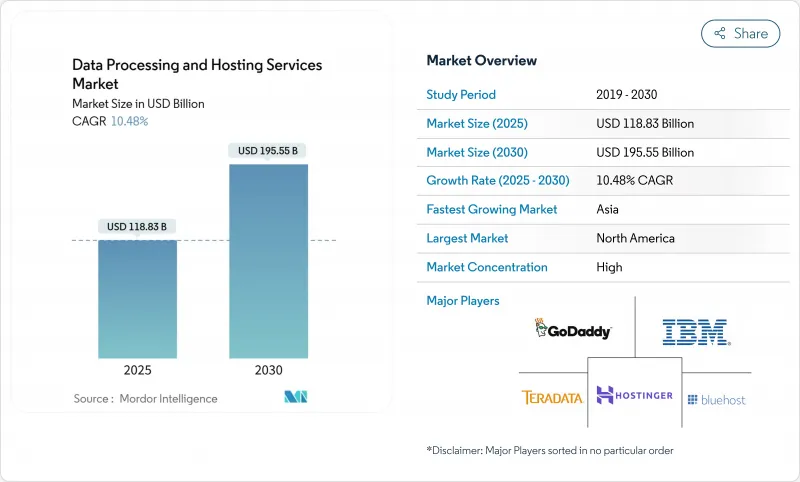

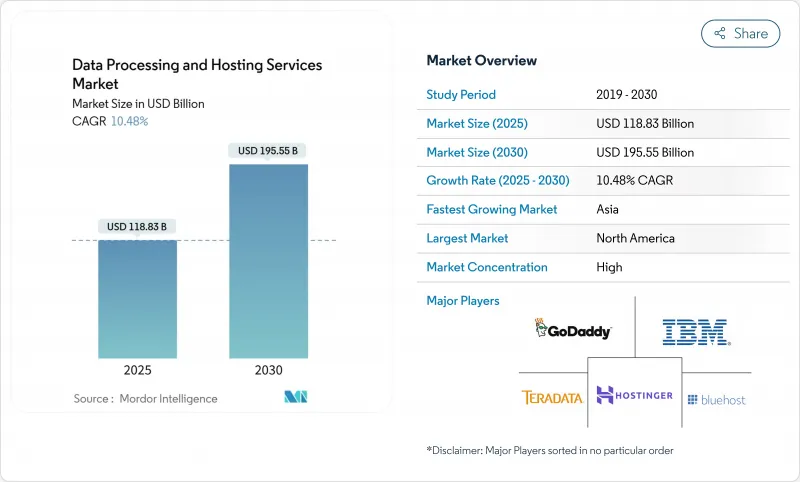

세계의 데이터 처리 및 호스팅 서비스 시장 규모는 2025년 1,188억 3,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 10.48%로 확대되어, 2030년까지 1,955억 5,000만 달러에 도달할 것으로 예측됩니다.

기업의 매니지드 컴퓨팅으로 대규모 이행, AI 대응 인프라로의 가속적인 시프트, 끊임없는 초대규모 설비 투자가 확대를 추진하고 있습니다. 기업은 예산을 온프레임 랙 업데이트에서 GPU 밀도가 높은 클라우드 인스턴스, 턴키 코로케이션 제품군, 데이터에서 통찰력으로의 사이클을 압축하는 지역 에지 노드로 향하고 있습니다. 유럽과 중동에서는 소버린 클라우드의 도입이 의무화되는 정책이 병행하여 진행되고 있으며, 세계 기업은 워크로드를 현지화하고 국내에서 새로운 용량 풀을 구축할 것을 강요하고 있습니다. 한편, 3대 퍼블릭 클라우드를 통한 이그레스 비용 철폐는 스위칭 비용을 낮추고 스택 실리콘, 근접성 또는 섹터별 컴플라이언스로 차별화하는 전문적인 과제들에게 기회를 주고 있습니다.

