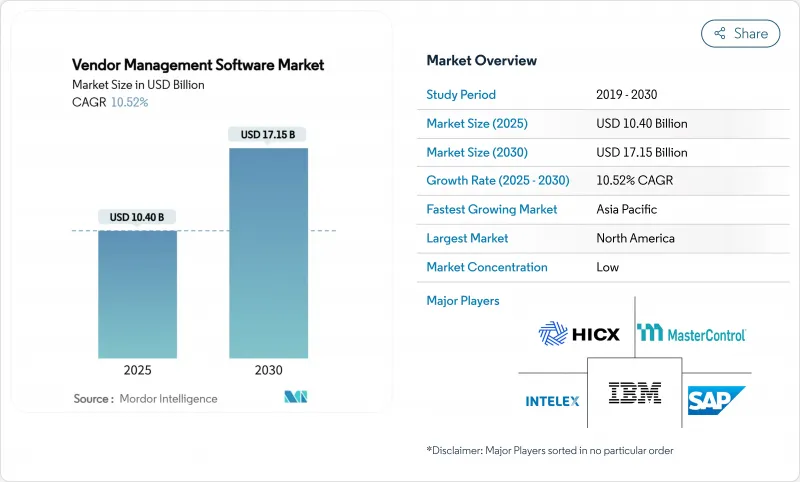

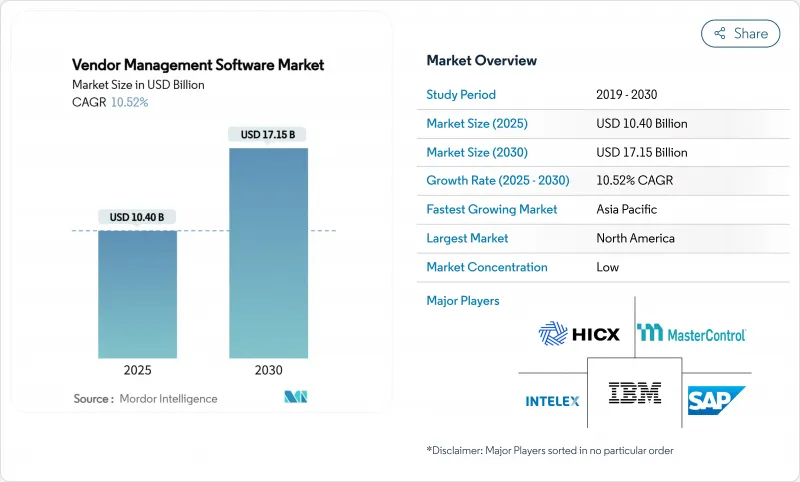

벤더 관리 소프트웨어 시장 규모는 2025년에 104억 달러에 이르고, CAGR은 10.52%를 나타내, 2030년에는 171억 5,000만 달러에 달할 것으로 예상됩니다.

강한 기세는 공급망의 복잡성, 재료비 상승, 규제 모니터링이 수렴함에 따라 공급업체와의 관계를 디지털화하고자 하는 기업의 요구를 반영합니다. 클라우드 네이티브 배포, AI 주도 분석, 임베디드 컴플라이언스 모니터링은 현재 새로운 구매의 기준이 되고 통합된 Source-to-Pay 제품군은 꾸준히 포인트 툴을 대체하고 있습니다. 수작업 모니터링은 수백 개의 타사로 확장할 수 없기 때문에 온보딩을 간소화하고 공급업체의 데이터를 중앙 집중화하며 예측 인사이트를 제공하는 플랫폼 공급업체가 우위를 차지하고 있습니다. 경쟁 구도은 여전히 완만하며 기존의 ERP 공급업체, 최고의 블리드 전문가, AI 네이티브 진출기업이 이 분야를 공유하고 있습니다.

