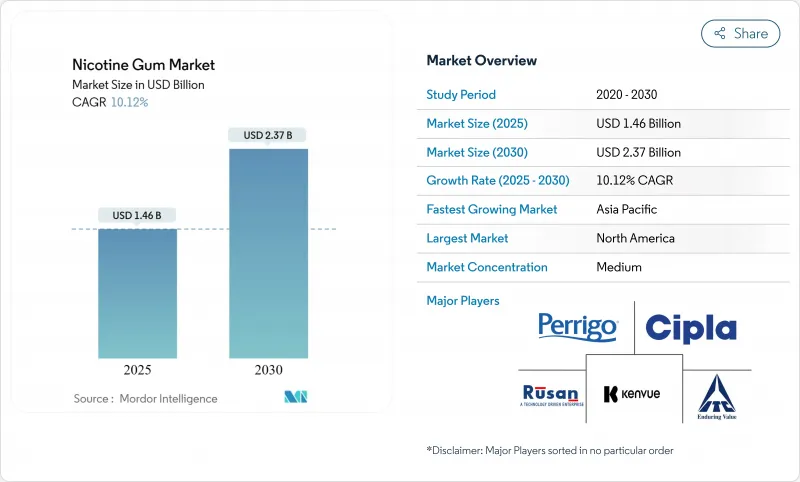

니코틴 껌 시장은 2025년에 14억 6,000만 달러로 추정되고, 2030년에는 CAGR 10.12%로 성장할 전망이며, 23억 7,000만 달러에 이를 것으로 예측됩니다.

담배 관련 질환의 감소에 주력하는 헬스케어 지불자, 금연 방법에 관한 규제 요건, 약물 요법의 통합이 시장 성장의 원동력이 됩니다. 금연을 시도하는 개인이 증가함에 따라 니코틴 대체 요법(NRT) 제품에 대한 세계 수요가 증가하고 있습니다. 이 성장은 견고한 헬스케어 시스템과 담배 규제 정책을 가진 지역에서 두드러집니다. 담배세, 금연 프로그램, 금연 캠페인 등 정부의 이니셔티브가 NRT 시장을 확대하고 있습니다. 제조업체 각 회사는 새로운 맛과 코팅 기술을 통해 제품의 선호도를 향상시키고 있습니다. 디지털 약국은 규정 준수를 유지하면서 제품에 대한 접근성을 높입니다. FDA는 경구제 신제품을 계속 승인하고 시장 경쟁을 격화시키고 있습니다. 이러한 규제 지원을 통해 제약 회사는 연구개발 투자를 촉구하고 있습니다. 금연 보조제에 대한 보험 적용 확대와 담배 관련 건강 위험에 대한 인식이 높아짐에 따라 시장 확대가 더욱 강화되고 있습니다.

흡연과 관련된 건강 위험에 대한 인식이 높아짐에 따라 금연 제품 및 서비스 시장의 성장이 이어지고 있습니다. 폐암, 심장병, 호흡기질환, 부류연기의 영향 등 이러한 리스크에 대한 소비자의 이해가 의지의 힘에만 의존하는 것이 아니라 근거 기반 솔루션에 대한 수요를 높이고 있습니다. 흡연률은 많은 지역에서 감소하고 있지만 인구 증가로 흡연자의 총 수가 증가하고 있으며 니코틴 패치, 껌, 로치, 처방약 등 금연 보조제에 대한 수요가 유지되고 있습니다. 니코틴 중독은 라이프 스타일의 선택이 아니라 만성 질환이라는 의학계의 인식이 장기적인 니코틴 대체 요법(NRT)의 사용을 정당화하고 있습니다. 이러한 의학적 관점에서 시장은 단기적인 해결책에 그치지 않고 행동 지원, 상담 서비스, 디지털 헬스 애플리케이션을 포함한 종합적이고 장기적인 중독 관리 접근법으로 확대되고 있습니다.

정부의 담배 규제에 대한 노력은 과세, 규제, 금연 지원을 결합한 프레임워크를 통해 니코틴 껌 수요를 촉진합니다. 호주 정부는 2024년 4월에 새로운 담배 규제를 실시했습니다. 이러한 규제는 향미 첨가물을 제거하고 제품 패키지를 표준화함으로써 담배 제품의 매력과 호소력을 저하시키는 것을 목표로 합니다. 이 규정은 담배 회사가 광고를 통해 담배 약자를 타겟팅하는 것을 제한합니다. 이 규정은 담배 팩, 파우치 및 스틱 담배 치수를 표준화해야 합니다. 영국 정부는 2024년에 연간 7,000만 파운드를 금연 서비스에 배정하고 매년 36만 명의 금연을 지원하며 니코틴 대체 요법 시장을 확대하는 것을 목표로 하고 있습니다. 이 자금은 무료 니코틴 대체 제품, 상담 서비스, 디지털 지원 도구 및 고위험 집단을 위한 전문 프로그램을 제공합니다. WHO 담배 규제 프레임워크 협약은 국가와 지역 간의 표준화된 접근 방식을 통해 시장 개척을 지원하고 가격 설정, 포장, 금연 지원 프로그램에 대한 지침을 수립합니다. 이 틀은 국제 협력, 조사 공유, 담배 규제 조치의 규제 기준의 조화를 촉진합니다.

