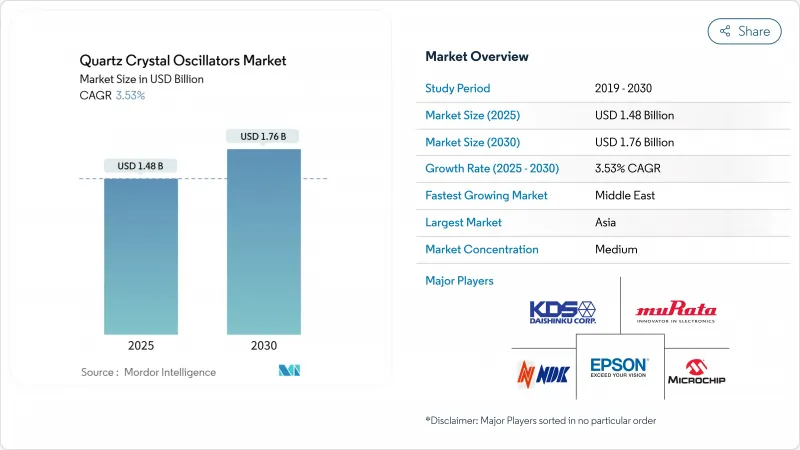

수정발진기 시장의 수익과 예측은 2025년에 14억 8,000만 달러에 이르고, 2030년에는 17억 6,000만 달러에 달할 것으로 예상됩니다.

스마트폰부터 5G 베이스 스테이션, 저궤도 위성에 이르기까지 고정밀 타이밍 솔루션에 대한 수요가 확대됨에 따라 CAGR은 3.53%로 안정적입니다.

크리스탈은 위상 잡음, 전력 소비 및 시동 시간에 라이벌 기술을 능가합니다. 아시아태평양의 반도체 공장 확대, 자동차 전동화 가속, 하이퍼스케일 데이터센터의 400/800G 광 링크로의 전환이 주된 촉매가 되고 있습니다. 동시에 고순도 크리스탈 공급망 충격이나 MEMS 발진기와의 경쟁은 궤도를 완만하게 하는 것, 고정밀 틈새 분야에서 기존 기술을 구축하기에는 이르지 않습니다.

ITU-T의 G.8272.1 등의 사양에서는 -30ns의 제한이 규정되어 있으며, Rakon과 같은 공급업체는 GNSS 손실시에 홀드오버할 수 있는 OCXO의 소형화를 진행하고 있습니다. 밀집된 도시 레이아웃의 각 스몰셀 노드는 현재 고유의 고정밀 소스를 내장하고 있으며, 매크로 전용 배포가 분산 안테나 시스템을 대체할수록 유닛 수요가 증가하고 있습니다. 오실로 쿼츠 OSA 5430과 같은 아키텍처는 5G 타이밍 아키텍처의 미래를 보장하는 광 원자 참조를 통합하여 피코초 수준의 지터 내성이 필수적인 크리스탈과의 연관성을 강화합니다.

레벨 3 자율 주행은 차량 탑재 이더넷의 서브 나노초 윈도우에 맞추어야 하는 센서 퓨전과 실시간 계산 부하를 증가시킵니다. Skyworks와 SiTime은 저지터 오실레이터를 AEC-Q100 및 ISO 26262 표준에 맞추어 20g 이상의 진동 피크를 견디면서 언제나 가동 영역에서 1µW 이하의 전력 예산을 실현합니다. TDK는 전기자동차의 생산량이 27% 증가할 것으로 예측하고, 존 ECU가 분산 아키텍처를 대체할수록 섀시당 타이밍 노드가 병렬로 확장됨을 시사합니다. PCIe로 연결된 중앙 집중식 프로세서는 RMS 위상 잡음이 100fs 이하인 클럭 소스를 요구합니다.

SiTime과 여러 회사의 라이벌은 현재 50,000g의 충격을 견디며 125°C까지 작동하는 프로그래머블 MEMS 클럭을 출시하고 있습니다. SiTime이 2024년에 1억 4,400만 달러의 매출을 기록했으며, 지난 10년간 7배로 증가함에 따라 판매량이 급증하고 비용 중심 설계에 널리 받아들여지고 있음을 보여줍니다. 그러나 0.18ps rms의 위상 노이즈, 3mA공급 전류, 100μs 이하의 기동을 가지는 수정이 사양서의 대부분을 차지해, 고성능인 수정발진기 시장을 유지하고 있습니다.

2024년 수정발진기 시장에서는 SPXO가 36.9%를 차지하고 대중용 전자기기에 널리 보급되고 있음을 반영했습니다. TCXO는 5G 라디오, 인더스트리 4.0 게이트웨이, ADAS 모듈에서 BOM 비용보다 열 안정성을 강조하기 때문에 연간 4.2% 확대될 것으로 예측됩니다. VCXO는 광 인터커넥트의 틈새 시장을 지원하며, 수정발진기 시장 규모 요구 사항은 56Gbps 이상의 위상 동기 루프 정확도와 직접 연결됩니다.

