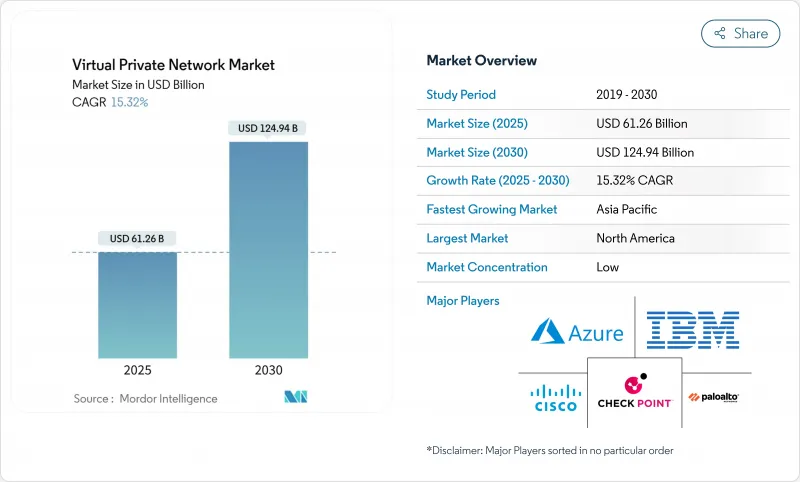

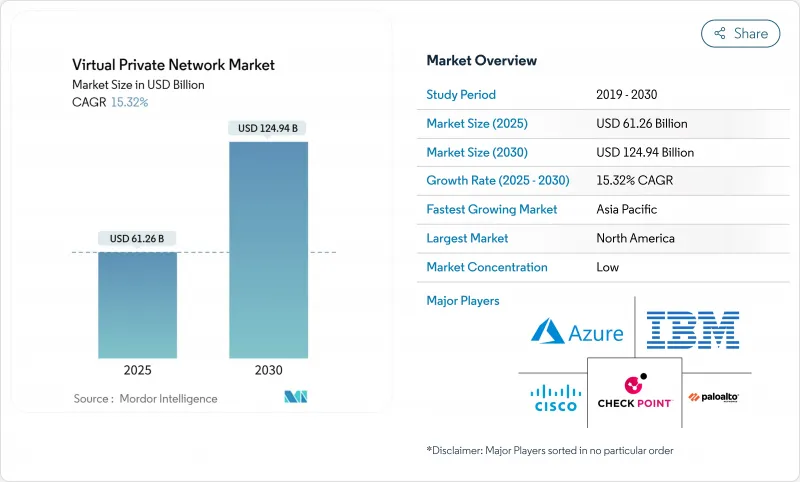

가상사설망(VPN) 시장은 2025년에 612억 6,000만 달러, 2030년에는 1,249억 4,000만 달러에 이르고, CAGR 15.32%를 나타낼 것으로 예측됩니다.

확장의 배경으로는 하이브리드 워크포스의 보안 요구 사항, 랜섬웨어의 지속적인 압력, 네트워킹 및 보안 기능을 통합하는 보안 액세스 서비스 에지(SASE) 플랫폼으로의 마이그레이션이 있습니다. 하드웨어 어플라이언스는 여전히 많은 배포의 핵심이지만 클라우드 서비스는 On-Premise 병목 현상을 제거하고 관리를 단순화하기 위해 가속화되고 있습니다. ZTNA(Zero Trust Network Access) 모델은 레거시 집중 장치를 대체하여 공격 대상 공간을 줄이고 사용자 환경을 개선합니다. 사물인터넷(IoT) 공장, 5G 배포 및 위성 광대역 배포에서 디바이스 실적가 증가함에 따라 암호화 연결 요구 사항이 새로운 사이트와 지역으로 확대되고 있습니다. 경쟁 우위는 AI 위협 감지, 포스트 양자암호화, 통합 정책 관리를 통합한 공급업체로 전환하고 있습니다.

근무 형태의 변화로 VPN 연결은 비즈니스 크리티컬한 상태로 높아지고 있습니다. 뉴욕시 교육부는 100만 명 이상의 사용자와 200만 대의 기기를 제로 트러스트 프레임워크로 전환하여 차단된 위협이 40% 증가하면서 공격이 15% 감소했다고 보고했습니다. 기업은 트래픽을 용도에 직접 라우팅하는 클라우드 네이티브 SASE 플랫폼의 채택이 증가하고 있으며 기존 집중 장치에서 발견되는 대기 시간 및 패치 적용 부담이 해소되었습니다.

산업용 네트워크에서는 현재 세분화된 ID 기반 액세스가 필요합니다. 시스코의 Secure Equipment Access는 광범위한 VPN 터널을 대신하여 운영 기술 리소스를 세밀하게 제로 트러스트 제어합니다. 광동대학교에서는 중국 모바일의 5G VPN이 2만 명의 동시 사용자를 지원하면서 기존 솔루션에 비해 10배의 다운링크 속도를 실현했습니다.

