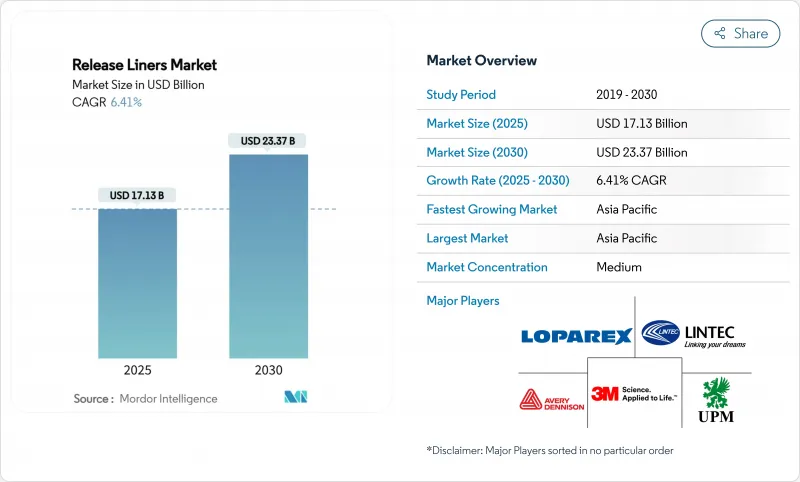

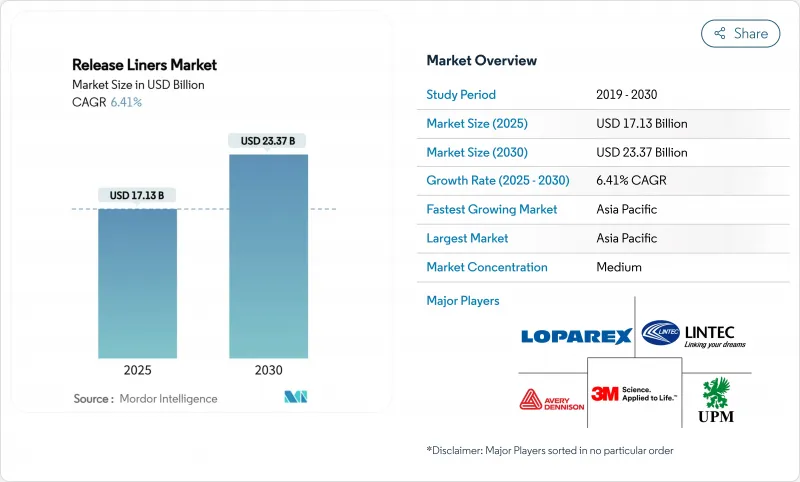

릴리스 라이너 시장 규모는 2025년에 171억 3,000만 달러, 2030년에는 233억 7,000만 달러에 이를 것으로 추정되며, 예측 기간(2025-2030년)의 CAGR은 6.41%를 나타낼 전망입니다.

전자상거래 물류, 고급 식품 포장, 선진 산업용 테이프 등 안정적인 박리 성능과 엄격한 치수 공차가 요구되는 용도가 견조한 수요를 낳고 있습니다. 라벨은 여전히 중심적인 용도이지만 의료기기, 프리프레그 복합재료, 배터리 셀 테이프는 보다 급속히 확대되고 있으며, 이익률이 높고 기술 집약적인 구조로 제품 구성을 바꾸고 있습니다. 아시아태평양은 생산량과 성장률의 양면에서 주도권을 잡고 있기 때문에 생산규모의 우위성이 강화되는 반면 서양 브랜드 소유자는 공급망 집중의 위험에 노출됩니다. 소재의 혁신은 가속화되고 있습니다. 그래신 종이는 여전히 주류이지만 컨버터는 재활용성을 희생하지 않고 내습성, 내열성, 내약품성을 요구하고 있기 때문에 필름이나 폴리코팅된 대체 소재가 급성장하고 있습니다.

