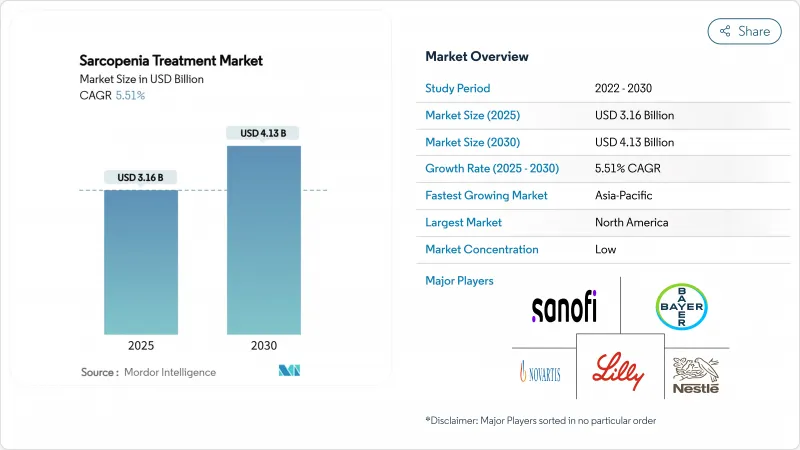

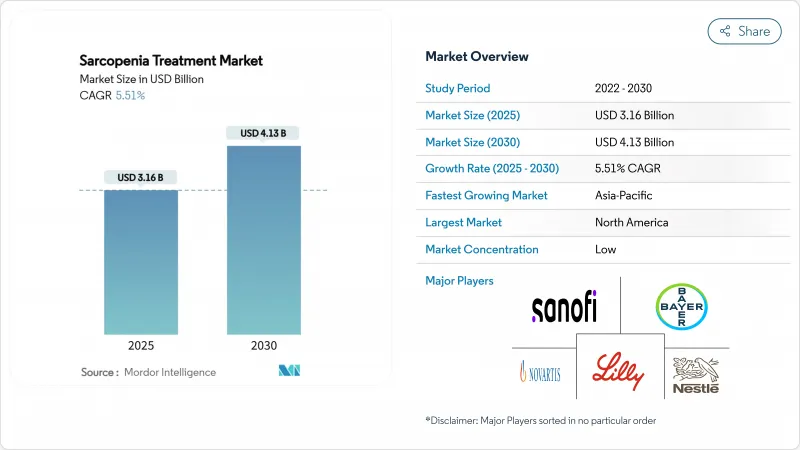

세계의 사코페니아 치료 시장 규모는 2025년 31억 6,000만 달러, 2030년까지 41억 3,000만 달러에 이를 것으로 예측되며, CAGR은 5.51%로 예상됩니다.

증거 기반 영양 프로토콜의 수용 확대, 미오스타틴 억제제 및 선택적 안드로겐 수용체 모듈레이터(SARMs)의 조기 파이프라인 기세, 디지털 진단의 이용 확대 등이 의료 현장에서의 꾸준한 보급을 지원하고 있습니다. 경쟁사와의 차별화가 가장 현저하게 나타나는 것은 건강증진 프로그램이 급속히 확대되고 있는 아시아태평양과 규제당국의 참여가 가속화되어 신규 후보약의 심사기간이 단축되고 있는 북미입니다. 한편, 임상 엔드포인트에 대한 규제 불확실성은 여전히 높으며, FDA와 EMA가 승인한 약리학적 제품도 없기 때문에 처방자가 보충제에서 약물 기반 요법으로 이동하는 속도는 제한되어 있습니다.

세계의 급속한 고령화가 사코페니아의 유병률을 급격히 밀어 올리고 있습니다. 유엔 데이터는 2070년대 후반에는 65세 이상의 노인이 22억 명에 달할 것으로 예측됩니다. 평균 수명이 연장됨에 따라 위험한 성인의 절대 수가 증가하고 임상 연구는 2형 당뇨병을 앓고 있는 노인 환자의 25.4%가 사코페니아를 일으키는 것으로 나타났습니다. 지불자는 근육 건강 상태의 스크리닝을 만성 질환의 경로에 통합함으로써 대응합니다. 일본의 지역 스크리닝 캠페인은 이미 근력 저하와 관련된 입원률을 줄이고 직접적인 비용 상쇄를 실증하고 있습니다. 그 결과 진단이 빨라지고 고품질의 단백질 블렌드의 처방량이 증가하고 약물 치료를 보완하는 운동 프로그램에 대한 등록이 증가하고 있습니다.

