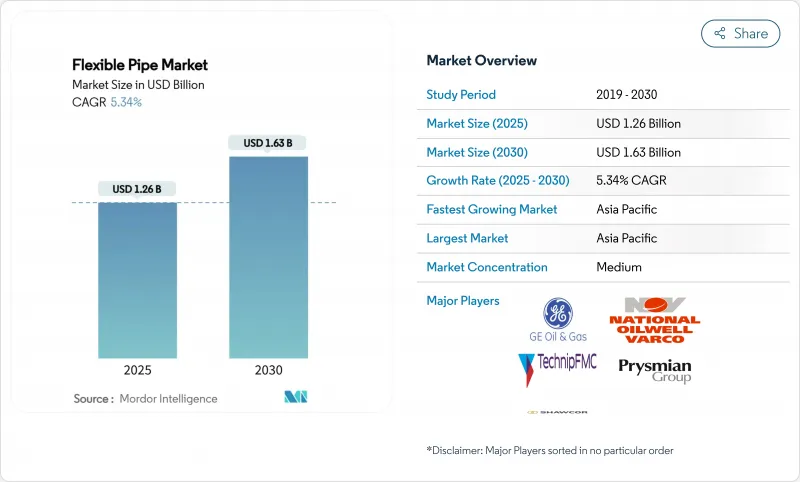

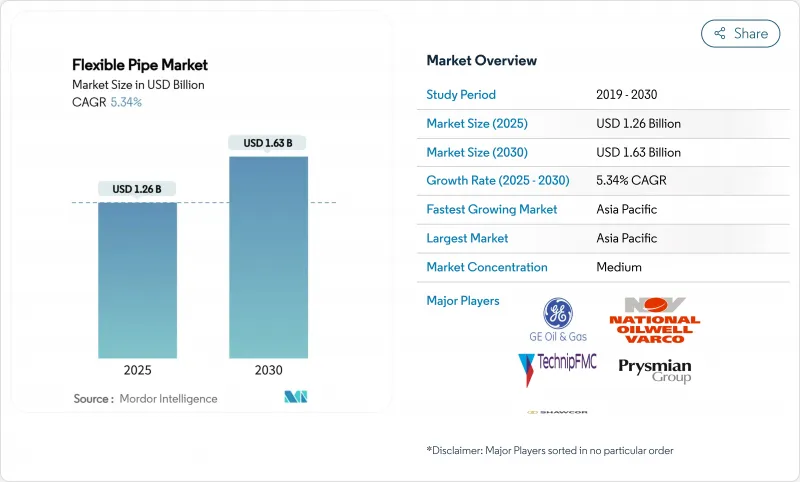

플렉서블 파이프 시장 규모는 2025년에 12억 6,000만 달러, 2030년에는 16억 3,000만 달러에 이를 것으로 예상되며, 예측 기간 동안 CAGR은 5.34%를 나타낼 전망입니다.

이 성장은 심해·초심해 탐사 프로그램, 부식을 완화하는 급속한 재료 혁신, 브라질과 가이아나에서의 선솔트 개발의 확대에 기인하고 있습니다. 업계 선두는 실시간으로 무결성 데이터를 제공하는 광섬유 센서를 내장하여 다운타임을 줄이는 동시에 자산의 수명을 연장하고 있습니다. 아시아태평양은 중국, 인도, 호주의 해외 프로그램에 힘입어 물류 비용을 낮추는 국내 제조에 힘입어 돌출된 지위를 차지하고 있습니다. 소재면에서는 고밀도 폴리에틸렌(HDPE)이 여전히 사업자의 기본 옵션이 되고 있지만, 경량화의 요구가 강해짐에 따라 탄소섬유 및 기타 복합 소재에 의한 솔루션이 견인력을 늘리고 있습니다. Saipem과 Subsea7의 합병 방안과 같은 수직 통합 전략의 가속화는 엔지니어링, 조달, 건설, 설치(EPCI) 능력을 하나의 기업 산하로 결합하여 경쟁 라인을 철회하려고 합니다.

복잡한 해저 지형에서는 경질 강관 시스템이 경제적이지 않기 때문에 운영자는 1,500m 이상의 프로젝트를 허가합니다. Chevron의 Anchor 필드에서 플렉서블 파이프 시장에 새로운 성능 기준을 설정하는 20ksi 해저 하드웨어가 실행되기 시작했습니다. 브라질의 프리솔트층에서는 수심 2,900m에서 CO2에 의한 부식 응력이 발생하기 때문에 입증된 복합재 기술을 가진 공급자가 유리합니다. TechnipFMC의 iEPCI와 같은 시스템 수준의 계약 모델은 일정을 최대 20% 압축하고 통합된 유연한 솔루션에 대한 수요를 강화합니다.

