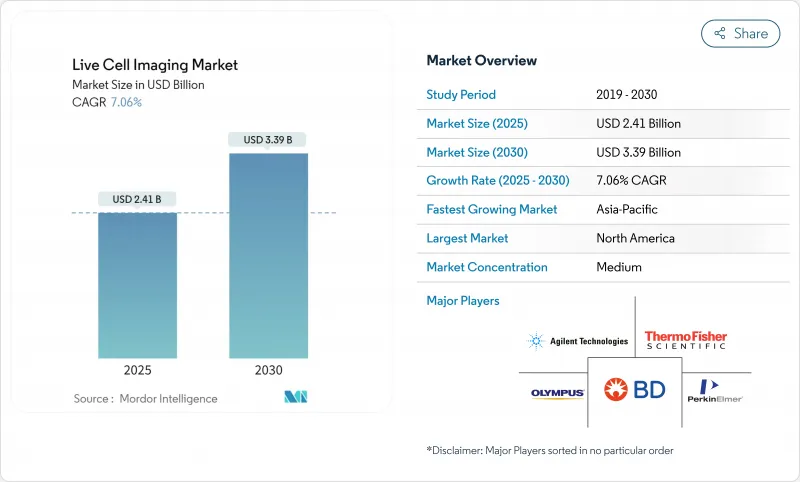

실시간 셀 이미징 시장 규모는 2025년에 24억 달러로 평가되었고 2030년에는 33억 9,000만 달러에 이를 것으로 예측되며, 기간 중 7.06%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

인공지능(AI)과 통합된 하이 컨텐츠 스크리닝(HCS) 플랫폼의 도입, 종양학 및 면역학 연구에 대한 강화된 자금 지원, 표준 인큐베이터 내부에 장착 가능한 소형화된 계측기 등이 종합적으로 이러한 확장을 뒷받침하고 있습니다. 제약사들은 AI 기반 이미징 시스템을 도입해 전임상 연구 기간을 단축하고 있습니다. 이 시스템은 나노스케일 해상도를 유지하면서 이미지 획득 주기를 40% 단축시켜 인간 대상 첫 임상시험까지의 시간을 압축합니다. 동시에 홀로토모그래피와 같은 라벨 프리(label-free) 기법은 형광물질 없이도 오가노이드를 실시간 관찰할 수 있게 하여 광독성 우려를 줄이고 세포 생리학을 수주간 보존합니다. 경쟁 구도는 순수 광학 기술에서 하드웨어, 소프트웨어, 클라우드 기반 분석을 통합한 엔드투엔드 솔루션으로 전환되며, 현미경 가치 사슬 전반에 걸쳐 전략적 협력과 표적 인수합병이 촉진되고 있습니다. 지역별로는 북미가 확립된 자금 조달 경로와 밀집된 제약 산업 기반 덕분에 가장 큰 라이브 셀 이미징 시장 점유율을 유지하고 있으나, 아시아태평양 지역은 현지 정부의 바이오기술 투자 유치 및 규제 조화로 현재 가장 가파른 물량 증가세를 보이고 있습니다.

하이 컨텐츠 스크리닝 시스템은 이제 웰당 수천 개의 표현형 변수를 단 몇 분 만에 분석하는 머신러닝 알고리즘을 통합하여, 과거 며칠이 소요되던 전통적 종점 분석법을 대체합니다. 2025년 1월 출시된 Molecular Devices의 ImageXpress HCS.ai 플랫폼은 복잡한 세포 표현형을 95% 정확도로 분류하면서 분석 시간을 60% 단축합니다. Molecular Devices. 제약 팀들은 이러한 처리량을 활용해 화합물 라이브러리를 신속하게 반복 검증함으로써 초기 발견 단계 예산을 최대 40%까지 절감하고, 자원을 조합 치료법 탐구에 할당할 수 있게 되었습니다. 동일한 자동화 기술은 오가노이드 기반 정밀의학 분야에서도 지원됩니다. 환자 유래 종양 모델을 수십 개의 약물 후보군과 병렬 테스트하여 맞춤형 치료 경로를 도출하는데, 이는 수동 이미징 워크플로우에서는 비용 부담으로 불가능했던 작업입니다.

