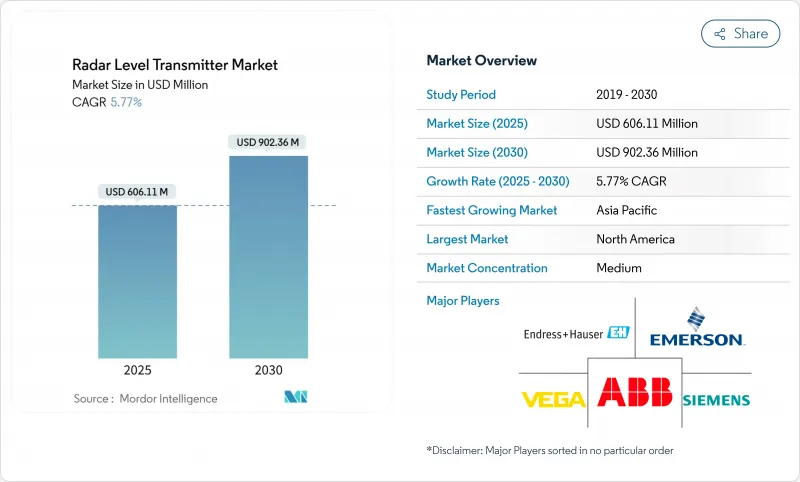

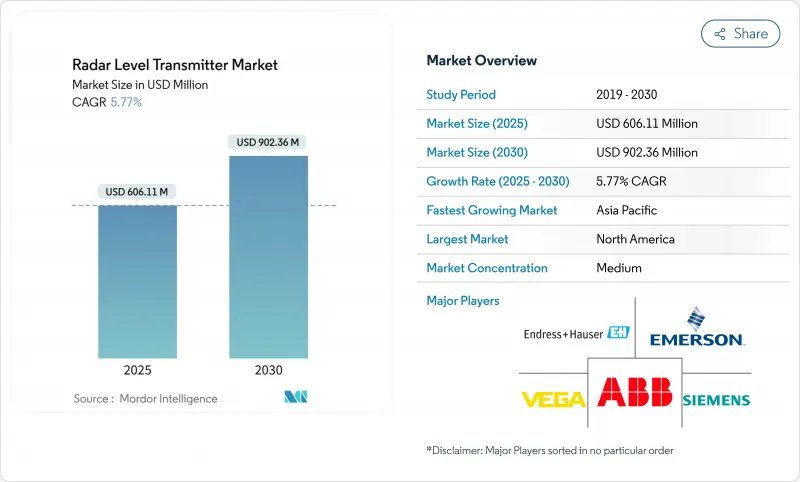

세계의 레이더 레벨 트랜스미터 시장 규모는 2025년 6억 611만 달러로, 2030년까지 9억 236만 달러에 이르고, CAGR 5.77%를 보일 것으로 예측됩니다.

수요는 보다 엄격한 환경 및 안전 규제를 충족하기 위해 정확한 레벨 모니터링이 필요한 산업 자동화 프로그램에 의해 지원됩니다. 유럽의 석유 터미널에서 초음파에서 80GHz 레이더로의 기술 전환, 걸프 국가의 해수 담수화 설비 투자 증가, 노후화된 북미 수도 사업체의 리노베이션 활동은 매우 중요한 성장 벡터입니다. 또한 중국의 석탄에서 화학제품으로의 변환 프로젝트에서는 복잡한 인터페이스 측정에 유도파 레이더를 채용하여 예지보전을 지원하는 무선, 산업용 인터넷 대응 센서로의 꾸준한 전환도 제조업체의 이익이 되고 있습니다. 경쟁 차별화는 안테나의 소형화, 발포체 및 저유전율 매체의 고급 신호 처리, 시운전 시간을 단축하는 서비스 에코시스템에 달려 있습니다.

유럽 규제는 고급 과충전 보호를 의무화하고 있으며, 사업자는 초음파 게이지를 80GHz 레이더로 대체하도록 촉구하고 있습니다. 좁은 빔 각도가 마이크로파 에너지를 집중시켜 증기나 온도 변동이 있어도 신뢰성 높은 측정을 실현하는 한편, 컴팩트한 안테나 설계는 플로팅 루프를 갖춘 탱크로의 개조가 간단해집니다. 유지 보수가 필요없는 작업과 함께이 기술은 컴플라이언스를 보장하고 수명주기 비용을 줄입니다.

