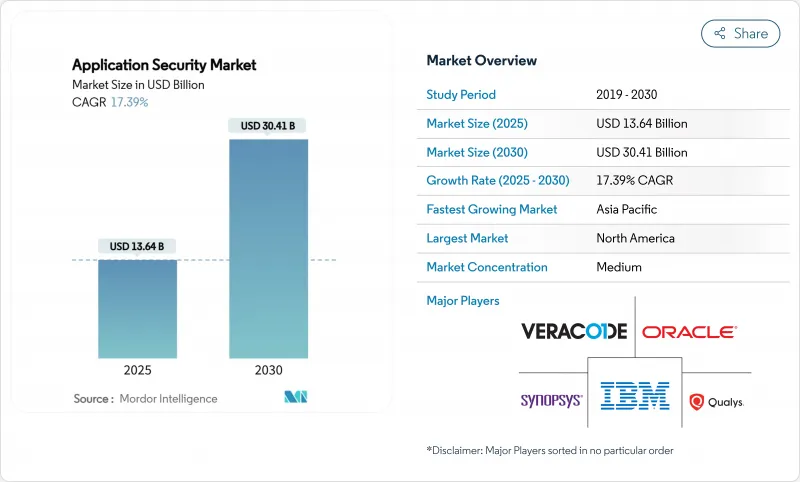

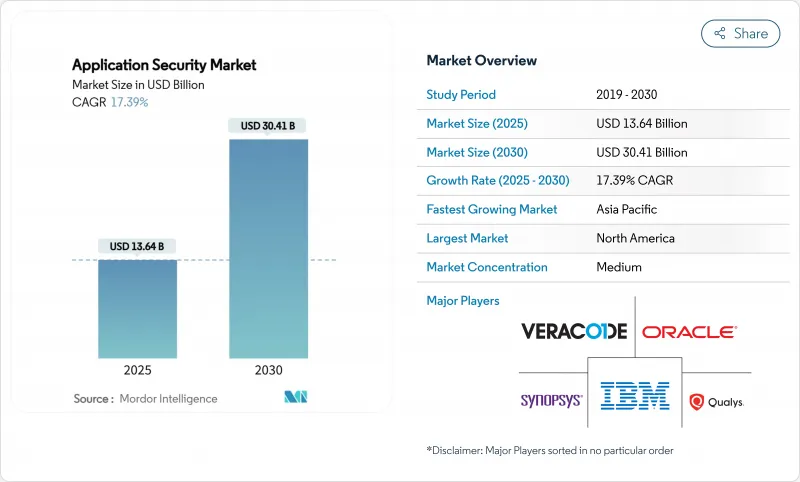

애플리케이션 보안 시장의 2025년 시장 규모는 136억 4,000만 달러로 추정되고, 2030년에는 304억 1,000만 달러에 이를 전망이며, CAGR 17.39%로 성장할 것으로 예측됩니다.

클라우드로의 전환, API 중심의 소프트웨어 설계, 규제 확대로 모든 주요 산업에서 도입이 가속화되고 있습니다. API 트래픽의 급증, AI에서 생성된 코드의 보급, 개발 라이프사이클의 초기 단계에서의 테스트 강화를 조직에 강한 인시던트 공개 규칙의 강화로 성장이 강화되고 있습니다. 대기업은 계속 지출 전체를 지원하고 있지만, 중소기업(SME)을 위한 매니지드 플랫폼은 벤더에게 새로운 대응 가능한 기반을 개척하고 있습니다. 기술 컨버전스는 경쟁력을 재구성하고 플랫폼 제공업체는 정적, 동적, 런타임 보호를 통합하여 툴 난립을 억제하고 개발자의 생산성을 향상시킵니다.

아시아태평양의 웹 애플리케이션 공격은 2024년에는 73% 증가한 510억 이벤트로 급증하였습니다. 연간 1,000개가 넘는 API를 개발하는 소매업체는 경계 관리를 피하는 공격 대상의 확대에 직면하고 있습니다. 공급망에 대한 침입은 2021-2023년 431% 증가하여 직접적인 코드 주입보다 종속성 악용으로 축발이 옮겨가고 있음을 보여줍니다. 기업은 정적 서명이 아닌 비정상적인 트래픽 패턴을 처리하기 위해 런타임 애플리케이션 자체 보호를 행동 분석과 통합합니다. 제조업에서는 API 인시던트 발생률이 79%에 달했고 적의 움직임이 대부분의 운영 기술 보안 프로그램보다 빠르다는 것이 확인되었습니다.

