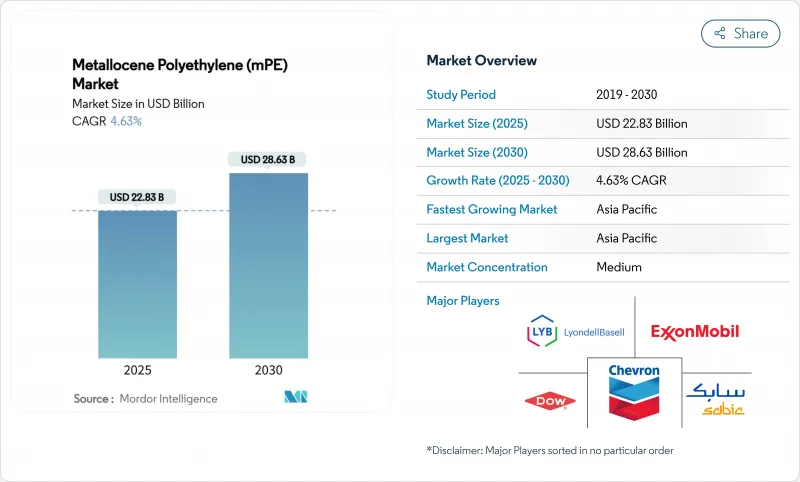

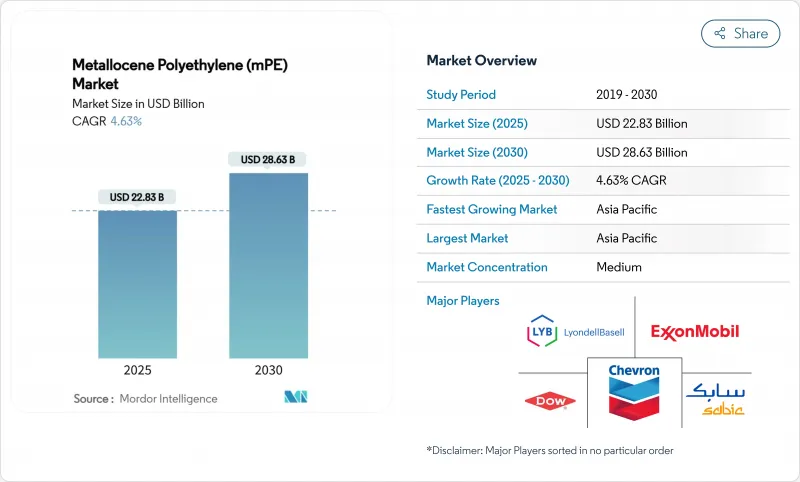

메탈로센 폴리에틸렌 시장 규모는 2025년에 228억 3,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 4.63%로 성장할 전망이며, 2030년에는 286억 3,000만 달러에 달할 것으로 예측됩니다.

고 클라리티 다운 게이지드 필름에 대한 왕성한 수요, 솔라 패널 봉지제 라인의 스케일 업, 농업의 근대화가 이 성장 노선을 지지하고 있습니다. 생산자는 좁은 분자량 분포를 제공하는 단일 사이트 촉매 기술의 혜택을 누리며 낮은 게이지에서 일관된 기계적 강도와 우수한 광학 특성을 제공합니다. 중국의 에틸렌 생산 능력 강화, 인도의 전자상거래 붐, 중동의 생산 능력 투자가 상반되어 업스트림 공급 안정성을 강화하는 한편, 순환형 플라스틱으로의 시프트가 진행되고 있으며, 고도의 재활용과 바이오 원료에 전략적 초점이 맞추어지고 있습니다. 따라서 메탈로센 폴리에틸렌 시장은 성능 향상과 지속가능성 목표를 양립시켜 차세대 연포장 솔루션의 핵심적인 존재로 자리매김하고 있습니다.

