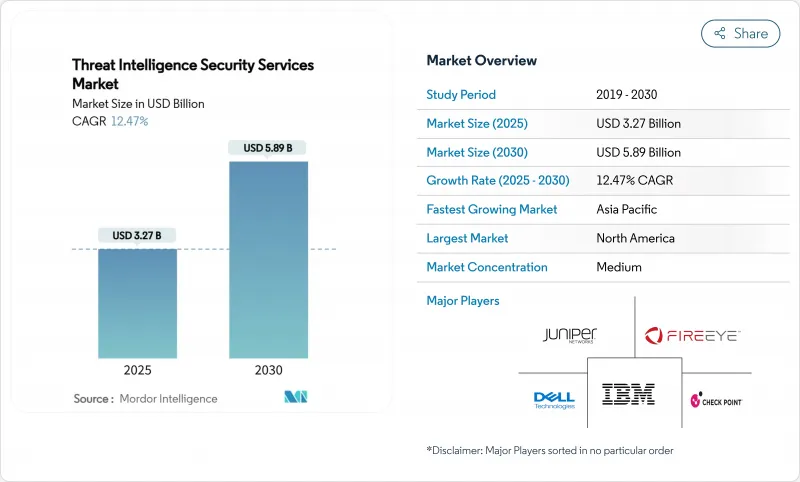

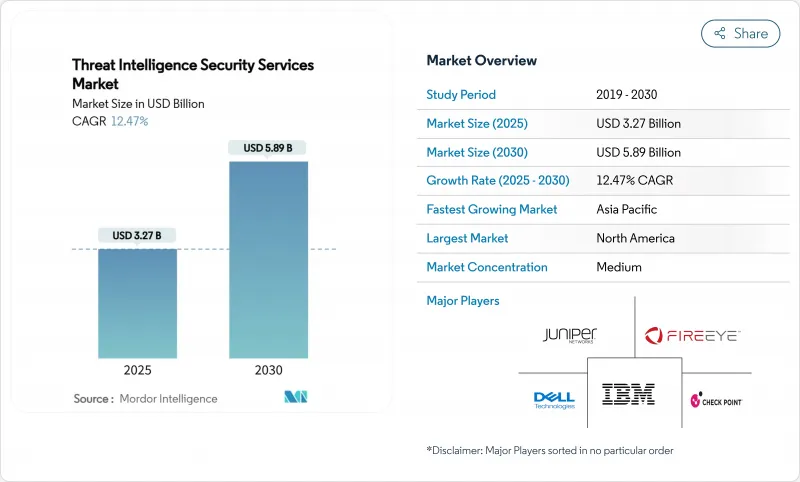

위협 인텔리전스 보안 서비스 시장 규모는 2025년에 32억 7,000만 달러, 2030년에는 58억 9,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 12.47%를 나타낼 전망입니다.

이 시장 확대는 리액티브 경계 방어에서 지속적인 위협 사냥, 노출 관리 및 예측 분석으로의 결정적인 변화를 반영합니다. 국가 주도의 캠페인이 격화되고 클라우드 보안 인시던트가 65% 증가하고 주요 사법 관할구에서 위반 통지가 의무화됨으로써 실시간 상황에 맞는 위협 데이터에 대한 수요가 높아지고 있습니다. 제로 트러스트와 XDR(Extended Detection and Response)의 전개로 대표되는 플랫폼의 융합은 보안팀이 통합된 가시성과 자동응답을 요구하는 가운데 투자를 더욱 가속화하고 있습니다. 동시에 애플리케이션 프로그래밍 인터페이스의 공격 대상이 급증하고 생성된 AI 코드 어시스턴트에서 발생하는 내부자 위험으로 인해 기업은 위험 태세를 재검토하고 있으며 위협 인텔리전스 보안 서비스 시장은 활기차고 있습니다.

Volt Typhoon 및 Salt Typhoon과 같은 국가 그룹은 중요한 인프라에 대한 활동을 강화하고 있으며, 조직은 전술적인텔리전스와 사고 발생 전의 기여 능력을 우선하도록 요구하고 있습니다. 사이버보안 및 인프라 보안국(CISA)은 2024년 3,368건의 랜섬웨어 사전 통지를 발행했으며 고급 침입 시도가 대량으로 진행되고 있음을 뒷받침했습니다. 공격은 이제 스파이 활동의 영역을 넘어 파괴적인 사전 배치를 포함하게 되어 지속적인 감시와 전문적인 사냥이 요구되고 있습니다. 이란 공격자는 의료 및 금융 서비스를 동시에 목표로 삼고 있으며 위협 인텔리전스는 섹터를 넘어선 전략적 필수 사항이 되었습니다. 이러한 움직임은 관리 감지, 멀웨어 분석 향상 및 컨텍스트 기반 기여 서비스에 대한 투자를 가속화합니다.