해외 연간 부식 비용은 25억 달러에 이르고, 음극 보호를 피하는 복합재에 의한 리노베이션의 경제성이 높아지고 있습니다. 사이헴의 플라스틱 라이닝 파이프라인 기술은 1,000bar 정격을 유지하면서 비용을 40% 절감합니다. 북해 운영자는 1990년 이전에 거슬러 올라가는 10,000km의 레거시 그리드에 직면해 있습니다. 플렉서블 파이프 시스템은 무거운 리프트 스프레드를 사용하지 않고 기존 통로에 삽입할 수 있어 리노베이션 가동 중지 시간을 줄일 수 있습니다. 베이커 퓨즈의 비금속 제품에 내장된 센서는 노동 집약적인 검사 라운드를 대체하는 무결성 분석을 제공합니다.

배럴당 70-90달러의 가격 변동은 최종 투자 결정을 지연시킵니다. 금리 상승은 장애물의 역치를 끌어올려 허가를 더욱 늘립니다. 성숙한 북해와 멕시코 만의 유전은 특히 취약하며 플렉서블 파이프가 프로젝트의 총 CAPEX의 최대 20%를 차지하고 경제성이 가격에 민감하기 때문입니다.

HDPE의 플렉서블 파이프 시장 규모는 2024년 4억 5,000만 달러에 이르렀으며 35.75%의 매출을 차지했습니다. 사업자는 비용 효율적인 압출 성형, 화학적 불활성, 용접이 없는 피팅 등의 관점에서 HDPE를 높이 평가합니다. 그럼에도 불구하고 탄소섬유 및 첨단 폴리머를 중심으로 한 기타 소재는 CAGR로 8.42%의 연평균 복합 성장률(CAGR)을 나타내고 부체식 생산 시스템이 상면에의 적재를 용이하게 하기 위한 대량 절약을 추구하는 가운데 기존 기업을 능가하고 있습니다. 시드니 대학은 CFRP의 폐기물량이 2030년까지 50만 톤에 달할 것으로 예상하고 있으며, 순환형 경제에 대한 압력이 강해지고 연구개발이 재활용 가능한 수지로 전환될 수 있습니다.

피로 수명과 온도창 강화로 플렉서블 파이프의 점유율 확대를 추진하는 재료 혁신자들. 첨단 PA 및 PVDF 층은 130℃의 서비스를 제공하여 고HTHP 유정으로 유연한 배치를 확대합니다. 열가소성 복합 파이프(TCP)는 탄소섬유 인장 케이싱과 PA12 라이너를 결합하여 부식 제로 및 저마찰 흐름 프로파일을 제공합니다. 심해에서의 활동이 확대됨에 따라 복합재료의 채용이 진행되고 2030년까지는 다른 재료의 기여가 플렉서블 파이프 시장의 1/3로 높아질 것으로 예측됩니다.

언본드 아키텍처는 후프 하중과 축 하중을 분리하는 다층 장갑을 활용하여 2024년 세계 매출의 45.65%를 차지했습니다. 수리가 가능하므로 동적 라이저 용도에 적합합니다. 그러나 금속 카커스를 사용하지 않는 강화 열가소성 파이프는 운영자가 부식이 없는 성능과 데크 하중의 가벼움을 목표로 하므로 CAGR 7.34%를 나타낼 전망입니다. FlexSteel의 스풀 가능한 RTP 솔루션은 애노드 및 코팅 캠페인을 필요로 하지 않으며 브라운필드 타이인에서 OPEX를 줄여줍니다.

플렉서블 파이프 시장에서 구조의 선택은 피로, 압력, 화학 물질에 대한 노출 프로파일에 달려 있습니다. 본드 파이프는 틈새 초고압 흐름 라인의 역할을 하지만 현장에서 수리 옵션이 제한되어 있으며 비용이 높다는 핸디캡이 있습니다. 아라미드와 유리 섬유의 권선에 있어서 기술 혁신은 피로 축적을 추적하는 디지털 트윈과 함께, 한때는 강도의 한계에 의해 진입이 막혀 있던 라이저 업무에 RTP를 침투시킬 수 있게 될 것으로 보입니다.