식음료 브랜드의 소유자는 표백된 기재와 솔벤트 기반 코팅을 표백되지 않은 글라신, 수용성 실리콘, 직접 식품과 접촉하는 규칙을 충족하는 퇴비화 가능한 화학물질로 대체하고 있습니다. 린텍의 자연스러운 톤 글래신은 형광 증백제를 사용하지 않고 그라비아 인쇄의 충실성을 실현하는 최소한의 가공을 한 종이에 축발을 보여줍니다. 기능적 성능은 현재 유지 및 수분에 대한 장벽 보호에 이르기까지 점착제의 전이 없이 성분의 투명화를 가능하게 하고 있습니다. 추적 가능성를 문서화할 수 있는 컨버터는 소매업체가 지속가능성 스코어카드를 강화하면서 가격 프리미엄을 획득하고 있습니다. PFAS 프리 시스템에 대한 수요는 EU에서 북미로 확산되고 있으며, 공급업체는 고속 도포에서도 깨끗하게 박리하는 불소 프리 대체품을 개발할 필요가 있습니다. 2024년 식음료 점유율은 29.26%에 이르며, 재료 업그레이드는 세계 수량에 빠르게 파급되어 공급업체의 인증 장애물을 강화했습니다.

클릭 & 콜렉트, 구독, 당일 배송 모델에서 소포량은 계속 증가합니다. 릴리스 라이너는 150m/min 이상의 자동 인쇄 라인, 가변 데이터 바코딩에 대응, -20℃에서 40℃까지의 콜드체인에 대한 내성을 요구합니다. 일관된 박리력과 웹의 평탄성은 가동 중지 시간과 잘못 붙여넣기를 최소화하고 포장 당 완성 비용에 직접 영향을 미칩니다. 프리미엄 앤 박스의 동향은 현재 옴니채널 식료품과 퍼스널케어의 출하에도 미치고 있으며, 촉감이 좋은 니스나 메탈릭한 악센트를 한 다층 라벨 수요를 밀어 올리고 있습니다. 이 라벨은 정밀 코팅 라이너를 사용하여 사용할 때까지 잉크 무결성을 보호하는 구조입니다. 따라서 릴리스 라이너 시장은 수량이 증가하고 로봇 및 이미지 검사 장비에 최적화된 고사양 종이 및 필름 안감으로 가치 이동하고 있습니다.

사용한 라이너는 실리콘 잔류물이 표준 재활용을 방해하기 때문에 대부분이 매립되어 있습니다. FINAT의 CELAB-Europe 컨소시엄에서는 2025년까지 75%의 재활용을 목표로 하고 있지만, 회수 물류와 회수 섬유에 대한 최종 시장 수요에 따라 진척이 결정됩니다. 웨스턴 미시간 대학의 수용성 장벽층은 펄프화 동안 실리콘 제거를 가능하게 하지만, 공정 개조와 베일 운송 비용으로 인해 상업적 채용은 여전히 제한되어 있습니다. 사스타나 그룹의 위스콘신 공장은 기술적 실현 가능성을 보여 주지만 그 지리적 범위는 좁습니다. 확대 생산자 책임 제도가 보급됨에 따라 컨버터는 라이너리스 및 재사용 가능한 형식에 대한 가격 경쟁력을 손상시키는 가격 상승에 직면하고 있습니다.

글래신은 2024년 릴리스 라이너 시장 규모에서 37.18%의 점유율을 유지하며 비용 효율성, 표면 평활성, FDA 식품 접촉 클리어런스 덕분에 계속해서 대량의 라벨 테이프 프로그램을 지원했습니다. 그러나 브랜드 소유자가 화물 배출량을 줄이기 위해 낮은 그램의 라이너를 지정하고 평방미터 수요가 증가하더라도 톤수가 감소하기 때문에 성장이 완만해집니다. 폴리에틸렌 코트 크래프트 종이는 내 습성이 비 코팅 등급보다 우수하기 때문에 냉장 식품 및 야외 라벨링으로 증가하고 있습니다. BO-PET나 BOPP제의 필름 라이너는 셀룰로오스계 종이의 유리 전이점을 넘는 온도에서 경화하는 일렉트로닉스, 항공우주, 자동차용 라미네이트로 급속히 확대되고 있습니다.