클라우드로의 전환은 공격 입구를 증가시키고 기업은 멀티클라우드 환경에서 수천 개의 API를 운영하고 있습니다. API의 장애는 2024년에 보고된 클라우드 침해의 대부분에 기여하고 있으며, 동서 트래픽의 가시성 격차가 드러났습니다. 전통적인 네트워크 모니터링에서는 찰나적인 워크로드에 대한 컨텍스트가 부족하여 종속성을 실시간으로 매핑할 수 있는 클라우드 네이티브 위협 인텔리전스의 채택이 가속화되었습니다. 마이크로서비스 아키텍처는 자산 목록을 더욱 복잡하게 만들고 자동 감지와 지속적인 위험 점수에 대한 의존도를 높이고 있습니다. 그 결과 서버리스 환경과 컨테이너 환경에 맞는 클라우드 제공 분석 엔진과 노출 관리 모듈의 기세가 지속되고 있습니다.

딥 포렌식과 멀웨어 리버스 엔지니어링 수요는 공급을 능가합니다. 국가 수준의 적 전술을 마스터하려면 오랜 훈련이 필요하지만 보안 팀은 인력 감소와 임금 상승에 직면 해 있습니다. 이 격차는 소규모 공급업체가 전문가를 확보하는 데 어려움을 겪고 있으며, 고객이 관리 감지 및 응답에 턴키 커버리지를 요청하게 됨에 따라 통합을 촉구합니다. 공급업체는 현재 루틴의 트리아지를 자동화하고 희귀 전문가를 보다 가치 있는 업무에 돌려주어야 하기 때문에 AI 지원 분석 모듈에 대한 관심이 높아지고 있습니다.

클라우드 배포는 이미 위협 인텔리전스 보안 서비스 시장 점유율의 58%를 차지합니다. 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 18.20%를 나타낼 것으로 예상되며 클라우드 네이티브 분석 엔진의 중요성이 높아지고 있습니다. 탄력적 컴퓨팅 분산 스토리지를 통해 공급자는 고객측 하드웨어 없이 페타바이트 규모의 원격 측정을 처리할 수 있습니다. 이는 위협 인텔리전스 보안 서비스 시장 규모가 2030년에 58억 9,000만 달러로 확대되는 데 매우 중요합니다. On-Premise 배포는 로컬 데이터 처리를 필요로 하는 소블린 클라우드 및 방어의 맥락에서 살아나고 있지만 개발 로드맵은 현재 독립형 어플라이언스보다 하이브리드 커넥터를 선호합니다.

하이브리드 배포는 클라우드를 사용하여 규모를 확장하면서도 규정 준수를 위해 특정 데이터 세트를 국내에 보유하는 규제 대상 기업들 사이에서 증가하고 있습니다. 기존 센서에서는 컨테이너 트래픽의 컨텍스트가 부족했기 때문에 API 중심의 공격 벡터는 클라우드와의 공명을 두드러지게 했습니다. Palo Alto Networks는 AI를 중심으로 한 연간 경상 수익이 2억 달러를 넘어 전년 대비 4배의 성장을 이뤘다고 보고하며 클라우드 제공 머신러닝 모듈에 대한 의욕을 입증하고 있습니다. 따라서 클라우드의 이점은 확립되었지만 공급업체는 추가 보급을 가속화하기 위해 대기 시간, 암호화 및 현지 요인을 해결해야 합니다.

Managed Detection & Response는 2024년 기준 위협 인텔리전스 보안 서비스 시장 점유율의 56%를 차지했으며 연간 18.55% 성장할 것으로 예측됩니다. MDR이 기업에 지지되고 있는 이유는 기술, 원격 측정, 인간 전문 지식을 융합하여 직원 부담 없이 평균 감지 시간을 단축할 수 있기 때문입니다. MDR 계약의 급증은 위협 인텔리전스 보안 서비스 시장이 성과 기반 딜리버리에 축발을 두는 방법을 보여줍니다. 전문 서비스는 성숙도 평가, 프레임워크 설계, 지속적인 위협 노출 관리의 전개에 필수적인 것은 아닙니다.

구독 피드는 상품 기반을 형성하지만 액터 프로파일 링과 위험 점수가있는 컨텍스트 풍부한 패키지로 진화하고 있습니다. 포티넷은 2025년 1분기에 전년 동기 대비 30.3% 증가한 4억 3,450만 달러의 보안 운영 ARR을 기록해 통합 MDR과 오케스트레이션이 기세를 늘리고 있음을 보여줍니다. 자동화된 봉쇄 워크플로우에 큐레이트된 텔레메트리를 혼합하는 공급업체는 툴의 통합이 진행되고 있는 가운데, 방어 가능한 차별화를 구축하고 있습니다.