2025년 1월에 FDA가 20유형의 ZYN 니코틴 파우치 제품을 판매 허가한 것은 경구 니코틴 전달의 선택에 큰 변화를 가져왔습니다. 니코틴 파우치는 씹기의 필요성을 없애고 턱의 피로를 방지하며, 입술 밑에서 눈에 띄지 않고, 직장 환경에서 섬세함이 필요한 전문가에게 호소합니다. 흡연 행동을 재현하는 치료용 VAPE 기기는 전통적인 흡연 습관을 모방하는 효과가 있기 때문에 금연 외래로부터의 지지가 높아지고 있습니다. 이러한 새로운 제품 카테고리는 소비자의 관심을 여러 니코틴 전달 형식으로 분산시키기 때문에 니코틴 껌 제조업체는 시장에서의 지위를 유지하기 위해 확립된 임상적 배경, 입증된 안전 기록, 관리된 투여 메커니즘을 강조할 수밖에 없습니다. 이러한 대체 니코틴 공급 시스템의 출현은 전통적인 니코틴 대체 요법 시장에 추가 경쟁 압력을 낳습니다.

2024년에는 3mg 미만이 압도적인 점유율을 차지하고 니코틴 껌 시장 점유율의 67.33%를 차지했습니다. 이 장점은 전신 노출량을 줄이고자 하는 사용자의 선호와 2mg 제품을 선호하는 약국의 재고 패턴이 확립되어 있기 때문입니다. 이 부문은 기존 제조업체에 안정적인 수익을 제공하고 금연을 시도하는 새로운 사용자의 첫 번째 옵션이 되었습니다. 그러나 임상 처방 패턴은 진화하고 있습니다. 의료 시설은 현재 니코틴 의존성의 Fagerstrom 테스트를 실시하고, 치료를 개별화하며, 연구에 의해 일반적인 재발 요인으로 확인된 과소 투여를 방지하고 있습니다.

3mg 이상의 부문은 가장 높은 성장률을 나타내며, 2030년까지 CAGR 9.35%로 성장이 예측됩니다. 헤비 스모커는 금연 후 72시간의 금단 증상을 다루기 때문에 높은 초기 혈장 농도가 필요합니다. 4mg 껌이 퇴원시 패키지에 포함되면 금연 프로그램에서 환자의 정착률이 향상되어 환자가 집으로 돌아온 후에도 처방전 보충이 계속됩니다. 제조업체는 맛과 인후 불편에 대한 이전의 사용자 우려를 해결하기 위해 텍스처를 강화한 이중층 구조의 고용량 제제를 개발했습니다. 이와 같은 고용량으로의 전환으로 니코틴 껌 시장에서는 평균 판매 가격이 상승하고 조익률이 향상되고 있습니다.

민트는 깔끔한 뒷맛과 약국 채널에서의 확립된 존재감에 의해 지원되고, 2024년 판매액의 45.34%를 차지했으며, 시장의 리더를 유지했습니다. 민트 맛의 니코틴 껌은 그 매력과 효과를 높이는 몇 가지 요인으로 시장을 독점하고 있습니다. 민트의 상쾌하고 청량감이 있는 감각은 니코틴의 쓴맛을 숨길 뿐만 아니라, 유저에게 껌을 보다 즐겁게 하고 있습니다. 소비자의 강한 수요에 부응하는 대형 제조업체는 자사의 포트폴리오에 민트의 바리에이션을 우선적으로 채용해, 브랜드 인지를 확실한 것으로 해, 널리 입수할 수 있도록 하고 있습니다. 니코틴 강도가 2mg, 4mg, 6mg인 민트향 껌은 다양한 니코틴 의존 수준에 대응하고, 금연을 목표로 하는 사람에게 맞는 지원을 제공합니다. 또한 시장 동향은 무당과 저칼로리 민트 옵션 등 혁신의 급증을 강조하고 있으며, 특히 건강 지향 소비자들 사이에서 그 매력이 높아지고 있습니다.

과일 카테고리는 풍미의 다양화로 인해 CAGR 9.69%로 성장할 전망입니다. 과일 맛의 프리미엄 제품은 재구매 빈도가 높고 금연 성공률이 향상되었습니다. 제조업체는 규제 파라미터의 범위 내에서 성인 소비자를 타겟으로 한 미묘한 온감 프로파일을 개발함으로써 대응하고 있습니다. 첨단 코팅 및 코어 기술은 향미료의 지속적인 방출을 가능하게 하여 완전한 소비 시간과 니코틴 흡수의 향상을 촉진하여 니코틴 껌 시장에서 소비자의 정착율 향상에 기여하고 있습니다.