DevSecOps의 보급률은 2020년의 27%에서 2024년에는 36%로 상승하였으며, 팀이 테스트를 지속적인 통합 파이프라인에 조기에 통합하게 되었습니다. ArmorCode와 같은 수십억 개의 발견을 처리하는 플랫폼은 머신러닝을 적용하여 취약성을 상관시키고 규모에 따라 복구 우선 순위를 결정합니다. 이러한 진전에도 불구하고, 기업의 78%가 '시프트 레프트 피로'를 보고하고 있으며, 이는 경고로 개발자를 압도하는 중복 도구로 악화되고 있습니다. 가장 효과적인 프로그램은 통합 개발 환경 내에서 보안 작업을 간소화하고 정책을 버전 관리된 아티팩트로 취급하며 커밋 시 자동으로 적용합니다. 이 모델은 코드 편집기 내에서 수정을 제안하는 AI 어시스턴트에 의해 확장되어 개발 포털과 보안 포털 간의 컨텍스트 전환 시간을 단축합니다.

SaaS의 인플레이션은 2024년 11.3%에 달했으며, 일부 공급업체는 25%나 가격을 인상했습니다. 중소기업의 42%는 아직 구조화된 사고 대응 계획을 수립하지 않았으며 예산 제약이 엔터프라이즈급 관리를 제한하고 있음이 밝혀졌습니다. 또한 스캐너, 에이전트, 정책엔진이 중복 도입되어 통합에 필요한 기술이 부족해 89%의 기업이 인력은 제자리걸음임에도 불구하고 추가 인력 확보가 필요할 것으로 예측했습니다. Contrast One(TM)과 같은 관리 플랫폼은 현재 전문가의 서비스와 도구를 번들로 관리 오버헤드를 줄이고 있습니다. 또한 소비 기반 가격 설정 모델도 등장하여 중소기업에서도 실제 테스트 빈도에 맞추어 지출을 조정할 수 있게 되었습니다.

2024년 점유율은 솔루션이 78.5%를 차지하고 통합 제품군에 대한 기업의 선호도를 반영합니다. 시장 리더는 SAST, DAST, IAST, RASP를 하나의 라이선스로 통합하여 도구 난립을 억제합니다. 통합된 대시보드는 컨텍스트 전환을 줄이고 의사 결정을 가속화합니다. 서비스 부문은 규모가 작은 반면, CAGR 17.9%로, 보다 광범위한 애플리케이션 보안 시장을 능가하고 있으며, 앞으로도 스킬 갭의 혜택을 계속 받을 것으로 보입니다.

전임 전문가를 고용할 여유가 없는 중소기업에서는 관리 보안 수요가 가속화되고 있습니다. 공급자는 예측 가능한 구독 가격과 성과 기반 서비스 수준 계약을 활용하여 비용 의식이 높은 구매자를 유치합니다. 대기업의 경우 정책 매핑, 파이프라인 통합 및 런타임 방어를 검증하는 레드 팀 시뮬레이션에 중점을 둔 전문 서비스를 제공합니다. 공급업체는 또한 고객이 영구 시트가 아닌 스캐닝 크레딧을 구매할 수 있는 소비 계층적 서비스를 도입하여 취약성 관리 예산 구성에 투명성을 제공합니다.

클라우드 전개는 2024년 애플리케이션 보안 시장의 65.9%를 차지하였고, CAGR 19.3%로 성장이 예측됩니다. DORA와 관련된 규정은 4시간 이내에 인시던트를 보고하는 것으로 규정되어 있지만, 중앙집중식 로깅과 확장 가능한 분석이 없으면 대응하기가 어렵습니다. 클라우드 네이티브 솔루션은 정책 업데이트를 신속하게 전개하고 컨테이너 오케스트레이션 시스템과 쉽게 통합할 수 있습니다.

