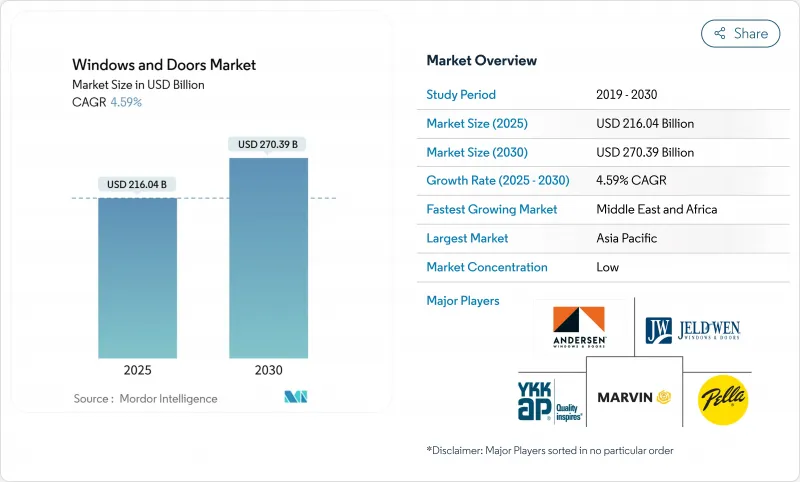

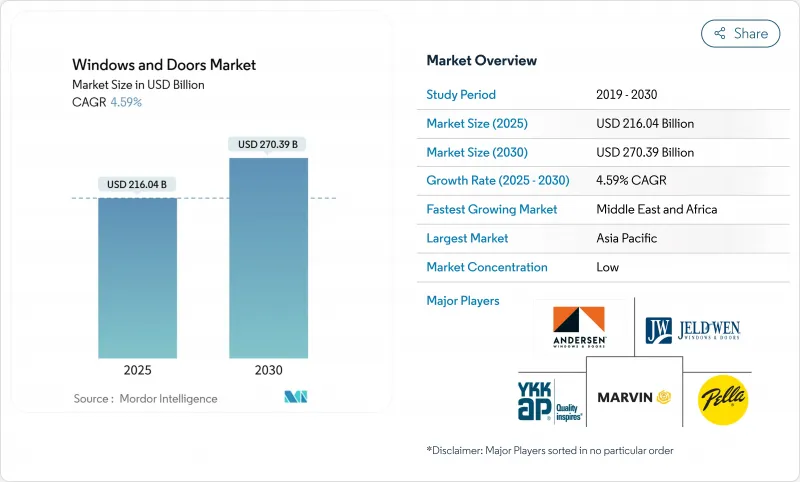

창호 시장의 2025년 시장 규모는 2,160억 4,000만 달러로 추정되고, 2030년에는 2,703억 9,000만 달러에 이를 것으로 예측되며, CAGR 4.59%로 성장할 전망입니다.

에너지 효율적인 건물 외벽에 대한 왕성한 수요, 성능 규정 강화 및 꾸준한 보수 비용이 이러한 성장을 지원합니다. ENERGY STAR 버전 7.0 업데이트는 이미 미국의 한랭지에서 U-팩터 한계를 0.22로 밀어 올려 삼중 창호 및 고급 프레임 워크를 동기화했습니다. EU의 건축물 에너지 성능 지령(EPBD)의 병행한 기세는 2030년까지 제로 에미션 건축물을 목표로 하는 사양에 방향타를 끊고 있어, 주택과 상업 프로젝트 모두에서 고성능 창호의 채용을 가속시키고 있습니다. 공급 측면 이동, 특히 경량 프레임 옵션, 모듈 구조, 스마트 유리로의 업그레이드는 알루미늄과 노동력 부족이 뿌리 깊은 역풍임에도 불구하고 설계 옵션을 넓히고 리드 타임을 단축하고 있습니다. 재료의 혁신, 자동화된 제조, 지역적 완성도를 결합할 수 있는 제조업체는 창호 시장에서 사양 주도 수요의 다음 파도를 포착할 수 있는 입장에 있습니다.