NDK, 엡손, 라콘은 서브 ppb의 안정성이 코어 네트워크에서 에지 노드로 전환되도록 OCXO의 전력 소비를 줄이기 위해 경쟁하고 있습니다. 엡손의 OG7050CAN은 레거시 디바이스보다 85% 소형이면서 56% 낮은 전력을 실현하여 랙 마운트형 베이스밴드 유닛에 OCXO를 침투시키는 길을 보여줍니다. 반면 FCXO 아키텍처는 표준 컷으로 달성할 수 없는 10-14 단기 안정성이 요구되는 양자 컴퓨터의 테스트 베드로 표면화되어 있습니다. 그 결과 수정발진기 시장의 세분화된 성격이 유지됨과 동시에 전문 공급자가 큰 마진을 획득할 수 있게 되었습니다.

스마트폰, 웨어러블 단말, IoT 센서는 자동화된 픽앤플레이스 라인에 대응하는 리플로우 납땜 가능한 부품을 추구하고 있기 때문에 표면 실장 패키지는 2024년 매출의 81.7%를 차지했습니다. 대진공 높이 0.5mm의 SPXO가 체적 효율로 업계의 벤치마크가 되고 있습니다.

스루홀형은 여전히 CAGR 3.7%로 성장을 지속하고, 있는데, 이는 방위항공전자기기나 가혹한 환경하에서 사용되는 기계가 반복되는 열사이클을 견디는 소켓형의 대체품으로 지지되고 있기 때문입니다. 대형 몸체 발진기는 하이 엔드 OCXO에 필수적인 히터 제어 챔버를 갖추고 있으며 좁지 만 수익성있는 부문을 유지합니다. 공급업체의 차별화는 현재 도금 화학 및 무연 납땜성에 달려 있으며, 이는 설계 라이프사이클이 15년이 넘는 자동차 및 철도 신호의 설치 기반을 보호하는 매개변수입니다.

수정발진기 시장 보고서는 회로 유형(단순 패키지 수정발진기(SPXO), 온도 보상형 수정발진기(TCXO) 등), 실장 유형(표면 실장, 기타), 수정 컷(AT 컷, 기타), 최종 사용자(소비자용 전자기기, 통신·네트워크, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

중국, 일본, 한국이 세계 칩의 70% 이상을 생산하고, 일류의 발진기 제조업체를 옹호하고 있기 때문에 아시아태평양은 2024년 매출의 45.6%를 차지했습니다. SEMI는 이 지역의 웨이퍼 스타트가 2025년에 7% 증가할 것으로 예측하고 있으며 테스트 및 계측 벤치 및 리소그래피 스테퍼에서 타이밍 디바이스의 풀스루가 증가하게 됩니다. NDK와 엡손과 같은 일본의 전통적인 공급업체는 현지 석영 광산과 수직으로 통합된 공장을 활용하여 서브 pS 지터 성능의 리더십을 유지하고 있습니다.

북미는 하이퍼스케일 데이터센터 건설과 활기찬 항공우주 부문의 혜택을 누리고 있습니다. RTX는 2024년에 807억 달러의 매출을 기록해 미사일 유도 및 안전한 통신 페이로드에 내방사선성 수정발진기를 지정하는 방어 계획을 지지했습니다. 독일에서는 인더스트리 4.0에 대한 대처가, 프랑스에서는 제조업의 활성화가 거시경제의 감속에도 불구하고 추풍이 되고 있습니다.

중동은 현재 소폭의 슬라이스를 유지하고 있지만, 아랍에미리트(UAE) 및 사우디아라비아의 오퍼레이터가 5G 및 스마트 시티 그리드를 급피치로 진행하고 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 3.9%로 성장을 지속하고, 있습니다. 국가의 다양화는 반도체 조립 프로그램을 추진하고 이산 타이밍 부품을 소비합니다. 라틴아메리카와 아프리카는 4G가 여전히 우세하고 전자 생산이 제한적이기 때문에 보다 광범위한 보급이 지연되고 있지만, 스몰셀 고밀도화와 IoT 농업 조종사는 수정발진기 시장 내 세계적인 수량 성장을 유지하는 수요 증가를 시사합니다.

Quartz crystal oscillators market size revenue reached USD 1.48 billion in 2025 and is forecast to climb to USD 1.76 billion by 2030, reflecting a steady 3.53% CAGR as demand for precise timing solutions spreads from smartphones to 5G base-stations and low-earth-orbit satellites.

The measured growth underscores a maturing yet resilient landscape in which quartz continues to outperform rival technologies on phase-noise, power consumption and start-up time. Expansion of semiconductor fabs in Asia-Pacific, accelerated electrification of vehicles, and migration of hyperscale data-centres to 400/800 G optical links are the principal catalysts. At the same time, supply-chain shocks in high-purity quartz and mounting competition from MEMS oscillators moderate the trajectory yet fail to displace the incumbent technology in high-precision niches.