이축 연신 폴리아미드, PTFE 코팅 유리 크로스, 마이크로피브릴화 셀룰로오스 복합재료는 정전기 방지, 260℃ 이상의 열 안정성, 발수성 등의 다기능 특성을 갖추고 있습니다. 컨버터가 멀티패스 코팅 라인과 인라인 플라즈마 처리로 이형제를 고정하기 때문에 치료는 틈새 시장이지만 평균 판매 가격은 상승하고 있습니다. 글래신 공급업체는 깨끗한 라벨 포장을 대상으로 미표시, 금속화, 탄산 칼슘 포함 등 배리어성을 강화한 바리에이션으로 대응하고 있습니다. 이러한 반복적인 이동으로 인해, 그래신은 가장 빠른 성장 슬라이스를 인공 필름에 양도하면서도 관련성을 유지하고 있습니다.

실리콘 시스템은 2024년 릴리스 라이너 시장의 81.22%를 차지하며 다목적 경화 화학, 낮은 표면 에너지, 풍부한 베이스 실록산 공급에 지지되었습니다. 백금 촉매 UV 실리콘은 경화 창을 단축하고 1,000m/분의 고속 코팅을 가능하게 함으로써 가격 경쟁력을 유지하고 있습니다. 불소 수지 기반 릴리스 라이너 시장 규모는 작지만 CAGR 7.64%를 나타낼 전망입니다. 이는 퍼플루오로 사슬이 고온 복합 금형이나 공격적인 접착 테이프에 필수적인 화학적 불활성과 초저박리력을 제공하기 때문입니다.

PFAS 화학물질에 대한 규제압력은 항공우주를 위한 기존의 플루오로실리콘이 수요를 유지하는 반면, 포장과 위생분야는 아크릴과 폴리올레핀의 박리 바니시로 이동하는 분열을 촉진하고 있습니다. 하이 타워 제품과 같은 공급업체는 현재 점도 및 고정 수지로 맞춤화된 PFAS 프리 처방을 판매하고 있으며 클린 릴리스와 재활용성의 균형을 맞추고 있습니다. 실리콘 제조업체는 광학 필름 및 반도체 웨이퍼로의 실록산 전환을 최소화하는 전환 제어 등급으로 지원합니다. 경쟁 우위는 하위 ppm의 전환을 검증하고 고객 인증을 가속화하는 분석 능력에 달려 있습니다.

2024년 시장 점유율은 아시아태평양이 42.74%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR) 7.56%를 나타낼 것으로 예측됩니다. 이는 이 지역의 수직 통합 펄프에서 코팅까지 공급망과 중간층의 소비 확대에 지원됩니다. 포장 컨버터가 전자상거래 풀필먼트 허브 근처에서 생산 능력을 증강하고 있기 때문에 증가 톤수의 대부분을 중국이 차지하고, 일본과 한국은 반도체 공장과 배터리 셀 조립용 고정밀 라이너에 특화하고 있습니다. 신재생에너지에 대한 정부의 우대조치도 풍력 블레이드 제조에서 프리프레그 라이너 수요를 끌어올리고 있습니다.

북미는 항공우주, 의료기기, 퀵서비스 레스토랑 포장에서 대규모 설치 기반을 유지하고 있습니다. 미국은 미네소타주, 매사추세츠주, 캘리포니아주를 중심으로 한 클러스터의 혜택을 받아 FDA 인가의 의료 테이프 개발의 중심지가 되고 있습니다. 캐나다는 풍부한 삼림 자원을 활용하여 FSC 인증 그래신과 크레이 코트 크래프트를 보급하고 소매업체의 지속가능성 의무에 부합하고 있습니다. 멕시코의 니어 쇼어링 붐을 통해 다국적 기업은 자동차 및 소비자용 전자 기기 공장 근처에 RFID, 라벨, 필름 코팅 시설을 설치하게 되었습니다. 에이브리 데니슨의 1억 달러 투자는 이 기세를 증명합니다.