사우디아라비아, UAE, 쿠웨이트를 합치면 세계 해수 담수화 능력의 절반을 차지합니다. 새로운 다단 플래시 및 역삼투막 플랜트에서는 부식성, 염분이 높은 염수를 견딜 수 있는 비접촉식 레이더가 필요합니다. 디지털 제어 시스템과의 통합은 에너지 효율과 물 회수를 개선하고 지역 EPC 계약에 레이더를 표준 사양으로 통합합니다.

두꺼운 거품층은 마이크로파를 감쇠시키고 스퓨리어스 에코를 발생시켜 에톡실화 용기와 발효 용기의 레벨 제어를 방해합니다. 고급 신호 처리와 레이더와 커패시턴스의 하이브리드 프로브가 이를 완화하지만 극단적인 발포는 물리적으로 레이더의 투과를 제한합니다.

비접촉식 센서는 2024년 매출의 65%를 차지했으며 부식성 또는 고온 작업에서 유지보수가 필요 없는 작동을 반영합니다. 이 하위 부문은 CAGR 6.8%로 확대되어 S/N비를 향상시키는 주파수 변조 연속파(FMCW) 플랫폼에 의해 강화됩니다. 유도파 레이더는 계면 감지와 무거운 거품이 많은 곳에서 틈새 위치를 유지하고 있습니다. 컴팩트한 80GHz 안테나는 한때 초음파 프로브에 한정된 선박에 뒷받침할 수 있게 되어 레이더 레벨 트랜스미터 시장의 대응 가능한 수요를 확대하고 있습니다.

블루투스 커미셔닝 및 센서 내 진단과 같은 디지털화는 컴플라이언스 감사를 단순화하고 레이더 레벨 송신기 업계의 가치 제안을 강화합니다. 공급업체는 자체 모니터링 기능을 노동력 부족에 대한 헤지로 자리매김하고 레이더를 기업의 자산 성능 플랫폼의 핵심 노드로 강화하고 있습니다.

K-band(24-26GHz)는 여전히 2024년 출하 대수의 38%를 차지했으며, 비용 대비 효과와 폭넓은 승인이 평가되었습니다. 그러나 W밴드(76-81GHz 및 120GHz) 센서는 교반 날개나 좁은 노즐을 무시하는 3°이하의 빔 각에 의해 CAGR 7.4%를 나타내며 40m의 컬럼이나 길쭉한 양조 주전자에서 신뢰성 높은 판독을 실현하고 있습니다. 미국, EU, 중국의 인증기관이 공정용으로 W밴드를 인가함으로써 규모의 경제가 촉진되고 역사적인 가격 프리미엄이 침식되고 있습니다. 부품 비용이 낮아지면서 W 밴드의 보급이 시장 경쟁력을 재구성할 것으로 보입니다.

북미의 판매 점유율 32%는 성숙한 석유, 화학, 식품 산업과 수도 인프라의 디지털 업그레이드를 장려하는 연방 정부의 보조금으로 인한 것입니다. 유틸리티 기업은 클라우드에 연결된 레이더를 활용하여 현장 방문을 줄이고, 크래프트 맥주 제조업체는 적극적인 클린 인 플레이스 사이클을 견디는 위생 모델을 채택하고 있습니다.

아시아태평양은 CAGR 7.5%의 성장 엔진으로 중국의 석탄에서 화학제품으로의 전환 플랜트와 인도의 스마트 시티 폐수 프로젝트가 견인하고 있습니다. 호주 광산 회사는 광미 관리를 위해 거품에 강한 80GHz 단위를 지정하고 동남아시아의 팜유 정제소는 끈끈한 매체를 다루는 유도파 모델을 요구합니다.

유럽에서는 독일의 화학 공업 단지에서 공정 최적화와 메탄 배출 규제에 의해 대륙 전역에서 탱크 계량의 정밀도 향상이 의무화되어 견조한 기세를 유지하고 있습니다. 스칸디나비아의 유틸리티 회사는 추운 곳의 저수지에 적합한 저전력 레이더 센서를 조달하여 지속가능성과 유지 보수 점검 횟수를 줄이는 데 중점을 둡니다.

중동에서는 해수 담수화 붐이 장기적인 수요를 지원하고 있으며, 라틴아메리카에서는 구리와 리튬의 확장이 고형물 중심의 레이더 배치를 지원하고 있습니다. 아프리카 시멘트와 음료 부문은 전기의 보급에 따라 비용을 최적화하는 24GHz 단위를 채택합니다.