차입 비용이 증가함에 따라 대부분의 주택 소유자는 유리한 금리에 고정되어 재량 자금을 이전보다는 업그레이드로 돌리고 있습니다. 리모델링 지출은 2024년에 급증하였고, 2025년에도 5% 성장을 유지할 것으로 예측됩니다. 이는 북미와 유럽 주택 기반의 노후화에 힘입어 20-39년 사이에 창틀 교체 시기를 맞이하기 때문입니다. 미국 해안의 카운티에서 허리케인 부흥 프로젝트의 절반 가까이는 창호 개조를 포함하고 있으며 보호 기능과 에너지 절약 기능의 이중 가치가 부각되고 있습니다. 또, 리폼 전문가는 보다 넓은 개구부, 보다 낮은 문턱의 높이, 인간 공학에 근거한 철물 등을 좋아하는 '고령화 대응'의 요망이 급증하고 있는 것에도 주목하고 있습니다. 이러한 사용 패턴을 통해 창호 시장은 소비자의 웰니스 및 탄력성의 우선 순위에 확고하게 일치합니다.

성능 기준은 주요 경제국 전체에서 협조적으로 강화되고 있습니다. 미국에서 ENERGY STAR V7.0은 U 계수를 이전 사이클에서 15%까지 낮추어 추운 곳에서 트리플 페인 구조를 실질적으로 표준화합니다. 2024년 국제 에너지 절약 기준에서는 공기 누설의 상한을 0.35 cfm/ft2로 하고, 웨더 스트립과 프레임 설계의 개선을 요구하고 있습니다. 유럽에서는 EPBD가 개정되어 2030년 이후의 신축 건축물에 대한 제로 에미션 요건과 기존 스톡에 대한 단계적 개수 목표가 포함되었습니다. 시장의 매력인 세액공제와 광열비 할인은 초기 비용의 일부를 상쇄하기 때문에 투자 회수가 빨라 창호 시장에서 제품의 차별화가 진행됩니다.

에너지 비용 상승 및 제련소 운영 중단으로 팬데믹 후 수요가 회복되자마자 알루미늄 공급이 줄어들어 평균 프리미엄이 상승하고 리드 타임이 길어졌습니다. PVC(PVC) 제조업체는 투입 비용 상승과 특히 환경 감시가 어려운 유럽에서 염소 생산 규제를 강화하기 위해 고민하고 있습니다. 변동 위험을 헤지하기 위해 제조업체는 재생 빌렛, 열가소성 수지로 강화된 프로파일 및 지역 조달 협정으로 축발을 옮깁니다. 강도를 희생하지 않고 금속 사용량을 줄일 수 있는 경량 복합 프레임은 여전히 점유율을 늘리고 있습니다. 그럼에도 불구하고 가격 변동은 소규모 가공업자의 금리를 압박하고 프로젝트 수주를 둔화시키고 창호 시장의 일부 성장을 억제합니다.

도어는 2024년 매출의 58.56%로 대부분을 차지했으며, 모든 건축 유형에서 그 기초적인 역할을 담당하고 있는 것으로 확인되었습니다. 보안 도어, 내화 어셈블리, 스마트 잠금 장치는 주기적인 감속 시에도 상대적으로 안정적인 수요를 유지하는 교체 빈도를 유지합니다. 반대로 창문은 엄격한 열 이득 제한과 유리를 통해 태양에너지를 직접 흡수하는 건물 일체형 태양광 발전의 상승으로 CAGR 7.49%로 성장을 웃돌고 있습니다. 이 풀 스루 효과로 창문은 창호 시장의 기술적 급선봉이 되었습니다.

도어 제조업체는 멀티 포인트 록, 내충격 패널, 원활한 스마트 홈의 통합에 투자하고 있지만, 가장 이익이 큰 것은 일렉트로크로믹 코팅과 태양광 하베스팅 중간막을 융합시킨 첨단 창 솔루션으로 이행하고 있습니다. 로렌스 버클리 국립연구소는 이러한 설치로 인한 건물 전체의 에너지 절약율을 최대 15.9%로 기록하고 있으며, 이 지표는 가격이 비싸고 짧은 투자 회수를 뒷받침하고 있습니다. 그 결과 창문 분야 시장 세분화는 2025년 890억 달러에서 2030년 1,230억 달러로 확대될 것으로 예측됩니다.