공급업체의 반복 작업을 자동화하면 조달 오버헤드를 줄이고 전략적 소싱을 위해 팀을 확보할 수 있습니다. Wefunder는 CloudEagle 플랫폼을 통해 계약 갱신을 자동화한 후 연간 1,350시간과 평생 비용 41만 6,000달러를 절약했습니다. BetterCloud는 3배의 ROI를 보장합니다. 인플레이션이 금리를 좁히는 동안 코스트 테이크 아웃 동기는 업계 전반에 걸쳐 채용을 가속화하고 있습니다.

클라우드 네이티브 플랫폼은 배포 주기를 단축하고, 자본 지출을 줄이고, 거래량에 따른 수수료를 지불하는 탄력적인 확장성을 제공합니다. Choice Hotels International은 Finnout의 SaaS 환경에서 프로덕션 직후 98.8%의 정확한 비용 배분을 달성했습니다. 실시간 협업, API 기반 ERP 연결 및 자동 보안 패치 적용으로 특히 IT 인력이 부족한 지역에서는 클라우드가 기본 옵션이 됩니다.

Conexis VMS는 통합, 커스터마이징 및 데이터 마이그레이션이 초기 예산을 두 배로 늘릴 수 있으며 소규모 기업에서는 단계적 롤아웃이 필요하다고 지적합니다.

클라우드 도입은 2024년에 벤더 관리 소프트웨어 시장의 63.2%를 차지했고, 2030년까지의 CAGR은 12.9%를 나타낼 것으로 예측되고 있습니다. 클라우드 배포는 초기 비용 절감, 가치 실현까지의 시간 단축, 보안 관리를 최신 상태로 유지하는 실시간 업데이트 푸시 기능으로 널리 받아들여지고 있습니다. Choice Hotels에서 Finnout의 성공은 기업이 기대하는 빠른 성과를 보여줍니다. 이와는 대조적으로, On-Premise 모델은 주로 민감한 주권을 의무화된 조직에 호소하고 있습니다. 통합 워크로드와 AI의 컴퓨팅 요구 사항은 비용 이익 방정식을 클라우드로 기울입니다. SaaS의 협업과 분석 레이어를 활용하면서 중요한 데이터를 사내에 유지하는 하이브리드 경로도 존재합니다. 시장 역학은 거래 처리 능력에 따라 확장되는 구독 가격으로 강화됩니다.

2세대 SaaS 제품군은 공급업체의 위험을 예측하고 비용 절감을 권장하며 컴플라이언스의 증거 수집을 자동화하는 AI 엔진도 번들로 제공합니다. 이러한 기능은 클라우드의 탄력성에 따라 달라지며 사용자는 맞춤형 인스턴스를 설정할 수 있습니다. 업그레이드가 자동으로 이루어지기 때문에 IT 팀은 일상적인 패치 적용이 아닌 전략적인 데이터 스튜어드십에 노력을 기울일 수 있습니다. 그 결과 클라우드는 벤더 관리 소프트웨어 시장이 진화하면서 중요한 역할을 계속하고 있습니다.

제조업은 2024년 매출의 37.3%를 차지하고 품질, 납기, ESG 지표의 세밀한 시각화를 요구하는 다층 공급망을 반영했습니다. Johnson Controls의 LeanDNA 배포는 동기화된 부품, 공급업체 및 재고 데이터로부터 공장 네트워크가 어떻게 혜택을 받는지 보여줍니다. 원재료의 급등과 지정학적 사건으로 인해 생산자는 조달처를 다양화할 필요가 있습니다. 소매업은 옴니채널의 성장, 프라이빗 브랜드의 확대, 소비자 수요에 맞춘 구색의 필요성 등을 배경으로 규모가 작은 것, CAGR은 가장 빠른 11.2%를 나타낼 전망입니다.

규제 당국이 핀테크 콜라보레이션을 정사하는 가운데 금융 서비스의 도입이 가속. Ncontracts사에 따르면 금융기관의 73%는 300개 이상의 벤더를 관리하면서도 2명 이하의 직원으로 벤더 리스크 부문을 구성하고 있습니다. 의료 제공자는 HIPAA에 준거한 감시를 우선합니다. 미국 Med-Equip사에서 Vanta를 도입하면 감사 준비가 50% 절감되었습니다. 각국 정부는 BidNet Direct와 같은 솔루션을 통해 투명성과 공급업체의 다양성을 높이기 위해 점차 조달을 현대화하고 있습니다.

