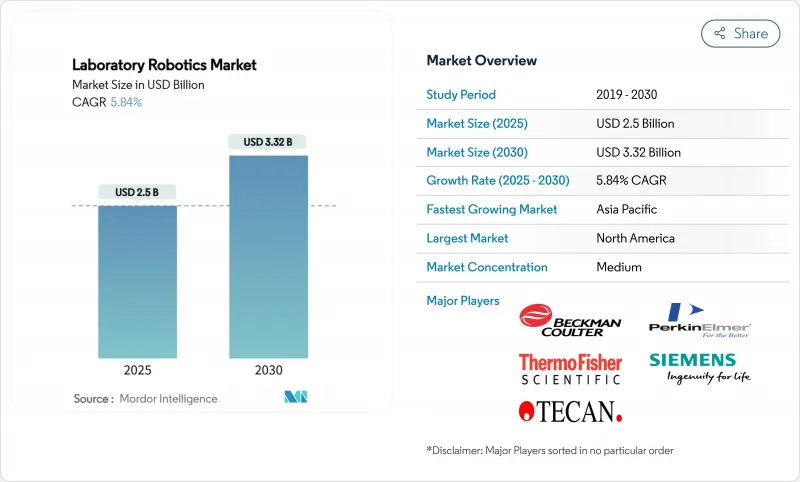

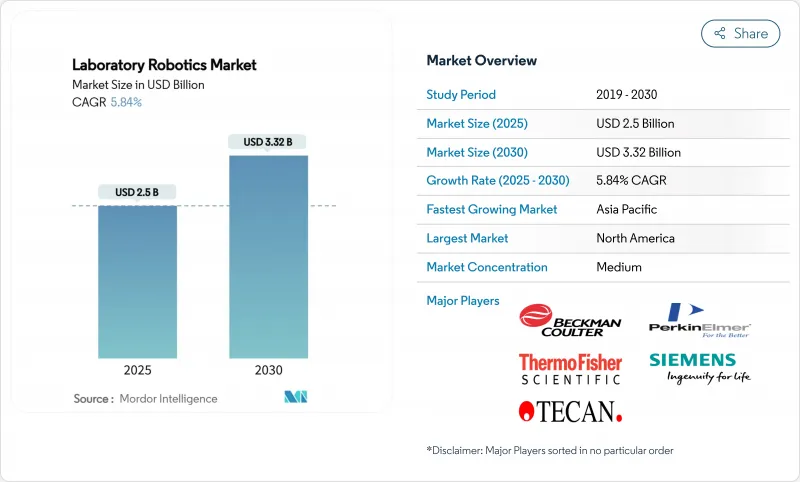

실험실 로봇 시장의 2025년 시장 규모는 25억 달러로, 2030년에는 33억 2,000만 달러에 이르고, CAGR 5.84%를 나타낼 것으로 예측됩니다.

측정된 궤적은 규율이 있는 장기적인 자동화 로드맵으로의 긴급 조달로부터의 변화를 시사합니다. FDA 대응 시스템에 대한 수요는 2025년에 Laboratory Developed Tests의 최종 규칙이 시행되어 검사실이 ISO-15189 준거의 로봇화를 목표로 하게 됨에 따라 높아집니다. 프리시전 메디신 파이프라인, 지속가능성 의무화, 모듈형 로봇 생태계는 투자 결정을 더욱 강화합니다. 소프트웨어, 장비, 밸리데이션 지원을 번들하는 공급업체가 계속 지갑 점유율을 획득하는 한편, 신흥 경쟁업체는 실험실 로봇 시장에서 차별화를 도모하기 위해 음향 분주, 모바일 조작, AI 통합에 주력하고 있습니다.

바이오리스크 완화 정책은 BSL-3 및 BSL-4 시설에서 감염성 샘플과의 수동 접촉을 제거해야 합니다. 메이요 클리닉의 자동화된 라인은 채혈량을 반감시키면서 연간 600만 이상의 분석을 처리하여 로보틱스가 어떻게 안전성과 시료 스튜어드십 모두를 향상시키는지를 입증하고 있습니다. 통합된 비전과 AI 모듈은 실시간으로 피펫팅 비정상적으로 플래그를 지정하여 데이터 무결성 감사를 만족시킵니다. 공급업체는 배치 사이에서 수행되는 자외선 오염 제거 사이클을 추가하여 운영자의 안전성을 손상시키지 않고 24시간 가동할 수 있습니다. 이러한 기능은 레퍼런스 실험실 및 백신 검사 센터를 중심으로 실험실 로봇 시장에서의 안정적인 수요를 지원합니다.