금속 프레임, 특히 알루미늄은 그 유리한 강도 대 중량비, 슬림한 시선, 재활용성으로 인해 2024년에는 46.62%의 매출을 차지합니다. 커튼월의 고층 빌딩, 병원, 교통의 요점에서는 문과 유리로 된 외관 모두에 알루미늄 프레임이 지정되는 것이 대부분입니다. 그러나 CAGR 8.73%라는 가장 빠른 성장을 기록하고 있는 것은 플라스틱/uPVC 프로파일이며, 예산 중시와 신속한 시공이 가장 중요한, 급성장 중인 교외 및 도시 근교의 주택가입니다. 유리 섬유와 강철의 미세 보강재를 포함한 최신의 배합은 강성을 손상시키지 않고 열 성능을 발휘해, PVC의 구조적 한계에 대한 이전의 비판에 응하고 있습니다.

라이프사이클의 조사에 의해 생산자는 프탈산에스테르 프리, 무연 안정제나, 프로파일의 단재를 새로운 압출재로 바꾸는 클로즈드 루프 리사이클에 대한 대처를 진행하고 있습니다. 한편, 신흥의 목재 플라스틱 복합재(WPC)나 유리 섬유 프레임은 알루미늄의 강성과 비닐의 단열성에서 중간적인 역할을 합니다. 이러한 배경에서 PVC 시스템의 창호 시장 규모는 2025년부터 2030년 사이에 140억 달러가 추가될 것으로 예상되는 반면 금속은 주요 알루미늄의 생산 능력 제약에 따라 성장이 완만해질 것으로 예측됩니다. EU에서 2030년 이후 PVC 단계적 감소 가능성에 대한 규제 논의는 전략적 위험을 창출하지만 재활용 가능한 폴리머 블렌드 및 바이오 폴리머 블렌드의 기술 혁신을 촉진하는 것입니다.

창호 시장은 제품 유형별(도어, 창문), 소재 유형별(목재, 금속, 플라스틱 및 UPVC와 복합재), 용도별(스윙, 슬라이드, 기타), 최종 사용자별(주택 및 비주택(상업, 산업, 시설)), 설치 유형별(신축, 교환 및 수리), 지역별로 분류됩니다. 시장 예측은 금액(달러)과 수량(단위)으로 제공됩니다.

아시아태평양은 2024년 매출의 42.13%를 차지했으며, 급속한 도시 건설 및 에너지 절약으로 기후 변화에 강한 건설에 대한 정책적 인센티브가 그 요인이 되고 있습니다. 중국, 인도, 인도네시아의 국가건축기준법은 허용 U값을 단계적으로 낮추고 있으며, 열 균열 프레임과 Low-E 단열 유리에 유리한 기준선을 설정하고 있습니다. 현지 패브리케이터는 단위화된 외관을 인근 시장으로 수출하는 것이 늘어나고 있어, 지역내 공급 체인을 강화해, 창호 시장의 물류 비용을 삭감하고 있습니다.

북미는 왕성한 개수비와 성숙해지고 있는 오프사이트 주택 부문에 밀려 시장 규모로 2위에 랭크되고 있습니다. ENERGY STAR 세금 공제와 주 수준의 폭풍우 대책 보조금은 주택 착공 건수의 변동에도 불구하고 수요를 견조하게 유지하고 있습니다. 숙련 노동자의 부족은 여전히 성장의 주요 병목이지만, 주요 공장에서 자동화 속도의 상승과 통합 설치 프로그램이 사이클 지연을 완화하고 있습니다. 캐나다와 미국 북부에서는 난방 부하를 줄이려는 집합 주택 프로젝트에서 트리플 유리가 빠르게 주류가되고 있습니다.

유럽에서는 EPBD가 2030년 이후의 신축 부동산에 제로 방출 목표를 의무화하고 있기 때문에 절대 슬라이스는 작지만 높은 마진 가능성이 있습니다. 또한 최저 에너지 성능 기준은 비주택 재고 중 최악의 16%가 같은 해까지 업그레이드되어 꾸준한 리노베이션 파이프라인을 확보합니다. 검증 가능한 환경 제품 선언 및 순환경제 프레임워크를 갖춘 제조업체는 우선 조달 점수를 얻을 수 있습니다. 창호 시장에서는 파리와 베를린과 같은 밀집한 도시에서는 소음 감쇠 유닛에 대한 프리미엄 수요가 보이고, 지중해 연안의 리조트에서는 적응형 차광 패키지가 표준이 되고 있습니다.