위협 인텔리전스 보안 서비스 시장은 배포 형태(클라우드, On-Premise), 서비스 유형(관리형 감지 및 응답, 전문/컨설팅 등), 조직 규모(대기업, 중소기업), 최종 사용자 산업(은행/금융 서비스, 헬스케어 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2025년을 향한 미국의 275억 달러의 사이버 보안 예산에 의해 지원되며 세계 수익의 38%를 차지합니다. 이 예산에는 정보 공유 네트워크를 확장하는 CISA 보조금에 대한 30억 달러가 포함됩니다. 제로 트러스트의 높은 채용률, 벤처 기업의 활발한 자금 조달, 클라우드 네이티브 공급업체 에코시스템이 이 지역의 리더십을 유지하고 있습니다. 연방행정명령 14028호는 정부기관에 위협 인텔리전스를 보안 업무에 통합하도록 강제하고 있으며, 인접한 업계는 공급망 보증 모델을 모방하고 있습니다. 캐나다는 미국의 정보 공개 기준과 조화를 이루고 있으며, 멕시코의 금융 규제 당국은 인시던트 보고서를 핀테크로 확대하고 새로운 수요 벡터를 추가하고 있습니다.

아시아태평양의 CAGR은 18.90%로 세계에서 가장 빠른 성장이 예측되고 있습니다. 중국의 사이버 보안 시장은 정부 프로그램에 의해 국내 보안 관리가 강화되어 2029년까지 236억 6,000만 달러에 달하는 기세입니다. 일본의 전략문서에서는 국내 사이버보안 매출을 3배로 늘리고 국가예산을 50% 증액하고 있으며 업계급 위협 인텔리전스에 대한 의욕이 높아지고 있습니다. 인도에서는 디지털화가 빠르게 진행되고 있습니다. CERT-IN 지침은 특정 사건의 실시간 보고를 의무화하고 서비스 이용을 촉진합니다. 호주에서는 5억 8,600만 달러의 사이버 회복력 강화책이 매니지드 인텔리전스 수요를 지원하고, 각 지역의 통신 사업자는 국경을 넘는 원격 측정 교환에 투자하고 있습니다.

유럽은 NIS2 지침과 각 지역의 데이터 보호 의무화로 꾸준한 성장을 유지하고 있습니다. 독일은 산업 자동화를 방해 행위로부터 보호하기 위해 2025년에 100억 유로를 넘는 사이버 보안 지출을 전망하고 있습니다. 영국은 정보기관에 6억 파운드의 추가 예산을 계상하고, 2035년까지 GDP의 5%를 국가 안보에 충당할 계획으로, 공급업체에게 장기적인 전망이 세워지기 쉬워지고 있습니다. 데이터 주권 요구 사항은 국경 내에서 원격 측정을 처리할 수 있는 지역 보안 운영 센터의 성장을 자극합니다. 따라서 거주지를 고려한 클라우드 패브릭과 다국어 분석가 지원을 제공하는 공급자를 선호합니다.

The threat intelligence security services market size stands at USD 3.27 billion in 2025 and is forecast to reach USD 5.89 billion by 2030, advancing at a 12.47% CAGR over the period.

The expansion reflects a decisive shift from reactive perimeter defense toward continuous threat hunting, exposure management, and predictive analytics. Escalating state-sponsored campaigns, a 65% rise in cloud security incidents, and mandatory breach-notification laws across major jurisdictions are amplifying demand for real-time, contextual threat data. Platform convergence, led by zero-trust and Extended Detection and Response (XDR) rollouts, is further accelerating investment as security teams seek unified visibility and automated response. At the same time, the proliferation of application programming interface attack surfaces and insider risks arising from generative AI code assistants have prompted organizations to reassess risk postures, energizing the threat intelligence security services market.

Nation-state groups such as Volt Typhoon and Salt Typhoon have intensified operations against critical infrastructure, prompting organizations to prioritize tactical intelligence and pre-incident attribution capabilities. The Cybersecurity and Infrastructure Security Agency issued 3,368 pre-ransomware notifications in 2024, underscoring the volume of advanced intrusion attempts. Attacks now go beyond espionage to include destructive pre-positioning, which demands continuous monitoring and specialized hunting. Iranian actors are simultaneously targeting healthcare and financial services, turning threat intelligence into a strategic imperative across sectors. These developments have accelerated spending on managed detection, enriched malware analysis, and contextual attribution services.

