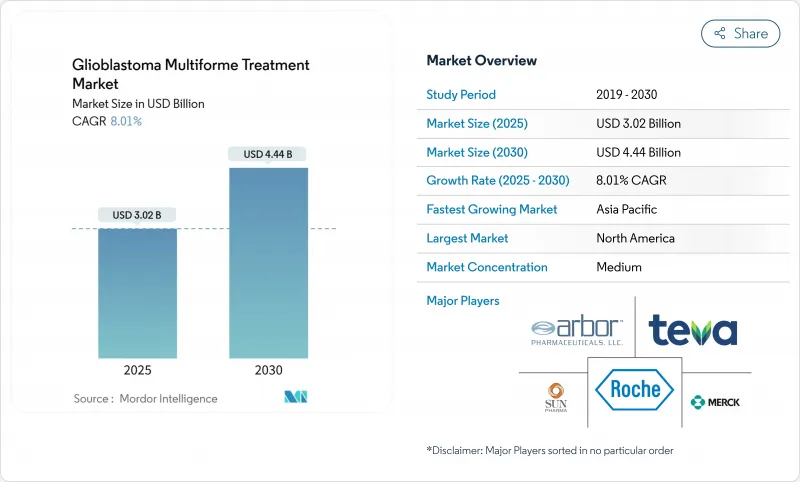

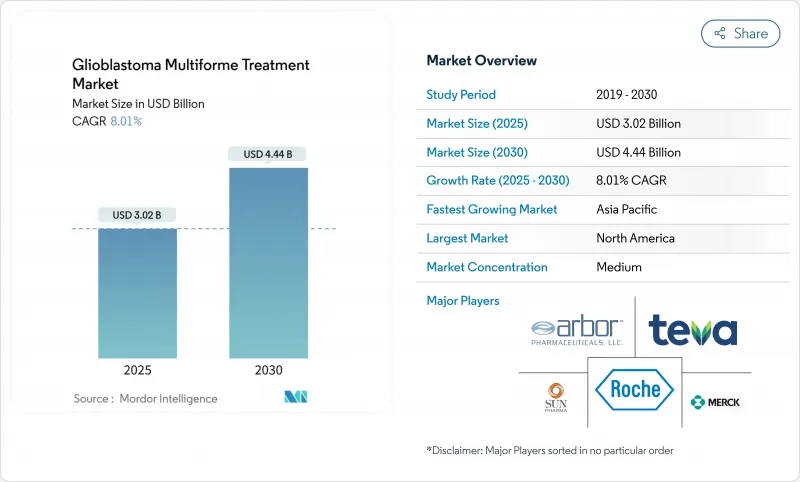

다형성 교모세포종 치료 시장의 2025년 시장 규모는 30억 2,000만 달러로 추정되고, 2030년에는 44억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 8.01%로 성장할 전망입니다.

생존 기간을 연장하는 치료에 대한 수요 증가, 종양 치료 영역(TTFields) 디바이스의 급속한 채용, 승인을 가속화하는 오펀 드러그 우대 조치, 혈액뇌 장벽(BBB) 투과 플랫폼에 대한 꾸준한 벤처 자금 조달이 이 궤도를 지원하고 있습니다. 또한 미국 식품의약국(FDA)이 수십년 만에 획기적인 신약(그레이드 2의 IDH 변이형 신경교종에 대한 보라시데닙)을 발표함으로써 다제 병용 개발 전략에 대한 신뢰가 새롭게 높아진 것도 투자에 박차를 가하고 있습니다. 한편, 의사는 단독 요법으로 점진적인 효과만을 얻을 수 있기 때문에 병용 요법으로 전환하고 있으며 장비와 약물의 통합 접근법에 대한 필요성을 강화하고 있습니다. TTFields와 면역 체크포인트 억제를 결합한 현재 진행 중인 임상시험은 개발자가 독성을 완화시키면서 지속적인 생존 기간을 연장하는 방법을 보여줍니다.