2024년 입법 예산 배정으로 연구 자금이 확대되며 정교한 이미징 수요가 증가했습니다. 국립암연구소(NCI)는 2024 회계연도에 72억 2,000만 달러(2023년 대비 1억 2,000만 달러 증가)를 배정받았으며, 상당 부분을 이미징 도구 혁신에 할당했습니다. 2025년 미국 국방부는 전립선암 연구 사업에 6억 5천만 달러를 배정하며 광학 진단 및 실시간 세포 모니터링 기술을 다시 한번 부각시켰습니다. 이 자금은 학술 연구 센터의 장비 도입 주기를 가속화하고, 연구비 지원 제안서에서 라이브 셀 이미징을 표준 관행으로 자리매김하며, 코호트 간 면역-종양 상호작용 비교를 위한 표준화된 영상 프로토콜에 의존하는 다기관 임상시험을 촉진합니다.

인공지능(AI)이 내장된 고급 공초점 또는 격자 광시트 현미경은 일반적으로 50만-150만 달러에 달하며, 서비스 계약은 매년 구입 가격의 10-15%를 추가로 부담합니다. 소모품(특수 배지, 마이크로플레이트, 환경 챔버 등)은 바쁜 핵심 시설의 연간 운영 비용을 5만 달러 이상으로 끌어올릴 수 있습니다. 신흥 시장 실험실은 관세와 변동성 높은 환율로 인해 20-30%의 추가 비용을 지불하는 경우가 있어 연구비 예산을 압박하고 장비 업그레이드를 지연시킵니다. 결과적으로 공유 장비 모델이 확산되지만, 시간대 제약으로 인해 과학자들이 실험 설계나 처리량 목표를 타협해야 하는 경우가 발생하여 시장 침투가 제한됩니다.

2024년 장비 부문은 라이브 셀 이미징 시장의 44.10%를 차지했으며, 이는 약 10억 6천만 달러 규모의 시장 규모에 해당합니다. 제약 및 학술 기관 구매자들이 고처리량 자동화를 우선시했기 때문입니다. 요코가와의 CQ3000과 같은 시스템은 공초점, 명시야, 위상차 모드를 단일 섀시에 통합하여 분석 설계자가 시료 이동 없이 다양한 모드 간 전환할 수 있게 합니다. 하드웨어 내장형 클라우드 기반 분석 기술은 이제 테라바이트급 이미지를 거의 실시간으로 처리하여 수동 배치 대기열을 제거합니다. 한편, 라벨 프리 홀로토모그래피에 최적화된 소모품-배지, 미세 패턴 멀티웰 플레이트, 형광체 안정화 완충액 등은 연평균 7.89%의 높은 성장률을 보이며 발전 중입니다. 공급업체들은 장기 조명 하에서도 세포 생리학을 보존하도록 시약을 맞춤화하고 있으며, 이는 pH 및 산소 농도 드리프트로 어려움을 겪었던 일주일 간의 오가노이드 연구에 중요합니다. 소프트웨어는 여전히 가장 작은 수익 비중을 차지하지만, 원시 이미지 스택을 실행 가능한 표현형으로 변환하는 AI 모듈을 활성화한다는 점에서 전략적 영향력을 행사합니다. 알고리즘 업데이트와 연계된 구독형 라이선싱은 하드웨어 포화 이후에도 공급업체가 반복 수익을 확보할 수 있도록 합니다.

두 번째 동향은 소형화입니다. 라이카의 벤치탑형 '마이크로허브(Mica Microhub)'는 기존 광시야 장비보다 65% 작은 공간에 온도·이산화탄소 조절, 환경 적응형 자동 초점, AI 분할 기능을 통합했습니다. 이러한 소형화는 혼잡한 인큐베이터 복도의 공간을 확보하고 생물안전 등급 환경 내 배치도 용이하게 합니다. 장비 밀도가 높아짐에 따라 소모품 수요는 기하급수적으로 증가합니다. 예전에는 현미경 두 대를 운영하던 실험실이 이제는 여섯 대를 가동할 수 있으며, 각 장비마다 전용 챔버 슬라이드와 교정 키트가 필요합니다. 다중 장치를 아우르는 플릿 관리를 조정하는 소프트웨어 스택은 필수 요소가 되어 범주 간 경계를 더욱 모호하게 만듭니다.

