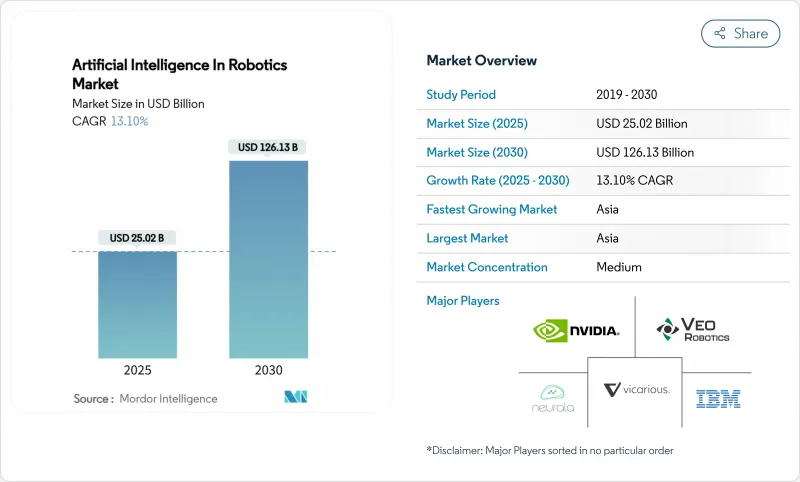

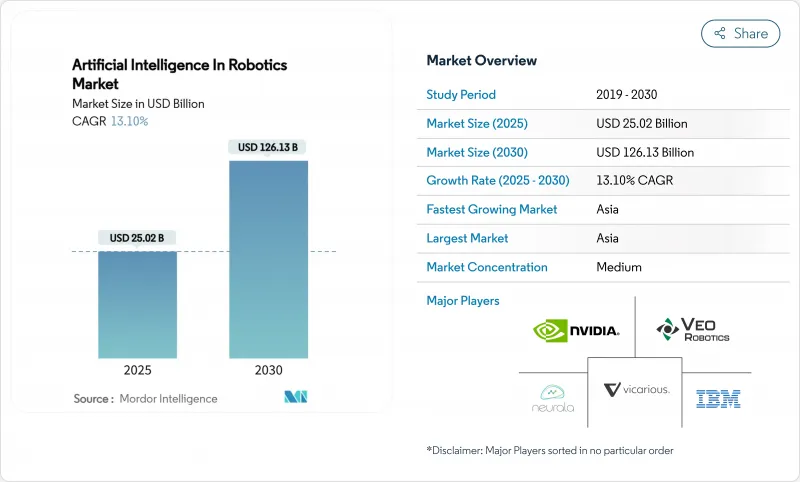

로봇공학 분야 인공지능(AI) 시장 규모는 2025년에 250억 2,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 13.10%로, 2030년에는 1,261억 3,000만 달러에 달할 것으로 예상됩니다.

그 기세를 지원하는 것은 엣지 컴퓨팅, 머신러닝 알고리즘, 고해상도 센서의 급속한 발전으로, 로봇은 주변 환경을 해석하고 밀리초 단위로 자율적으로 행동할 수 있습니다. 제조업체는 순수한 기계적 업그레이드에서 인텔리전스 중심 개선으로 전환하고 있으며 생산 라인 및 서비스 환경에서 의사 결정 대기 시간을 단축하는 맞춤형 AI 프로세서 모듈을 통합합니다. 아시아 제조업 투자, 북미 전자상거래 붐, 유럽의 협력 연구 프로그램은 전개 시나리오를 확대하고 가치 실현까지의 시간을 가속화하기 위해 수렴하고 있습니다. 하드웨어는 여전히 큰 비용 드라이버이지만, 소프트웨어 장착률의 상승은 가치 창출이 지각, 추론, 적응 제어 스택으로 이동하고 로봇이 커넥티드 팩토리 및 물류 생태계 내에서 지속적으로 학습하는 자산이 되고 있음을 보여줍니다. 이러한 동향의 복합 효과에 의해 인간의 오퍼레이터를 치환하는 것이 아니라, 오히려 보완하는 인텔리전트 머신의 설치 베이스가 점점 확대되고, 로봇 AI 시장의 대응 가능한 수요가 확대하고 있습니다.