유럽은 여전히 규제 선진을 끊고 있으며 소비자 사용 후 라이너의 재활용률을 증명할 수 있는 공급업체에게 보상을 주는 순환성 목표를 추진하고 있습니다. 독일은 자동차 경량화와 관련된 산업용 테이프 기술 혁신의 선두에 서서 이탈리아와 프랑스는 소량 생산으로 마무리 좋은 라벨이 고급 라이너를 요구하는 고급 포장에 자본을 투하하고 있습니다. 북유럽 국가들은 PFAS의 단계적 폐지를 의무화하고 바이오 대체품을 추진함으로써 세계적인 재료 표준에 영향을 미치고 있습니다. 동유럽은 EU 단일 시장에 공급하는 비용 효율적인 생산 코리도로서 기능하고 있지만, 지정학적 긴장이 원료 물류를 혼란시킬 수도 있습니다.

The Release Liners Market size is estimated at USD 17.13 billion in 2025, and is expected to reach USD 23.37 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

Steady demand stems from e-commerce logistics, premium food packaging, and advanced industrial tapes, all of which require consistent release performance and tight dimensional tolerances. Labels remain the anchor application, yet medical devices, prepreg composites, and battery cell tapes are expanding faster and reshaping the product mix toward higher-margin, technology-intensive constructions. Asia-Pacific's dual leadership in volume and growth reinforces production scale advantages while exposing Western brand owners to supply-chain concentration risks. Material innovation is accelerating: glassine paper still dominates, but filmic and poly-coated alternatives are growing quickly as converters seek moisture, heat, and chemical resistance without sacrificing recyclability.

Food and beverage brand owners are replacing bleached substrates and solvent-based coatings with unbleached glassine, water-borne silicones, and compostable chemistries that meet direct-food-contact rules. LINTEC's natural-tone glassine illustrates the pivot toward minimally processed papers that enable gravure print fidelity while eliminating optical brighteners . Functional performance now extends to barrier protection against grease and moisture, permitting clear ingredient transparency without adhesive migration. Converters able to document traceability capture price premiums as retailers tighten sustainability scorecards. Demand for PFAS-free systems is spreading from the EU to North America, pushing suppliers to scale fluorine-free alternatives that still release cleanly at high application speeds. With food and beverage holding 29.26% share in 2024, iterative material upgrades ripple quickly across global volumes and reinforce supplier qualification hurdles.

Parcel volumes continue rising with click-and-collect, subscription, and same-day delivery models. Release liners must perform across automated print-apply lines that exceed 150 m/min, handle variable-data barcoding, and endure cold-chain swings from -20 °C to 40 °C. Consistent release force and web flatness minimize downtime and misapplies, directly influencing fulfillment cost per package. Premium unboxing trends now extend to omnichannel grocery and personal-care shipments, boosting demand for multi-layer labels with tactile varnishes and metallic accents. These constructions rely on precision-coated liners to protect ink integrity until point-of-use. The release liner market, therefore, sees volume gains plus a value shift toward high-spec paper and film backings optimized for robotics and vision inspection equipment.

Used liner is largely landfilled because silicone residues impede standard recycling. FINAT's CELAB-Europe consortium aims for 75% recycling by 2025, but progress hinges on collection logistics and end-market demand for recovered fibers. Western Michigan University's water-soluble barrier layer enables silicone removal during pulping, yet commercial adoption remains limited by process retrofits and bale transport costs. Sustana Group's Wisconsin plant shows technical feasibility, but its geographic reach is narrow. As Extended Producer Responsibility schemes spread, converters face escalating fees that erode price competitiveness versus linerless or reusable formats.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Glassine retained 37.18% share of release liner market size in 2024 and continues to anchor high-volume label and tape programs thanks to cost efficiency, surface smoothness, and FDA food-contact clearances. Yet growth moderates as brand owners specify lower-grammage liners to cut freight emissions, eroding tonnage even where square-meter demand rises. Polyethylene-coated kraft papers are gaining in chilled-food and outdoor labeling where moisture resistance outperforms uncoated grades. Filmic liners made from BO-PET and BOPP are expanding quickly in electronics, aerospace, and automotive laminates that cure at temperatures beyond the glass-transition point of cellulosic papers.