이환 동향으로 다형성 교모세포종 치료 시장은 견조한 성장을 계속하고 있습니다. 교모세포종은 이미 세계의 원발성 악성 뇌종양의 절반 가까이를 차지하고 있으며, 진단에 대한 의식이 높아짐에 따라, 더 많은 환자가 질병 경과 초기에 치료 경로에 들어가게 되었습니다. 주요 학술 센터의 신경 종양학 부서는 이러한 사례 수를 수용하기 위해 규모를 확대하고 있으며 승인된 약물, TTFields 장비 및 관련 진단 약물에 대한 예측 가능한 수요를 창출하고 있습니다. 또한 증례 수 증가는 임상시험 등록을 가속화하고 차세대 요법의 개발주기를 단축합니다. 제조업체 각 회사는 대응 가능한 인구 증가를 활용하여 추가 기술 혁신에 자금을 제공하는 프리미엄 가격 전략을 정당화합니다.

미국과 EU의 규제에 따른 패스트트랙과 희소질환용 의약품의 지정은 비용과 제품화까지의 시간을 모두 삭감하고 교아종을 역사적으로 매력이 없는 틈새에서 상업적 우선순위로 변모시킵니다. FDA에 의한 악성 신경교종에 대한 ERAS-801의 희귀의약품으로서의 승인과 보라시데닙의 신속한 클리어런스 경로는 언메트 요구가 높을 경우 대리 종단을 받아들이겠다는 규제 당국의 의사를 나타냅니다. 이러한 지정에 이어 독점 기간은 기업에 있어서, 환자수가 적은 것에 수반하는 리스크를 상쇄하는 수익 보호가 됩니다. 이러한 환경은 국경을 넘은 라이선스 계약이나 머크에 의한 모디피 바이오사이언시스의 인수와 같은 테모졸로미드 내성 극복을 목표로 한 대기업 제약회사의 인수를 촉진하고 있습니다.

의료기술 평가기관은 보험 적용을 인정하기 전에 실세계에서 비용 효과의 증거를 점점 요구하고 있습니다. TTField의 경우, 지불자는 종종 입원 및 유해 사례 관리 비용의 감소를 보여주는 시판 후 조사를 요구합니다. 규제 당국의 승인부터 최종 상환 결정까지 12-24개월의 지연이 발생하면 수익까지의 과정이 길어져 디바이스 기업의 유동성을 시험하게 됩니다. 유럽에서는 재무 리스크를 제조업체에 전가하는 성과 기반 계약이 표준이 되고 있으며, 소규모 진출기업에 있어서는 장애물이 높아지고 있습니다.

화학요법은 제네릭의 테모졸로미드가 계속 최전선의 프로토콜을 지원하고 있기 때문에 2024년 총 매출의 47.21%를 차지했습니다. TTFields 치료는 2030년까지 CAGR 8.89%로 성장할 전망이며, 전신성 부작용을 피하는 장치 중심 접근법에 대한 임상가의 신뢰가 가속되고 있음을 보여줍니다. 양성자선을 포함한 방사선 요법은 국소 제어를 위해 여전히 중요하며, '기타' 바구니에는 백신, 방사성 의약품 및 면역 요법의 조합이 포함되며, 이들은 중간 단계 임상시험을 통과하고 있습니다. 시장 진출 기업은 치료의 번들화를 추진하고 있습니다. 노보큐어 및 MSD는 TTFields와 펨브롤리주맙의 병용 요법을 등록 시험으로 평가하고 있는데, 이는 지속적인 생존에 다제 병용요법이 필요하다는 컨센서스를 반영하고 있습니다.

치료 믹스 이동은 공급망 및 상환 모델에 영향을 미칩니다. TTFields 시스템은 일회용 약물 주입과는 다른 구독 스타일의 소모품 수요를 생성합니다. 새로운 병용 요법이 승인되면 임상 경로는 순차적 또는 동시식이 요법을 특징으로 하며 복잡성이 증가하고 대응 가능한 지출이 확대됩니다. 장비 및 약물의 비용 효율적인 통합을 입증한 개발 기업은 압도적인 점유율을 얻는 것으로 보입니다.

신규 진단 사례는 2024년 매출의 68.44%를 차지했으며 인구 증가와 Stupp 프로토콜 채용에 견인됩니다. 그러나 재발 사례의 2030년까지 CAGR은 8.78%로 성장할 전망이며, 기술 혁신의 프론티어가 어디에 있는지를 나타내고 있습니다. 알파 DaRT의 FDA 지원에 의한 라듐 224 요법의 파일럿 시험과 RRx-001 병용 프로토콜은 구제 의료에서의 적극적인 실험의 초기 예입니다.