벤더 관리 소프트웨어 시장은 배포(클라우드, On-Premise), 최종 사용자 업계(소매, 은행, 금융서비스 및 보험(BFSI), 제조, 기타), 조직 규모(대기업, 중소기업), 구성 요소/모듈(벤더 온보딩 및 정보 관리, 벤더 위험 및 컴플라이언스 관리 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 디지털 조달의 조기 성숙, 클라우드 인프라의 충실, 벤더 리스크 워크플로우를 제도화하는 은행 및 헬스케어 규제의 엄격화로 2024년 27.9%의 점유율을 유지했습니다. 특히 금융서비스는 OCC와 CFPB의 지침을 탐색하기 위해 플랫폼을 채택하고 있습니다. 국내 SaaS 벤더의 끊임없는 혁신이 새로 고침주기를 유지하고 이 지역의 리드를 더욱 견고하게 만듭니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 13.2%로 성장 엔진으로 대두합니다. 정부의 지원에 의한 디지털화 프로그램, 급증하는 제조업 수출, 증가하는 사이버 사건에 의해 기업은 제3자 감시의 전문화를 진행시킵니다. 싱가포르 기업에서는 공급망의 사이버 침해가 70% 이상 보고되었으며, 90%가 리스크 관리 예산 인상을 받았습니다. 인도의 중견 중소기업은 수출의 48%를 차지하고 있으며 국제 경쟁을 이기기 위해 최신 공급업체 포털에 의존하고 있습니다. 중국의 강제 노동 컴플라이언스는 하층 공급업체를 추적하는 스크리닝 도구에 대한 수요를 증가시키고 있습니다.

유럽에서는 ESG와 실사의 지시에 따라 자동화된 정보 공개가 필요하며 안정적인 성장을 유지하고 있습니다. 기업은 Scope-3 배출량과 윤리적 조달 증명서를 공급망 전체에서 파악하기 위한 플랫폼을 도입하고 있습니다. 중동 및 아프리카와 남미는 절대액으로는 후진을 숭배하고 있지만, 클라우드 접속의 개선과 공공 부문의 근대화 자금의 유입에 따라 채용이 증가하고 있습니다. 지역 전체에서 벤더 관리 소프트웨어 시장은 전자 조달의 성숙도와 규제의 의무화와 강한 상관관계를 보여주며 미래의 보급을 위한 명확한 로드맵을 설정하고 있습니다.

The vendor management software market size reached USD 10.40 billion in 2025 and is forecast to post a 10.52% CAGR, lifting value to USD 17.15 billion by 2030.

Strong momentum reflects enterprises' need to digitize supplier relationships as supply-chain complexity, material-cost inflation, and regulatory scrutiny converge. Cloud-native deployment, AI-driven analytics, and embedded compliance monitoring now set the baseline for new purchases, while integrated source-to-pay suites are steadily replacing point tools. Platform vendors that streamline onboarding, centralize supplier data, and surface predictive insights win preference because manual oversight cannot scale across hundreds of third parties. Competitive conditions remain moderate; established ERP providers, best-of-breed specialists, and AI-native entrants share the field, creating ample scope for niche differentiation without any single firm dominating.

Automating repetitive supplier tasks reduces procurement overhead and frees teams for strategic sourcing. Wefunder saved 1,350 hours annually and USD 416,000 in lifetime costs after automating contract renewals through CloudEagle's platform. Similar deployments typically cut processing expenses by 20-30% within year one, a result BetterCloud formalizes through its 3x ROI guarantee. As inflation narrows margins, the cost-take-out motive accelerates adoption across industries.