온프레미스 솔루션은 데이터 레지던시를 필요로 하는 방위 및 공공 기관의 워크로드에서 여전히 널리 사용되고 있습니다. 금융기업이 민감한 워크로드를 프라이빗 인프라에 배치하고 개발 시 클라우드 스캐너를 사용하는 하이브리드 패턴이 증가하고 있습니다. 클라우드 벤더는 오랫동안 주권에 대한 우려를 해결하기 위해 하드웨어에 뒷받침되는 인증과 기밀 컴퓨팅에 투자하고 있습니다. 현재 경쟁의 중심은 인프라와 애플리케이션 두 계층에 걸친 구성 오류를 매핑하는 클라우드 보안 태세 관리 기능과의 무결성입니다.

애플리케이션 보안 시장은 용도 유형별(웹 애플리케이션 보안, 기타), 컴포넌트별(솔루션, 서비스), 전개 모드별(클라우드, 온프레미스), 조직 규모별(중소기업, 대기업), 보안 테스트 유형별(SAST, DAST 등), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료, 소매, 전자상거래 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 매출 점유율 28.9%로 애플리케이션 보안 시장을 선도했으며, 강한 규제 압력과 연간 2,000만 달러를 넘는 포춘 500사의 평균 보안 예산에 지지되고 있습니다. 엔터프라이즈는 원격 근무과 하이브리드 작업을 지원하기 위해 신원, 네트워크 및 애플리케이션 제어를 통합하는 제로 트러스트 아키텍처를 통합합니다. 벤더가 AI를 활용한 취약성 상관 워크로드를 시험적으로 도입하여 평균 복구 시간 단축을 실현하는 기술 허브가 전진하고 있습니다.

아시아태평양은 2030년까지 예측 CAGR 17.5%로 최고 속도를 기록할 전망이며, 디지털 정부 프로그램, 핀텍 도입 증가, 2024년에 510억 이벤트에 이르는 웹 애플리케이션 공격의 73% 급증이 그 요인이 되고 있습니다. 싱가포르와 인도 정부는 중요한 인프라의 최소 관리 기준을 보여주는 사이버 전략을 발표했습니다. 이 지역의 제조업은 디지털 성숙도가 낮음에도 불구하고 API 인시던트의 비율이 가장 높으며 공급업체는 위협 인텔리전스와 언어별 복구 리소스를 현지화해야 합니다.

유럽의 기세는 DORA, 사이버 레지리언스법, GDPR(EU 개인정보보호규정) 등 종합적인 법규제에 달려 있습니다. 금융기관은 2025년 1월 이후 ICT 위험 관리 프레임워크를 도입하여 4시간 이내에 정보 유출 통지를 해야 합니다. 기업은 IT 예산의 약 9%를 정보 보안에 할당하고 있지만 89%는 이러한 의무를 해결하기 위해 고용 증가를 예상하고 있습니다. 데이터 주권 조항은 기밀성이 높은 워크로드의 온프레미스 처리를 장려하는 반면, 중요도가 낮은 데이터에 대해서는 클라우드 기반 애널리틱스가 인정되고 있기 때문에 하이브리드 전개의 선호가 근본적입니다.

The application security market was valued at USD 13.64 billion in 2025 and is expected to reach USD 30.41 billion by 2030, advancing at a 17.39% CAGR.

Cloud migration, API-centric software design and expanding regulatory mandates are accelerating adoption across every major industry vertical. Growth is reinforced by a sharp increase in API traffic, the widespread use of AI-generated code and heightened incident disclosure rules that force organizations to strengthen testing earlier in the development life cycle. Large enterprises continue to anchor overall spending, yet managed platforms aimed at small and medium enterprises (SMEs) are opening a sizeable new addressable base for vendors. Technology convergence is reshaping competitive dynamics, with platform providers integrating static, dynamic and runtime protection to curb tool sprawl and improve developer productivity.

Web application attacks in the Asia-Pacific region surged 73% to 51 billion events in 2024, underscoring how attackers now exploit APIs at scale. Retailers developing more than 1,000 APIs yearly confront an enlarged attack surface that bypasses perimeter controls. Supply-chain breaches climbed 431% between 2021 and 2023, demonstrating a pivot toward dependency exploitation rather than direct code injection. Enterprises are integrating runtime application self-protection with behavioral analytics to act on anomalous traffic patterns rather than static signatures. Manufacturing recorded a 79% API incident rate, confirming that adversaries move faster than most operational technology security programs.