에지 AI 프로세서는 의사 결정 대기 시간을 몇 초에서 밀리초로 줄여 클라우드에 의존하지 않고 자율 이동 로봇(AMR)이 동적 생산 현장을 탐색할 수 있도록 합니다. 어드밴텍의 2025년 쇼케이스에서는 AMR 플릿에 NVIDIA Jetson Thor 모듈을 통합한 후 응답 시간이 75% 빨라진 것을 소개했습니다. 심천과 수원에 위치한 전자기기 제조업체는 비전과 모션 데이터를 현지에서 처리함으로써 첫 패스 수율과 택트 타임 절감에서 측정 가능한 이익을 보고합니다. 또한 대기 시간이 낮아짐에 따라 예측 유지 보수를 위한 피드백 루프가 강화되고 정밀 조립 라인의 예정되지 않은 다운타임이 줄어듭니다. 에지에 최적화된 AI 모델이 성숙함에 따라 프로세서 비용이 낮아지고 있으며, 중견 공급업체가 새로운 유닛을 구입하는 대신 기존 로봇을 개조하도록 권장합니다. 따라서 이러한 촉진요인은 다양한 공장에서의 채용을 확대하고 로봇 AI 시장에 플러스에 기여합니다.

파나소닉, 소프트뱅크, 일본 정부가 지원하는 신흥기업은 딥 뉴럴 네트워크를 사용하여 넘어짐을 감지하고, 투약 스케줄을 리마인드하고, 자연스러운 대화로 상호작용하는 이동 로봇과 사회적 반주 로봇을 전개하고 있습니다. 임상시험에서는 로봇이 반복적으로 수행되는 리프팅 및 감시작업을 재할당함으로써 간호사가 환자와의 직접적인 관계에 집중할 수 있게 되어 직원의 효율이 향상되는 것으로 나타났습니다. 같은 인구동태의 역풍에 직면하고 있는 한국은 '로봇산업비전 2030' 계획을 통해 AI 로봇 간병사에 투자하고 있으며, 병원 배치 및 재택간병 시험에 보조금을 내고 있습니다. 이 두 문화적 조기 어댑터의 성공은 인구 고령화가 진행되는 유럽의 건강 관리 제공업체의 벤치마크가 되어 로봇 시장에서 AI의 미래 대응 가능 수요를 확대할 것입니다.

Frontiers in Robotics and AI는 일관성이 없는 불완전한 데이터 세트가 인간과 로봇의 협력 작업의 신뢰성을 저하시킨다는 점을 강조합니다. 예를 들어, 농작물 수확기는 다양한 작물 품종의 숙도를 측정하는 데 어려움을 겪고 있으며, 시험 농장 이외의 상업적 배포가 제한됩니다. 데이터 갭은 안전성 검증을 방해하기 때문에 공급업체는 인식 스택을 과도하게 설계할 수 없으며 제품화 시간이 길어집니다. 독자적인 데이터 세트는 대규모 기존 기업에 해자를 제공하여 소규모 혁신자가 성능 벤치마크와 비교할 수 없게 만듭니다. 합성 데이터 생성과 전이 학습이 이 장벽을 완화하고 있다고는 해도, 부족은 로봇 시장에서의 AI의 전체적인 확대의 발판이 되고 있습니다.

로봇에 물리적인 존재감을 주는 센서, 액추에이터, 구동 장치, 구조 프레임을 반영해 2024년 로봇 AI 시장 점유율의 62%를 하드웨어가 차지했습니다. 힘 센서를 내장한 자본 집약형 산업용 암은 용접, 도장, 정밀 자재관리에 필수적인 것으로 변함이 없습니다. 공급업체는 현재 시스템을 전반적으로 오버홀하지 않고 그리퍼, 카메라, AI 에지 모듈을 교체할 수 있는 모듈 설계를 출시하고 있으며, 총 소유 비용을 절감하고 장비 수명 주기를 연장하고 있습니다. 하드웨어 로드맵은 전력 효율적인 서보 컨트롤러와 가벼운 복합 조인트를 강조하고 있으며, 좁은 공장 통로를 이동하는 로봇에 있어서 중요한 보다 높은 휴대 중량 대 중량비를 실현하고 있습니다.