공중보건기구는 수십억 달러 규모의 예산을 할당하고 서지 대응 자동화를 명확하게 요구하고 있습니다. CEPI와 BARDA 보조금은 몇 주 내에 연구에서 대량 시험까지 확장하는 플랫폼을 규정하고 있습니다. 셰필드 대학의 자율주행 화학 연구실은 폐쇄형 루프 AI 로봇 워크플로우를 통해 폴리머의 발견 기간을 엄청나게 단축했습니다. 제조업체는 현재 실험실이 바이러스학, 혈청학 및 백신의 역가 측정을 위해 단시간에 재구성할 수 있는 모듈식 카트를 설계하고 있습니다. 이와 같이 준비 자금은 실험실 로봇 시장 전체의 유연한 시스템에 몰입하고 있습니다.

ISO 15189 : 2022는 엄격한 검증 및 문서화를 요구합니다. A2LA는 2024년 미국 최초의 실험실을 신규격으로 인정하고 임상 등급의 로봇 공학에 필요한 광범위한 감사 추적을 강조했습니다. 중복 전원 공급 장치, 클린룸 HVAC, 안전한 데이터 백본으로 인해 생명 과학 시설의 리노베이션은 현재 평방 피트당 평균 837달러입니다. 라틴아메리카와 아프리카의 소규모 시설에서는 종종 구매가 선보이며, 실험실 로봇 시장의 단기적인 확대가 억제되고 있습니다.

2024년 실험실 로봇 시장에서는 병원이 시료 처리를 고처리량 라인에 통합하여 임상 진단이 41%의 최대 점유율을 차지했습니다. 그러나 유전체학 솔루션은 2030년까지 11.20%의 연평균 복합 성장률(CAGR)을 나타내며 다른 모든 용도를 능가합니다. 로봇 액체 처리기는 종양학 및 희귀질환 패널에서 신뢰할 수 있는 변종 호출의 필수 조건인 균일한 라이브러리 전처리를 보장합니다. 미생물학 연구소에서는 자동화된 병원체 확인 셀을 도입하여 소요 시간을 3시간 미만으로 단축하고 항균제 관리 이니셔티브를 지원합니다. 신약 개발 플랫폼은 이미징 스테이지와 플레이트 무버를 통합하고, 스케일 업한 표현형 스크리닝을 실현하고, 단백질체학 워크플로우는 바이오마커 탐색을 위한 고분해능 질량 분석기와 로봇의 조합에 의해 견인력을 늘리고 있습니다.

유전체학 워크플로우와 관련된 실험실 로봇 시장 규모는 시퀀싱 비용이 낮고 검사량이 증가함에 따라 함께 성장합니다. 음향 이송, 환경 제어 및 바코드를 통한 추적성을 결합한 시스템은 현재 국립 유전체 센터 자본 예산의 짧은 목록에 게시됩니다. 제약 회사의 파이프라인은 임상 바이오마커의 검증을 가속화하기 위해 이러한 유연한 로봇에 의존하고 있으며, 유전체 산업이 실험실 로봇 산업에서 가장 빠르게 발전하는 분야임을 뒷받침합니다.

2024년 실험실 로봇 시장 수익의 38.50%는 제약 및 생명공학 기업이었습니다. 반면에 CRO는 스폰서의 아웃소싱 동향을 반영하며 CAGR 9.80%의 속도입니다. CRO는 클라우드 제어 실험실에 투자하고 고객이 원격 조작으로 로봇 프로토콜을 시작함으로써 프로젝트 사이클을 단축하고 사내 용량을 확보합니다. 학술기관은 보조금과 공급업체와의 제휴를 통해 소유 비용 없이 최첨단 자동화를 이용할 수 있습니다. 임상 실험실은 인력 부족을 해결하기 위해 자동화하고, 로봇을 사용하여 밤새도록 분석기를 로드하고, 환자의 결과를 신속하게 발행합니다.

임상시험 설계가 분산되고 환자 중심 형식으로 이동하는 동안 CRO는 실시간으로 보관 상태를 기록하면서 분석 스테이션간에 플레이트를 리디렉션 할 수있는 모바일 로봇을 채택합니다. 실험실 로봇 시장은 피-포-서비스 모델이 많은 후원자들에게 자본 지출을 분산시키고 지속적인 함대 확장을 촉진함으로써 이익을 얻고 있습니다.