재발에 초점을 맞추면 더 작고 적응력 있는 시험 설계가 장려되고 일정이 단축되고 필요한 자본이 줄어듭니다. 이러한 특징은 머크사가 테모졸로미드 내성에 임하기 위해서 모디피 바이오사이언시스사를 인수한 것처럼, 바이오벤처의 자금이나 대기업 제약회사의 옵션 거래를 끌어들입니다. 여기서 성공은 병용 요법의 확대를 통해 최전선의 표준에 파급되어 재발과 신규 진단의 치료 알고리즘 사이의 루프를 닫을 것으로 보입니다.

북미가 매출의 40.14%를 차지하고 있는 이유는 메디케어와 민간보험사가 TTFields와 최신 화학요법제에 보험금을 지불하고 600개 이상의 임상센터가 임상시험 인프라를 제공하고 있기 때문입니다. 규제가 명확하고 희귀의약품(오펀 드러그)으로서의 이점이 있기 때문에 파이프라인의 조기 출시가 가능하고, 벤처 캐피탈의 에코시스템이 밀집되어 있기 때문에 얼리 스테이지의 혁신에 자금이 공급됩니다. 종합적인 신경 종양학 프로그램은 수술, 방사선, 장비 및 약물 시험을 결합하여 미국을 새로운 치료법 개발의 기준 시장으로 자리매김하고 있습니다.

유럽은 두 번째로 큰 지역 기회이지만 엄격한 의료 기술 평가를 의무화하는 비용 효율적인 임계 값을 채택합니다. 독일은 치료가 어려운 암에 대한 수지상 세포 요법의 상환의 선구자이며, 프리미엄 개입에 대한 선택적 개방성을 나타내고 있습니다. 유럽의약청(EEA)의 일원화된 절차는 판매 승인을 가속화하지만, 상환은 국가마다 다르므로 널리 보급되기까지의 시간이 길어집니다. 개발자는 생존기간과 QOL 지표에 따라 지불을 하는 결과 기반 계약을 잘 활용해야 합니다.

아시아태평양은 CAGR 9.04%로 가장 빠르게 성장하고 있는 지역입니다. 각국 정부는 정밀의료 인프라에 투자하고 있으며 주요 암 전문 병원은 고급 신경 외과 수술용 수술실을 갖추고 있습니다. 일본의 국민 모두 보험제도에서는 국내의 임상 데이터에서 유용성이 입증된 경우, 고비용의 치료법에 자금을 제공하는 경우가 늘어나고 있으며, 중국의 집중 수량 기준의 조달 이니셔티브에는 신경 종양학 기기가 포함되기 시작하고 있습니다. 현지 제조업체는 TTFields 및 나노입자 분야에 진출하여 경쟁력 있는 가격 설정과 광범위한 액세스를 촉진하고 있습니다. 다국적 기업은 지역 개발 업무 수탁기관과 제휴하여 적응 시험을 실시하여 주요 아시아 시장에서의 승인을 가속화하고 있습니다.

The glioblastoma multiforme treatment market is valued at USD 3.02 billion in 2025 and is forecast to reach USD 4.44 billion by 2030, reflecting an 8.01% CAGR over the period.

Growing demand for therapies that prolong survival, rapid adoption of Tumor-Treating Fields (TTFields) devices, orphan-drug incentives that accelerate approvals, and steady venture funding for blood-brain-barrier (BBB)-penetrating platforms underpin this trajectory. Investment is also spurred by the first major U.S. Food and Drug Administration (FDA) breakthrough in decades -vorasidenib for Grade 2 IDH-mutant glioma-which has renewed confidence in multimodal development strategies. Meanwhile, physicians are shifting toward combination regimens because monotherapies deliver only incremental benefit, reinforcing the need for integrated device-drug approaches. Ongoing clinical trials that combine TTFields with immune checkpoint inhibition illustrate how developers intend to capture durable survival gains while mitigating toxicity.

Incidence trends keep the glioblastoma multiforme treatment market on a firm growth footing. Glioblastoma already represents nearly half of all malignant primary brain tumors worldwide, and rising diagnostic awareness is bringing more patients into care pathways earlier in their disease course. Neuro-oncology units at major academic centers are scaling to meet these volumes, creating predictable demand for approved drugs, TTFields devices, and related diagnostics. Higher case numbers also accelerate clinical-trial enrollment, shortening development cycles for next-generation therapies. Manufacturers leverage the larger addressable population to justify premium pricing strategies that fund further innovation.