중동 및 아프리카는 2030년까지 CAGR 7.10%로 가장 빠른 성장이 전망되며, 대규모 접객, 헬스케어, 교육 프로젝트에 지지되고 있습니다. 혹독한 지역에서는 실내 및 실외 혼합 거주 패턴에 해당하는 넓은 스윙 도어 시스템과 결합된 태양광 제어 글레이징이 필요합니다. 정부에 의한 그린빌딩 인증의 의무화와 에너지 요금의 상승으로 저방사율 코팅으로의 이동이 가속화되고 있습니다. 걸프 국가의 현지 조립 기지가 동아프리카 회랑에 서비스를 제공하기 시작했으며 리드 타임을 단축하여 창호 시장의 지역 회복력을 강화하고 있습니다.

남미는 브라질, 콜롬비아, 칠레에서 도시의 고밀도화에 힘입어 견조한 상승을 보여줍니다. 고인플레이션은 단기 재량 지출을 제한하고 있지만 장기적인 인프라 권리가 제도적 프로젝트를 전진시키고 있습니다. 칠레와 페루의 성능 규정이 개정되어 고지의 신축에는 복층 유리가 의무화되어 에너지에 배려한 창의 대응 가능 시장이 더욱 확대되었습니다.

The windows and doors market was valued at USD 216.04 billion in 2025 and is forecast to reach USD 270.39 billion by 2030, posting a 4.59% CAGR.

Strong demand for energy-efficient building envelopes, tighter performance codes, and steady renovation spend underpin this growth. The ENERGY STAR Version 7.0 update is already pushing U-factor limits toward 0.22 in colder U.S. zones, motivating triple-pane glazing and advanced framing. Parallel momentum in the EU's Energy Performance of Buildings Directive (EPBD) is steering specifications toward zero-emission buildings by 2030, accelerating adoption of high-performance fenestration across both residential and commercial projects. Supply-side shifts-especially light-weight framing options, modular construction, and smart-glass upgrades-continue to widen design choices and shorten lead times, even as aluminum and labor shortages remain persistent headwinds. Manufacturers able to combine material innovation, automated fabrication, and regional fulfillment are positioned to capture the next wave of specification-driven demand in the windows and doors market.

Elevated borrowing costs have locked most homeowners into favorable rates, channeling discretionary capital toward upgrades rather than relocation. Remodel spending grew sharply in 2024 and is projected to maintain 5% growth in 2025, supported by an aging North American and European housing base, much of which crosses the 20- to 39-year prime replacement window for fenestration. Nearly half of hurricane recovery projects in coastal U.S. counties now include window or door upgrades, highlighting the dual value of protective and energy-saving features. Remodeling professionals also note a surge in "aging-in-place" requests that favor wider clear openings, lower sill heights, and ergonomic hardware. These usage patterns keep the windows and doors market firmly aligned with consumer wellness and resilience priorities.

Performance codes are tightening in a coordinated fashion across major economies. In the United States, ENERGY STAR V7.0 pushes U-factors down 15% from the previous cycle, practically standardizing triple-pane construction in cold climates. The 2024 International Energy Conservation Code now caps air leakage at 0.35 cfm/ft2, demanding improved weather-stripping and frame design. Europe's revised EPBD locks in zero-emission requirements for new buildings starting 2030, along with staged renovation targets for the existing stock. Attractive tax credits and utility rebates offset part of the upfront cost, fostering faster payback and heightening product differentiation within the windows and doors market.

Energy cost spikes and smelter curtailments have trimmed aluminum supply just as post-pandemic demand recovered, lifting average premiums and lengthening lead times. PVC producers also struggle with higher input costs and stricter chlorine-production rules, especially in Europe, where environmental scrutiny is intense. To hedge volatility, manufacturers are pivoting toward recycled billet, thermoplastic-reinforced profiles, and regional sourcing agreements. Lightweight composite frames, which reduce metal use without sacrificing strength, continue to gain share. Nonetheless, price swings squeeze smaller fabricators' margins, slowing project awards and tempering growth in parts of the windows and doors market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Doors generated the majority of 2024 revenue at 58.56%, confirming their foundational role in every building type. Security doors, fire-rated assemblies, and smart locks sustain a replacement cadence that keeps demand relatively stable even during cyclical slowdowns. Conversely, windows outpace in growth at a 7.49% CAGR thanks to stringent heat-gain limits and the rise of building-integrated photovoltaics, which capture solar energy directly through glass. This pull-through effect positions windows as the technological spearhead of the windows and doors market.