머신 러닝 및 딥러닝 소프트웨어는 CAGR 24%로 확장되었으며, 사전 학습된 지각 및 모션 계획 라이브러리로 번들링되는 경우가 많습니다. 이러한 스택은 외부 프로그래밍 없이 결함 감지, 예측 유지 보수 및 적응형 파지를 가능하게 함으로써 기존 기계에서 더 많은 가치를 끌어냅니다. 조기 도입 기업의 보고에 따르면 소프트웨어 업그레이드만으로 전체 기기의 효율성을 두 자리 올릴 수 있으며, 기준선이 작음에도 불구하고 소프트웨어가 물리적 지출을 초과하는 이유를 보여줍니다. 통합, 원격 모니터링 및 지속적인 모델 재교육을 다루는 서비스는 고객이 라이프사이클 지원을 요청함에 따라 공급업체에게 증가하는 연금 흐름을 형성합니다. 이 변화는 로봇공학 분야 인공지능(AI) 시장에서 메커니즘이 아닌 인텔리전스가 경쟁사를 차별화하는 방법을 명확하게 보여줍니다.

산업용 로봇은 2024년 로봇 AI 시장 규모의 68%를 차지하며 자동차 및 전자기기 생산에 도입되는 다관절 암이 견인했습니다. 로봇 설치 대수는 세계 공장에서 428만대를 돌파해 연률 10% 증가로 수요 정착이 부각되었습니다. AI 업그레이드를 통해 이러한 시스템은 재티칭을 위한 다운타임 없이 가변 부품 형상을 처리할 수 있어 자산 활용도가 향상됩니다. 코봇은 아직 출하 대수의 소수파이지만, 다품종 소량 생산 환경에서는 유연한 자동화가 불가결해져, 대폭적인 성장을 이루고 있습니다.

의료 및 헬스케어 로봇은 2025-2030년의 CAGR이 26%로, 가장 급성장하고 있는 클래스입니다. 컴퓨터 비전과 포스 피드백을 통합한 수술 시스템은 낮은 침습 수술로 임상의를 지원하고 수술 후 합병증과 입원 기간을 단축합니다. 병원 물류 로봇은 AI 의사 결정 엔진과 융합된 동시 정위 매핑(SLAM)을 사용하여 혼잡한 복도에서 린넨과 약을 자율적으로 운반합니다. 고령자의 일상생활 작업을 지원하는 재택 간병 로봇이 증명하고 있는 것처럼, 소비자의 수용은 퍼지고 있습니다. 이러한 동향을 종합하면 수익 풀이 다양화되고 자동차 중심 수요에 내재하는 순환성이 완화되기 때문에 로봇 AI 시장은 혜택을 받게 됩니다.

로봇공학 분야 인공지능(AI) 시장은 구성 요소별(하드웨어, 기타), 로봇 유형별(산업용 로봇, 서비스 로봇, 기타), 용도별(제조·조립, 물류 및 창고, 헬스케어·수술, 기타), 최종 사용자 산업별(자동차, 일렉트로닉스, 반도체, 기타), 지역별로 분류되어 있습니다.

아시아태평양은 중국, 일본, 한국의 대규모 자동화 프로그램에 견인되어 2024년에는 세계 매출의 47%를 차지했습니다. 중국에서만 2023년에 27만 6,288대의 산업용 로봇이 설치되었으며, 이는 세계 출하 대수의 51%에 해당합니다. 지방 당국이 제조 경쟁력을 높이기 위해 세제 우대 조치와 저이자 대출을 제공하고 있기 때문입니다. 한국의 일렉트로닉스 기업은 미크론 단위의 웨이퍼 레벨의 공차를 관리하기 위해 픽 앤 플레이스 셀에 엣지 AI 비전을 추가하고, 일본의 자동차 제조업체는 인간과 같은 손쉬움을 필요로 하는 최종 트림 작업에 AI 코봇을 도입하고 있습니다. 이 지역의 CAGR 예측 18%는 제조업의 우위성뿐만 아니라, 급속히 대두하는 헬스케어나 서비스 로봇의 파일럿도 반영하고 있습니다.

북미는 AI 소프트웨어에 관한 전문지식이 풍부한 미국을 중심으로 신흥기업의 설립과 벤처기업의 자금조달이 활발해 2위를 차지하고 있습니다. 물류 대기업은 기존 컨베이어 그리드를 AI 모바일 로봇으로 개수하여 2시간 이내 배송을 실현하고 있습니다. 자동차 제조업체는 공장이 배터리 전기자동차에 대응하기 위해 AI를 활용하여 새로운 경량 소재의 용접 품질을 모니터링하고 도입을 가속화하고 있습니다. 캐나다의 광업 부문은 AI 인식 스택을 활용하여 저 GPS 환경 하에서 노천 채굴장을 탐색하는 자율주행식 운반 트럭을 시험적으로 도입하여 AI 로봇 시장의 침투를 공장 벽을 넘어 확대합니다. 멕시코의 산업 지대는 마찬가지로 USMCA의 컨텐츠 규칙에 따라 경쟁력을 유지하기 위해 AI 리노베이션을 도입했습니다.