숙련된 엔지니어 수요는 공급을 상회하고 기업은 매니지드 서비스를 이용하게 되어 있습니다. 공급자의 보고에 따르면 직원의 인건비는 총 운영비의 30%에 육박하는 기세이며, 고객은 수작업에 의한 유지 관리를 경감하는 통합 SASE 서비스에 조타하고 있습니다.

하드웨어 어플라이언스는 2024년 가상사설망(VPN) 시장의 43.5%를 차지하며 대규모 원격 액세스 배포를 지원했습니다. 이 부문의 탄력성은 On-Premise 컴플라이언스가 의무화된 영역에서 긴 업데이트 사이클과 연결됩니다. 그러나 컨테이너화된 게이트웨이와 하이퍼스케일 클라우드에 몇 분 안에 배포할 수 있는 가상 방화벽은 소프트웨어의 CAGR 성장률이 15.9%에 달할 전망입니다. 반도체를 둘러싼 공급망의 박박은 AWS나 Azure 상의 pfSense Plus와 같은 클라우드 호스트형 이미지의 채용을 촉진하여 개념 실증을 가속화했습니다. 관리 운영 및 구현 프로젝트에 걸친 서비스 수익은 SASE 마이그레이션과 연계하여 확대되어 현재 구성 요소 지출의 세 번째 기둥을 형성하고 있습니다. 각 조직은 계속해서 현장 성능을 위한 하드웨어와 도달범위를 확장하기 위한 소프트웨어 게이트웨이를 융합시키고 있으며 이는 대체가 아닌 공존을 의미합니다.

호스팅 및 매니지드 서비스는 2024년 가상사설망(VPN) 시장 점유율의 24.7%를 나타냈습니다. 이러한 서비스는 지속적인 업데이트, 위협 인텔리전스 피드 및 24시간 365일 모니터링을 예측 가능한 구독 모델에 통합한 것입니다. 한편, MPLS VPN은 르네상스를 보여주고 있으며, 하이브리드 클라우드와 미션 크리티컬 협업을 위해 확정적인 대기 시간이 필요한 기업이 늘어나면서 CAGR은 16.9%를 나타낼 전망입니다. 클라우드 VPN과 보다 광범위한 SASE 제품군은 IPsec, SD-WAN, 방화벽 애즈어 서비스를 통합 오케스트레이션 하에 수렴하여 정책 난립을 줄입니다. IPsec VPN은 확립된 프로토콜 인증을 준수하는 방어 및 정부 기관에 여전히 필수적이지만, 신흥 WireGuard 솔루션은 간소화된 코드베이스와 회선 속도에 가까운 처리량을 강조합니다.

가상사설망(VPN) 시장은 구성 요소별(하드웨어, 소프트웨어, 서비스), 유형별(호스팅/매니지드, IPsec VPN, MPLS VPN 등), 배포별(클라우드, On-Premise), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, IT 및 통신 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 가상사설망(VPN) 시장 매출의 27.1%를 차지하며, 가장 규모가 큰 지역 공헌국인 것으로 변함이 없었습니다. 제로 트러스트의 조기 시험 도입과 엄격한 정보 공개 규제로 지출의 기세가 유지되고 있습니다. 연방 및 주정부 프로그램은 IPsec 집중 장치에서 ID 중심 SASE 노드로 업그레이드를 가속화하고 하이퍼스케일러의 고밀도 PoP 분산은 분산된 사용자 대기 시간을 낮게 유지합니다.

아시아태평양은 CAGR 16.3%로 가장 빠르게 확대되고 있습니다. 대규모 디지털화 계획과 사이버 보험의 보급이 결합되어 기업은 클라우드 워크로드와 모바일 워크포스의 안전성을 높일 필요가 있습니다. 중국 대학에서 실시한 평가판은 5G 독립형 네트워크에서 모바일 VPN의 성능이 10배 향상됨을 입증했습니다. 인도의 금융 규제 당국은 아웃소싱 처리 센터에 대한 암호화 연결을 요구하고 있으며, 도입이 더욱 가속화되고 있습니다.

유럽에서는 일반 데이터 보호 규칙의 시행이 꾸준히 진행되고 있습니다. 기업은 주권을 확보하기 위해 지역 내에 데이터센터가 있는 공급자를 선호하며, 많은 공급업체는 규정 준수를 위해 VPN에 데이터 유출 방지 기능을 추가합니다. 독일과 프랑스의 정부 프로젝트에서는 새로운 원격 액세스 조달에 포스트 퀀텀에 대한 대응이 명시되어 있습니다. 한편, 중동 및 아프리카에서는 지역으로 광대역을 확장하는 Starlink의 배포가 진행되고 있으며, 신흥 전자상거래 및 전자 정부 트래픽을 보호하기 위해 VPN 서비스가 이용되고 있습니다. 라틴아메리카에서는 브라질 은행과 멕시코 소매업체가 현지 인력 부족을 피하기 위해 관리형 VPN을 도입하고 있습니다.

