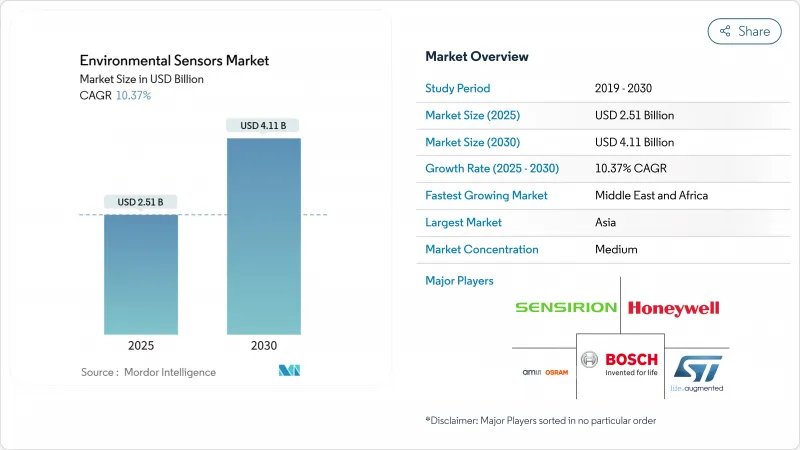

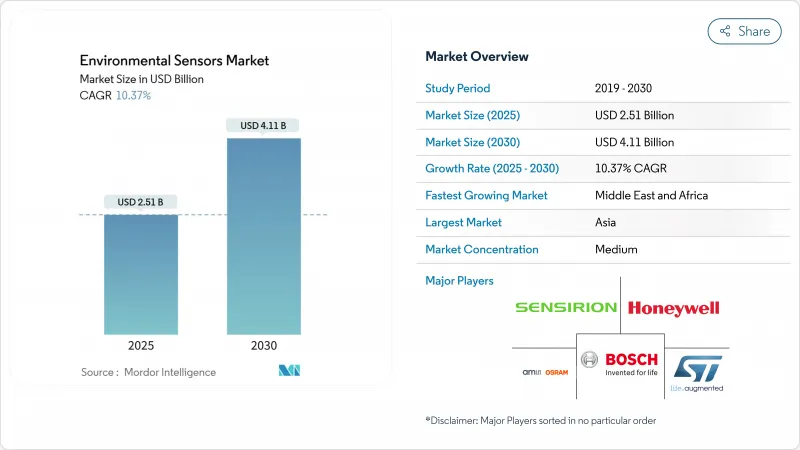

환경센서 시장의 2025년 시장 규모는 25억 1,000만 달러로 평가되었고 CAGR은 10.37%를 나타낼 것으로 예측되며 2030년에는 41억 1,000만 달러에 달할 전망입니다.

이러한 견고한 전망은 강력한 규제 압박, NB-IoT의 신속한 보급 확대, 그리고 스마트 시티, 산업용 IoT, 소비자 웨어러블 기기 분야에서의 확산을 반영합니다. 미국 대형 가속 신고 기업들은 이제 제3자 검증과 함께 스코프 1 및 스코프 2 온실가스 배출량을 공개해야 하므로, 지속적인 모니터링을 위한 센서 전개가 가속화되고 있습니다. 유럽에서는 2025년 3월 발효되는 개정 대기질 지침으로 회원국들이 초미세 입자를 실시간으로 추적해야 하므로, 비용 효율적인 센서 네트워크에 대한 수요가 확대되고 있습니다. 아시아태평양 지역은 고밀도 도시 모니터링을 지원하는 중국의 NB-IoT 인프라 덕분에 환경 센서 시장을 주도하고 있으며, 북미는 산불 감지 네트워크와 엣지 AI 플랫폼 혁신을 주도하고 있습니다. 반도체 대기업, 틈새 MEMS 공급업체, 클라우드 네이티브 IoT 기업들이 탄력적이고 사이버 보안이 강화된 자가 보정 솔루션을 제공하기 위해 경쟁하면서 경쟁 강도는 여전히 높습니다.

중국 통신사들은 현재 9억 개 이상의 NB-IoT 연결을 운영 중이며, 2030년까지 19억 개로 확대할 계획으로 심천 같은 도시들에 블록 단위 대기질 매핑의 기반을 제공하고 있습니다. 이 저전력 광역 표준은 10년 이상의 배터리 수명, 실내 깊숙한 곳까지의 신호 도달, 라이선스 스펙트럼의 안정성을 지원하여 지자체가 케이블 매설 없이도 고층 지역을 포괄적으로 커버할 수 있게 합니다. 태국부터 UAE에 이르는 인접 국가들도 스마트시티 구축 가속화와 ESG 규정 준수를 위해 이 모델을 모방하고 있습니다.