주요 기술과 규제 촉매가 경쟁 균형을 재구성했습니다. 북미는 파이버 네트워크, 신뢰할 수 있는 전력, 고밀도 하이퍼스케일 클러스터를 지원하며 현재 39%의 판매 점유율을 차지하고 있습니다. 한편 아시아는 5G의 보급, AI의 신흥기업 활동, 정부의 세제우대조치가 데이터센터의 신설을 뒷받침해 CAGR 13.4%로 가장 급속히 확대하고 있습니다. 호스팅 서비스는 여전히 64%의 점유율로 데이터 프로세싱 및 호스팅 서비스 시장을 독점하고 있지만, IaaS, PaaS, SaaS를 중심으로 하는 이 카테고리의 클라우드 네이티브 제공 제품은 고객이 탄력성을 우선하고 있기 때문에 CAGR은 14.1%로 가장 높습니다. 하이브리드 및 멀티클라우드 전략은 CAGR 12.5%로 급증하고 있으며, 기업이 클라우드를 포트폴리오로 파악하고 있음을 보여줍니다.

기업은 미션 크리티컬한 시스템을 하이퍼스케일 지역으로 전환함으로써 자본 예산의 위험을 완화하고 있으며, 미국 데이터센터의 전력 수요는 2030년까지 35GW로 두배로 될 것으로 예측됩니다. 이러한 움직임은 AI 가속기에 대한 액세스와 On-Premise에서 엄청나게 비싸게 유지되는 관리형 보안 서비스를 중심으로 점점 더 능력이 주도되고 있습니다. 특히 전력 할당에 제약이 있는 애쉬번, 피닉스, 더블린, 프랑크푸르트에서는 프레리스 계약에 의해 물리적인 인도보다 몇년전에 용량을 확보할 수 있게 되어 있습니다.

2025년까지 40,000개 이상의 기업이 이산 GPU에서 프로덕션 AI를 실행하여 계산 밀도와 냉각 요건이 높아집니다. Lambda 및 CoreWeave와 같은 전용 GPU 클라우드는 교육, 미세 조정 및 추론 워크로드에 대한 H100 및 MI300 재고를 보장하므로 3자리 성장을 기록하고 있습니다.

남아시아와 아프리카의 전력 공급 부족과 과징금이 데이터센터 신설의 발판이 되고 있습니다. 데이터센터가 2023년 미국에서 소비하는 전력은 176TWh로, 이는 미국의 전력 수요의 4.4%에 해당하며, 계산 능력 증가와 송전망의 용량 사이에 긴장 관계가 있음을 돋보이고 있습니다. 사업자는 현장 태양열 + 배터리 및 마이크로그리드 솔루션으로 중심을 옮겨 자본 요구 사항이 부풀어 오르고 도입 일정을 장기화합니다.

대기업은 2024년 매출의 71%를 차지했고 메인프레임 근대화, 컨테이너 오케스트레이션 채용, 세계 DR 복제본 구축 등에 풍부한 자금을 활용하고 있습니다. 이와는 대조적으로, 중소기업은 마이그레이션 플레이스 크레딧, 관리형 DevOps 서비스가 마이그레이션 도구 간소화, 기술 장벽을 평탄화하고 CAGR 11.7%로 가속화하고 있습니다. 아프리카와 라틴아메리카 시장에서는 중소기업의 90% 이상이 디지털 결제를 도입하고 있으며 보급을 뒷받침하고 있습니다. 정부가 교육과 클라우드 바우처에 보조금을 내는 것으로 더욱 보급이 진행되고 있습니다. 중소기업의 절대적인 시장 규모는 2030년까지 두 배가 될 것으로 예측되고 있지만 대기업 사업도 계속 확대되고 있기 때문에 중소기업 지출 전체에서 차지하는 비율은 30% 미만에 그치고 있습니다.