The virtual private network market generated USD 61.26 billion in 2025 and is forecast to reach USD 124.94 billion by 2030, advancing at a 15.32% CAGR.

Expansion stems from hybrid-workforce security requirements, persistent ransomware pressure, and firm migration toward Secure Access Service Edge (SASE) platforms that merge networking and security functions. Hardware appliances still anchor many deployments, yet cloud-delivered services accelerate because they remove on-premises bottlenecks and simplify administration. Zero-trust network access (ZTNA) models are replacing legacy concentrators, trimming attack surfaces and enhancing user experience. Growing device footprints in Internet of Things (IoT) factories, 5G deployments, and satellite broadband roll-outs extend encrypted connectivity requirements into new sites and geographies. Competitive advantage is shifting to vendors that integrate AI-driven threat detection, post-quantum encryption, and unified policy management.

Shifts in work patterns have elevated VPN connectivity to business-critical status. The New York City Department of Education migrated more than 1 million users and 2 million devices to a zero-trust framework and reported a 15% reduction in attacks alongside a 40% increase in blocked threats. Enterprises increasingly adopt cloud-native SASE platforms that route traffic directly to applications, eliminating the latency and patching burdens found in traditional concentrators.

Industrial networks now demand granular, identity-based access. Cisco's Secure Equipment Access replaces broad VPN tunnels with fine-grained, zero-trust controls for operational technology resources. At Guangdong University, China Mobile's 5G VPN delivered ten-fold downlink speed versus legacy solutions while supporting 20,000 concurrent users.

Demand for skilled engineers exceeds supply, pushing organizations toward managed services. Providers report staffing outlays approaching 30% of total operating expense, steering customers to integrated SASE offerings that reduce manual upkeep.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware appliances accounted for 43.5% of the virtual private network market in 2024, underpinning many large-scale remote access roll-outs. Segment resilience is tied to long refresh cycles in sectors with on-premises compliance mandates. Yet software is growing at a 15.9% CAGR, fueled by containerized gateways and virtual firewalls that deploy in minutes on hyperscale clouds. Supply-chain tightness around semiconductors catalyzed adoption of cloud-hosted images such as pfSense Plus on AWS and Azure, accelerating proofs of concept. Services revenue, spanning managed operations and implementation projects, scales in tandem with SASE transitions and currently forms the third pillar of component spend. Organizations continue to blend hardware for on-site performance with software gateways to extend reach, signalling coexistence rather than replacement.

Hosted and managed offerings secured 24.7% of virtual private network market share in 2024 as enterprises shifted maintenance burdens to specialists. These services integrate continuous updates, threat intelligence feeds, and 24X7 monitoring within predictable subscription models. Meanwhile, MPLS VPN shows a renaissance, pacing at 16.9% CAGR as firms require deterministic latency for hybrid cloud and mission-critical collaboration. Cloud VPN and broader SASE suites converge IPsec, SD-WAN, and firewall-as-a-service under unified orchestration, trimming policy sprawl. IPsec VPN remains essential for defense and government entities adhering to established protocol accreditation, while emerging WireGuard solutions emphasize streamlined code bases and near-line-rate throughput.

Virtual Private Network Market is Segmented by Component (Hardware, Software, Services), Type (Hosted/Managed, Ipsec VPN, MPLS VPN and More), Deployment Mode (Cloud, On-Premise), End-User Industry (BFSI, Healthcare and Life Sciences, IT and Telecom and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America remained the largest regional contributor with 27.1% of virtual private network market revenue in 2024. Spending momentum is sustained by early zero-trust pilots and stringent breach disclosure regulations. Federal and state programs accelerate upgrades from IPsec concentrators to identity-centric SASE nodes, while hyperscalers' dense PoP distribution keeps latency low for dispersed users.

Asia-Pacific delivers the fastest expansion at 16.3% CAGR. Massive digitization programs, combined with rising cyber insurance uptake, push enterprises to secure cloud workloads and mobile workforces. Trials in Chinese universities demonstrate ten-fold performance gains for mobile VPN on 5G stand-alone networks. India's financial regulators now require encrypted connectivity for outsourced processing centers, further catalyzing adoption.

Europe maintains steady progress under General Data Protection Regulation enforcement. Enterprises prefer providers with in-region data centers to ensure sovereignty, and many layer VPN with data-loss prevention for compliance. Government projects in Germany and France specify post-quantum readiness in new remote access procurement. Meanwhile, Middle East and Africa benefit from Starlink roll-outs that extend broadband to rural districts; VPN services ride on top to protect emerging e-commerce and e-government traffic. Latin America gains traction as Brazilian banks and Mexican retailers embrace managed VPN to bypass local talent shortages.