컨버터는 기계적 무결성을 유지하면서 더 얇은 필름으로의 전환을 계속하고 있으며, 단일 사이트 촉매는 다트 충격 강도와 함께 투명성을 제공하는 균일한 공단량체 분포를 촉진합니다. 일반적으로 15-20%의 게이지 감소는 재료 사용량과 탄소 강도를 낮추고 브랜드 소유자의 지속가능성 맹세를 직접 지원합니다. 분자량 분포가 좁기 때문에 블로우 필름 제조 라인에서의 엣지 트림 폐기물도 삭감할 수 있어 제봉 처리량도 향상하므로, 컨버터의 영업 이익률도 향상합니다. 엑시드 XP와 같은 프리미엄 메탈로센 등급은 콜드체인 물류에 적합한 강인성을 일년 내내 제공하는 반면, 옴니채널 소매의 급속한 증가로 인해 더 강하고 가벼운 필름이 필요한 소포 취급의 스트레스가 높아지고 있습니다.

소매업체가 선반 효율 및 물류 비용 절감을 우선시함에 따라 식품, 홈 케어, 퍼스널케어의 각 분야에서 플렉서블 포맷이 경질 용기를 대체합니다. 메탈로센 폴리에틸렌은 보다 강력한 핫 택과 넓은 밀봉 창을 제공하여 고속 수직 폼 필 밀봉 장치에서 누출을 감소시킵니다. 접촉 용도에 있어서 폴리염화비닐의 거래 금지에 의해 재활용 가능한 폴리에틸렌 혼합 소재로의 이행이 가속되고 있으며, 염화비닐을 함유하지 않고 폴리염화비닐의 투명성을 재현한 PreservaWrap 라인이 그 일례입니다. 의료기기 제조업체는 또한 생체적합성을 요구하여 PVC에서 메탈로센 폴리에틸렌으로 축발을 옮기고 있으며, 헬스케어 수요를 강화하고 부문을 확대하고 있습니다.

원유 가격 및 천연 가스 가격의 변동은 에틸렌 가격의 변동에 연쇄하여 15-20%의 촉매 프리미엄을 지불하는 특수 수지 제조업체의 마진을 압박합니다. 전자 크래커와 탄소 포집 장치의 개수는 자본 비용을 상승시켜 원료 상승 시의 압력이 됩니다. 수직 통합 중동 생산자가 비용 리더십을 유지하는 반면 수입에 의존하는 아시아 컨버터는 변동이 심해집니다. 바이오에틸렌의 루트는 부분적으로 변동성을 헤지하는 것, 인프라 정비를 병행해 실시할 필요가 있기 때문에 선행 투자 자금이 필요합니다.

2024년 메탈로센 폴리에틸렌 시장 점유율은 mLLDPE가 59.01%를 차지했습니다. 이 부문은 뛰어난 내천자성 및 다트 충격 강도 덕분에 패키징에 실패하지 않고 15-20%의 다운가우징을 가능하게 하여 리더십을 유지하고 있습니다. 2024년에는 많은 음료 파우치 제조업체들이 mLLDPE 구조로 전면 전환합니다. 파이프 코팅을 사용하면 mLLDPE의 유연성이 코일 온 릴에서 처리할 때 균열의 위험을 줄입니다.

mHDPE는 2030년까지 연평균 복합 성장률(CAGR) 6.65%로 성장할 것으로 예측되며, 개발도상국의 압력 파이프 및 화학 드럼 수요가 이를 뒷받침합니다. 응력 균열에 강한 등급은 연료 탱크의 블로우 성형이나 언더푸드 부품에도 사용됩니다. 틈새 mLDPE 라인은 용융 강도가 중요한 특수 캐스트 필름 용도에 사용됩니다. UHMWPE의 발전으로 인공 관절 및 보호 장비 시장도 확대되고 메탈로센 폴리에틸렌 시장의 가치 풀이 강화되고 있습니다.

2024년 지르코노센 촉매의 점유율은 62.75% 지르코노센 촉매는 기상 반응기 및 용액 반응기에서의 조작성이 입증되었습니다. 실적이 풍부하기 때문에 식품 접촉 인증에 필수적인 인증 시간이 단축됩니다.