Door makers invest in multi-point locking, impact-rated panels, and seamless smart-home integration; however, the highest margins are migrating to advanced window solutions that fuse electro-chromic coatings with solar-harvesting interlayers. Lawrence Berkeley National Laboratory recorded up to 15.9% whole-building energy savings from such installations, a metric that drives premium pricing and short paybacks. As a result, the windows and doors market size for the window segment is projected to rise from USD 89 billion in 2025 to USD 123 billion by 2030, even though the door segment will still dominate on volume.

Metal frames, particularly aluminum, held 46.62% revenue in 2024 because of their favorable strength-to-weight ratio, slim sightlines, and recyclability. Curtain-wall high-rises, hospitals, and transport hubs nearly always specify aluminum frames for both doors and glazed facades. Yet plastic/uPVC profiles are capturing the fastest gains-8.73% CAGR-inside fast-growing suburban and peri-urban housing corridors where budget sensitivity and quick installation matter most. Updated formulations featuring embedded fiberglass or steel micro-reinforcements deliver thermal performance without compromising rigidity, answering earlier criticisms of PVC's structural limits.

Lifecycle scrutiny is pushing producers toward phthalate-free, lead-free stabilizers and closed-loop recycling commitments that turn profile off-cuts into new extrusions. Meanwhile, emerging wood-plastic composites and fiberglass frames offer a middle ground between aluminum's stiffness and vinyl's insulative edge. Against this backdrop, the windows and doors market size for PVC systems is projected to add USD 14 billion between 2025 and 2030, while metal growth moderates in line with primary-aluminum capacity constraints. Regulatory debates in the EU about potential PVC phase-downs beyond 2030 create strategic risk but also encourage innovation in recyclable and bio-based polymer blends.

The Windows and Doors Market is Segmented by Product Type (Doors, Windows), Material Type (Wood, Metal, Plastic / UPVC / Composite), Application (Swinging, Sliding, and More), End User (Residential and Non-Residential (Commercial, Industrial, Institutional)), Installation Type (New Construction, Replacement / Retrofit), Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific held 42.13% of 2024 revenue, anchored by rapid urban build-outs and policy incentives for energy-conserving, climate-resilient construction. National building codes in China, India, and Indonesia have progressively lowered allowable U-values, setting a lucrative baseline for thermally broken frames and low-e insulated glass. Indigenous fabricators increasingly export unitised facades to neighboring markets, strengthening intra-regional supply chains and shaving logistics costs for the windows and doors market.

North America ranks second in size, propelled by strong renovation expenditure and a maturing off-site housing segment. ENERGY STAR tax credits and state-level storm hardening grants keep demand solid despite fluctuating housing starts. Skilled-labor scarcity remains the main growth bottleneck; however, rising automation rates at major plants, plus integrated installation programs, are mitigating cycle delays. Across Canada and the northern United States, triple glazing is fast becoming the baseline for multi-family projects seeking lower heating loads.

Europe commands a smaller absolute slice but offers high margin potential because the EPBD mandates zero-emission targets for new builds from 2030. Minimum energy performance standards also force upgrades of the worst 16% of non-residential stock by that same year, ensuring a steady retrofit pipeline. Manufacturers with verifiable environmental product declarations and circular-economy frameworks stand to gain preferential procurement scores. The windows and doors market sees premium demand for noise-attenuating units in dense cities such as Paris and Berlin, while adaptive shading packages become standard in Mediterranean resorts.

Middle East & Africa records the fastest CAGR at 7.10% through 2030, underpinned by large-scale hospitality, healthcare, and education projects. Extreme heat zones require solar-control glazing paired with wide-swing door systems that accommodate mixed indoor-outdoor occupancy patterns. Government mandates for green-building certifications, plus rising energy tariffs, hasten the shift to low-emissivity coatings. Local assembly hubs in the Gulf are beginning to serve East African corridors, reducing lead times and bolstering regional resilience within the windows and doors market.

South America shows a steadier climb, supported by urban densification in Brazil, Colombia, and Chile. High inflation limits short-term discretionary spend, yet long-term infrastructure concessions keep institutional projects moving forward. Revised performance codes in Chile and Peru now prescribe double-glazing for new high-altitude construction, further enlarging the addressable market for energy-conscious fenestration.