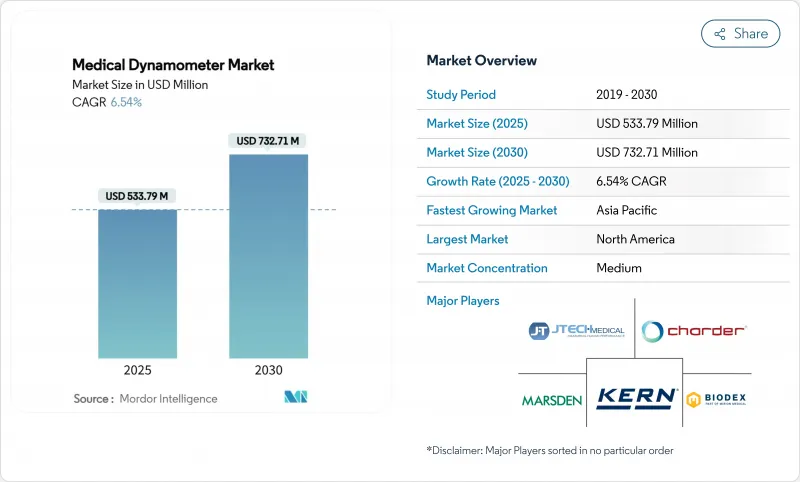

의료용 동력계 시장 규모는 2025년에 5억 3,379만 달러, 2030년에는 7억 3,271만 달러에 이를 것으로 예상되며, CAGR은 6.54%를 나타낼 전망입니다.

수요의 배경으로는 세계 인구의 고령화, 사르코페니아가 명확한 질환으로 임상적으로 인식되게 된 것, 가치관에 기초한 케어의 지침으로서 정확한 근력 데이터가 사용되게 된 것 등이 있습니다. 다이나모 미터를 전자 의료 기록 및 가상 재활 플랫폼과 연결하면 장비 연결이 옵션에서 필수로 바뀝니다. 병원은 연결된 시스템을 절약된 진단 도구로 간주하고, 지불자는 이러한 장비에 의해 생성된 객관적인 결과 지표에 보상합니다. 센서, 애널리틱스 및 클라우드 기반 대시보드를 통합할 수 있는 제조업체들은 계속해서 인기를 끌고 있습니다.

임상 지침에서 Sarcopenia는 기본 치료에서 조기 스크리닝이 필요한 단독 질환으로 분류됩니다. 노인의 세계적인 유병률은 21%에 달하며 중국의 코호트 데이터에서 낮은 악력은 고관절 골절 위험과 관련이 있습니다. 병원에서는 핸드헬드 다이나모미터를 노인 검진에 통합하여 운동 능력의 저하를 지적하고 근력 트레이닝 계획을 세우고 있습니다. 지역 클리닉에서는 빈번한 장소 간의 이동을 견디는 휴대용 유닛이 선호됩니다. 디지털 대시보드는 악력의 기준선을 집계하여 임상의가 급속한 악화를 발견하고 넘어짐과 관련된 입원에서 비용이 증가하기 전에 개입할 수 있도록 합니다.

아시아태평양의 40세 이상 여성의 골다공증률은 30%에 달하고, 골절 발생률은 10만명 당 1,000건에 달한다고 보고되었습니다. 정형외과에서는 약한 악력이 취약성 골절을 예측하는 것을 높이 평가하고 있으며, DEXA 스캐너를 이용할 수 없는 경우에 동력계를 저비용의 트리어지 툴로서 사용하고 있습니다. 일본 소매 약국에서는 익명화된 데이터를 병원 네트워크에 업로드하는 스마트폰 연동형 기기를 이용한 지역 스크리닝의 날을 시작했습니다. 공중보건기구는 현재 추락 예방 지침에 골밀도 스캔과 함께 동력계에 의한 악력 검사를 게재하고 조달 예산의 폭을 넓히고 있습니다.

연간 교정 비용은 클리닉 장비 예산의 3-5%에 달하며, FDA 규정은 공인 서비스 제공업체가 의무화하고 있습니다. 소규모 클리닉에서는 종종 재교정이 늦어지고 부정확한 측정으로 인해 치료 성적이 저하될 위험이 있습니다. 현재 현금 흐름을 원활하게 하기 위해 다년간 교정 계약을 임대 모델에 통합하는 공급업체도 있습니다. 클라우드 기반 자가 진단 기능을 통해 사용자는 드리프트가 임계값을 초과할 때만 서비스를 받는 일정을 설정할 수 있어 다운타임을 줄일 수 있습니다. 이러한 지원에도 불구하고 라틴아메리카 병원에서는 스티커 충격이 여전히 구매를 방해하고 있습니다.