실험실 로봇 시장 보고서는 용도(신약 개발, 임상 진단, 미생물학, 유전체학, 단백질체학), 최종 사용자(임상 실험실, 조사 실험실, 제약 및 생명공학, 크로스), 로봇 유형(리퀴드 핸들링, 샘플 핸들링, 협동 모바일, 완전 통합), 워크플로우 단계(분석 전, 분석, 분석 후), 지역별로 분류됩니다.

북미는 성숙한 바이오 의약품 파이프라인과 FDA 준거 자동화의 조기 도입으로 2024년의 실험실 로봇 시장 점유율의 40.80%를 획득했습니다. 병원 네트워크는 직원의 감소에 대항하기 위해 지출을 가속화하고 보스턴과 샌디에고 벤처 지원의 생명 공학 허브는 자체 최적화 탐색 셀을 도입하고 있습니다. NIH의 Advanced Research Projects Agency for Health를 통한 연방 정부의 자금 지원은 정밀의료 실험실에 대한 주문을 더욱 향상시킵니다.

아시아태평양의 2030년까지의 CAGR은 8.30%로 예측되며, 이는 세계 최고입니다. 중국의 5개년 계획에서는 로봇 연구 개발에 4,520만 달러, 일본의 새로운 로봇 전략에서는 4억 4,000만 달러, 한국에서는 지능형 시스템에 1억 2,800만 달러의 예산을 계상해 국내 공급자를 자극하고 있습니다. 제약 제조업체는 ICH나 PIC/S 규격에 대응하기 때문에 품질 관리 실험실을 생산 라인과 병행하여 확장하여 유연한 로봇의 보급을 촉진합니다. 집단 유전학에 특화된 학술 메가랩은 대규모 바이오뱅크 검체를 처리하기 위해 음향 핸들러와 이동 로봇을 도입합니다.

유럽에서는 Horizon Europe의 1억 8,350만 달러의 로봇 공모에 힘입어 꾸준한 기세를 유지하고 있습니다. 지속가능성에 관한 법령은 압축공기에 대한 의존을 줄이는 에너지 효율이 높은 로봇을 연구실에 추천하고 있습니다. 독일의 자동화 기업은 EU 전역에 모듈식 워크셀을 수출하여 지역 내 공급망을 강화합니다. 중동 및 아프리카는 헬스 투어리즘의 허브와 백신 충진 마감 공장이 병리학과 QC 실험실을 현대화함에 따라, 모아적이면서 가속화되는 수요를 기록합니다. 남미에서는 기술 이전 프로그램과 현지 시약 제조가 결합되어 혜택을 누리고 있습니다.

The laboratory robotics market is valued at USD 2.5 billion in 2025 and is forecast to reach USD 3.32 billion by 2030, advancing at a 5.84% CAGR.

The measured trajectory signals a shift from emergency-driven procurement toward disciplined, long-term automation roadmaps. Demand for FDA-ready systems grows as the Laboratory Developed Tests final rule comes into force in 2025, pushing laboratories toward ISO-15189-compliant robotics. Precision medicine pipelines, sustainability mandates, and modular robotic ecosystems further reinforce investment decisions. Vendors that bundle software, instruments, and validation support continue to capture wallet share, while emerging competitors focus on acoustic dispensing, mobile manipulation, and AI integration to differentiate in the laboratory robotics market.

Bio-risk mitigation policies now require BSL-3 and BSL-4 facilities to eliminate manual contact with infectious samples. Automated lines at Mayo Clinic process more than 6 million assays annually while halving blood-draw volumes, demonstrating how robotics improve both safety and specimen stewardship. Integrated vision and AI modules flag pipetting anomalies in real time, satisfying data-integrity audits. Vendors add ultraviolet decontamination cycles that run between batches, allowing around-the-clock operation without compromising operator safety. These capabilities underpin steady demand within the laboratory robotics market, especially in reference labs and vaccine-testing centers.

Public-health agencies allocate multibillion-dollar budgets that expressly call for surge-ready automation. CEPI and BARDA grants stipulate platforms that scale from research to mass testing within weeks. The University of Sheffield's self-driving chemistry lab cut polymer discovery timelines by orders of magnitude through closed-loop AI-robot workflows. Manufacturers now design modular carts that laboratories can reconfigure for virology, serology, or vaccine potency assays on short notice. Preparedness funding thus acts as a tailwind for flexible systems across the laboratory robotics market.

