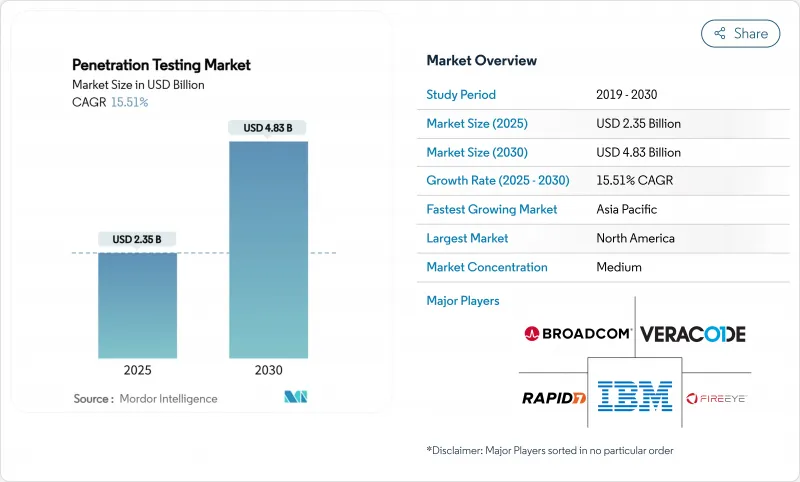

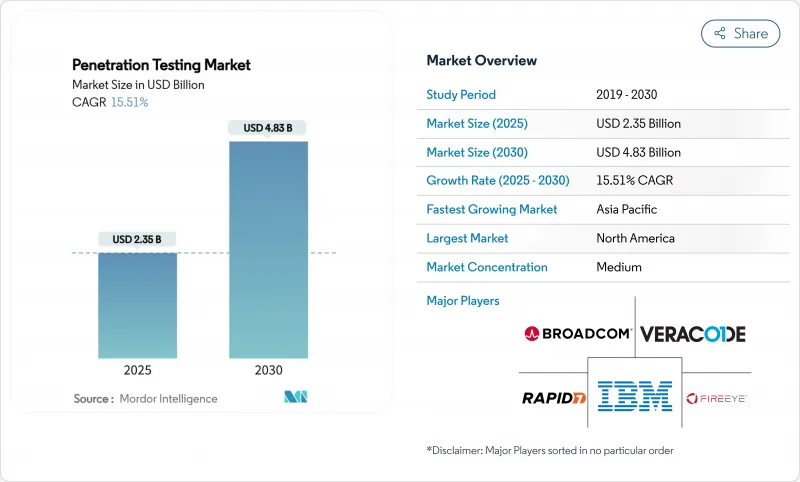

세계의 침투 테스트 시장은 2025년 23억 5,000만 달러로, 2030년까지 48억 3,000만 달러에 달할 것으로 예상되며, 2025-2030년의 CAGR은 15.51%를 보일 것으로 예측됩니다.

성장을 뒷받침하는 것은 사이버 공격 수법의 예리함, 프라이버시에 관한 법규제 강화, 독립적인 보안 검증을 이사회 수준의 우선순위로 하는 사이버보험의 전제조건 강화입니다. HIPAA, PCI DSS 4.0, Digital Operational Resilience Act(Digital Operational Resilience Act)에 근거한 새로운 의무화를 통해 기업은 지속적인 관리의 효과를 규제 당국에 증명해야 하므로 대응 가능한 지출이 확대되고 있습니다. 투자는 사이클 타임을 단축하고 자원에 제약이 있는 팀에 대한 액세스를 확대하는 AI 지원 API 기반 테스트 자동화로 전환하고 있습니다. 클라우드 채택, DevSecOps 연습, 은행, 헬스케어, 제조업의 적극적인 디지털화는 컨설팅, 툴 및 관리 서비스를 번들로 제공하는 공급자에게 새로운 수익원을 창출합니다. 경쟁은 세계 딜리버리의 확장과 Time-to-Value의 단축을 목적으로 하는 플랫폼의 인수, 인재의 롤업, 벤처 기업의 자금 조달에 의해 대응하고 있습니다.

FedRAMP의 2024년 지침과 향후 예정된 HIPAA 업데이트 등 개정된 프레임워크는 매년 또는 지속적으로 침투 테스트를 실시하도록 규정되어 있으며, 대상 사업자와 클라우드 벤더는 공격적인 평가를 보안 프로그램에 통합할 의무가 있습니다. PCI DSS 4.0만으로도 카드 회원 데이터 환경에 대한 보다 깊은 시나리오 기반 테스트를 명시적으로 언급한 63개의 새로운 제어문이 도입되었습니다. EU의 금융기관도 DORA 하에서 유사한 조사에 직면하고 있으며, 전문 서비스 제공업체에게 수년간의 추풍이 보장되고 있습니다.

