보험 적용 확대와 도시화에 의한 외상 발생률의 상승에 따라 세계 수술실 활동이 활발해지고 있습니다. 응급실은 골절을 수동 공구보다 빨리 안정화시키고 결과를 개선하고 심각한 환자를위한 침대를 확보하기 위해 전동 드릴과 톱을 사용합니다. 아시아태평양의 대규모 센터에서는 배터리 모드와 유선 모드를 결합한 하이브리드 콘솔이 도입되어 외상 사례 간의 회전 시간이 단축됩니다. 교통사고와 노동재해는 예측 가능한 수요를 창출하고 급성장하는 대도시권의 동력식 수술기구 시장을 지원하고 있습니다. 복잡한 다발 외상을 치료하는 병원에서는 재고 합리화와 신속한 멸균 사이클을 보장하기 위해 모듈 식 핸드 피스 시스템의 구매가 증가하고 있습니다. 외과의사는 수술 시간 단축을 보고하고 전력 플랫폼에 대한 지속적인 투자에 대한 행정 지원을 강화하고 있습니다.

65세 이상의 노인은 선진국에서 가장 빠르게 증가하고 있는 코호트이며, 인공관절 치환술과 척추고정술의 건수를 끌어 올리고 있습니다. 이 수술은 높은 토크 드릴과 리머에 의존하며 동력 수술기구 시장의 장기 수익 기반을 확보하고 있습니다. 미국에서는 인공 고관절 치환술과 인공 슬관절 치환술의 진료 보상 번들에 의해 병원은 수술을 효율적으로 완료하도록 요구되고 있으며, 외과의의 피로를 경감하는 경량 배터리 핸드피스가 지지되고 있습니다. 유럽의 당일치기 수술시설에서는 수술실의 셋업을 간소화하기 위해 무선 시스템을 활용하여 고관절의 당일 재치환술을 실시했습니다. 일본의 클리닉에서는 이동 수술 팀을 통해 지방 노인 환자를 수용하기 위해 휴대용 콘솔을 배치하여 접근 폭을 넓히고 있습니다. 이러한 인구동태에 연동한 수요는 구조적이며 공급업체에게는 2030년 이후에도 지속적인 판매 파이프라인이 확보되게 됩니다.

초기 구매 가격은 50,000-20만 달러이며 연간 서비스 계약은 일반적으로 초기 구매 금액의 10-15%에 상당하기 때문에 소규모 시설의 예산은 엄격합니다. 연구에 따르면, 로봇 담낭 적출술의 일회용은 복강경 수술의 동등품을 능가하지만, 우수한 치료 성적은 얻지 못하고 관리자는 고급 콘솔의 ROI를 의문시하고 있습니다. 신흥 시장 클리닉에서는 배터리 교체 비용을 피하기 위해 중고 유선 시스템을 구입하고 업그레이드를 지연시키는 경우가 많습니다. 다년간 임대 모델이 보급되고 있지만, 금리 변동은 자금 조달 비용을 증가시키고 단기 구매 계획을 억제할 수 있습니다. 그 결과, 임상 팀이 유선 솔루션을 강력히 희망하고 있음에도 불구하고 자본 집약도가 보급을 억제하고 있습니다.

리튬 이온 배터리 플랫폼이 동력식 수술 기구 시장을 견인해 배터리 시스템은 2030년까지의 CAGR을 4.92%로 예측했습니다. 2024년에도 유선식 기구의 점유율은 41.23%로, 중단 없는 전류를 중시하는 대량 생산 센터에서의 기존 설치를 반영하고 있습니다. 교체 가능한 배터리 포드를 특징으로 하는 어셈블리는 외래 치료실에서의 회전 시간을 단축하고 정형외과 외상실에서의 지지를 모으고 있습니다. 하이브리드 콘솔은 수술 중 체위 전환 시 벽 전원에서 배터리 백업으로 원활하게 이동하여 케이블이 없는 드레이프의 무균성을 보장합니다. 현재 경쟁의 중심은 충전 사이클의 수명과 병원 자산 소프트웨어에 반영되는 실시간 배터리 진단입니다. 예측 기간 동안, 특히 아시아태평양의 확대 당일치기 수술망에서는 휴대성의 이점으로부터 배터리 유닛이 새로운 설치의 선두에 서게 됩니다.