핸드 다이나모미터는 2024년 매출의 37.51%를 차지하며, 1차 케어에서 신속한 악력 평가의 기본 툴로서의 역할을 강조했습니다. 그러나 스마트한 다기능 모델이 CAGR 13.25%를 나타낼 전망입니다. 이는 단일 테스트에서 피크, 평균 및 지구력을 측정하는 관성 센서가 내장되어 있기 때문입니다. 푸시풀 디바이스는 제조 공장에서 인체공학적 감사를 지배하고 있으며, 안전 관리 담당자는 힘 데이터를 사용하여 워크플로우를 재설계하고 있습니다. 흉부 다이나모미터는 틈새이지만 COVID 후 폐 재활 프로그램에서 흡기 근력을 모니터링하는 데 사용되었습니다. 최근의 설계는 충전식 리튬 팩을 내장하고, 배터리 교체 비용을 60% 절감하고, 녹색 조달의 의무화를 지원하고 있습니다.

의료용 동력계 시장에서는 하드웨어와 견고한 분석 기능을 결합한 공급업체에 대한 평가가 높아지고 있습니다. 클라우드 대시보드는 치료사에 색으로 구분된 경과 그래프를 제공하고 HL7 호환 파일을 병원 기록 시스템으로 내보내 수동 데이터 입력을 제거합니다. 구독 기반 소프트웨어 계층을 도입한 기업에서는 고객 유지율이 25% 향상된 것으로 보고되었습니다. 중국제 부품에 대한 관세가 2025년에 125%에 달했기 때문에 북미 기업은 공급망 위험을 줄이기 위해 센서 조립을 재위탁했습니다. 이 변화로 인해 평균 판매 가격이 상승했지만 퇴역 군인의 구매자에게 영향을 미치는 '국내 원산' 품질 클레임의 마케팅 여지가 탄생했습니다.

북미는 2024년 매출의 35.32%를 차지했으며, 높은 수술 건수, 외래 재활의 민간 지불 보험 적용, 클라우드 링크 디바이스의 조기 도입에 지지되었습니다. Kaiser Permanente 및 Veterans Health Administration을 포함한 대규모 통합 의료 네트워크는 현재 입찰에서 데이터 상호 운용 가능한 동역학을 지정합니다. 원격 치료 모니터링을 환불하는 연방 정부 지침은 주문량을 더욱 확대합니다. 국내 제조업체는 현지 생산의 기폭제로서 관세를 추진해, 공급 체인의 탄력성을 요구하는 공공 부문의 바이어에게 어필하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.71%로 가장 급성장하고 있는 지역으로, 고령화 사회와 일본, 한국, 중국에서의 적극적인 운동기 검진 캠페인에 지지되고 있습니다. 중국 기업은 현재 세계 최고의 브랜드에 부품 공급의 80% 이상을 차지하고 있으며, 리드 타임을 단축하고 맞춤형 제조를 지원합니다. 인도네시아와 인도에서는 정부의 경기 자극책이 2급 도시에서 디지털 재활 장비에 대한 보조금을 계상하여 대도시 병원 이외의 접근을 넓히고 있습니다. 지역 공급업체는 언어 현지화된 앱을 활용하여 지역 의료 센터에 침투합니다.

유럽은 성숙하지만 혁신 주도의 상황입니다. 의료기기 규제 시행은 문서화 비용을 끌어올리지만 인증을 받은 제조업체는 경쟁 혼란을 줄일 수 있습니다. 2024년 아마존과 OSHA 협정과 같은 인체공학적 스크리닝의 의무화는 산업안전보건에 새로운 수요를 창출했습니다. 공공 부문 입찰은 탄소 발자국 공개를 선호하며 공급업체는 포장재를 생분해성 소재로 전환하도록 촉구합니다. 유럽우주기관이 근위축증 연구를 위해 우주비행사의 악력을 평가하는 파일럿 프로그램을 실시함으로써 틈새 시장에서의 선전효과가 태어나 유사한 기술에 대한 병원의 관심이 높아집니다.

The medical dynamometer market size is USD 533.79 million in 2025 and is forecast to reach USD 732.71 million in 2030, advancing at a 6.54% CAGR.

Demand stems from an aging global population, the clinical recognition of sarcopenia as a distinct disorder, and the rising use of precise muscle-strength data to guide value-based care. Device connectivity has shifted from optional to essential, linking dynamometers to electronic health records and virtual-rehab platforms. Hospitals view connected systems as labor-saving diagnostic tools, while payers reward objective outcome measures generated by these devices. Manufacturers able to merge sensors, analytics, and cloud-based dashboards continue to gain traction.

