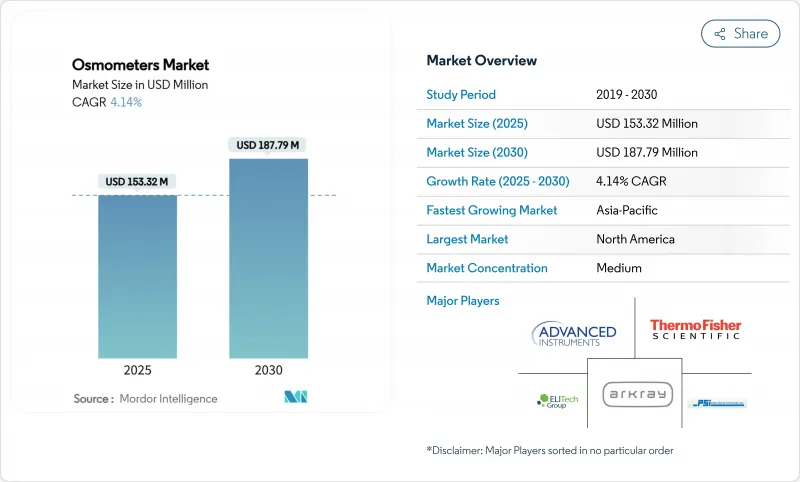

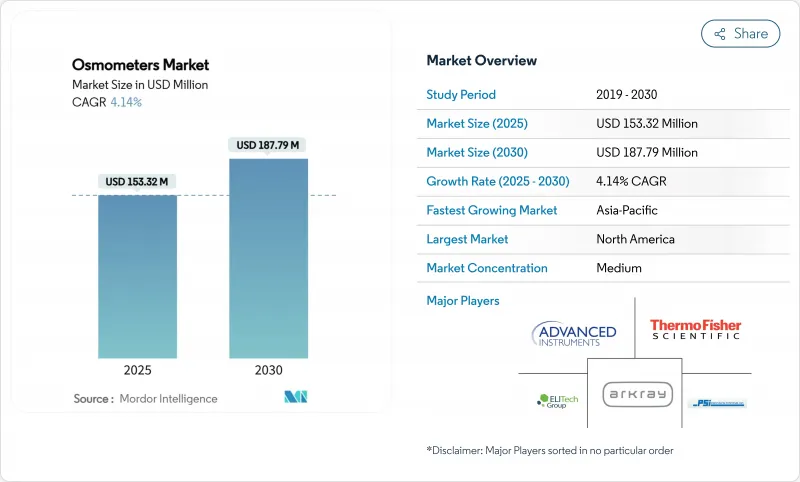

삼투압계 시장은 2025년에 1억 5,332만 달러, 2030년에는 1억 8,779만 달러에 이를 것으로 예측됩니다.

유럽연합의료기기규칙(EU MDR) 하에서 기기의 승인에 시간이 걸린다 하더라도, 검사실의 자동화, 컴플라이언스 규칙의 엄격화, 고농도 생물제제에 대한 바이오파마의 기울기가 수요를 뒷받침하고 있습니다. 고급 기기가 개발한 Nova Biomedical의 22억 달러를 인수한 전략적 통합은 복잡한 세계 규제를 수용할 수 있는 통합 분석 플랫폼에 대한 업계 전환을 보여줍니다. 한편, 공급 정지 6개월 전에 규제 당국에 사전 경고할 것을 제조업체에게 의무화하는 EU의 새로운 규칙은 모든 주요 공급업체의 리스크 관리 플레이북을 재구성하고 있습니다. 북미에서는 임상 인프라에 대한 지속적인 투자가 안정적인 교체 수요를 지지하는 한편, 아시아태평양에서는 최신화 추진이 동향 이상의 대수 성장을 가속하고 임피던스 기반 POC(Point of Care) 신규 진출기업과의 경쟁을 가속화하고 있습니다.