외과의사는 2시간이 넘을 수 있는 관절성형술에서 코드의 산란을 줄이고 핸드피스를 가볍게 하는 것이 인체공학적 주요 이점이라고 합니다. 공압식 플랫폼은 매우 부드러운 토크 전달로 인해 뇌신경 수술에서 틈새 수요를 유지하지만 병원이 디지털 OR 투자에 기대하는 연결성이 부족합니다. 따라서 공급업체는 Bluetooth를 통한 펌웨어 업데이트를 배터리 핸들에 통합하고 멸균 가능한 충전 도크와 결합합니다. 라틴아메리카의 가격에 민감한 병원에서는 초기 비용을 줄일 수 있는 인하 프로그램에 의해 개조된 유선 장비가 여전히 선호되고 있습니다. 전동 수술기구 시장은 배터리 기술 혁신이 지속적인 성장 레버임을 강조하면서도 전원 유형 간의 균형 잡힌 구매로 다양성을 유지하고 있습니다.

핸드피스는 2024년 매출의 60.45%를 차지하며 전동 수술기구 시장의 경제적 요점이 되고 있습니다. 톱 시스템과 고속 드릴은 정형외과 수요를 이끌고, 면도기는 이비인후과와 스포츠 의학실에서 점유율을 늘리고 있습니다. 반면, 액세서리와 소모품은 CAGR 5.12%로 확대되었으며 일회용 바스, 블레이드 및 슬리브는 제조업체에 예측 가능한 케이스당 수입을 제공합니다. 소모품은 재멸균의 번거로움을 없애고 감염 관리 감사에 적합하기 때문에 병원은 높은 변동비를 받아들입니다.

OEM은 스마트 콘솔의 사용 데이터를 기반으로 블레이드를 자동 발송하는 서비스 계약을 번들하여 연금과 같은 수익을 창출합니다. 소모품의 확대는 또한 주기적인 자본 예산에 대한 수익을 평준화하고 거시 경제의 변동을 극복하기 위한 공급업체의 자리를 차지합니다. 성형 수술 클리닉은 코 성형술을 수정하기 위해 마이크로 버링 팁을 채택하고 절차에 특화된 소모품이 고객 기반을 넓히는 방법을 보여줍니다. 재고 센서와 연동한 디지털 주문 포털이 고객을 더욱 둘러싸고 끈끈한 관계를 통해 동력식 수술 기구 시장을 강화하고 있습니다.

2024년 매출 점유율은 북미가 35.45%로 선두를 차지했습니다. 메디케어 번들이 수술 시간을 단축하는 장비에 대한 설비 투자를 자극하는 반면 미국의 외과의사는 예지 서비스 진단이 가능한 스마트 콘솔을 채택하고 있습니다. 캐나다의 지방 구매 그룹은 보편적인 예산 하에서 이익을 극대화하기 위해 다중 치료 키트를 지원하고, 멕시코 국경을 따라 병원은 의료 관광객에게 서비스를 제공하기 위해 역동적 인 수술기구 시장을 이용합니다.

유럽은 2위 지역입니다. 독일, 프랑스, 이탈리아에서는 고령화에 따른 정형외과 사례 증가가 보이며, 병원은 재원일수 단축에 보상하는 가치 기반 계약을 채택하고 있습니다. 영국에서는 NHS의 사례당 비용 임계값에 구매 가이드라인을 맞추어 콘솔 로그에서 얻은 수명 분석에 중점을 둔 조달을 실시했습니다. EU의 의료기기 규정은 환자의 안전성을 강화하는 동시에 가격 중심의 경쟁으로부터 브랜드를 보호하기 위해 기존 브랜드가 제공할 수 있는 견고한 임상 데이터를 요구하고 있습니다.