유럽은 윤리적이고 안전하며 신뢰할 수 있는 인공지능을 중시하며 기술 개발과 규제 프레임워크을 형성하고 있습니다. 독일은 2023년에 2만 8,355대의 로봇을 신규 도입하여 로봇 밀도를 선도했습니다. 호라이즌 유럽의 보조금은 농업 기술, 건강 관리 및 녹색 제조 산업을위한 로봇공학의 산학 클러스터를 장려합니다. 하지만 CE 마킹과 AI의 책임에 대한 해석이 나뉘어져 있기 때문에 특히 코봇에 대해서는 국경을 넘은 전개가 늦어지고 있습니다. 노동력 부족이 공장에 투자를 촉구하는 가운데 중동유럽의 성장 잠재력은 여전히 높습니다. 남미, 중동 및 아프리카의 소규모 시장은 아직 발전도상이지만 선행투자 장벽을 낮추는 턴키·Robot-as-a-Service 계약의 혜택을 받고 있으며, 로봇 AI 시장의 세계적인 확대를 뒷받침하고 있습니다.

The Artificial Intelligence In Robotics Market size is estimated at USD 25.02 billion in 2025, and is expected to reach USD 126.13 billion by 2030, at a CAGR of 13.10% during the forecast period (2025-2030).

Momentum is underpinned by rapid advances in edge computing, machine learning algorithms, and high-resolution sensor suites that allow robots to interpret their surroundings and act autonomously in milliseconds. Manufacturers are shifting from purely mechanical upgrades to intelligence-centric improvements, embedding custom AI processor modules that shorten decision latency on production lines and in service environments. Asia's manufacturing investments, North America's e-commerce boom, and Europe's coordinated research programs are converging to expand deployment scenarios and accelerate time-to-value. Hardware remains a large cost driver, yet rising software attach rates illustrate how value creation is migrating toward perception, reasoning, and adaptive-control stacks, turning robots into continuously learning assets within connected factory and logistics ecosystems. The combined effect of these trends is creating an ever-larger installed base of intelligent machines that complement, rather than displace, human operators, widening addressable demand for the AI in robotics market.

Edge-AI processors cut decision-making latency from seconds to milliseconds, enabling autonomous mobile robots (AMR) to navigate dynamic production floors without cloud dependence. Advantech's 2025 showcase highlighted 75% faster response times after integrating NVIDIA Jetson Thor modules into AMR fleets. Electronics manufacturers in Shenzhen and Suwon report measurable gains in first-pass yield and takt-time reduction when vision and motion data are processed locally. Lower latency also tightens feedback loops for predictive maintenance, decreasing unscheduled downtime in precision assembly lines. As edge-optimized AI models mature, processor costs are falling, encouraging mid-tier suppliers to retrofit existing robots instead of purchasing new units. The driver, therefore, widens adoption across diverse factory footprints and contributes positively to the AI in robotics market .

Japan's share of residents aged 65 plus exceeded 29% in 2025, amplifying a projected shortfall of 377,000 caregivers.Panasonic, SoftBank, and startups backed by the Japanese government are rolling out mobility and social-companion robots that use deep neural networks to detect falls, remind medication schedules, and interact through natural speech. Clinical pilots show robots increase staff efficiency by reallocating repetitive lifting or monitoring tasks, letting nurses focus on direct patient engagement. South Korea faces similar demographic headwinds and is investing in AI robotic caregivers through its "Robot Industry Vision 2030" plan, which subsidizes hospital deployments and homecare trials. Success in these two cultural early adopters sets benchmarks for healthcare providers in Europe as their populations age, broadening future addressable demand for AI in the robotics market.