Clinical guidelines now classify sarcopenia as a stand-alone condition that warrants early screening in primary care. Global prevalence reaches 21% among older adults, and Chinese cohort data link low grip strength to hip-fracture risk. Hospitals embed handheld dynamometers into geriatric checkups to flag mobility decline and tailor strength-training plans. Community clinics prefer portable units that withstand frequent transit between locations. Digital dashboards aggregate grip-strength baselines, enabling clinicians to spot rapid deterioration and intervene before fall-related admissions increase costs.

Asia-Pacific reports osteoporosis rates as high as 30% for women aged 40+ and fracture incidence up to 1,000 per 100,000 person-years. Orthopedic departments appreciate that weak grip strength predicts fragility fractures and use dynamometers as low-cost triage tools when DEXA scanners are unavailable. Retail pharmacies in Japan have begun community screening days with smartphone-linked devices that upload anonymized data to hospital networks. Public-health agencies now list dynamometer grip testing alongside bone-density scans in fall-prevention guidelines, broadening procurement budgets.

Annual calibration expenses run 3-5% of a clinic's equipment budget, and FDA rules mandate certified service providers. Small practices often delay recalibration, risking inaccurate readings that can compromise treatment outcomes. Some vendors now bundle multiyear calibration contracts into leasing models to smooth cash flow. Cloud-based self-diagnostics help users schedule service only when drift exceeds thresholds, cutting downtime. Despite such aids, sticker shock still stalls purchases in community hospitals across Latin America.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hand dynamometers generated 37.51% of 2024 revenue, underlining their role as the baseline tool for quick grip assessments in primary care. However, smart multifunction models are scaling at a 13.25% CAGR, aided by embedded inertial sensors that capture peak, average, and endurance force in one trial. Push-pull devices dominate ergonomic audits in manufacturing plants, where safety officers use force data to redesign workflows. Chest dynamometers, though niche, gained adoption in post-COVID pulmonary rehab programs that monitor inspiratory-muscle strength. Recent designs integrate rechargeable lithium packs, cutting battery replacement costs by 60% and supporting green-procurement mandates.

The medical dynamometer market increasingly rewards suppliers that pair hardware with robust analytics. Cloud dashboards deliver color-coded progress charts to therapists and export HL7-compliant files to hospital record systems, eliminating manual data entry. Companies introducing subscription-based software layers report 25% higher customer retention. As tariffs on Chinese components reached 125% in 2025, North American firms reshored sensor assembly to mitigate supply-chain risk. The shift lifted average selling prices but created marketing room for "domestic-origin" quality claims that resonate with veterans-affairs buyers.

The Medical Dynamometer Market Report is Segmented by Product (Chest Dynamometer, Hand Dynamometer, Push-Pull Dynamometer, and More), Application (Orthopedics & Sports Medicine, Neurology & Stroke Rehab, Cardiology & Pulmonary Rehab, and More), End-User (Hospitals & Clinics, Rehabilitation Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 35.32% of 2024 revenue, buoyed by high procedure volumes, universal private-payer coverage for outpatient rehab, and early adoption of cloud-linked devices. Large integrated health networks, including Kaiser Permanente and the Veterans Health Administration, now specify data-interoperable dynamometers in tenders. Federal guidelines that reimburse remote therapeutic monitoring further expand order volumes. Domestic manufacturers promote tariffs as catalysts for local production, appealing to public-sector buyers seeking supply-chain resilience.

Asia-Pacific is the fastest-growing region at a 10.71% CAGR to 2030, underpinned by aging demographics and proactive musculoskeletal screening campaigns in Japan, South Korea, and China. Chinese companies now account for more than 80% of component supply to top global brands, which shortens lead times and supports customized builds. Government stimulus funds in Indonesia and India earmark grants for digital rehab equipment in secondary-tier cities, widening access beyond metropolitan hospitals. Regional suppliers leverage language-localized apps to penetrate community health centers.

Europe represents a mature but innovation-driven landscape. Enforcement of the Medical Device Regulation raises documentation costs, yet manufacturers that achieve certification enjoy reduced competitive clutter. Ergonomic-screening mandates such as the 2024 Amazon-OSHA agreement create fresh demand in industrial health and safety. Public-sector tenders prioritize carbon-footprint disclosures, prompting suppliers to shift packaging to biodegradable materials. The European Space Agency's pilot program assessing astronaut grip strength for muscle-atrophy research offers niche-market publicity that drives hospital interest in similar tech.