2025년 3월 발효되는 이 지침은 연간 PM2.5 기준을 25 μg/m³에서 10 μg/m³로 하향 조정하고 초미세 입자 추적을 의무화하여, 회원국들이 고가의 기준 관측소에 고밀도 센서 클러스터를 보완하도록 강제합니다. 실시간 공공 데이터 접근 조항은 측정값을 중앙 대시보드로 스트리밍하는 IoT 지원 모듈을 우선시하여, 도시 스모그 환경에서 ±5 μg/m3 정확도를 구현할 수 있는 보정된 MEMS 장치 수요를 촉진합니다.

실외 환경에 배치된 전기화학 센서는 온도 변동, 습도 변화, 간섭 가스 노출로 인해 상당한 교정 드리프트를 경험하며, 허용 가능한 정확도를 유지하기 위해 3개월마다 재교정이 필요할 정도로 빈번한 재교정 주기가 요구됩니다. 이러한 유지보수 부담은 상당한 운영 비용을 발생시키며, 특히 환경적 스트레스 요인이 센서 열화를 가속화하는 가혹한 기후에서는 배치 첫 해에 초기 센서 조달 비용을 초과할 수 있습니다. 연구에 따르면 정기 점검 시 90% 이상의 센서가 교정 사양 범위 내에 머무르며, 이는 현재 유지보수 일정이 지나치게 보수적이지만 규정 미준수 시 발생하는 높은 비용으로 인해 불가피함을 시사합니다.

2024년 환경 센서 시장 규모에서 고정 설치형이 62%의 매출로 우위를 점했으며, 이는 플랜트 운영자의 규제 준수 증명에 대한 지속적인 요구를 반영합니다. 벽면 장착형 또는 덕트 삽입형 프로브는 감사관이 범위 1 검증에 의존하는 환경 관리 시스템에 24시간 데이터를 공급합니다. 휴대용 기기는 규모는 작지만, 응급 대응팀, 광산 기업, 건설 컨소시엄이 변화하는 작업 현장에 신속한 배치를 선호함에 따라 2030년까지 연평균 12.8% 성장률을 기록할 전망입니다. 국토안보부의 산불 시범 사업에서 트레일러 장착형 미세먼지(PM) 측정 노드가 위성 영상보다 30분 빠른 리드 타임을 제공한 것으로 나타나, 이동형 그리드의 사업 타당성이 입증되었습니다.

휴대형 기기는 고정형 배열을 대체하기보다 보완하는 역할을 점차 확대하고 있습니다. 예를 들어 전력사는 규정 준수를 위해 유선 SO2 스택을 설치한 후, 유지보수 중단 시 배터리 구동 VOC 감지기를 이동시켜 사용합니다. 웨어러블 장치는 아직 초기 단계이지만, 소비자 OEM 업체들에게 건강 중심 차별화 경로를 제공하며, 피트니스 대시보드에 꽃가루 농도나 오염 경보를 통합할 수 있습니다. 예측 기간 동안 영구적 기준선과 재배치 가능한 클러스터를 결합한 하이브리드 아키텍처가 환경 센서 시장 전반의 조달 지침을 재정의할 것입니다.

가스 분석기는 공장, 터널, 보일러에서 CO, NOx 및 휘발성 유기 화합물을 감지하는 성숙한 전기화학 셀과 NDIR 광학 기술 덕분에 2024년 환경 센서 시장 점유율의 26%를 차지했습니다. 그러나 미세먼지(PM) 관련 기기는 공중보건 기관들이 PM2.5 노출 기준을 강화함에 따라 13.5%의 연평균 성장률(CAGR)을 기록 중입니다. EU와 캘리포니아의 연간 평균 10μg/m³ 의무 기준 요구에 힘입어 PM 측정 기기 시장 규모는 2030년까지 10억 1,000만 달러에 달할 전망입니다.

온도, 습도, 압력 칩은 여전히 보편적인 관리 매개변수로, 다중 매개변수 모듈 내 주요 가스 또는 PM 기능과 함께 번들로 제공되는 경우가 많습니다. Bosch Sensortec의 BME688은 4개의 물리적 센서와 온보드 AI 추론을 통합하여, 이전에 개별 부품을 구매했던 OEM 업체들의 부품 비용을 20% 절감합니다. 융합으로 인해 기존의 범주 경계가 모호해지면서, 구매는 단일 매개변수 부품보다는 전체적인 “환경 팩”으로 전환되고 있습니다.