세포 생물학은 유전체학, 단백질체학, 대사 연구 전반에 걸친 기초적 역할로 2024년 매출의 28.45%를 유지했습니다. 연구자들은 노화 연구와 관련된 대사 스트레스 모델 하에서 세포골격 재구성, 미토콘드리아 역학, 오토파지 흐름을 관찰하기 위해 라이브 셀 이미징을 활용합니다. 그러나 신약 개발 분야가 8.52%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 2030년까지 라이브 셀 이미징 시장 점유율에서 더 큰 비중을 차지할 전망입니다. 제약 그룹들은 오가노이드 공동 배양과 하이 컨텐츠 분석을 결합하여 AI 스크리닝 파이프라인에 공급되는 풍부한 표현형 데이터셋을 생성합니다. 이 접근법은 독성 위험을 조기에 발견함으로써 전임상 단계의 히트-투-리드(hit-to-lead) 과정에서의 실패율을 줄였습니다.

줄기세포 및 발달 생물학 분야 활용 사례도 증가하고 있으며, 이는 분화 경로의 종단적 이미징을 요구하는 재생의학 파이프라인에 힘입은 바 큽니다. 홀로토모그래피(Holotomography)는 외인성 표지자 없이도 장기 규모의 형태발생 과정을 3D로 시각화할 수 있게 하여 조직 특이적 구조 검증에 핵심적 역할을 합니다. 암 면역학 분야에서는 T세포와 환자 유래 종양 오가노이드를 공동 배양하여 면역 시냅스 형성을 정량화함으로써 면역요법 투여 요법을 안내합니다. 신경 생물학의 최전선은 칼슘 지시약 염료와 초당 100프레임 스캐너를 결합하여 피질 오가노이드의 시냅스 발화 패턴을 밀리초 단위가 아닌 분 단위로 매핑하는 데 활용됩니다.

라이브 셀 이미징 시장 보고서는 업계를 제품별(장치, 소모품, 소프트웨어, 서비스), 용도별(세포 생물학, 발달 생물학, 줄기세포 생물학, 신약 개발, 기타 용도), 지역별(북미, 유럽, 아시아태평양, 중동, 남미)로 분류하고 있습니다. 5년간 시장 예측과 함께 5년간의 과거 데이터를 얻을 수 있습니다.

북미는 2024년 42.23%의 매출로 라이브 셀 이미징 시장을 주도했으며, 5-7년마다 장비 교체를 지원하는 NIH 및 국방부 보조금에 힘입어 그 위상을 유지하고 있습니다. 상위권 대학들은 다기관 암 임상시험 경쟁력 유지를 위해 HCS 장비군을 정기적으로 갱신합니다. FDA의 선제적 입장(2025년 1월 광학 이미징 약물 초안 지침에서 확인됨)은 치료진단 영상에 집중하는 상업적 R&D 스핀아웃을 촉진하는 규제 명확성을 제공합니다. 매사추세츠, 캘리포니아, 온타리오의 대형 제약 캠퍼스는 공급업체 주변에 집적되어 기능 출시를 가속화하는 신속한 피드백 루프를 조성합니다. 그러나 대부분의 선도 기관이 이미 2세대 AI 지원 현미경을 운영 중이어서 성장이 정체되고 있습니다. 향후 판매는 신규 설치보다는 교체 및 소프트웨어 라이선스 확장에 의존할 전망입니다.

아시아태평양 지역은 9.20%의 연평균 성장률(CAGR)로 전 세계에서 가장 빠른 성장을 기록할 것으로 예상됩니다. 일본은 2028년까지 민간 바이오테크 자본을 두 배로 늘리고, 2030년까지 15조 엔 규모의 바이오테크 경제를 목표로 삼고 있습니다. 로드맵에는 세포 치료 상용화를 위한 핵심 기둥으로 이미징 인프라가 명시되어 있습니다. 중국은 신규 CGT(세포·유전자 치료) 제조 단지 내 GMP 등급 이미징 시설을 확장하며, 현지 전자 산업 역량을 활용해 하위 조립품을 생산하고 비용을 절감하고 있습니다. 아세안(ASEAN) 의료기기 규정의 조화로 국경 간 조달 장벽이 낮아져 싱가포르 기반 CRO(계약 연구 기관)가 표준화된 이미징 프로토콜로 지역 임상시험을 지원할 수 있게 되었습니다.