아시아태평양은 남중국해 심해 블록과 호주 LNG 매복 프로그램을 배경으로 2024년 매출의 38.23%를 유지했습니다. 이 지역의 플렉서블 파이프 시장 규모는 CAGR 8.35%로 상승하고 다른 압도로 예측됩니다. 중국과 인도의 사업자용으로 릴 부설의 리드 타임을 단축하는 동남아시아의 TechnipFMC 공장과 같은 지역 제조 허브 건설에 박차를 가합니다. 일본과 한국에서는 해상풍력발전의 도입이 확대되고 있어 해저전력케이블과 다이나믹 앰빌리컬에 대한 수요가 파급되어 복합재료의 상호비옥화가 더욱 촉진되고 있습니다.

북미는 20ksi의 유연한 점퍼를 필요로 하는 멕시코만의 초심해 제재에 힘입어 2위의 지역이 되고 있습니다. 아나다르코 분지의 개더링 라인과 파미안의 수소 실증 프로젝트가 육상에서의 스풀러블 채용을 뒷받침하고 있습니다. 그러나 아시아태평양의 CAGR은 멕시코 만의 리플레이스 파도가 발견률의 정체로 상쇄되기 때문에 뒤처지고 있습니다.

유럽은 북해의 연명 프로젝트와 노르웨이와 영국의 초기 수소 백본 파일럿 사업으로 균형 잡힌 성장을 보여줍니다. 엄격한 폐로법은 노후화된 강재의 철거를 가속화하고, 타이백 체계에서 유연한 라인 대체를 위한 복고풍의 기회를 제공합니다. 그러나 재활용의 의무화로 인해 공급업체는 고분자 회수를 위한 폐쇄 루프 모델을 제안해야 하며 총 장비 비용이 증가할 수 있습니다.

중동 및 아프리카에서는 카타르 에너지 노스필드 컴프레션 프로그램과 서아프리카 FPSO 캠페인이 부식에 강한 복합재료를 요구하고 있으며 급속한 채용이 진행되고 있습니다. 사이펨이 카타르에서 40억 달러의 EPC를 수주한 것은 하이 스펙 플로우 라인과 광섬유 앰빌리컬에 대한 이 지역의 의욕을 뒷받침합니다. 튀르키예의 Sakarya 2단계에서는 2,200m 정격의 파이프가 158km에 설치될 예정이며, 흑해 유역의 성숙을 보여줍니다. 브라질의 프리솔트와 가이아나의 스탤브로엑 블록을 중심으로 한 중남미는 세계 SURF 백로그의 대부분을 차지하고 리오 근교에 스풀 기지를 병설한다는 제조업체의 결정을 뒷받침하고 있습니다.

The flexible pipe market size stands at USD 1.26 billion in 2025 and is projected to climb to USD 1.63 billion by 2030, representing a 5.34% CAGR through the forecast period.

This growth is traced to deep- and ultra-deepwater exploration programs, rapid material innovation that mitigates corrosion, and expansion in pre-salt developments in Brazil and Guyana. Industry leaders are embedding fiber-optic sensors that deliver real-time integrity data, reducing downtime while lengthening asset life. Asia-Pacific holds the pre-eminent position, propelled by offshore programs in China, India, and Australia and supported by domestic manufacturing that lowers logistics costs. On the materials front, High-Density Polyethylene (HDPE) remains the default choice for operators, yet carbon-fiber and other composite solutions are gaining traction as weight-saving imperatives intensify. Accelerating vertical-integration strategies, such as the proposed Saipem-Subsea7 merger, are redrawing competitive lines by aligning engineering, procurement, construction, and installation (EPCI) capabilities inside one corporate umbrella.

Operators are sanctioning projects beyond 1,500 m as rigid steel systems become uneconomic in complex seabed topography. Chevron's Anchor field inaugurated 20 ksi subsea hardware that sets a new performance bar for the flexible pipe market. Brazil's pre-salt reservoirs impose CO2-driven corrosion stresses at 2,900 m depth, favoring suppliers with proven composite technology. System-level contracting models such as TechnipFMC's iEPCI compress schedules by up to 20%, reinforcing demand for integrated flexible solutions.

Annual offshore corrosion expenses reach USD 2.5 billion, elevating the economics of composite retrofits that sidestep cathodic protection. Saipem's plastic-lined pipeline technology trims costs by 40% while sustaining 1,000 bar ratings. North Sea operators confront a 10,000 km legacy grid dating back pre-1990; flexible pipe systems slot into existing corridors without heavy-lift spreads, cutting retrofit downtime. Embedded sensors inside Baker Hughes' non-metallic products feed integrity analytics that replace labor-intensive inspection rounds.