아시아태평양의 CAGR은 5.46%로 가장 높습니다. 중국의 현립병원은 국민보험에 의한 정형외과의 보험 적용 확대에 따라 도구 재고를 업그레이드하고 있습니다. 인도의 도시 클러스터에는 버터라이즈드 키트를 선호하는 대량 진료 데이 클리닉이 개설됩니다. 일본의 초고령화 사회는 고관절과 척추의 수술 건수를 안정적으로 유지하고, 한국의 미용 투어리즘은 외국인 환자를 만족시키기 위해 유럽의 마이크로 드릴을 수입하고 있습니다. ASEAN의 하모니제이션은 승인에 걸리는 시간을 단축하고 있지만, 로컬 컨텐츠 규칙은 다국적 기업과 지역 OEM 간의 파트너십을 촉진하고 있습니다. 이러한 역학이 결합되면서 아시아 신흥국 전체의 동력식 수술기구 시장에 결정적인 성장의 벡터가 보입니다.

The powered surgical instruments market size stands at USD 2.28 billion in 2025 and is on track to reach USD 2.78 billion by 2030, advancing at a 4.06% CAGR.

Aging populations, higher surgical volumes, and incremental technological gains sustain growth after the early-adoption phase. Demand is reinforced by minimally invasive technique preferences, while regulatory moves toward standardized sterilization favor incumbent suppliers. Hospitals also prioritize integrated instrument platforms to satisfy value-based care metrics, supporting premium pricing. Asia-Pacific's infrastructure build-out and the rise of specialist day-surgery centers underpin a geographic shift that balances North America's current revenue leadership within the powered surgical instruments market.

Global operating-room activity is rising as insurance coverage broadens in emerging economies and urbanization elevates trauma incidence. Emergency departments rely on power-driven drills and saws to stabilize fractures faster than manual tools, improving outcomes and freeing critical-care beds. High-volume centers in Asia-Pacific now integrate hybrid consoles that combine battery and wired modes, shortening turnover time between trauma cases. Traffic accidents and industrial injuries create predictable demand, anchoring the powered surgical instruments market in fast-growing metropolitan regions. Hospitals that treat complex polytrauma increasingly purchase modular handpiece systems to streamline inventory and ensure quick sterilization cycles. Surgeons report shorter operative times, reinforcing administrative support for continued investment in power platforms.

People aged 65 + are the fastest-growing cohort in developed economies, pushing joint-replacement and spinal-fusion volumes upward. These interventions depend on high-torque drills and reamers, securing a long-term revenue base for the powered surgical instruments market. United States reimbursement bundles for hip and knee arthroplasty pressure hospitals to complete procedures efficiently, favoring lightweight battery handpieces that mitigate surgeon fatigue. European day-surgery units now perform same-day hip revisions, leveraging cordless systems to simplify OR setup. Japanese clinics deploy portable consoles to serve rural geriatric patients via mobile surgical teams, widening access. This demographic-linked demand is structural, ensuring a durable sales pipeline for suppliers through 2030 and beyond.