유럽은 독일, 스위스, 영국의 다국적 제약사를 중심으로 견고한 설치 기반을 유지합니다. 호라이즌 유럽(Horizon Europe) 보조금은 범유럽 컨소시엄을 장려하며, 재현성 보장을 위해 모든 컨소시엄이 통합 영상 플랫폼을 도입해야 합니다. 환경 관리 이니셔티브는 수은 램프 대비 전력 소비를 최대 30% 절감하는 LED 조명 시스템을 장려하여 EU 그린딜 목표와 부합합니다. 유럽의약품청(EMA)의 영상 바이오마커 자문은 동반진단 개발을 위한 하드웨어 투자의 정당성을 더욱 강화합니다. 총 GDP 성장률은 둔화되었으나, 연구 우수성 평가에서 영상 역량이 점차 중요해짐에 따라 장비 교체 주기는 건전한 상태를 유지하고 있습니다.

The live cell imaging market size reached USD 2.4 billion in 2025 and is forecast to attain USD 3.39 billion by 2030, advancing at a 7.06% CAGR over the period.

Uptake of high-content screening (HCS) platforms integrated with artificial intelligence (AI), stronger funding for oncology and immunology research, and miniaturized instrumentation that fits inside standard incubators collectively underpin this expansion. Pharmaceutical companies shorten pre-clinical timelines by deploying AI-enabled imaging systems that cut image-acquisition cycles by 40% while retaining nanoscale resolution, thereby compressing the time to first-in-human studies. At the same time, label-free modalities such as holotomography help researchers observe organoids in real time without fluorophores, reducing phototoxicity concerns and preserving cellular physiology for weeks. Competitive activity has shifted from pure optics toward end-to-end solutions that blend hardware, software, and cloud-based analytics, prompting strategic collaborations and targeted acquisitions across the microscopy value chain. Regionally, North America continues to command the largest live cell imaging market share because of established funding avenues and a dense pharmaceutical footprint, yet Asia-Pacific now delivers the steepest volume gains as local governments court biotechnology investment and harmonize regulations.

High-content screening systems now integrate machine-learning algorithms that dissect thousands of phenotypic variables per well in minutes, replacing traditional endpoint assays that once required days. Molecular Devices' ImageXpress HCS.ai platform, launched in January 2025, classifies complex cellular phenotypes with 95% accuracy while shrinking analysis time by 60% Molecular Devices. Pharmaceutical teams leverage such throughput to iterate compound libraries rapidly, trimming early discovery budgets by up to 40% and freeing resources to explore combination therapies. The same automation supports organoid-based precision medicine, where patient-derived tumor models undergo parallel testing against dozens of drug candidates, revealing bespoke treatment paths that would have been cost-prohibitive under manual imaging workflows.

Legislative appropriations widened research coffers in 2024, lifting demand for sophisticated imaging. The National Cancer Institute received USD 7.22 billion for fiscal 2024, USD 120 million more than 2023, earmarking a substantial slice for imaging tool innovation. In 2025 the U.S. Department of Defense allocated USD 650 million for prostate-cancer initiatives, again highlighting optical diagnostics and real-time cellular monitoring. These funds accelerate procurement cycles at academic cores, position live cell imaging as standard practice in grant proposals, and catalyze multi-center trials that rely on harmonized imaging protocols to compare immune-tumor interactions across cohorts.

Advanced confocal or lattice-light-sheet microscopes embedded with AI typically list at USD 500,000-1.5 million, and service contracts add 10-15% of purchase price each year. Consumables-specialized media, microplates, environmental chambers-can drive annual operating outlays above USD 50,000 for busy core facilities. Emerging-market laboratories sometimes pay 20-30% premiums owing to customs duties and volatile exchange rates, stretching grant budgets and delaying upgrades. Consequently, shared-instrument models proliferate, but time-slot constraints can force scientists to compromise experimental design or throughput goals, muting wider market penetration.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Equipment captured 44.10% of the live cell imaging market in 2024, translating to roughly USD 1.06 billion of the live cell imaging market size, as pharmaceutical and academic buyers prioritized high-throughput automation. Systems such as Yokogawa's CQ3000 consolidate confocal, bright-field, and phase-contrast modes in a single chassis, letting assay designers pivot between modalities without sample transfer. Cloud-based analytics embedded inside hardware now parse terabytes of images in near real time, eliminating manual batching queues. Meanwhile, consumables-media optimized for label-free holotomography, micro-patterned multi-well plates, and fluorophore-stabilization buffers-advance at a brisk 7.89% CAGR. Vendors tailor reagents to preserve cellular physiology under long-term illumination, important for week-long organoid studies that previously suffered drift in pH and oxygen tension. Software remains the smallest monetary slice but wields strategic clout because it unlocks AI modules that convert raw image stacks into actionable phenotypes. Subscription licensing tied to algorithm updates ensures vendors book recurring revenue even after hardware saturation.