Price swings in the USD 70-90 per-barrel band delay final investment decisions as boards now demand 18-24 months' price stability before greenlighting offshore projects. Higher interest rates lift hurdle thresholds, further deferring sanctioning. Mature North Sea and Gulf of Mexico fields are particularly vulnerable because flexible pipes constitute up to 20% of total project CAPEX, rendering economics price sensitive.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flexible pipe market size for HDPE reached USD 0.45 billion in 2024, translating into 35.75% revenue dominance. Operators value HDPE for cost-efficient extrusion, chemical inertia, and weld-free joints. Still, Other Materials-chiefly carbon-fiber and advanced polymers-record an 8.42% CAGR, outstripping incumbents as floating production systems chase mass savings to ease topside loading. University of Sydney forecasts CFRP waste streams hitting 500,000 t by 2030, intensifying circular-economy pressures that could redirect R&D toward recyclable resins.

Material innovators push flexible pipe market share gains by enhancing fatigue life and temperature windows. Advanced PA and PVDF layers deliver 130 °C service, expanding flexible deployment into high-HTHP wells. Thermoplastic composite pipes (TCP) marry carbon-fiber tensile casing with a PA12 liner to achieve zero corrosion and low-friction flow profiles. As deepwater activity scales, composite uptake is expected to raise Other Materials' contribution to one-third of the flexible pipe market by 2030.

Unbonded architectures accounted for 45.65% of global revenue in 2024, capitalizing on multilayered armor that decouples hoop and axial loads. Their repairability underpins preference in dynamic riser applications. Yet Reinforced Thermoplastic Pipes, devoid of metallic carcasses, expand 7.34% CAGR as operators target corrosion-free performance and lighter deck loads. FlexSteel's spoolable RTP solutions eliminate anodes and coating campaigns, lowering OPEX in brownfield tie-ins.

Structural choice in the flexible pipe market hinges on fatigue, pressure, and chemical exposure profiles. Bonded pipes serve niche ultra-high-pressure flowlines but are handicapped by limited field repair options and higher cost. Innovations in aramid and glass-fiber winding, coupled with digital twins tracking fatigue accumulation, will allow RTP to penetrate riser duty where strength limits once blocked entry.

The Flexible Pipes Market Report is Segmented by Material Type (High-Density Polyethylene, Polyamide, and More), Pipe Structure Type (Unbonded Flexible Pipe, Bonded Flexible Pipe, Reinforced Thermoplastic Pipe), Functional Application (Flowlines, Risers, Jumpers and Tie-Ins, Export/Loading Hoses), Installation Environment (Offshore, Onshore), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific retained 38.23% of 2024 revenue on the back of South China Sea deepwater blocks and Australian LNG backfill programs. The region's flexible pipe market size is forecast to rise at an 8.35% CAGR, outpacing all others. Government policy favoring local content spurs construction of regional manufacturing hubs, such as TechnipFMC's plant in Southeast Asia that shortens reel-lay lead times for Chinese and Indian operators. Growing offshore wind deployment in Japan and Korea creates spill-over demand for subsea power cables and dynamic umbilicals, further nurturing composite capability cross-fertilization.

North America follows as the second-largest region, underpinned by Gulf of Mexico ultra-deepwater sanctions that require 20 ksi flexible jumpers. Anadarko basin gathering lines and Permian hydrogen demonstration projects drive onshore spoolable adoption. Yet regional CAGR lags Asia-Pacific because the replacement wave in the Gulf is offset by plateauing discovery rates.

Europe shows balanced growth built on North Sea life-extension projects and nascent hydrogen backbone pilots across Norway and the United Kingdom. Strict decommissioning legislation accelerates removal of ageing steel, offering retrofit openings for flexible line substitution in tie-back schemes. Recycling mandates, however, require suppliers to propose closed-loop models for polymer recovery, potentially elevating total installed cost.

Middle East and Africa register rapid adoption as QatarEnergy's North Field Compression Program and West Africa's FPSO campaigns solicit corrosion-immune composites. Saipem's USD 4 billion EPC award in Qatar confirms regional appetite for high-specification flowlines and optic-fiber-infused umbilicals. Turkey's Sakarya Phase 2 calls for 158 km of 2,200 m-rated pipe, signalling Black Sea basin maturation. South America, anchored by Brazil's pre-salt and Guyana's Stabroek block, remains a central pillar, accounting for the bulk of global SURF backlogs and reinforcing manufacturers' decision to co-locate spool-bases near Rio.