아시아태평양 지역은 2024년 매출의 38%를 차지하며 환경 센서 시장을 주도했습니다. 이는 중국과 인도의 스마트시티 메가 프로젝트가 가로등, 버스, 학교에 NB-IoT 노드를 내장한 데 힘입은 결과입니다. 선전(深?) 시만 해도 공개 데이터 포털에 데이터를 제공하는 3만 7,000개 이상의 대기질 측정기를 운영 중입니다. 강력한 전자 부품 공급망으로 부품 비용이 절감되어 지자체가 1만 5,000달러 미만으로 평방킬로미터 단위 그리드를 구축할 수 있습니다. 일본과 한국의 반도체 공장은 첨단 MEMS 생산 능력을 공급하는 반면, 호주 주정부들은 산불 대응을 위한 연기·연기 감지 어레이에 투자하고 있습니다.

북미는 가치 기준으로 2위를 차지합니다. 이곳 환경 센서 시장은 SEC 기후 정보 공개 의무와 캘리포니아, 오리건, 브리티시컬럼비아 전역의 산불 방어 자금 지원으로 성장 동력을 얻고 있습니다. 클라우드-엣지 동맹이 번성합니다. 허니웰과 애널로그 디바이스의 2024년 협약으로 건물 자동화 게이트웨이가 Azure IoT 허브에 직접 연결되어 통합 시간이 절반으로 단축됩니다. CHIPS 및 과학법 하의 연방 보조금은 사이버 복원력 센서 펌웨어 연구개발로 자금을 집중합니다.

유럽은 여전히 핵심적입니다. 강화된 PM2.5 및 초미세먼지 규제로 400개 이상 도시에서 센서 개조가 추진됩니다. 독일은 환경 원격 측정 데이터를 인더스트리 4.0 디지털 트윈과 연계하고, 북유럽 유틸리티 기업들은 지역난방 저장고 내부에 이슬점 배열을 설치해 응결 에너지 손실을 관리합니다. EU 기금이 호라이즌 유럽(Horizon Europe) 하에서 대기질 네트워크 비용의 최대 75%를 환급함에 따라 구현 리드 타임이 단축됩니다.

중동 및 아프리카 지역은 현재 한 자릿수 점유율을 보이지만 14.2%의 연평균 성장률(CAGR)을 기록 중입니다. 걸프 석유 수출국들은 ESG 연계 채권 발행을 위해 연속 누출 감지 시스템을 도입하고 있으며, 남아프리카 광업 부문은 노동 안전 감사를 강화하기 위해 저비용 PM(미세먼지) 그물망 시범 운영을 진행 중입니다. 부족한 교정 실험실이 여전히 장애물이지만, 2026-2027년 가동 예정인 기부금 지원 기준 관측소들이 나이로비, 아크라, 라고스에서 대량 주문을 가능하게 할 것입니다.

The environmental sensors market was valued at USD 2.51 billion in 2025 and is forecast to grow at a 10.37% CAGR, reaching USD 4.11 billion by 2030.

This robust outlook reflects intense regulatory pressure, rapid NB-IoT roll-outs, and widening adoption across smart cities, industrial IoT, and consumer wearables. Large accelerated filers in the United States must now disclose Scope 1 and Scope 2 greenhouse-gas emissions with third-party assurance, prompting accelerated sensor deployment for continuous monitoring. In Europe, the revised Ambient Air Quality Directive effective March 2025 forces member states to track ultrafine particles in real time, expanding demand for cost-effective sensor networks. Asia-Pacific leads the environmental sensors market thanks to Chinese NB-IoT infrastructure that supports high-density urban monitoring, while North America drives innovation in wildfire-detection networks and edge-AI platforms. Competitive intensity remains high as semiconductor majors, niche MEMS suppliers, and cloud-native IoT firms race to deliver resilient, cyber-secure, and self-calibrating solutions.

Chinese operators now run more than 900 million NB-IoT connections, and expansion plans aim for 1.9 billion by 2030, giving cities like Shenzhen the backbone for block-level air-quality mapping. The low-power wide-area standard supports decade-long battery life, deep-indoor penetration, and licensed-spectrum reliability, letting municipalities blanket high-rise districts without trenching cables. Neighboring economies from Thailand to the UAE mirror this model to accelerate smart-city roll-outs and ESG compliance.

The March 2025 directive slices the annual PM2.5 limit from 25 µg/m3 to 10 µg/m3 and mandates ultrafine particle tracking, forcing member states to supplement costly reference stations with dense sensor clusters. Real-time public-data access clauses privilege IoT-ready modules that stream measurements to central dashboards, spurring demand for calibrated MEMS units capable of +-5 µg/m3 accuracy in urban smog.