Frontiers in Robotics and AI highlights that inconsistent, incomplete datasets reduce the reliability of human-robot collaboration, especially where robots must recognize uncommon objects. For example, agricultural harvesters struggle to gauge ripeness across diverse crop varieties, limiting commercial deployment beyond pilot farms. Data gaps also impede safety validation, forcing vendors to over-engineer perception stacks and prolong time-to-market. Proprietary datasets give large incumbents a moat, making it harder for smaller innovators to match performance benchmarks. While synthetic data generation and transfer learning mitigate the barrier, the shortage remains a drag on the overall expansion of AI in the robotics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware accounted for 62% of the AI in robotics market share in 2024, reflecting the sensors, actuators, drives, and structural frames that give robots their physical presence. Capital-intensive industrial arms with integrated force-torque sensors remain indispensable for welding, painting, and precision material handling. Vendors are now shipping modular designs that let manufacturers swap grippers, cameras, or AI edge modules without full system overhauls, lowering total cost of ownership and prolonging equipment life cycles. Hardware roadmaps emphasize power-efficient servo controllers and lightweight composite joints, enabling higher payload-to-weight ratios crucial for mobile robots in tight factory aisles.

Machine Learning & Deep Learning software is expanding at a 24% CAGR and is increasingly bundled as pre-trained perception and motion-planning libraries. These stacks extract more value from existing machines by enabling defect detection, predictive maintenance, and adaptive grasping without external programming. Early adopters report that software upgrades alone can raise overall equipment effectiveness by double digits, illustrating why software is outpacing physical spend despite its smaller baseline. Services covering integration, remote monitoring, and continuous model retraining form a rising annuity stream for vendors as customers seek lifecycle support. The shift underlines how intelligence rather than mechanics now differentiates competitors in the AI in robotics market.

Industrial robots commanded 68% of the AI in robotics market size in 2024, led by articulated arms deployed in automotive and electronics production. Their installed base surpassed 4.28 million units in factories worldwide, a 10% annual gain that highlights entrenched demand. AI upgrades are letting these systems handle variable part geometries without downtime for re-teaching, boosting asset utilization. Cobots, still a minority of shipments, enjoy outsized growth as flexible automation becomes essential for high-mix, low-volume environments.

Medical & healthcare robots represent the fastest-growing class at a 26% CAGR for 2025-2030. Surgical systems incorporating computer vision and force feedback assist clinicians in minimally invasive procedures, trimming post-operative complications and length of stay. Hospital logistics robots autonomously ferry linens and medications through crowded corridors using simultaneous localization and mapping (SLAM) fused with AI decision engines. Consumer acceptance is widening, evidenced by homecare robots that support daily living tasks for seniors. Altogether, these trends diversify revenue pools and mitigate cyclicality inherent in automotive-centric demand, benefiting the AI in robotics market.

The Artificial Intelligence in Robotics Market is Segmented by Component (Hardware and More), Robot Type (Industrial Robots, Service Robots and More), Application (Manufacturing and Assembly, Logistics and Warehousing, Healthcare and Surgery and More), End-User Industry (Automotive, Electronics, and Semiconductors, and More), and Geography.

Asia Pacific generated 47% of global revenue in 2024 driven by extensive automation programs in China, Japan, and South Korea. China alone installed 276,288 industrial robots in 2023, equal to 51% of world shipments, as local authorities provide tax incentives and low-interest loans to upgrade manufacturing competitiveness ifr.org. Korean electronics firms add edge-AI vision to pick-and-place cells to manage wafer-level tolerances measured in microns, while Japanese automakers deploy AI cobots for final trim operations that require human-like dexterity. The region's projected 18% CAGR reflects not only manufacturing dominance but also fast-emerging healthcare and service robotics pilots.

North America ranks second, anchored by the United States where AI software expertise seeds robust startup formation and venture funding. Logistics giants retrofit existing conveyor grids with AI mobile robots to meet two-hour delivery windows. Automakers accelerate adoption as factories retool for battery electric vehicles, using AI to monitor weld quality on new lightweight materials. Canada's mining sector pilots autonomous haulage trucks that leverage AI perception stacks to navigate open-pit sites in low-GPS conditions, extending AI in robotics market penetration beyond factory walls. Mexico's industrial corridors likewise embrace AI retrofits to stay competitive following USMCA content rules.

Europe emphasizes ethical, safe, and trustworthy AI, shaping both technology development and regulatory frameworks. Germany leads robot density with 28,355 new installations in 2023, aided by government subsidies for Mittelstand automation projects. Horizon Europe grants encourage academic-industry clusters in robotics for agri-tech, healthcare, and green manufacturing. Nonetheless, diverging interpretations of CE marking and AI liability delay cross-border deployments, particularly for cobots. Growth potential in Central and Eastern Europe remains high as labor shortages push factories to invest. Smaller markets in South America, the Middle East, and Africa are nascent but benefit from turnkey Robot-as-a-Service contracts that lower upfront capital barriers, nudging global uptake of the AI in robotics market.