Cloud migration has multiplied attack entry points, with organizations operating thousands of APIs across multi-cloud settings. API failures contributed to a majority of cloud breaches reported in 2024, revealing visibility gaps in east-west traffic. Traditional network monitoring lacks context for ephemeral workloads, fuelling adoption of cloud-native threat intelligence that can map dependencies in real time. Microservices architectures further complicate asset inventories, increasing reliance on automated discovery and continuous risk scoring. The outcome is sustained momentum for cloud-delivered analytics engines and exposure management modules tailored to serverless and container environments.

Demand for deep forensics and malware reverse-engineering outpaces supply. Years of training are needed to master nation-state adversary tactics, yet security teams face attrition and wage inflation. The gap is driving consolidation as smaller vendors struggle to retain experts, and clients turn to Managed Detection and Response for turnkey coverage. Providers must now automate routine triage to free scarce specialists for higher-value pursuits, heightening interest in AI-assisted analysis modules.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud deployment already commands 58% of the threat intelligence security services market share. The segment is projected to expand at an 18.20% CAGR through 2030, reinforcing the centrality of cloud-native analytics engines. Elastic compute and distributed storage enable providers to process petabytes of telemetry without customer-side hardware, which is critical as threat intelligence security services market size grows to USD 5.89 billion in 2030. On-premises deployments persist in sovereign cloud and defense contexts that require local data processing, although development roadmaps now prioritize hybrid connectors rather than standalone appliances.

Hybrid adoption is rising among regulated firms that embrace the cloud for scale yet retain select data sets in country for compliance. API-centric attack vectors accentuate cloud resonance since traditional sensors lack context for container traffic. Palo Alto Networks reported AI-centric Annual Recurring Revenue above USD 200 million with 4x year-over-year growth, validating appetite for cloud-delivered machine learning modules. Cloud superiority is therefore entrenched, but vendors must address latency, encryption, and locality factors to accelerate further penetration.

Managed Detection and Response own 56% of the threat intelligence security services market share as of 2024 and are forecast to grow 18.55% annually. Enterprises favour MDR because it fuses technology, telemetry, and human expertise, reducing mean time to detect without staffing burdens. The surge in MDR contracts underlines how the threat intelligence security services market pivots toward outcome-based delivery. Professional services remain vital for maturity assessments, framework design, and Continuous Threat Exposure Management rollouts.

Subscription feeds form a commodity base but are evolving toward context-rich packages with actor profiling and risk scoring. Fortinet posted Security Operations ARR of USD 434.5 million in Q1 2025, up 30.3% year on year, signalling that integrated MDR plus orchestration gains momentum. Vendors blending curated telemetry with automated containment workflows are building defensible differentiation as tool consolidation continues.

Threat Intelligence Security Services Market Segmented by Deployment Mode (Cloud, On-Premises), Service Type (Managed Detection & Response, Professional/Consulting and More), Organization Size (Large Enterprises, Small & Medium Enterprises), End-User Industry (Banking & Financial Services, Healthcare and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America controls 38% of global revenue, supported by the United States' USD 27.5 billion cybersecurity allocation for 2025, which includes USD 3 billion for CISA grants that expand intelligence sharing networks. High adoption of zero-trust, robust venture funding, and an ecosystem of cloud-native vendors sustain regional leadership. Federal Executive Order 14028 compels government agencies to integrate threat intelligence into security operations, and adjacent industries replicate the model for supply-chain assurance. Canada is harmonizing with U.S. disclosure norms, while Mexico's financial regulator extends incident reporting to fintech, adding new demand vectors.

Asia-Pacific is projected to grow at an 18.90% CAGR, the fastest worldwide. China's cybersecurity market is on track to reach USD 23.66 billion by 2029 as government programs enforce in-country security controls. Japan's strategic documents call for tripling domestic cybersecurity sales and boosting national budgets by 50%, which elevates appetite for industry-grade threat intelligence. India continues rapid digitization; its CERT-IN directives oblige real-time reporting for specified incidents, driving service uptake. Australia's AUD 586 million cyber resilience package underpins managed intelligence demand, and regional telecom providers are investing in cross-border telemetry exchanges.

Europe maintains steady growth propelled by the NIS2 directive and local data protection mandates. Germany expects cybersecurity spending beyond €10 billion in 2025 to shield industrial automation from sabotage. The United Kingdom earmarked an extra £600 million for intelligence agencies and plans to devote 5% of GDP to national security by 2035 reinforce long-term visibility for vendors. Data-sovereignty requirements stimulate growth of regional security operations centers capable of processing telemetry within national borders. Providers offering residency-aware cloud fabrics and multilingual analyst support are therefore preferred.