CAGR 5.25%로 확대되는 하프노센 시스템은 기상의 처리량 향상을 가능하게 하는 고온 중합이 우수합니다. 최근 리간드의 혁신은 90℃ 이상에서의 활성 저하를 억제하고 상업적 가능성을 넓히고 있습니다. 듀얼 사이트 및 하이브리드 설계는 좁은 분자 분획 및 넓은 분자 분획을 한 단계로 통합하여 재단사의 용융 레올로지를 실현합니다. 이러한 혁신으로 메탈로센 폴리에틸렌 시장의 제품 라인업은 더욱 다양해지고 있습니다.

메탈로센 폴리에틸렌 시장 보고서는 유형별(메탈로센 선형 저밀도 폴리에틸렌(mLLDPE), 메탈로센 고밀도 폴리에틸렌(mHDPE), 기타), 촉매 유형별(단일 사이트 지르코노센, 하프노센, 포스트메탈로센 등), 용도별(필름, 시트, 기타), 최종 사용자 산업별(포장, 농업, 기타), 지역별(아시아태평양, 북미, 기타)

2024년 점유율은 46.21%로 아시아태평양이 선도했으며, 이는 중국 180만 톤의 에틸렌 장치의 신설과 인도의 패키징 호전에 지지되고 있습니다. 이러한 투자는 원료의 안정성 확보 및 지역 컨버터의 납기 단축을 가능하게 합니다. 패키징, 건축용 멤브레인, 자동차용 연료탱크는 모두 지역의 오프테이크를 밀어 올리고 메탈로센 폴리에틸렌 시장의 CAGR은 5.71%를 유지할 것으로 예측됩니다.

북미는 셰일 에탄 비용의 이점과 촉매 혁신의 리더십에 의존하고 있습니다. 다우가 알버타 주에 건설 예정인 넷 제로 크래커는 저배출 가스로 프리미엄 수지의 생산을 지원하는 태세를 갖추고 있습니다. 멕시코는 미국 걸프 콤비나트에서 원료를 수입하고 부가가치가 높은 필름으로 전환하여 국내 소비 및 수출을 실시함으로써 백인테그레이션의 이익을 확보하고 있습니다.

유럽의 엄격한 플라스틱 규제는 수요에 도전하는 동시에 재활용 가능한 유연한 패키징으로 가는 길을 열어줍니다. 독일 자동차 부문은 경량화를 중시하고 북유럽 소매업체는 기계적 재활용을 단순화하는 단일 소재 구조를 지원합니다. Total Energys의 Amiral Complex는 중동 기업이지만 유럽에 수량을 공급하고 부족한 국내 공급을 보완하고 있습니다. 남미와 중동 및 아프리카는 신흥의 급성장중인 클러스터입니다. 브라질의 온실 부문 및 카타르의 폴리머 컴플렉스 확장은 메탈로센 폴리에틸렌 시장을 더욱 견인합니다.

The Metallocene Polyethylene Market size is estimated at USD 22.83 billion in 2025, and is expected to reach USD 28.63 billion by 2030, at a CAGR of 4.63% during the forecast period (2025-2030).

Robust demand for high-clarity down-gauged films, the scale-up of solar panel encapsulant lines, and modernization in agriculture sustain this growth path. Producers benefit from single-site catalyst technology that yields narrow molecular weight distribution, enabling consistent mechanical strength and superior optical properties at lower gauges. China's ethylene capacity additions, India's e-commerce boom, and capacity investments in the Middle East together reinforce upstream supply security, while ongoing shifts toward circular plastics keep strategic focus on advanced recycling and bio-based feedstocks. The Metallocene polyethylene market therefore marries performance gains with sustainability objectives and positions itself as a core enabler of next-generation flexible packaging solutions.

Converters continue to migrate toward thinner films that preserve mechanical integrity, and single-site catalysts facilitate uniform comonomer distribution that yields clarity alongside dart impact strength. Typical gauge reductions of 15-20% lower material use and carbon intensity, directly supporting brand-owner sustainability pledges. Narrow molecular weight distribution also cuts edge-trim waste on blown-film lines and improves bag-making throughput, which increases operating margins for convertors. Premium metallocene grades such as Exceed XP provide year-round toughness suited to cold-chain logistics, while the rapid rise of omnichannel retail elevates parcel-handling stresses that require stronger but lighter films.