스폰서가 SARM과 마이오스타틴 억제제를 개발하여 임상 기세가 가속화되고 있습니다. Rejuvenate Biomed의 RJx-01은 제1b상 시험에서 악력과 피로 저항성을 개선하고, 2024년에 제2상 다시설 공동 시험을 개시합니다. GLP-1 보조요법의 병행 연구는 급무가 되고 있으며, Veru Inc.의 enobosarm은 2025년 분석 결과 세마글루티드 단독보다 제지방 체중을 71% 많이 유지했습니다. 투자자의 의욕은 골다공증과 허약체질의 이중적응의 조기 시사에 의해 더욱 높아지고 있으며, 보다 광범위한 상환 가능성을 시사하고 있습니다. 이러한 진전은 단기 변절을 시사하며 중요한 데이터가 성숙하면 영양 부위의 우위를 침식 할 수 있습니다.

사코페니아에 특화된 의약품은 아직 FDA도 EMA도 승인하지 않았기 때문에 많은 의사들이 영양 프로토콜에 의존하고 있습니다. 후기 단계에 있는 후보 약물은 제지방 체중을 증가시키지만, 기능적 엔드포인트 장애물에 도달하지 못할 수 있으며, 규제 당국의 신뢰를 손상시킵니다. 이 격차는 보험 회사에 의한 보험 적용을 지연시키고, 보험 청구서에 사코페니아를 표시하려고 하는 처방자의 의욕을 제한하고, 파이프라인이 부풀어 있어도 단기적인 의약품의 흡수를 억제하고 있습니다.

영양제제는 2024년의 사코페니아 치료 시장 매출의 80.91%를 차지해, 류신을 강화한 단백질이 근단백합성 합성을 촉진한다는 임상 근거의 확산과 소매점에서의 입수의 용이함이 뒷받침했습니다. 고령자가 약사의 상담을 요구하는 소매 약국에서의 매출이 급증하고, 정기 구입의 전자상거래 사이트는 자동 리필에 의한 어드히어런스를 강화했습니다. 동시에, 테스토스테론과 ACE 억제제가 매우 중요한 임상시험을 향해 진전하고 있기 때문에 의약품 부문은 CAGR 6.99%로 약진하고 있습니다. 퍼스트 인 클래스 승인이 가이드 라인의 무결성과 일치하면 의약품의 사코페니아 치료 시장 규모는 2030년까지 2억 6,600만 달러를 초과 할 수 있습니다.

파이프라인의 다양성이 이 가속을 지원합니다. GLP-1에 의한 제지방 체중 감소를 완화하는 Enobosarm의 능력은 내분비 전문의의 관심을 모으고 있으며, Epirium Bio의 MF-300은 미토콘드리아 경로를 표적으로 하고, 2024년 후반에 IND가 승인됩니다. 고품질의 단백질과 경구 SARMs를 결합한 병용 요법도 초기 시험 단계에 있으며, 근력, 지구력, 일상 생활 기능에 걸친 멀티 모달 효과를 노리고 있습니다.

2024년의 사코페니아 치료 시장 매출의 87.37%를 경구 요법이 차지하고 있는데, 이것은 소비자가 분말, 정제, 츄어블에 익숙해져 있는 유산입니다. 1일 1회 복용할 수 있는 파우치의 편리성은 노인의 복약 준수의 실태에 합치하고 있어, 제조업체는 차별화를 도모하기 위해, 비타민 D, 오메가 3, 프로바이오틱스를 제품에 계속 강화하고 있습니다. 이와 대조적으로, 비경구 약물의 선택, 주로 피하 투여되는 펩티드 생물학적 제형은 CAGR 5.92%로 확대될 전망입니다. 높은 생체이용률과 분기별 투여가 가능한 주사제는 흡수 불량이나 심한 이동 제한에 직면한 환자에게 매력적입니다.

또한, 장시간 작용하는 미오스타틴 항체는 초기 시험에서 지속적인 제지방 체중 증가를 보여줍니다. 경피 흡수 패치는 여전히 수작업 상태이지만 국소 근육 감소에서 틈새 이용 사례를 열 수 있습니다.

사코페니아 치료 시장 보고서는 치료 유형별(단백질 보충제, 의약품, 병용 요법), 투여 경로별(경구, 비경구, 경피 및 국소), 유통 채널별(병원 약국, 소매 약국, 기타), 질환 유형별(원발성 사코페니아, 2차성 사코페니아), 지역별로 분류하고 있습니다. 시장 및 예측은 금액(달러)으로 제공됩니다.