Cloud-native platforms shorten implementation cycles, lower capital outlay, and offer elastic scalability that aligns fees with transaction volume. Choice Hotels International achieved 98.8% accurate cost allocation soon after going live on Finout's SaaS environment. Real-time collaboration, API-based ERP connectivity, and automatic security patching turn cloud into the default option, especially where IT talent is scarce.

Conexis VMS notes that integration, customization, and data migration can double initial budgets, pushing small firms toward phased rollouts.Annual operational spend covers software development, support, and cybersecurity, yet return on investment typically arrives within 18 months as automated workflows unlock savings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud deployment captured 63.2% of the vendor management software market in 2024 and is forecast to expand at a 12.9% CAGR to 2030. Broad acceptance follows lower upfront spend, faster time-to-value, and the ability to push real-time updates that keep security controls current. Finout's success at Choice Hotels illustrates the quick wins enterprises expect. In contrast, on-premises models now appeal mainly to organizations with sensitive sovereignty mandates. Integration workloads and AI compute requirements tip the cost-benefit equation further toward cloud. Hybrid paths persist, letting firms retain critical data in-house while exploiting SaaS collaboration and analytics layers. The vendor management software market continues to shift budgets accordingly, a dynamic reinforced by subscription pricing that scales with transaction throughput.

Second-generation SaaS suites also bundle AI engines that predict supplier risk, recommend cost savings, and automate compliance evidence gathering. These capabilities rely on cloud elasticity, encouraging users to sunset bespoke instances. As upgrades arrive automatically, IT teams redirect effort toward strategic data stewardship instead of routine patching. Consequently, cloud remains the anchor as the vendor management software market advances.

Manufacturing held 37.3% of 2024 revenues, reflecting multi-tier supply chains that demand granular visibility into quality, delivery, and ESG metrics. LeanDNA's rollout at Johnson Controls shows how plant networks benefit from synchronized part, supplier, and inventory data. Inflationary raw-material swings and geopolitical events push producers to diversify sourcing, raising onboarding volumes and reinforcing platform necessity. Retail, while smaller, posts the fastest 11.2% CAGR on the back of omnichannel growth, private-label expansion, and the need to align assortments with consumer demand.

Financial-services uptake accelerates as regulators scrutinize fintech collaborations. Ncontracts found 73% of institutions staffing vendor risk functions with two or fewer employees even while managing 300+ vendors. Healthcare providers prioritize HIPAA-aligned oversight; Vanta's deployment at US Med-Equip reduced audit prep by 50%. Governments gradually modernize procurement to heighten transparency and supplier diversity, aided by solutions such as BidNet Direct.

Vendor Management Software Market is Segmented by Deployment (Cloud, On-Premises), End-User Industry (Retail, BFSI, Manufacturing, and More), Organization Size (Large Enterprises, Smes), Component / Module (Vendor Onboarding and Information Management, Vendor Risk and Compliance Management, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 27.9% share in 2024 owing to early digital procurement maturity, deep cloud infrastructure, and stringent banking and healthcare regulations that institutionalize vendor-risk workflows. Financial services, in particular, adopt platforms to navigate OCC and CFPB guidance. Continuous innovation from domestic SaaS vendors sustains refresh cycles, further anchoring the region's lead.

Asia-Pacific rises as the growth engine with a 13.2% CAGR through 2030. Government-backed digitization programs, burgeoning manufacturing exports, and increasing cyber incidents push organisations to professionalize third-party oversight. Singaporean firms reported over 70% supply-chain cyber breaches, spurring 90% of them to raise risk-management budgets. India's MSMEs contribute 48% of national exports and rely on modern vendor portals to compete globally. China's forced-labor compliance drives demand for screening tools that trace sub-tier suppliers.

Europe maintains steady growth as ESG and due-diligence directives necessitate automated disclosures. Firms deploy platforms to capture Scope-3 emissions and ethical-sourcing attestations across supply chains. Middle East and Africa along with South America trail in absolute value but display rising adoption as cloud connectivity improves and public-sector modernization funds flow. Across regions, the vendor management software market demonstrates strong correlation to e-procurement maturity and regulatory mandates, setting a clear roadmap for future penetration.