북미는 2024년 매출의 84.69%를 차지했으며, 종합적인 보험 적용, 병원 기반 옵트아웃 프로토콜, 확립된 소매 네트워크가 견인하고 있습니다. 인디애나주의 'Quit Now' 프로그램에서는 2023년에 니코틴 치환요법과 상담을 병용했을 경우의 금연률이 40%였던 반면, 단독으로는 4-7%였다고 보고되었습니다. 캐나다 규제에서는 특정 제품에 대한 약사의 참여가 의무화되어 있으며 접근성을 유지하면서 전문가의 감시가 이루어지고 있습니다. FDA 인증 파우치와 치료 VAPE가 경쟁을 늘리는 반면, 니코틴 껌은 자체 투여 기능과 경구 만족감을 선호하는 강력한 사용자 기반을 유지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.66%로 가장 높은 성장률을 보일 전망입니다. 이 성장은 특히 저중소득 국가에서 높은 흡연율에 기인합니다. 남아시아 시장은 금연 프로그램의 큰 격차가 설문 조사에 제시되어 있기 때문에 큰 잠재력을 가지고 있습니다. 이러한 시장에서는 보다 효과적인 금연 전략을 개발하기 위해 금연 추진 단체, 정책 입안자, 의료 전문가의 협력을 강화해야 합니다.

유럽에서는 확립된 헬스케어 시스템이 안정적인 수요를 유지하고 있습니다. 영국에서는 지역 금연 서비스와 흡연자에게 니코틴 껌과 같은 대체품을 제공하는 'Swap to Stop' 프로그램에 매년 자금이 제공됩니다. 동유럽에서는 구매력이 낮기 때문에 더 작고 저렴한 포장 형태에 기회가 있습니다. 남미, 아프리카, 중동은 정부가 세계보건기구(WHO)의 권고를 실시함에 따라 성장할 가능성이 있지만, 헬스케어 시스템의 개발은 여전히 중요합니다. 국제 기업은 금연 이니셔티브를 위해 지역의 비정부 조직과 제휴하여 니코틴 껌 시장의 존재를 확대하고 있습니다.

The nicotine gum market reached USD 1.46 billion in 2025 and is projected to reach USD 2.37 billion by 2030, at a CAGR of 10.12%.

Healthcare payers' focus on reducing tobacco-related diseases, regulatory requirements for cessation methods, and pharmacotherapy integration drive market growth. Global demand for nicotine replacement therapy (NRT) products has risen as more individuals attempt to quit smoking. This growth is significant in regions with robust healthcare systems and tobacco control policies. Government initiatives, including cigarette taxes, cessation programs, and anti-smoking campaigns, expand the NRT market. Manufacturers are improving product palatability through new flavors and coating technologies. Digital pharmacies enhance product accessibility while maintaining regulatory compliance. The FDA continues to approve new oral products, increasing market competition. This regulatory support has prompted pharmaceutical companies to invest in research and development. The market expansion is further supported by increased insurance coverage for cessation products and heightened awareness of tobacco-related health risks.

The increasing awareness of smoking-related health risks drives the growth of the smoking cessation products and services market. Consumers' understanding of these risks, including lung cancer, heart disease, respiratory problems, and secondhand smoke effects, has increased the demand for evidence-based solutions over reliance on willpower alone. While smoking prevalence has decreased in many regions, population growth has led to a higher total number of smokers, maintaining the demand for cessation aids such as nicotine patches, gums, lozenges, and prescription medications. The medical community's recognition of nicotine dependence as a chronic condition, rather than a lifestyle choice, has validated the use of long-term nicotine replacement therapies (NRTs). This medical perspective has expanded the market beyond short-term solutions to include comprehensive, long-term addiction management approaches, incorporating behavioral support, counseling services, and digital health applications.

Government tobacco control initiatives drive nicotine gum demand through frameworks that combine taxation, regulation, and cessation support. The Australian government implemented new tobacco control regulations in April 2024 . These regulations aim to reduce the appeal and attractiveness of tobacco products by eliminating flavor additives and standardizing product packaging. The measures restrict tobacco companies' ability to target vulnerable populations through advertising. The regulations mandate standardized dimensions for tobacco packs, pouches, and cigarette sticks. The UK government allocated GBP 70 million annually to stop smoking services in 2024, aiming to help 360,000 people quit each year, expanding the nicotine replacement therapy market . The funding provides free nicotine replacement products, counseling services, digital support tools, and specialized programs for high-risk populations. The WHO Framework Convention on Tobacco Control supports market development through standardized approaches across jurisdictions, establishing guidelines for pricing, packaging, and cessation support programs . The framework promotes international cooperation, research sharing, and harmonized regulatory standards for tobacco control measures.