중소기업 클라우드의 성숙은 새로운 파트너 생태계를 창출합니다. 리셀러는 판매 시점 정보 관리(POS), 분석 및 자국어 지원을 번들로 제공하고 계산 비용을 서비스 요금에 통합합니다. 고급 관측 가능성 스택은 이상을 표면화하고 수리 스크립트를 자동으로 적용하여 한때 중소기업을 막고 있던 기술 격차를 완화합니다. 이러한 효율화는 구독 갱신 및 업셀 증가를 촉진하고 중소기업 부문은 보다 광범위한 데이터 처리 및 호스팅 서비스 시장에서 지속적인 성장을 이루는 원동력으로 자리매김하고 있습니다.

호스팅 서비스는 신뢰할 수 있는 컴퓨팅, 스토리지, 네트워크 프리미티브에 의해 지원되며 2024년에는 이 분야의 수익의 64%를 차지합니다. 클라우드 호스팅(IaaS, PaaS, SaaS)의 하위 부문은 2030년까지 연평균 복합 성장률(CAGR)이 14.1%입니다. 고객은 워크로드에 최적화된 티어, AI용 GPU 클러스터, 웹 티어용 ARM 코어, 금융 원장용 서비스로서 z-parity CICS를 점점 선호하고 있습니다. 동시에 클라우드 네이티브 재설계, 데이터 파이프라인 리팩토링, FinOps 거버넌스를 요구하는 기업이 늘어나면서 프로페셔널 서비스의 수익도 증가하고 있습니다. 에지 및 공동 위치 공급자는 클라우드와 유사한 프로비저닝을 포털에 통합하여 코어 호스팅과 분산 호스팅의 경계를 모호하게 만듭니다. 시간이 지남에 따라 데이터 준비와 컴퓨팅을 연결하는 통합 파이프라인은 독립형 ETL 공급업체를 침식하여 경제성을 데이터 처리 및 호스팅 서비스 시장의 게이트키퍼에 통합할 것으로 보입니다.

재정적인 유연성은 여전히 매력입니다. 초 단위의 청구 및 지속적 사용 크레딧은 총 소유 비용을 낮춥니다. 에너지 비용이 변동되면 워크로드는 실시간 전력 스팟 가격에 따라 지역 간 균형을 조정합니다. 그 결과 이용률이 구조적으로 향상되고 공급자는 마진을 늘리고 테넌트는 비용을 예측할 수 있습니다.

북미는 2024년 매출의 39%를 차지하는 광대한 섬유 백본, 까다로운 세제 우대 조치, 밀집된 하이퍼스케일 클러스터를 배경으로 했습니다. 버지니아 주 라우돈 카운티에서만 3천만 평방 피트를 넘는 레이즈드 플로어가 있으며 변압기의 제약으로 인한 그리드 상호 연결의 일시 정지에 직면하고 있습니다. 공급업체는 캠퍼스 규모의 마이크로그리드, 24시간 365일 재생에너지 PPA, 재생 열 재사용 프로그램으로 대응하며 지속가능성 조사에 대응하고 있습니다. AWS, Microsoft, Google의 3개 회사는 2025년 미국에서 새로 건설하는 홀을 위해 총 2,550억 달러 이상을 기록해 이 지역의 용량 리드를 확실히 하고 있습니다. 캘리포니아 CCPA 및 텍사스 프라이버시 보호 법안과 같은 주 수준의 프라이버시 보호 법은 데이터 사본을 주에 남겨두고 데이터 처리 및 호스팅 서비스 시장 내 배포 실적를 미묘하게 재형성할 수 있습니다.

5G의 보급, 디지털 뱅킹, AI 스타트업의 에코시스템이 융합해, 아시아가 CAGR 13.4%를 기록했습니다. 싱가포르의 데이터센터 신설 허가 모라토리엄에 의해 조호르, 바탐, 방콕, 하이데라바드에 설비 투자가 집중됐습니다. 일본의 사업자는 홋카이도의 이용되지 않은 지열을 이용하고, 중국의 하이퍼스케일러는 국내의 슈퍼 앱 스택을 동남아시아에 복제해, 컴퓨트와 결제나 물류를 융합시킵니다. 스마트폰 포화 및 실시간 번역 서비스는 데이터 흐름을 증가시키고 내구성 있는 수요를 지원합니다.