2024년 사코페니아 치료 시장 매출의 42.57%는 북미가 차지했는데, 이것은 왕성한 보험 상환과 배합 단백질이나 임상시험 SARM에 정통한 노년병 전문의의 치밀한 네트워크가 원동력이 되고 있습니다. Lipocine의 LPCN 1148이 2024년 12월에 FDA의 패스트트랙에 인정된 것은 간경변과 관련된 사코페니아에 대한 규제 당국의 주목도가 높아지고 있다는 것을 강조하는 것이지만, 헬스케어 기업의 AI 대응 스크리닝 툴은 1차 케어 의사가 조기에 이 지역의 사코페니아 치료 시장 규모는 Medicare Advantage 플랜이 예방 근육 건강 혜택을 통합함에 따라 꾸준히 상승할 것으로 예측됩니다.

아시아태평양은 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 7.17%에서 가장 빠르게 성장하는 지역입니다. 일본의 국가적인 프레일티 체크 프로그램은 약국에서의 악력 검사를 조성하고 중국은 관민 자본을 레지스턴스 트레이닝 기술을 갖춘 노인 케어 거점에 투입하고 있습니다. Astellas과 Jiangsu Hengrui 등 현지 제약 기업은 동아시아의 표현형에 맞춘 미오스타틴 항체 프랜차이즈에 연구 개발 자금을 투입하고 있습니다. 스마트폰의 보급률도 높기 때문에 개인에 맞춘 봉지를 발송하는 원격 영양 서비스의 보급도 가속하고 있습니다.

유럽은 수년간의 노인 의료 인프라와 EWGSOP2 정의의 통일적 역할을 통해 확고한 발판을 유지하고 있습니다. 독일과 영국은 골다공증과 사코페니아를 중앙 집중화하고 어드히어런스를 높이는 근육 클리닉을 시험적으로 도입하고 있습니다. Horizon-Europe의 보조금은 데이터 보호 규정을 준수하는 근력 측정 웨어러블을 개발하는 중소기업에 인센티브를 부여하고, 지중해 연안 국가는 전통적인 식생활의 단백질 강화를 강조합니다. 남미, 중동, 아프리카는 규모는 작지만 다국간 보건 원조 프로그램이 1차 케어 센터에 단백질 혼합 식품을 보관하는 지역 영양 계획에 자금을 제공하고 있기 때문에 전진하고 있습니다.

The sarcopenia treatment market size stands at USD 3.16 billion in 2025 and is forecast to reach USD 4.13 billion by 2030, reflecting a 5.51% CAGR.

Moderate expansion stems from a formal disease classification that is raising diagnosis rates while reimbursement pathways broaden in the most developed health systems Growing acceptance of evidence-based nutritional protocols, early pipeline momentum for myostatin inhibitors and selective androgen receptor modulators (SARMs), and rising use of digital diagnostics all underpin steady uptake across care settings. Competitive differentiation is most visible in Asia-Pacific, where healthy-aging programmes are scaling rapidly, and in North America, where accelerated regulatory engagement is shortening review times for novel candidates. Meanwhile, persistent regulatory uncertainty around clinical endpoints and the ongoing absence of an FDA- or EMA-approved pharmacological product restrain the pace at which prescribers pivot from supplementation to drug-based regimens.

A rapidly aging world is sharply boosting sarcopenia prevalence. United Nations data project that people aged >= 65 will number 2.2 billion by the late 2070s. Higher life expectancy raises the absolute pool of at-risk adults, and clinical studies reveal that 25.4% of older patients living with type 2 diabetes subsequently develop sarcopenia. Payers are responding by embedding muscle-health screening into chronic-disease pathways. Japan's community screening campaigns have already trimmed hospitalization rates tied to muscle weakness, demonstrating direct cost offsets. The upshot is earlier diagnosis, rising prescription volumes of high-quality protein blends, and heightened enrolment in exercise programmes that complement pharmacotherapy.

Clinical momentum is accelerating as sponsors advance SARMs and myostatin inhibitors. Rejuvenate Biomed's RJx-01 improved grip strength and fatigue resistance in Phase 1b, prompting a Phase 2 multicentre trial in 2024. Parallel work on GLP-1-adjunct therapies has gained urgency; Veru Inc.'s enobosarm preserved 71% more lean mass than semaglutide alone in a 2025 read-out. Investor appetite is further buoyed by early indications of dual indications in osteoporosis and frailty, suggesting broader reimbursement potential. These advances signal a near-term inflection that could erode the nutritional segment's dominance once pivotal data mature.