최신 테스트 플랫폼에 내장된 머신러닝 엔진은 악용 가능한 경로를 거의 실시간 정확도로 감지하므로 수작업을 줄이고 자금 조달로 고통받는 중소기업에 대한 시장 진입의 폭이 넓어집니다. 조기 도입 기업은 사이클 타임이 최대 70% 단축되어 구독의 엔트리 포인트가 월 100달러 미만이 됨으로써, 단발 계약이 벤더의 정기적인 수익원으로 바뀌었다고 보고하고 있습니다.

예산 제한과 인력 부족으로 인한 정보 유출 위험이 커지고 있음에도 불구하고 중소기업에서 침투 테스트의 도입은 아직 진행되지 않았습니다. 교육 캠페인, 번들 보험 할인, 저렴한 가격의 자동화 제품군으로 인해 차이가 점차 줄어들고 있지만 성숙도 지표는 여전히 대기업에 뒤처져 있습니다.

기업이 전자상거래 포털과 SaaS 워크로드를 강화했기 때문에 웹 애플리케이션 프로젝트는 2024년 침투 테스트 시장 점유율의 36%를 차지했습니다. 고객을 위한 서비스 스택은 항상 브라우저 기반 인터페이스를 포함하기 때문에 취약점의 정기적인 검증이 필요하며 수요가 안정적입니다. 반면 모바일 애플리케이션 테스트는 은행 및 소매업과의 상호작용이 Android 및 iOS 채널로 전환됨을 반영하여 CAGR 19.23%로 확대되고 있습니다.

앱 스토어의 게이트키퍼와 금융 감독 당국으로부터의 감시가 강화되어 개발자는 모바일에 특화된 위협 모델링, 세션 관리 체크, 런타임 보호의 통합을 강요하고 있습니다. 클라우드와 API를 중심으로 한 아키텍처는 공격 대상 영역을 더욱 확대하고 보안 팀을 웹, 모바일, 마이크로서비스를 단일 참여 스케줄로 스캔하는 통합 플랫폼으로 향하게 합니다.

On-Premise 프로그램은 2024년 매출의 61%를 유지하고 있습니다. 이것은 데이터 상주의 의무화와 사내 테스트 오케스트레이션의 편안함의 증거입니다. 하지만 클라우드 기반 구독은 에이전트를 즉시 스핀업하고 조사 결과를 DevSecOps 대시보드로 스트리밍하는 능력으로 인해 20.27% 성장했습니다.

공급업체는 엄격한 구매자를 안심시키기 위해 제로 트러스트 커넥터, 익명화된 데이터 챔버 및 지역별로 분리된 워크로드를 추가합니다. 로컬 테스트 하네스와 클라우드 분석을 결합한 하이브리드 딜리버리는 주권과 효율성의 균형을 이루는 기업의 과도적인 상태로 부상하고 있습니다.

북미는 2024년 매출의 39%를 차지했으며 클라우드 벤더를 위한 FedRAMP 테스트 지침과 IRS의 프로덕션 환경 규칙 등 연방 정부의 지시에 힘입어 있습니다. 헬스케어의 개본 개혁안이 정리되면, 46억 달러의 새로운 보안 비용이 투입될 가능성이 있습니다. 첨단 벤더 생태계, 성숙한 사이버 보험 시장, 벤처 자금 조달의 집중이 이 지역의 리더십을 강화하고 있습니다.

아시아태평양은 가장 급성장하는 지역으로, 보험 회사가 검증되지 않은 환경에 보험료를 올리고 정부가 중요 인프라 감사 일정을 공식화함에 따라 CAGR은 17.04%를 기록했습니다. 일본의 사이버 콜로세움 교육 파이프라인, 중국의 자립형 보안 스택의 추진, 인도의 핀테크의 급증이 함께 테스트 빈도의 요건이 높아지고 있습니다. ASEAN의 Tier2 이코노미는 국내 인력 부족을 보완하기 위해 매니지드 서비스를 위탁하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)과 디지털 운영 탄력성 법(Digital Operational Resilience Act) 하에서 꾸준한 확대가 기록되고 있으며, 은행과 보험 회사는 국경을 넘는 기업체 전체의 관리 체제를 검증할 필요가 있습니다. 기존의 통신 클러스터 및 제조 클러스터는 산업 제어 및 5G 네트워크의 테스트 범위를 위탁함으로써 두께를 늘리고 있습니다. 동유럽 기업들은 인근 분쟁으로 인한 공급망 파급에 직면하여 지속적인 참여 모델로 빠르게 전환하고 있습니다.