Fast-track and orphan designations under U.S. and EU regulations reduce both cost and time-to-market, transforming glioblastoma from a historically unattractive niche into a commercial priority. The FDA's orphan approval of ERAS-801 for malignant glioma and the swift clearance pathway for vorasidenib demonstrate regulators' willingness to accept surrogate endpoints when unmet need is high. Exclusivity periods that follow such designations provide companies with revenue protection that offsets the risks associated with small patient populations. The environment is catalyzing cross-border licensing deals and big-pharma acquisitions, such as Merck's purchase of Modifi Biosciences, targeted at overcoming temozolomide resistance .

Health-technology assessment bodies increasingly demand real-world cost-benefit evidence before granting coverage. For TTFields, payers often require post-market studies showing reductions in hospitalizations and adverse-event management costs. Delays of 12-24 months between regulatory clearance and final reimbursement decisions prolong the path to revenue, testing the liquidity of device firms. Outcome-based contracts that shift financial risk to manufacturers are becoming standard in Europe, raising hurdles for smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Chemotherapy generated 47.21% of total revenue in 2024 as generic temozolomide continues to anchor frontline protocols. TTFields therapy's 8.89% CAGR to 2030 signals accelerating clinician confidence in a device-centric approach that avoids systemic side effects. Radiation, including proton techniques, remains critical for local control, while a growing "others" basket contains vaccine, radiopharmaceutical, and immunotherapy combinations that are moving through mid-phase trials. Market participants increasingly bundle modalities: Novocure and MSD are evaluating TTFields plus pembrolizumab in registrational studies, reflecting consensus that multimodal attack is necessary for durable survival.

The treatment-mix shift influences supply chains and reimbursement models. TTFields systems create subscription-style consumables demand, distinct from one-time drug infusions. As new combinations reach approval, clinical pathways will feature sequential or concurrent regimens, adding complexity but enlarging the addressable spend. Developers that prove cost-effective integration of devices with drugs will capture outsized share.

Newly diagnosed cases dominated with 68.44% revenue in 2024, driven by the larger incident population and accepted Stupp protocol adoption. Yet the recurrent segment's 8.78% CAGR to 2030 illustrates where the innovation frontier lies. Alpha DaRT's FDA-supported pilot trial of radium-224 therapy and RRx-001 combination protocols are early examples of aggressive experimentation in salvage settings.

The recurrent focus encourages smaller, adaptive study designs, shortening timelines and reducing capital requirements. These features attract biotech venture funding and big-pharma option deals, as demonstrated by Merck's acquisition of Modifi Biosciences to tackle temozolomide resistance. Success here will likely ripple into frontline standards through combination expansion, closing the loop between recurrent and newly diagnosed care algorithms.

The Glioblastoma Multiforme Treatment Market Report is Segmented by Treatment Modality (Chemotherapy, Radiation Therapy, and More), Patient Type (Newly Diagnosed GBM, Recurrent GBM), End User (Hospitals and Clinics, and More), Age Group (Adults, Pediatric, Geriatric), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America holds 40.14% of revenue because Medicare and private insurers reimburse TTFields and the latest chemotherapeutic agents, while more than 600 clinical centers provide trial infrastructure. Regulatory clarity and orphan-drug benefits encourage rapid launch of pipeline assets, and the region's dense venture-capital ecosystem funds early-stage innovation. Comprehensive neuro-oncology programs combine surgery, radiation, devices, and drug trials, positioning the United States as the reference market for new therapy rollouts.

Europe represents the second-largest regional opportunity but employs cost-effectiveness thresholds that mandate rigorous health-technology assessments. Germany has pioneered dendritic-cell therapy reimbursement for difficult-to-treat cancers, signaling selective openness to premium interventions. The European Medicines Agency's centralized procedure expedites marketing authorization, yet reimbursement remains country specific, lengthening time to broad uptake. Developers must navigate outcome-based agreements that align payment with survival or quality-of-life metrics.

Asia-Pacific is the fastest-growing territory at 9.04% CAGR. Governments are investing in precision-medicine infrastructures, and major oncology hospitals are equipping operating suites for advanced neurosurgery. Japan's universal coverage system increasingly funds high-cost therapies when domestic clinical data demonstrate benefit, and China's centralized volume-based procurement initiatives are beginning to include neuro-oncology devices. Local manufacturers are entering the TTFields and nanoparticle spaces, thereby driving competitive pricing and broader access. Multinational firms partner with regional contract research organizations to run adaptive trials that expedite approval in key Asian markets.