A second dynamic involves miniaturization. Leica's bench-top Mica Microhub combines temperature and CO2 regulation, environmental-adaptive auto-focus, and AI segmentation inside a footprint 65% smaller than legacy wide-field rigs. Such compactness frees space in crowded incubator corridors and facilitates deployment in biosafety-level environments. As equipment density rises, demand for consumables scales multiplicatively-the same lab that once ran two microscopes may now operate six, each requiring dedicated chamber slides and calibration kits. Software stacks that orchestrate fleet management across multiple devices become mandatory, further blending categories.

Cell biology retained 28.45% of 2024 revenue given its foundational role across genomics, proteomics, and metabolic studies. Investigators exploit live cell imaging to observe cytoskeletal reorganization, mitochondrial dynamics, and autophagy flux under metabolic stress models pertinent to aging research. Drug discovery, however, posts the strongest 8.52% CAGR and is on course to command a larger slice of live cell imaging market share by 2030. Pharmaceutical groups marry organoid co-cultures with high-content analytics, generating phenotype-rich datasets that feed AI screening funnels. The approach has trimmed attrition in pre-clinical hit-to-lead phases by surfacing toxicity liabilities earlier.

Stem-cell and developmental-biology use cases also ascend, buoyed by regenerative-medicine pipelines that demand longitudinal imaging of differentiation pathways. Holotomography enables researchers to visualize organ-scale morphogenesis in 3D without exogenous labels, crucial for verifying tissue-specific architecture. In cancer-immunology, researchers co-culture T-cells with patient-derived tumor organoids to quantify immune synapse formation, guiding immunotherapy dosing regimens. The frontier of neurobiology benefits from calcium-indicator dyes paired with 100-frame-per-second scanners that map synaptic firing patterns in cortical organoids over minutes instead of milliseconds.

The Live Cell Imaging Market Report Segments the Industry Into by Product (Equipment, Consumables, Software and Services), by Application (Cell Biology, Developmental Biology, Stem Cell Biology, Drug Discovery, Other Applications) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Get Five Years of Historical Data Alongside Five-Year Market Forecasts.

North America led the live cell imaging market with 42.23% revenue in 2024, sustained by NIH and Department of Defense grants that subsidize equipment turnover every 5-7 years. Top-tier universities routinely refresh HCS fleets to maintain competitiveness for multi-center oncology trials. The FDA's proactive stance-evident in January 2025 draft guidance on optical-imaging drugs-provides regulatory clarity that spurs commercial R&D spin-outs focused on theranostic imaging. Large pharmaceutical campuses in Massachusetts, California, and Ontario cluster around suppliers, fostering rapid feedback loops that accelerate feature roll-outs. Yet growth is plateauing as most category-leading institutions already operate second-generation AI-ready microscopes; future sales lean on replacement and software-license expansions rather than new-site installs.

Asia-Pacific is projected to record a 9.20% CAGR, the fastest globally. Japan aims to double private biotech capital by 2028, targeting a 15-trillion-yen biotechnology economy by 2030; the roadmap specifically lists imaging infrastructure as a pillar toward cell-therapy commercialization. China expands GMP-grade imaging suites inside new CGT manufacturing parks, using local electronics capability to fabricate sub-assemblies and moderate costs. Harmonized ASEAN medical-device regulations lower barriers for cross-border procurement, letting Singapore-based CROs serve regional trials with standardized imaging protocols.

Europe maintains a robust installed base anchored by pharmaceutical multinationals in Germany, Switzerland, and the United Kingdom. Horizon-Europe grants encourage pan-continental consortia, all of which must deploy harmonized imaging platforms to ensure reproducibility. Environmental stewardship initiatives incentivize LED-illuminated systems that reduce power consumption by up to 30% versus mercury bulbs, aligning with EU Green Deal targets. European Medicines Agency consultations on imaging biomarkers further legitimize hardware investments geared toward companion-diagnostic development. Despite slower aggregate GDP growth, refurbishment cycles remain healthy because research excellence rankings increasingly weigh imaging capacity.