The shift from 4G frequency-only synchronisation to 5G's time-division-duplex architecture imposes UTC-traceable phase accuracy within +-1.5 µs, compelling operators to deploy ePRTC-grade OCXOs and TCXOs in radio heads and grandmasters.Specifications such as ITU-T G.8272.1 prescribe +-30 ns limits, encouraging vendors like Rakon to miniaturise OCXOs able to holdover during GNSS loss. Each small-cell node in dense urban layouts now embeds its own precision source, multiplying unit demand as macro-only roll-outs give way to distributed antenna systems. Solutions such as Oscilloquartz OSA 5430 integrate optical atomic references to future-proof 5G timing architectures, reinforcing quartz relevance where picosecond-level jitter tolerance is mandatory.

Level-3 autonomy increases sensor fusion and real-time compute loads that must align to sub-ns windows over automotive Ethernet. Skyworks and SiTime have qualified low-jitter oscillators to AEC-Q100 and ISO 26262 standards, delivering power budgets below 1 µW for always-on domains while surviving vibration peaks above 20 g. TDK forecasts 27% electric-vehicle production growth, implying a parallel expansion in timing nodes per chassis as zonal ECUs replace distributed architectures. Centralised processors linked by PCIe demand clock sources with RMS phase-noise under 100 fs, a threshold still favouring quartz in high-reliability settings.

SiTime and a handful of rivals now ship programmable MEMS clocks that withstand 50,000 g shocks and operate up to 125 °C, benefits that resonate in smart-phones, action cameras and industrial IoT . Unit absorption escalated after SiTime posted USD 144 million revenue in 2024, up seven-fold in a decade, indicating broad acceptance in cost-sensitive designs. Yet quartz retains supremacy where 0.18 ps rms phase-noise, 3 mA supply current and sub-100 µs start-up dominate the specification sheet, sustaining the Quartz crystal oscillators market at the high-performance end.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SPXOs held 36.9% of the Quartz crystal oscillators market in 2024, reflecting their ubiquity in mass-market electronics. TCXOs, while accounting for a smaller slice today, are projected to expand 4.2% annually as 5G radios, Industry 4.0 gateways and ADAS modules place thermal-stability above BOM cost. VCXOs uphold a niche in optical interconnects where the Quartz crystal oscillators market size requirement ties directly to phase-locked loop accuracy at 56 Gbps and above.

NDK, Epson and Rakon race to shrink power draw in OCXOs so that sub-ppb stability migrates from core networks to edge nodes. Epson's OG7050CAN, 85% smaller than legacy devices yet delivering 56% lower power, signals a pathway for OCXO penetration into rack-mounted base-band units . Meanwhile, FCXO architectures surface in quantum-computing testbeds that demand 10-14 short-term stability unattainable by standard cuts. The resulting mix preserves the fragmented character of the Quartz crystal oscillators market while enabling specialist suppliers to capture outsized margins.

Surface-mount packages accounted for 81.7% revenue in 2024 as smartphones, wearables and IoT sensors pursue reflow-solderable components compatible with automated pick-and-place lines. The Quartz crystal oscillators market continues shifting toward chip-scale and µ-package footprints, with Daishinku's 0.5 mm-high SPXOs setting industry benchmarks in volumetric efficiency.

Through-hole formats still chart a 3.7% CAGR because defense avionics and harsh-environment machinery favour socketed replacements that survive repeated thermal cycling. Large-body oscillators also host heater-regulated chambers indispensable for high-end OCXOs, sustaining a profitable if narrow segment. Supplier differentiation now hinges on plating chemistry and lead-free solderability, parameters that protect installed bases across automotive and rail signalling where design lifecycles exceed 15 years.

The Quartz Crystal Oscillator Market Report is Segmented Into Circuit Type (Simple Packaged Crystal Oscillator (SPXO), Temperature-Compensated Crystal Oscillator (TCXO), and More), Mounting Type (Surface Mount, and More), Crystal Cut (AT-Cut and More), End-User (Consumer Electronics, Telecom and Networking and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 45.6% of 2024 revenue as China, Japan and South Korea manufactured more than 70% of global chips and housed tier-one oscillator makers. SEMI projects wafer starts in the region to climb 7% in 2025, translating into incremental pull-through for timing devices across test-and-measurement benches and lithography steppers. Japan's heritage suppliers such as NDK and Epson exploit local quartz mines and vertically integrated fabs to retain leadership in sub-pS jitter performance.

North America benefits from hyperscale data-centre build-outs and a vibrant aerospace sector. RTX recorded USD 80.7 billion sales in 2024, underlining defense programmes that specify rad-hard quartz oscillators in missile guidance and secure communication payloads. Europe advances industrial-automation and electric-vehicle ecosystems that favour TCXO deployments for deterministic networking; Germany's Industry 4.0 initiatives and France's manufacturing revitalisation create tailwinds despite macroeconomic slowdowns.

The Middle East, while currently holding a modest slice, registers the fastest 3.9% CAGR to 2030 as operators in the United Arab Emirates and Saudi Arabia fast-track 5G and smart-city grids. National diversification drives semiconductor assembly programmes that in turn consume discrete timing parts. Latin America and Africa lag broader adoption because 4G still predominates and electronics production remains limited, yet small-cell densification and IoT agriculture pilots hint at incremental demand that sustains global volume growth within the Quartz crystal oscillators market.