DevSecOps penetration rose from 27% in 2020 to 36% in 2024 as teams embed testing earlier in continuous integration pipelines. Platforms processing billions of findings, such as ArmorCode, apply machine learning to correlate vulnerabilities and prioritize remediation at scale. Despite progress, 78% of enterprises report "shift-left fatigue," aggravated by redundant tools that overwhelm developers with alerts. The most effective programs streamline security tasks inside integrated development environments, treating policies as version-controlled artifacts automatically enforced at commit. This model is extending through AI assistants that suggest fixes inside code editors, thereby reducing context-switch time between development and security portals.

Software-as-a-service inflation reached 11.3% in 2024, with some vendors lifting prices by 25%.Forty-two percent of SMEs still lack a structured incident response plan, revealing budget constraints that limit enterprise-grade controls. Organizations deploy overlapping scanners, agents and policy engines that demand scarce integration skills, leading 89% of firms to foresee additional staffing needs despite flat headcounts. Managed platforms such as Contrast One(TM) now bundle expert services with tooling to cut administrative overhead. Consumption-based pricing models are also emerging, enabling smaller businesses to align spending with actual test frequency.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions retained a 78.5% share in 2024, reflecting enterprise preference for integrated suites. Market leaders combine SAST, DAST, IAST and RASP under one license to limit tool sprawl. Consolidated dashboards reduce context switching and speed decision-making, fixing a common pain point cited by development teams. The service segment, though smaller, outran the broader application security market with a 17.9% CAGR and will continue to benefit from skills gaps.

Demand for managed security accelerates within SMEs that cannot afford full-time specialists. Providers use predictable subscription pricing and outcome-based service-level agreements to attract cost-conscious buyers. For large enterprises, professional services focus on policy mapping, pipeline integration and red-team simulations that validate runtime defenses. Vendors also introduce consumption-tiered offerings, letting customers buy scanning credits rather than perpetual seats, bringing transparency to budgeting for vulnerability management.

Cloud deployment controlled 65.9% of the application security market in 2024 and is forecast to advance at a 19.3% CAGR. DORA and related regulations specify four-hour incident reporting, a timeline difficult to meet without centralized logging and scalable analytics. Cloud-native solutions enable rapid rollout of policy updates and integrate easily with container orchestration systems.

On-premises solutions remain prevalent in defense and public-sector workloads that require data residency. Hybrid patterns are growing as financial firms keep sensitive workloads on private infrastructure while using cloud scanners during development. Cloud vendors invest in hardware-backed attestation and confidential computing to address lingering sovereignty concerns. Competition now centers on alignment with cloud security posture management functions that map misconfigurations across both infrastructure and application layers.

Application Security Market is Segmented by Application Type (Web Application Security, and More), Component (Solutions, Services), Deployment Mode (Cloud, On-Premises), Organization Size (SMEs, Large Enterprises), Security Testing Type (SAST, DAST, and More), End-User Industry (BFSI, Healthcare, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led the application security market with a 28.9% revenue share in 2024, underpinned by strong regulatory pressure and average Fortune 500 security budgets exceeding USD 20 million annually. Enterprises integrate zero-trust architectures that merge identity, network and application controls to support remote and hybrid work. Advancements originate in technology hubs where vendors pilot AI-driven vulnerability correlation workloads, delivering faster mean time to remediation.

Asia-Pacific records the fastest projected 17.5% CAGR through 2030, fueled by digital government programs, rising fintech adoption and a 73% spike in web application attacks that hit 51 billion events in 2024. Governments in Singapore and India release refreshed cyber strategies that map minimum control baselines for critical infrastructure. The region's manufacturing sector, despite lower digital maturity, faces the highest share of API incidents, pushing vendors to localize threat intelligence and language-specific remediation resources.

Europe's momentum hinges on comprehensive statutes such as DORA, the Cyber Resilience Act and GDPR. Financial entities must implement ICT risk management frameworks and deliver four-hour breach notifications from January 2025. Organizations allocate around 9% of IT budgets to information security, yet 89% still anticipate hiring increases to meet these mandates. Hybrid deployment preferences persist because data-sovereignty clauses encourage on-premise processing of sensitive workloads while permitting cloud-based analytics for less critical data.