Electrochemical sensors deployed in outdoor environments experience significant calibration drift due to temperature fluctuations, humidity variations, and exposure to interfering gases, requiring recalibration intervals as frequent as every 3 months to maintain acceptable accuracy. This maintenance burden creates substantial operational costs that can exceed initial sensor procurement costs within the first year of deployment, particularly in harsh climates where environmental stressors accelerate sensor degradation. Research indicates that over 90% of sensors remain within calibration specifications during routine checks, suggesting that current maintenance schedules are overly conservative but necessary due to the high cost of compliance failures.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fixed installations dominated the environmental sensors market size with 62% revenue in 2024, reflecting plant operators' need for uninterrupted proof of regulatory conformity. These wall-mounted or duct-inserted probes feed 24/7 data to environmental management systems that auditors rely on for Scope 1 verification. Portable devices, although smaller in volume, are pacing a 12.8% CAGR through 2030 as first-responders, mining firms, and construction consortia favor rapid deployment along shifting work sites. The Department of Homeland Security's wildfire pilot showed that trailer-mounted PM nodes delivered 30-minute lead times over satellite imagery, validating the business case for mobile grids.

Portables increasingly complement-not replace-fixed arrays. Utilities, for instance, install hard-wired SO2 stacks for compliance, then wheel battery-powered VOC sniffers during maintenance outages. Wearable units remain nascent but give consumer OEMs a route to health-centric differentiation, bundling pollen counts or pollution alerts into fitness dashboards. Over the forecast cycle, hybrid architectures blending permanent baselines with redeployable clusters will redefine procurement guidelines across the environmental sensors market.

Gas analyzers captured 26% of environmental sensors market share in 2024 thanks to mature electrochemical cells and NDIR optics that detect CO, NOx, and volatile organic compounds in factories, tunnels, and boilers. Particulate-matter devices, however, are charting a 13.5% CAGR as public-health agencies tighten PM2.5 exposure thresholds. Environmental sensors market size for PM instruments is forecast to reach USD 1.01 billion by 2030, buoyed by EU and California mandates demanding 10 µg/m3 annual averages.

Temperature, humidity, and pressure chips remain ubiquitous housekeeping parameters, often bundled with primary gas or PM functions inside multi-parameter modules. Bosch Sensortec's BME688 unites four physical sensors plus on-board AI inference, slicing bill-of-materials cost by 20% for OEMs that previously bought discrete components. Convergence blurs historical category lines, steering purchasing toward holistic "environment packs" rather than single-parameter parts.

The Environmental Sensors Market Report is Segmented by Product Type (Fixed, Portable, Wearable), Sensing Type (Gas, Temperature, Humidity, Pressure, Particulate Matter (PM), Multi-Parameter Modules), Connectivity (Wired, Wireless), End-User Industry (Industrial, Medical and Healthcare, Consumer Electronics, Automotive), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific led the environmental sensors market with 38% revenue in 2024, powered by smart-city mega-projects in China and India that embed NB-IoT nodes in streetlights, buses, and schools. Shenzhen alone operates more than 37,000 air-quality boxes feeding open data portals. Strong electronics supply chains lower bill-of-materials, letting municipalities deploy square-kilometer grids for less than USD 15,000. Japanese and South Korean fabs inject advanced MEMS capacity, while Australian states invest in PM-and-smoke arrays for bushfire response.

North America ranks second by value. The environmental sensors market here gains momentum from SEC climate disclosure obligations and wildfire-defense funding across California, Oregon, and British Columbia. Cloud-edge alliances flourish: Honeywell's 2024 pact with Analog Devices links building-automation gateways directly to Azure IoT hubs, cutting integration times by half. Federal grants under the CHIPS and Science Act funnel R&D toward cyber-resilient sensor firmware.

Europe remains pivotal; tightened PM2.5 and ultrafine norms drive sensor retrofits across 400+ cities. Germany ties environmental telemetry to Industry 4.0 digital twins, while Nordic utilities install dew-point arrays inside district-heating vaults to manage condensation energy losses. Implementation lead times shorten because EU funds now reimburse up to 75% of air-quality network costs under Horizon Europe.

The Middle East and Africa presently represent a single-digit share but exhibit 14.2% CAGR. Gulf petro-states adopt continuous-leak detection for ESG-linked bond issuance, and South Africa's mining sector pilots low-cost PM nets to bolster labor-safety audits. Scarce calibration labs remain a hurdle, but donor-funded reference stations scheduled for 2026-2027 will unlock volume orders across Nairobi, Accra, and Lagos.