Flexible formats replace rigid containers across food, home-care, and personal-care sectors as retailers prioritize shelf efficiency and lower logistics costs. Metallocene polyethylene delivers stronger hot-tack and wider sealing windows, reducing leakers on high-speed vertical form-fill-seal equipment. Trade bans on PVC in contact applications accelerate transition toward recyclable polyethylene blends, illustrated by PreservaWrap lines that replicate PVC clarity without chloride content. Medical device makers also pivot from PVC to metallocene polyethylene for biocompatibility, which reinforces healthcare demand and widens segment reach.

Swing crude and natural-gas prices cascade into ethylene swings, compressing margins for specialty resin producers who pay a 15-20% catalyst premium. Electrified crackers and carbon-capture retrofits inflate capital cost, adding pressure during feedstock spikes. Vertically integrated Middle Eastern producers retain cost leadership while Asian converters reliant on imports see steeper volatility. Bio-ethylene routes partly hedge volatility yet call for parallel infrastructure build-out, raising upfront cash needs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

mLLDPE commanded 59.01% Metallocene polyethylene market share in 2024. The segment retains leadership thanks to superior puncture resistance and dart impact strength that allow 15-20% down-gauging without packaging failure. Many beverage pouch producers shifted entirely to mLLDPE structures in 2024. In pipe coatings, mLLDPE's flexibility reduces cracking risk during coil-on-reel handling.

mHDPE is forecast to log a 6.65% CAGR through 2030, boosted by pressure pipe and chemical drum demand in developing economies. Stress-crack-resistant grades also penetrate fuel tank blow-molding and under-hood parts. Niche mLDPE lines serve specialty cast-film uses where melt strength is crucial. UHMWPE advances broaden reach into artificial joints and protective gear markets, fortifying value pools for the Metallocene polyethylene market.

Zirconocene catalysts held 62.75% share in 2024. Producers favor their proven operability across gas-phase and solution reactors. Strong track records shorten qualification times, essential for food-contact certifications.

Hafnocene systems, expanding at 5.25% CAGR, excel in high-temperature polymerization that enables faster gas-phase throughput. Recent ligand innovations temper activity drop-off above 90 °C, widening the commercial window. Dual-site and hybrid designs merge narrow and broad molecular fractions in one step, unlocking tailored melt rheology. These innovations further diversify offerings within the Metallocene polyethylene market.

The Metallocene Polyethylene Market Report is Segmented by Type (Metallocene Linear Low-Density Polyethylene (mLLDPE), Metallocene High-Density Polyethylene (mHDPE), and More), Catalyst Type (Single-Site Zirconocene, Hafnocene and Post-Metallocene, and More), Application (Films, Sheets, and More), End-User Industry (Packaging, Agriculture, and More), and Geography (Asia-Pacific, North America, and More).

Asia-Pacific led with 46.21% share in 2024, anchored by China's new 1.8 million t ethylene units and India's packaging upturn. These investments ensure feedstock security and shorten delivery time for regional converters. Packaging, construction membranes, and automotive fuel tanks together lifted regional off-take and are expected to keep the Metallocene polyethylene market on a 5.71% CAGR trajectory.

North America relies on shale-linked ethane cost advantages and catalyst innovation leadership. Dow's forthcoming net-zero cracker in Alberta is poised to support premium resin output with low embedded emissions. Mexico secures back-integration gains by importing feedstock from US Gulf complexes and converting into value-added films for domestic consumption and export.

Europe's strict plastic rules challenge demand yet simultaneously open space for recyclable flexible packaging. Germany's auto sector values weight reduction, and Nordic retailers champion mono-material structures that simplify mechanical recycling. TotalEnergies' Amiral complex, though Middle Eastern, channels volumes into Europe, supplementing short domestic supply. South America and the Middle East & Africa remain emerging yet fast-growing clusters. Brazil's greenhouse sector and Qatar's polymer complex expansion add incremental pull on the Metallocene polyethylene market.