No drug has yet cleared either FDA or EMA review specifically for sarcopenia, keeping many physicians anchored to nutritional protocols. Late-stage candidates occasionally boost lean mass yet miss functional-endpoint hurdles, undermining regulatory confidence. This gap delays payer coverage and limits prescriber willingness to label sarcopenia on claims forms, muting near-term pharmaceutical uptake even as pipelines swell.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Nutritional formulations generated 80.91% of the sarcopenia treatment market revenue in 2024, bolstered by ready retail access and expanding clinical evidence that leucine-enriched protein elevates muscle-protein synthesis. Sales surged through retail pharmacies where seniors seek pharmacist counselling, while subscription e-commerce sites enhanced adherence through auto-refill. At the same time, the pharmaceutical segment is pacing ahead at a 6.99% CAGR as testosterone and ACE inhibitors progress toward pivotal trials. The sarcopenia treatment market size for pharmaceuticals could exceed USD 266 million by 2030 if first-in-class approvals align with guideline harmonisation.

Pipeline diversity underpins this acceleration. Enobosarm's ability to mitigate GLP-1-induced lean-mass loss has attracted the interest of endocrinologists, and Epirium Bio's MF-300 targets mitochondrial pathways, with an IND cleared in late 2024. Combination regimens pairing high-quality protein with oral SARMs are also in early testing, aiming to deliver multimodal benefits across strength, endurance, and daily-living function.

Oral therapies commanded 87.37% share of sarcopenia treatment market sales in 2024, a legacy of consumer familiarity with powders, tablets, and chewables. The convenience of once-daily sachets aligns with geriatric adherence realities, and manufacturers continue to fortify products with vitamin D, omega-3s, and probiotics for added differentiation. In contrast, parenteral options-chiefly peptide biologics delivered subcutaneously-are expanding at an 5.92% CAGR. High bioavailability and the possibility of quarterly dosing make injectables attractive for patients facing malabsorption or severe mobility limitations.

Developers are refining depot formulations to minimise clinic visits, and long-acting myostatin antibodies have shown durable increases in appendicular lean mass in early pilots. Transdermal patches remain exploratory but could open niche use cases in regional muscle loss.

The Sarcopenia Treatment Market Report is Segmented Into by Treatment Type (Protein Supplements, Pharmaceuticals, and Combinational Therapies), by Route of Administration (Oral, Parenteral, and Transdermal / Topical), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), Disease Type (Primary Sarcopenia and Secondary Sarcopenia), and Geography). The Market and Forecasts are Provided in Terms of Value (USD).

North America accounted for 42.57% of sarcopenia treatment market revenue in 2024, driven by robust reimbursement and a dense network of geriatricians familiar with curated protein blends and investigational SARMs. FDA Fast Track status for Lipocine's LPCN 1148 in December 2024 underscores growing regulatory focus on cirrhosis-related sarcopenia, while AI-enabled screening tools from health-tech firms help primary-care doctors spot early deficits. The sarcopenia treatment market size in the region is projected to climb steadily as Medicare Advantage plans integrate preventive muscle-health benefits.

Asia-Pacific is the fastest-growing arena at a 7.17% CAGR between 2025 and 2030. Japan's national Frailty Check programme subsidises grip-strength testing in pharmacies, while China channels public-private capital into elder-care hubs outfitted with resistance-training technology. Local pharma players such as Astellas and Jiangsu Hengrui are funnelling R&D funds into myostatin-antibody franchises tailored for East-Asian phenotypes. High smartphone penetration also accelerates adoption of tele-nutrition services that ship personalised sachets.

Europe retains a solid foothold owing to longstanding geriatric-care infrastructure and the unifying role of EWGSOP2 definitions. Germany and the United Kingdom are piloting "muscle-clinics" that co-manage osteoporosis and sarcopenia under one roof, boosting adherence. Horizon-Europe grants incentivise SMEs to develop strength-measuring wearables compliant with data-protection rules, while Mediterranean countries emphasise protein enrichment of traditional diets. South America, the Middle East, and Africa are smaller but advancing as multilateral health-aid programmes finance community-nutrition schemes that stock protein blends in primary-care centres.