ISO 15189:2022 demands rigorous validation and documentation. A2LA accredited the first U.S. lab under the new standard in 2024, highlighting the extensive audit trail required for clinical-grade robotics. Life-science fitouts now average USD 837 per square foot, owing to redundant power, clean-room HVAC, and secure data backbones. Smaller facilities in Latin America and Africa often postpone purchases, tempering near-term uptake within the laboratory robotics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Clinical diagnostics contributed the largest 41% share to the laboratory robotics market in 2024 as hospitals consolidated sample processing under high-throughput lines. Genomics solutions, however, are charted for 11.20% CAGR through 2030, outperforming all other applications. Robotic liquid handlers ensure uniform library prep, a prerequisite for reliable variant calling in oncology and rare-disease panels. Microbiology labs deploy automated pathogen-identification cells that cut turnaround to under three hours, supporting antimicrobial stewardship initiatives. Drug-discovery platforms integrate imaging stages with plate movers for phenotypic screening at scale, while proteomics workflows gain traction as robots couple with high-resolution mass-spectrometers for biomarker discovery.

The laboratory robotics market size tied to genomics workflows will grow in lockstep with falling sequencing costs and rising test volumes. Systems that combine acoustic transfer, environmental controls, and barcode-verified traceability now appear on capital-budget shortlists at national genome centers. Pharmaceutical pipelines lean on these flexible robots to accelerate clinical biomarker validation, reinforcing genomics as the fastest-advancing slice of the laboratory robotics industry.

Pharmaceutical and biotechnology companies accounted for 38.50% of laboratory robotics market revenue in 2024 because R&D spends prioritize validated, closed-loop platforms. Contract research organizations, meanwhile, are on pace for 9.80% CAGR, reflecting sponsor outsourcing trends. CROs invest in cloud-controlled labs where clients trigger robotic protocols remotely, shortening project cycles and freeing internal capacity. Academic institutes pair grants with vendor partnerships to access state-of-the-art automation without full ownership costs. Clinical labs automate to curb staffing shortages, using robots to load analysers overnight and speed patient results.

As trial designs shift toward decentralized and patient-centric formats, CROs embrace mobile robots that can redirect plates among assay stations while documenting custody in real time. The laboratory robotics market benefits because fee-for-service models spread capital expenditure across many sponsors, encouraging continued fleet expansion.

The Laboratory Robotics Market Report is Segmented by Application (Drug Discovery, Clinical Diagnostics, Microbiology, Genomics, Proteomics), End-User (Clinical Labs, Research Labs, Pharma & Biotech, Cros), Robot Type (Liquid-Handling, Sample-Handling, Collaborative Mobile, Fully Integrated), Workflow Stage (Pre-Analytical, Analytical, Post-Analytical), and Geography. Market Forecasts in Value (USD).

North America captured 40.80% of laboratory robotics market share in 2024 due to mature biopharma pipelines and early adoption of FDA-compliant automation. Hospital networks accelerate spending to counter staff attrition, while venture-backed biotech hubs in Boston and San Diego install self-optimizing discovery cells. Federal funding via the NIH's Advanced Research Projects Agency for Health further underwrites purchase orders for precision-medicine labs.

Asia-Pacific is projected for 8.30% CAGR through 2030, the highest worldwide. China's Five-Year Plan directs USD 45.2 million into robotics R&D, Japan's New Robot Strategy adds USD 440 million, and Korea earmarks USD 128 million for intelligent systems, catalysing domestic suppliers. Pharmaceutical manufacturers scale quality-control labs alongside production lines to meet ICH and PIC/S standards, driving pull-through for flexible robots. Academic mega-labs focused on population genetics install acoustic handlers and mobile robots to process large-scale biobank specimens.

Europe maintains steady momentum supported by Horizon Europe's USD 183.5 million robotics call. Sustainability statutes nudge laboratories toward energy-efficient robots that reduce compressed-air dependence. German automation firms export modular work cells across the EU, reinforcing intra-regional supply chains. The Middle East and Africa register nascent yet accelerating demand as health-tourism hubs and vaccine-fill-finish plants modernize pathology and QC laboratories. South America benefits from technology-transfer programs paired with local reagent manufacturing, yet broader uptake hinges on credit availability and engineer training pipelines.