유럽의 실험실은 분석용 LC-MS, 화학 분석기, 검사 정보 시스템과 직접 연결되는 완전 자동화된 삼투압 측정 워크셀을 채택하여 수작업을 줄이고 교차 오염의 위험을 최소화합니다. 북아일랜드의 CoreLIMS 전주 전개는 원활한 통합으로 실시간 삼투압 데이터가 혈액은행 및 미생물학 모듈로 흘러들어 하루에 1,200개의 샘플 포인트 추적성이 향상됨을 보여줍니다. 공급업체는 현재 60 초 이내에 HL7 형식의 결과를 생성하는 "연결"삼투압계를 판매하고 있습니다. 따라서 삼투압계 시장은 소프트웨어, 사이버 보안 업데이트 및 원격 진단 번들과 관련된 평균 판매 가격 상승을 목격하고 있습니다. 북미의 핵심 레퍼런스 랩에서의 도입이 가장 진행되고 있지만, EU를 기반으로 하는 네트워크는 지역이 자금을 제공하는 디지털 헬스 프로그램을 통해 그 차이를 줄이고 있습니다.

첨단 치료의 세계 연구 개발 비용은 삼투압을 공정 분석의 최전선으로 끌어 올리고 있습니다. 최근의 임상시험은 생산자가 배양 도중에 삼투압을 타이밍 좋게 이동시켰을 때 아데노 관련 바이러스의 역가가 22% 튀는 것을 보여주고 있습니다. 만성 신장병의 유병률은 EU 성인 인구의 9%를 넘어 신속한 요삼투압 측정에 의존하는 분산 신장 기능 스크리닝의 필요성이 증가하고 있습니다. Nova Biomedical사의 CE 마크를 취득한 크레아티닌/eGFR 측정기는 삼투압과 신장 마커를 2분간의 검사로 조합해, 지방의 의사가 중앙 검사실의 서포트 없이 환자를 분류할 수 있게 해줍니다. 따라서 높은 질병 부담이 삼투압계 시장의 임상 설치 베이스를 증폭하여 조달 기준을 속도, 분석 깊이, 인체공학적 디자인이 융합된 기기로 전환시킵니다.

단백질 부하가 150mg/mL를 초과하면 응고점 사이클이 3분을 넘어 이미 연간 8억 건의 검사를 실시하고 있는 메가랩의 1일 처리 능력이 저하됩니다. 증기압 장치는 정밀도를 향상시키지만 장시간의 평형화를 필요로 하기 때문에 15분의 턴어라운드를 양도할 수 없는 STAT 벤치에는 거의 들어가지 않습니다. 이 트레이드 오프로 인해 일부 구매자는 비접촉 굴절 센서로 유도되어 신속 반응 틈새 시장에서 대응 가능한 점유율을 침식합니다.

응고점 측정기는 2024년 삼투압계 시장 점유율의 68.78%를 차지하며 수십년에 걸친 임상적 신뢰와 명확한 규제 당국의 승인에 지지되고 있습니다. 임피던스 시스템은 현재의 삼투압계 시장 규모의 단지 일부에 불과하지만, 중요한 관리, 투석 및 동물 용도에 적합한 휴대용 설계로 CAGR 7.73%로 성장하고 있습니다. 증기압 장치는 좁은 고농도 생물 제제의 틈새를 차지하며, 그 성능의 높이는 사이클 시간의 느림을 보완합니다. 제조업체는 현재 유지 보수 계약, 원격 펌웨어 푸시 및 자동 교정 기능을 번들로 제공하여 컴플라이언스 비용을 예측할 수 있습니다.

기술 업데이트는 연결성과 서비스에 대한 업계의 움직임으로 호응하고 있습니다. 임피던스 장비는 신생아 스크리닝 및 동물 건강에 필수적인 20μL 이하의 샘플로 95.5%의 정확도를 달성하여 Bluetooth 지원 환자용 앱에 직접 연결할 수 있습니다. 프리징 포인트 리더는 바코드 스캐너, 재시약 로트 추적성, AI 기반 품질 관리 경보를 통합하여 대응하여 비표준 재시약을 줄입니다. 증기압 공급자는 유전자 치료 CDMO를 유치하는 스테인레스 스틸의 접액 경로와 21 CFR Part 11의 감사 추적에 주력하고 있습니다.