The radar level transmitter market is valued at USD 606.11 million in 2025 and is forecast to reach USD 902.36 million by 2030, advancing at a 5.77% CAGR.

Demand is anchored in industrial automation programs that require precise level monitoring to meet stricter environmental and safety mandates. Technology migration from ultrasonic to 80 GHz radar in European oil terminals, growing desalination capital spending across the Gulf states, and retrofit activity in aging North-American water utilities are pivotal growth vectors. Manufacturers are also benefiting from coal-to-chemicals projects in China, where complex interface measurements favor guided-wave radar, and from a steady move toward wireless, Industrial-Internet-ready sensors that support predictive maintenance. Competitive differentiation hinges on antenna miniaturization, advanced signal processing for foam or low-dielectric media, and service ecosystems that shorten commissioning times.

European regulations mandate advanced overfill protection, prompting operators to replace ultrasonic gauges with 80 GHz radar. Narrow beam angles concentrate microwave energy, delivering reliable measurements even through vapors and temperature swings, while compact antenna designs simplify retrofits in tanks fitted with floating roofs. Coupled with maintenance-free operation, the technology ensures compliance and lowers lifecycle cost.

Saudi Arabia, the UAE, and Kuwait collectively account for half of global desalination capacity. New multi-stage flash and reverse-osmosis plants demand non-contact radar that withstands corrosive, high-salinity brines. Integration with digital control systems improves energy efficiency and water recovery, embedding radar as a standard specification in regional EPC contracts.

Thick foam layers attenuate microwaves, causing spurious echoes that disrupt level control in ethoxylation or fermentation vessels. Enhanced signal processing and hybrid radar-capacitance probes mitigate, but physics still limits radar penetration in extreme foaming.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Non-contact sensors captured 65% of 2024 revenue, reflecting preference for maintenance-free operation in corrosive or high-temperature duties. The sub-segment will expand at 6.8% CAGR, reinforced by frequency-modulated continuous-wave (FMCW) platforms that sharpen signal-to-noise ratios. Guided-wave radar retains a niche where interface detection or heavy foam is prevalent. Compact 80 GHz antennas now retrofit vessels once limited to ultrasonic probes, enlarging addressable demand for the radar level transmitter market.

Digital advances such as Bluetooth commissioning and in-sensor diagnostics simplify compliance audits, enhancing the radar level transmitter industry's value proposition. Suppliers position self-monitoring features as a hedge against workforce shortages, elevating radar to a core node in enterprise asset-performance platforms.

K-band (24-26 GHz) still held 38% of 2024 shipments, appreciated for cost-effectiveness and broad approvals. Yet W-band (76-81 GHz and 120 GHz) sensors show 7.4% CAGR due to sub-3° beam angles that ignore agitator blades and narrow nozzles, delivering reliable readings in 40-m columns or slender brew kettles. Certification agencies in the United States, EU, and China cleared W-band for process use, driving scale economies that are eroding historic price premiums. As component costs fall, W-band penetration will remake competitive positioning in the radar level transmitter market.

The Radar Level Transmitter Market Report is Segmented by Technology (Contact System, Non-Contact System), Frequency Range (C and X Band, K Band, W Band), Application (Liquids/Interfaces, Solids), End-User Industry (Oil and Gas, Chemicals, Water, Power Generation, Pharmaceuticals and Biotechnology, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America's 32% revenue share stems from mature oil, chemical, and food industries, coupled with federal grants that incentivize digital upgrades in water infrastructure. Utilities leverage cloud-connected radar to cut field visits, while craft brewers adopt hygienic models that withstand aggressive clean-in-place cycles.

Asia-Pacific is the growth engine at 7.5% CAGR, led by Chinese coal-to-chemicals plants and Indian smart-city wastewater projects. Australian miners specify foam-tolerant 80 GHz units for tailings management, and Southeast Asian palm-oil refineries demand guided-wave models that handle sticky media.

Europe maintains steady momentum, driven by process optimization in Germany's chemical parks and methane-emission rules that mandate tighter tank-gauging accuracy across the continent. Scandinavian utilities procure low-power radar sensors suited to cold-climate reservoirs, emphasizing sustainability and reduced servicing trips.

The Middle East's desalination boom anchors long-term demand, whereas Latin America's copper and lithium expansions support solids-focused radar deployments. Africa's cement and beverage sectors adopt cost-optimized 24 GHz units as electrification spreads.