The penetration testing market was valued at USD 2.35 billion in 2025 and is forecast to reach USD 4.83 billion in 2030, advancing at a 15.51% CAGR over 2025-2030.

Growth is propelled by sharper cyber-attack tactics, tighter privacy statutes, and rising cyber-insurance prerequisites that make independent security validation a board-level priority. New mandates under HIPAA, PCI DSS 4.0, and the Digital Operational Resilience Act are expanding the addressable spend as organizations must prove continuous control efficacy to regulators. Investment is shifting toward AI-enabled, API-driven test automation that cuts cycle time and broadens access for resource-constrained teams. Cloud adoption, embedded DevSecOps practices, and aggressive digitalization across banking, healthcare, and manufacturing create fresh revenue pools for providers willing to bundle consulting, tooling, and managed services. The competitive field is responding through platform acquisitions, talent roll-ups, and venture funding aimed at scaling global delivery and shortening time-to-value.

Revised frameworks such as FedRAMP's 2024 guidance and forthcoming HIPAA updates now specify annual or even continuous penetration tests, obliging covered entities and cloud vendors to hard-wire offensive assessments into security programs. PCI DSS 4.0 alone introduces 63 new control statements that explicitly reference deeper, scenario-based testing for cardholder data environments. Financial entities in the EU face similar scrutiny under DORA, guaranteeing a multi-year tailwind for specialist service providers.

Machine-learning engines embedded in modern testing platforms detect exploitable paths with near-real-time accuracy, trimming manual effort and widening market reach to cash-strapped SMEs. Early adopters report cycle-time reductions of up to 70% and subscription entry points under USD 100 per month, converting one-off engagements into recurring revenue streams for vendors.

Budget limits and staffing shortages continue to dampen penetration testing uptake among smaller firms despite evidence of rising breach exposure. Education campaigns, bundled insurance discounts, and lower-priced automated suites are gradually narrowing the gap, but the segment still lags larger enterprises on maturity metrics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Web application projects generated 36% penetration testing market share in 2024 as companies fortified e-commerce portals and SaaS workloads. Demand stays stable because every customer-facing service stack now includes browser-based interfaces needing recurring exploit validation. Mobile application testing, however, is scaling at a 19.23% CAGR, reflecting the migration of banking and retail interactions to Android and iOS channels.

Intensifying scrutiny from app-store gatekeepers and financial supervisors forces developers to integrate mobile-specific threat modeling, session management checks, and runtime protections. Cloud and API-centric architectures further enlarge the attack surface, pushing security teams toward unified platforms that scan web, mobile, and micro-services in a single engagement cadence.

On-premise programs retained 61% of 2024 revenues, a testament to data-residency mandates and comfort with in-house test orchestration. Yet cloud-based subscriptions are growing 20.27% annually, buoyed by the ability to spin up agents instantly and stream findings back into DevSecOps dashboards.

Providers are adding zero-trust connectors, anonymized data chambers, and regionally segregated workloads to reassure highly regulated buyers. Hybrid delivery-local test harnesses coupled with cloud analytics-emerges as the transitional state for firms balancing sovereignty with efficiency.

The Penetration Testing Market Report is Segmented by Testing Type (Network Penetration Testing, and More), Deployment Mode (On-Premise, and Cloud), Organization Size (Large Enterprises, and SMEs), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (Government and Defense, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 39% of 2024 revenues, supported by federal directives such as FedRAMP test guidance for cloud vendors and IRS production-environment rules. Healthcare overhaul proposals alone could inject USD 4.6 billion in fresh security outlays once finalized. An advanced vendor ecosystem, mature cyber-insurance market, and venture funding concentration reinforce regional leadership.

Asia-Pacific is the fastest-growing arena, charting a 17.04% CAGR as insurers premium-price untested environments and governments formalize critical-infrastructure audit schedules. Japan's Cyber Colosseo training pipeline, China's push for self-reliant security stacks, and India's fintech surge combine to elevate test frequency requirements. Tier-2 economies in ASEAN are also commissioning managed services to plug local talent gaps.

Europe records steady expansion under GDPR and the Digital Operational Resilience Act, compelling banks and insurers to validate controls across cross-border entities. Incumbent telecom and manufacturing clusters add depth by commissioning industrial-control and 5G-network test scopes. Eastern European firms, confronted with supply-chain spillovers from nearby conflicts, are moving quickly toward continuous engagement models.