Alternative substrates inside the "Others" category are setting the pace: bi-axially oriented polyamide, PTFE-coated glass cloth, and micro-fibrillated cellulose composites deliver multi-functional properties such as anti-static release, thermal stability above 260 °C, and repulpability. Adoption remains niche yet lifts average selling price because converters implement multi-pass coating lines and inline plasma treatments to anchor release agents. Glassine suppliers are responding with barrier-enhanced variations-unbleached, metallized, or calcium-carbonate-filled-aimed at clean-label packaging. These iterative shifts ensure glassine stays relevant while ceding the fastest growth slices to engineered films.

Silicone systems controlled 81.22% of the 2024 release liner market, supported by versatile cure chemistries, low surface energy, and abundant supply of base siloxanes. Platinum-catalyzed UV silicones shorten cure windows, enabling high-speed 1,000 m/min coating that sustains price competitiveness. The release liner market size for fluoropolymer-based agents is smaller yet advancing at 7.64% CAGR because perfluorinated chains deliver chemical inertness and ultra-low release force vital in high-temperature composite molds and aggressive adhesive tapes.

Regulatory pressure on PFAS chemicals is fostering a split: legacy fluoro-silicones for aerospace retain demand, while packaging and hygiene sectors shift toward acrylic or polyolefin release varnishes. Suppliers such as Hightower Products now market PFAS-free formulations customized by viscosity and anchorage resins, balancing clean release with recyclability. Silicone producers answer with controlled-migration grades that minimize siloxane transfer onto optical films and semiconductor wafers. Competitive advantage hinges on analytical capability to verify sub-ppm migration and accelerate customer qualification.

The Release Liner Market Report is Segmented by Substrate (Clay-Coated Kraft Paper, Filmic Liners, and, More), Release Agent (Silicone, Fluoropolymer, and More), Application (Labels, Graphics, and More), End-Use Industry (Food and Beverage, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominated with 42.74% market share in 2024 and is projected to grow at a 7.56% CAGR through 2030, underpinned by the region's vertically integrated pulp-to-coating supply chain and expanding middle-class consumption. China accounts for the bulk of incremental tonnage as packaging converters ramp capacity near e-commerce fulfilment hubs, while Japan and South Korea specialize in high-precision liners for semiconductor fabs and battery cell assembly. Government incentives for renewable energy also lift demand for prepreg liners in wind-blade production.

North America preserves a sizeable installed base in aerospace, medical device, and quick-service restaurant packaging. The United States is the hub for FDA-cleared medical tape development, benefiting from clusters around Minnesota, Massachusetts, and California. Canada leverages abundant forest resources to promote FSC-certified glassine and clay-coated kraft, aligning with retailer sustainability mandates. Mexico's near-shoring boom encourages multinationals to co-locate RFID, label, and filmic coating facilities close to automotive and consumer-electronics plants; Avery Dennison's USD 100 million investment testifies to this momentum.

Europe remains the regulatory vanguard, driving circularity targets that reward suppliers able to certify post-consumer liner recycling rates. Germany spearheads industrial tape innovation linked to automotive lightweighting, whereas Italy and France capitalize on luxury packaging where small-batch, high-finish labels command premium liners. Nordic countries influence global material standards by mandating PFAS phase-outs and promoting bio-based alternatives. Eastern Europe serves as a cost-effective production corridor supplying the EU single market, though geopolitical tensions occasionally disrupt feedstock logistics.