유럽의 주권 아젠다가 조달 동향을 주도합니다. EU의 디지털, 유럽 및 프로그램은 클라우드 마켓플레이스 및 보안 센터에 9억 유로를 할당하여 국내 능력을 자극하고 있습니다. 독일과 프랑스는 원자력 발전과 수력 발전의 조합으로 AI 훈련 클러스터를 획득합니다. Gaia-X는 원래 예상했던 것보다 늦었지만, 상호 운용성의 기준을 책정했습니다. 북유럽 국가들은 저렴한 수력 발전을 활용하면서도 제한된 광섬유 경로를 고민하고 있습니다. 동유럽 국가들은 경제특구를 통해 투자자를 유치하고 있지만 지정학적 리스크는 여전히 장애물이 되고 있습니다. 특필해야할 것은 브렉시트 후 영국이 데이터센터 기기에 대한 부가가치세를 완화하고 대서양을 넘은 투자를 유치하고 런던의 폴 포지션을 강화했다는 것입니다.

The Data Processing And Hosting Services Market size is estimated at USD 118.83 billion in 2025, and is expected to reach USD 195.55 billion by 2030, at a CAGR of 10.48% during the forecast period (2025-2030).

Expansion is propelled by large-scale enterprise migrations to managed compute, an accelerating shift toward AI-ready infrastructure, and unrelenting hyperscale capital expenditure. Enterprises are diverting budgets from refreshed on-prem racks to GPU-dense cloud instances, turnkey colocation suites, and regional edge nodes that compress data-to-insight cycles. Parallel policy shifts in Europe and the Middle East mandate sovereign-cloud deployments, prompting global corporations to localize workloads and create fresh pools of in-country capacity. Meanwhile, the removal of egress fees by the three largest public clouds has lowered switching costs, opening opportunities for specialist challengers that differentiate on stacked silicon, proximity, or sector-specific compliance.

Key technology and regulatory catalysts have reshaped the competitive balance. North America currently commands a 39% revenue share, underpinned by deep fiber networks, reliable power, and dense hyperscale clusters. Asia, in contrast, is expanding the fastest at a 13.4% CAGR as 5G penetration, AI start-up activity, and government tax incentives converge to boost new datacenter builds. Hosting services continue to dominate the data processing and hosting services market with a 64% share, yet cloud-native offerings within that category, especially IaaS, PaaS, and SaaS, post the strongest 14.1% CAGR as customers prioritize elasticity. Hybrid and multi-cloud strategies are surging at 12.5% CAGR, signaling that enterprises now view cloud as a portfolio rather than a monolith.

Enterprises continue to de-risk capital budgets by shifting mission-critical systems to hyperscale regions, with U.S. datacenter power demand expected to double to 35 GW by 2030. The move is increasingly capability-driven, anchored in access to AI accelerators and managed security services that remain prohibitively expensive on-prem. Pre-lease agreements now secure capacity years ahead of physical handover, particularly in Ashburn, Phoenix, Dublin, and Frankfurt, where power allotments are constrained.

By 2025, over 40,000 companies will run production AI on discrete GPUs, raising computational density and cooling requirements. Dedicated GPU clouds such as Lambda and CoreWeave post triple-digit growth as they guarantee H100 and MI300 inventory for training, fine-tuning, and inference workloads.

Electricity supply shortfalls and surcharges in South Asia and Africa throttle new builds. Data centers consumed 176 TWh of U.S. power in 2023, or 4.4% of national demand, underscoring the tension between compute growth and grid capacity. Operators pivot to onsite solar-plus-battery and micro-grid solutions, inflating capital requirements and elongating deployment schedules.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Large enterprises controlled 71% of 2024 revenue, leveraging deep coffers to modernize mainframes, adopt container orchestration, and spin up global DR replicas. In contrast, SMEs are the fastest movers, accelerating at 11.7% CAGR as simplified migration tooling, marketplace credits, and managed DevOps services flatten technical barriers. In African and Latin American markets, more than 90% of SMEs have adopted digital payments, underscoring widespread digital adoption. Governments subsidize training and cloud vouchers, further broadening reach. The absolute data processing and hosting services market size for SMEs is projected to double by 2030, while their slice of overall spending remains under 30% because large-enterprise estates also keep expanding.