Initial purchase prices range from USD 50,000 to USD 200,000, while annual service contracts typically equal 10-15% of the original spend, challenging budgets of smaller facilities. Studies show robotic cholecystectomy disposables can exceed laparoscopic equivalents without superior outcomes, prompting administrators to question ROI on advanced consoles. Emerging-market clinics often delay upgrades, buying pre-owned wired systems to avoid battery replacement expense. Multiyear leasing models are spreading, yet interest-rate volatility raises financing costs and may temper acquisition plans in the near term. Consequently, capital intensity restrains penetration even as clinical teams voice strong preference for powered solutions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Lithium-ion battery platforms have propelled the powered surgical instruments market, with battery systems tracking a 4.92% CAGR through 2030. In 2024 wired-electric devices still held 41.23% share, reflecting legacy installations at high-volume centers that value uninterrupted current. Assemblies featuring swappable battery pods cut turnover time in ambulatory suites and gain traction in orthopedic trauma rooms. Hybrid consoles seamlessly transfer from wall power to battery backup during intraoperative repositioning, ensuring sterility of cable-free drapes. Competition now centers on charge-cycle longevity and real-time battery diagnostics that feed into hospital asset software. Over the forecast period, portability advantages keep battery units at the forefront of new installations, especially across Asia-Pacific's expanding day-surgery grid.

Surgeons cite reduced cord clutter and lighter handpieces as key ergonomic benefits during arthroplasty that may last beyond two hours. Pneumatic platforms retain niche demand in neurosurgery for their ultra-smooth torque delivery, but they lack the connectivity that hospitals expect from digital OR investments. Suppliers therefore integrate Bluetooth firmware updates into battery handles, pairing them with sterilizable charging docks. Price-sensitive hospitals in Latin America still favor wired rigs refurbished through trade-in programs that lower upfront expense. Balanced purchasing across power types keeps the powered surgical instruments market diversified while underscoring battery innovation as an enduring growth lever.

Handpieces dominated 60.45% of revenues in 2024, making them the economic cornerstone of the powered surgical instruments market. Saw systems and high-speed drills lead orthopedic demand, while shavers carve share in ENT and sports medicine suites. Meanwhile, accessories and consumables are expanding at a 5.12% CAGR, with single-use burs, blades, and sleeves offering predictable per-case income to manufacturers. Hospitals accept higher variable costs because disposables eliminate re-sterilization labor and align with infection-control audits.

OEMs bundle service contracts with auto-shipping of blades based on usage data from smart consoles, creating annuity-like revenue. Consumable expansion also smooths earnings against cyclical capital budgets, positioning suppliers to weather macroeconomic swings. Plastic-surgery clinics adopt micro-burring tips for rhinoplasty refinements, illustrating how procedure-specific consumables widen the customer base. Digital ordering portals tied to inventory sensors further lock in clients, reinforcing the powered surgical instruments market through sticky relationships.

The Powered Surgical Instrument Market Report is Segmented by Power Source (Wired-Electric, Battery-Powered (Li-Ion, Nimh), and More), Product Type (Handpieces, and More), Application (Orthopedic & Trauma, and More), End-User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 35.45% revenue share in 2024. Medicare bundles stimulate capital spending on instruments that cut theater time, while United States surgeons adopt smart consoles capable of predictive service diagnostics. Canada's provincial buying groups favor multi-procedure kits to maximize return under universal budgets, and Mexico's border hospitals tap the powered surgical instruments market to serve medical tourists.

Europe is the second-largest region. Germany, France, and Italy see orthopedic case growth tied to aging citizens, and hospitals adopt value-based contracts that reward shorter length of stay. The United Kingdom aligns purchasing guidelines to NHS cost-per-case thresholds, which puts procurement weight on lifespan analytics from console logs. EU Medical Device Regulation demands robust clinical data that established brands can supply, shielding them against price-led competition while reinforcing patient safety.

Asia-Pacific posts the strongest 5.46% CAGR. China's county hospitals upgrade tool inventories as national insurance expands orthopedic coverage. India's urban clusters open high-volume day clinics that prefer batterized kits. Japan's super-aged society sustains steady hip and spine volumes, while South Korea's cosmetic tourism imports European micro-drills to satisfy foreign patients. ASEAN harmonization has trimmed approval timelines, yet local-content rules spur partnerships between multinationals and regional OEMs. Combined, these dynamics outline a decisive growth vector for the powered surgical instruments market across emerging Asian economies.