The FDA's marketing authorization for twenty ZYN nicotine pouch products in January 2025 marks a significant shift in oral nicotine delivery options . Nicotine pouches eliminate the need for chewing, prevent jaw fatigue, and remain discreet under the lip, appealing to professionals who require subtlety in their workplace environments. Therapeutic vaping devices that replicate smoking behaviors receive increasing support from cessation clinics due to their effectiveness in mimicking traditional smoking habits. These new product categories divide consumer attention across multiple nicotine delivery formats, compelling nicotine gum manufacturers to highlight their established clinical background, proven safety record, and controlled dosage mechanisms to maintain their market position. The emergence of these alternative nicotine delivery systems creates additional competitive pressure in the traditional nicotine replacement therapy market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The below 3 mg tier dominated in 2024, capturing 67.33% of the nicotine gum market share as light and moderate smokers selected gradual tapering programs. This dominance stems from user preference for lower systemic exposure and established pharmacy inventory patterns favoring 2 mg products. The segment provides stable revenue for existing manufacturers and serves as an initial option for new users attempting to quit. However, clinical prescribing patterns are evolving. Healthcare facilities now implement the Fagerstrom Test for Nicotine Dependence to personalize treatment and prevent under-dosing, which studies have identified as a common relapse factor.

The above 3 mg segment demonstrates the highest growth rate, with a projected 9.35% CAGR through 2030. Heavy smokers require the elevated initial plasma concentration to manage withdrawal symptoms during the crucial first 72 hours after quitting. Improved patient retention occuers in cessation programs when 4 mg gum is included in discharge packages, resulting in continued prescription refills after patients return home. Manufacturers have developed bi-layer high-dose formulations with enhanced texture to address previous user concerns about taste and throat discomfort. This shift toward higher doses increases the average selling price and enhances gross margins in the nicotine gum market.

Mint maintains market leadership with 45.34% of 2024 sales value, supported by its clean aftertaste and established presence in pharmacy channels. Mint-flavored nicotine gums dominate the market, driven by several factors that enhance their appeal and effectiveness. The refreshing and cooling sensation of mint not only masks the bitter taste of nicotine but also makes the gum more enjoyable for users. Leading manufacturers, responding to strong consumer demand, prioritize mint variants in their portfolios, ensuring robust brand recognition and widespread availability. With nicotine strengths of 2 mg, 4 mg, and 6 mg, mint-flavored gums cater to varying levels of nicotine dependence, offering tailored support for those looking to quit. Additionally, market trends highlight a surge in innovations, such as sugar-free and low-calorie mint options, amplifying their allure, particularly among health-conscious consumers.

The fruit category exhibits 9.69% CAGR through flavor diversification. Premium fruit-flavored variants demonstrate higher repurchase frequency and improved cessation success rates. Manufacturers respond by developing subtle warming profiles that target adult consumers within regulatory parameters. Advanced coated-core technology enables sustained flavor release, promoting complete consumption time and enhanced nicotine absorption, contributing to increased consumer retention in the nicotine gum market.

The Nicotine Gum Market Report is Segmented by Dosage (Below 3 Mg and Above 3 Mg), by Flavor (Mint, Fruit, and Others), by End User (Male and Female), by Distribution Channel (Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores, and Other Distribution Channels), and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 84.69% of revenue in 2024, driven by comprehensive insurance coverage, hospital-based opt-out protocols, and established retail networks. Indiana's "Quit Now" program reported 40% quit rates when combining nicotine replacement therapy with counseling, compared to 4-7% for unaided attempts in 2023. Canadian regulations require pharmacist involvement for specific products, providing professional oversight while maintaining accessibility. While FDA-cleared pouches and therapeutic vapes increase competition, nicotine gum maintains a strong user base who prefer its self-dosing capability and oral satisfaction.

The Asia-Pacific region demonstrates the highest growth rate at 10.66% CAGR through 2030. This growth stems from high smoking rates, particularly in lower-middle-income countries. South Asian markets offer significant potential, as research indicates major gaps in smoking cessation programs. These markets require improved coordination between anti-smoking organizations, policymakers, and healthcare professionals to develop more effective cessation strategies.

Europe maintains consistent demand through established healthcare systems. The United Kingdom provides annual funding for local smoking cessation services and the "Swap to Stop" program, which offers alternatives like nicotine gum to smokers. In Eastern Europe, lower purchasing power creates opportunities for smaller, more affordable packaging formats. South America, Africa, and the Middle East present growth potential as governments implement World Health Organization recommendations, though healthcare system development remains crucial. International companies partner with regional non-governmental organizations on smoking cessation initiatives to expand nicotine gum market presence.