2024년 삼투압계 시장의 60.36%는 단일 샘플 분석기였습니다. 그러나 CAGR 8.12%로 상승하고 있는 다검체 분석장치에는 로보틱 로드 드로어나 LIS 허브가 탑재되어 시간당 최대 90개의 튜브를 처리할 수 있게 되었습니다. 따라서 높은 처리량 단위 시장 규모는 병원이 모듈식 자동화를 중심으로 핵심 실험실을 재설계함에 따라 예측 기간 동안 과거 평균을 초과해야 합니다.

유럽의 시설에서는 스마트폰형 터치스크린을 갖춘 24대의 랙을 채택해, 1명의 검사기사가 전해질, 포도당, 삼투압 검사를 병행하여 감독할 수 있도록 하고 있습니다. 현지 의료 센터에서는 컴팩트한 단일 시료 검사 장비가 생존하고 있지만 공급업체는 클라우드 로깅, 간소화된 QC 및 원버튼 유지보수로 이들을 새로 고칩니다. 이러한 균형 잡힌 수요로 인해 두 범주는 적절하지만 처리량과 연결성으로 명확하게 차별화됩니다.

북미는 2024년 삼투압계 시장의 37.77%를 차지하며 상환 안정성과 시험량이 많아 꾸준한 업그레이드를 지원하고 있습니다. 이 지역은 CLIA 인증 실험실의 기초가 가장 두껍고 공정 분석 기술을 중시하는 바이오파마 회랑이 밀집되어 있는 것이 장점입니다. CAGR 7.98%로 성장하는 아시아태평양은 중국, 인도, 한국에서 국민건강보험 확대, 적극적인 생물제제 생산능력 증강, 침대사이드 검사 채택 증가로 이익을 얻고 있습니다. 유럽은 규제 병목 현상을 방해하면서도 자동화의 진전과 강력한 백신 파이프라인을 활용하여 경쟁력을 유지하고 있습니다. 중동 및 아프리카는 아직 개발도상이지만 병원건설 프로그램과 현지 장비 조립 인센티브가 결합되어 2자리대의 성장을 확보하고 있습니다.

싱가포르, 한국, 중국의 정부 보조금으로 높은 처리량으로 21 CFR Part 11에 대응하는 설비 투자가 진행됩니다. EU MDR의 장기화된 인증 사이클은 일부 제품 상시를 지연시키지만, 프리노티파이드 바디 전략을 가진 민첩한 공급업체에 여백을 생성합니다. 모든 지역에서 워크플로우를 압축하고 데이터 스트림을 통합하며 총 소유 비용을 줄이는 플랫폼에 대한 수요가 증가하고 있습니다.

The osmometers market reached USD 153.32 million in 2025 and is forecast to climb to USD 187.79 million by 2030, reflecting a steady 4.14% CAGR that signals a mature but opportunity-rich landscape.

Demand is buoyed by laboratory automation, stricter compliance rules and biopharma's tilt toward high-concentration biologics, even as device approvals take longer under the European Union Medical Device Regulation (EU MDR). Strategic combinations-such as Advanced Instruments' pending USD 2.2 billion purchase of Nova Biomedical-underline an industry pivot toward integrated analytical platforms able to navigate complex global regulations. Meanwhile, the new EU rule that forces manufacturers to pre-alert regulators six months before supply interruptions is reshaping risk-management playbooks for every major supplier. In North America, continued clinical infrastructure investment supports stable replacement demand, while Asia-Pacific's modernization push drives above-trend unit growth and fuels competition from impedance-based, point-of-care (POC) newcomers.

European laboratories are adopting fully automated osmometry workcells that link directly with analytical LC-MS, chemistry analyzers and laboratory information systems, shrinking manual steps and minimizing cross-contamination risks. A province-wide CoreLIMS roll-out in Northern Ireland has shown how seamless integration allows real-time osmolality data to flow into blood-bank and microbiology modules, improving traceability across 1,200 sample points per day. Vendors now position "connected" osmometers that generate HL7-formatted results in under 60 seconds, a capability that resonates with hospitals chasing zero-waste, high-throughput operations. The osmometers market is thus witnessing higher average selling prices tied to software, cyber-security updates and remote diagnostics bundles. Adoption is sharpest in North America's core reference labs, but EU-based networks are narrowing the gap through region-funded digital health programs.