SME cloud maturation creates new partner ecosystems. Resellers bundle point-of-sale, analytics, and local-language support, embedding compute costs into service fees. Advanced observability stacks surface anomalies and auto-apply remediation scripts, mitigating the skill gap that once stymied smaller firms. Those efficiencies, in turn, reinforce subscription renewals and incremental upsell, positioning the SME segment as a durable growth flywheel within the broader data processing and hosting services market.

Hosting services delivered 64% of sector revenue in 2024, anchored by reliable compute, storage, and network primitives. The sub-segment of cloud hosting (IaaS, PaaS, SaaS) commands a 14.1% CAGR to 2030, fueled by elastic scaling, bundled APIs, and declining unit pricing as hyperscalers aggregate demand. Customers increasingly favor workload-optimized tiers, GPU clusters for AI, ARM cores for web tier, and z-parity CICS as a service for financial ledgers. Concurrently, professional services revenue grows as firms seek cloud-native redesign, data pipeline refactor, and FinOps governance. Edge and colocation providers embed cloud-like provisioning into portals, blurring the lines between core and distributed hosting. Over time, integrated pipelines that marry data preparation with compute will erode standalone ETL vendors, folding their economics into the data processing and hosting services market gatekeepers.

Financial flexibility remains a draw. Pay-by-the-second billing and sustained-usage credits lower the total cost of ownership. As energy costs fluctuate, workloads re-balance across regions based on real-time power spot prices, a capability accessible only through cloud automation. The result is a structurally higher utilization rate, translating to margin expansion for providers and cost predictability for tenants.

The Data Processing and Hosting Services Market Report is Segmented by Organisation (Large Enterprise and Small and Medium Enterprises [SME]), Offering (Data Processing Services and Hosting Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid and Multi-Cloud), End-User Industry (IT and Telecommunication, BFSI, Retail and E-Commerce, Manufacturing, Healthcare and Life Sciences, and More), and Geography

North America claimed 39% of 2024 revenue on the back of vast fiber backbones, generous tax incentives, and dense hyperscale clusters. Loudoun County, Virginia, alone hosts over 30 million square feet of raised floor and is now facing grid-interconnection pauses due to transformer constraints. Providers respond with campus-scale micro-grids, 24X7 renewable PPAs, and reclaimed-heat reuse programs to counter sustainability scrutiny. AWS, Microsoft, and Google collectively earmarked more than USD 255 billion for new U.S. halls in 2025, ensuring the region's capacity lead. Privacy legislation at the state level, such as California CCPA and Texas privacy bills, could demand that data copies remain in-state, subtly reshaping deployment footprints inside the data processing and hosting services market.

Asia records the fastest 13.4% CAGR as 5G proliferation, digital banking, and AI start-up ecosystems converge. Singapore's moratorium on new datacenter permits diverts cap-ex toward Johor, Batam, Bangkok, and Hyderabad, all vying to become the region's latency hubs. Japanese operators exploit underused geothermal in Hokkaido while Chinese hyperscalers replicate domestic super-app stacks to Southeast Asia, blending compute with payments and logistics. Smartphone saturation and real-time translation services multiply data flows, anchoring durable demand.

Europe's sovereignty agenda steers procurement trends. The EU's Digital Europe Programme has allocated EUR 900 million to cloud marketplaces and security centers, catalysing domestic capacity. Germany and France vie for AI training clusters by touting nuclear and hydro power mixes. Gaia-X lays interoperability standards, albeit slower than first envisioned. Nordic states leverage cheap hydroelectricity yet grapple with limited fiber routes; Eastern European states woo investors through special economic zones, though geopolitical risk remains a hurdle. Notably, post-Brexit UK relaxes VAT on datacenter gear, attracting trans-Atlantic investment and reinforcing London's pole position.