Global R&D outlays in advanced therapies push osmolality to the front line of process analytics, with recent trials showing adeno-associated virus titers jump 22% when producers orchestrate timed osmolality shifts mid-culture. Chronic kidney disease prevalence, now topping 9% of the EU adult population, heightens need for decentralized kidney-function screens that depend on rapid urine osmometry. Nova Biomedical's CE-marked creatinine/eGFR meter pairs osmolarity and kidney markers in a two-minute test, enabling rural physicians to triage patients without central lab support. High disease burden therefore amplifies the osmometers market's clinical installed base and shifts procurement criteria toward devices that blend speed, analytical depth and ergonomic design.

Freezing-point cycles surpass three minutes when protein loads exceed 150 mg/mL, throttling daily capacity inside mega-labs that already run 800 million tests annually. Vapor-pressure devices improve accuracy but require long equilibration; thus they seldom slot into STAT benches where 15-minute turnaround is non-negotiable. This trade-off steers some buyers to non-contact refractive sensors, eroding addressable share in rapid-response niches.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Freezing point instruments retained 68.78% of 2024 osmometers market share, underpinned by decades of clinical trust and clear regulatory acceptance. Impedance systems, though only a fraction of today's osmometers market size, are growing at 7.73% CAGR thanks to portable designs that suit critical care, dialysis and veterinary applications. Vapor-pressure units occupy a narrow high-concentration biologics niche where their performance premium offsets slower cycle times. Manufacturers now bundle maintenance contracts, remote firmware pushes and auto-calibration features to keep compliance costs predictable.

Technology updates echo industry moves toward connectivity and service. Impedance devices achieve 95.5% accuracy with sub-20 µL samples-critical for newborn screening and animal health-and plug directly into Bluetooth-enabled patient apps, expanding the osmometers industry footprint in decentralized setting. Freezing-point leaders respond by embedding barcode scanners, reagent-lot traceability and AI-based quality control alerts that slash out-of-spec reruns. Vapor-pressure suppliers focus on stainless-steel wetted paths and 21 CFR Part 11 audit trails that attract gene-therapy CDMOs.

Single-sample analyzers held 60.36% of the osmometers market in 2024 as clinics and emergency rooms favored lower purchase prices and easy workflows. Yet multi-sample versions, climbing at 8.12% CAGR, now ship with robotic load drawers and LIS hubs that process up to 90 tubes per hour-features North American mega-labs deem essential for value-based reimbursement targets. The osmometers market size for high-throughput units should therefore outpace historical averages over the forecast as hospitals redesign core labs around modular automation.

European sites adopt 24-place racks with smartphone-style touchscreens, allowing one technologist to oversee parallel electrolyte, glucose and osmolality tests. In rural health centers, compact single-sample devices persist, but vendors refresh them with cloud logging, simplified QC and one-button maintenance. This balanced demand keeps both categories relevant yet sharply differentiated on throughput and connectivity.

The Osmometers Market Report is Segmented by Product Type (Freezing Point Osmometers, Vapor Pressure Osmometers, and More), Sampling Capacity (Single-Sample and Multi-Sample Osmometers), Application (Clinical, Pharmaceutical & Biotech, and More), End User (Hospitals, Diagnostic and Laboratory Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America kept 37.77% of global osmometers market share in 2024 as reimbursement stability and high test volumes underpinned steady upgrades. The region benefits from the deepest base of CLIA-certified labs and a dense biopharma corridor that values process analytical technology. Asia-Pacific, compounding at 7.98% CAGR, benefits from national health insurance expansions, aggressive biologics capacity build-outs and rising adoption of bedside testing in China, India and South Korea. Europe, while hampered by regulatory bottlenecks, leverages automation uptake and strong vaccine pipelines to maintain competitive parity. Middle East and Africa remain nascent but secure double-digit unit growth where hospital build programs pair with local device assembly incentives.

Government subsidies in Singapore, Korea and China tilt capex toward high-throughput, 21 CFR Part 11-ready osmometers that future-proof regulatory filings. EU MDR's protracted certification cycles delay some product launches, but also create white-space for nimble suppliers with pre-notified-body strategies. Across all regions, demand gravitates toward platforms that compress workflow, integrate data streams and reduce total cost of ownership.