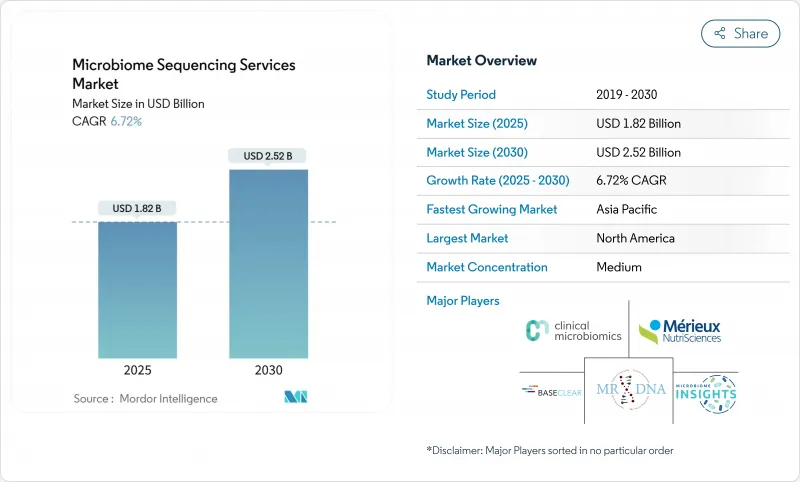

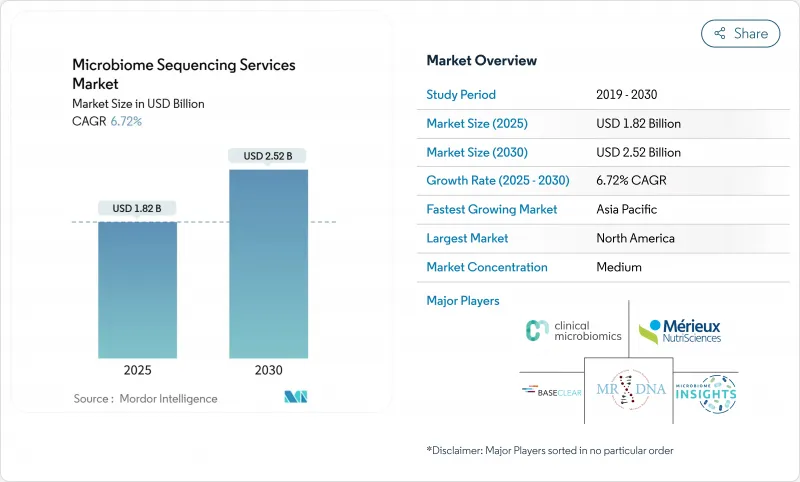

마이크로바이옴 시퀀싱 서비스 시장은 2025년에 18억 2,000만 달러로 평가되고, 2030년에는 25억 2,000만 달러로 확대될 것으로 예측되며, 기간 동안 6.72%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

임상시험, 치료법 발견, 정밀의료 워크플로우에 있어서 마이크로바이옴·프로파일링의 일관된 채용이 이 확대를 지지하는 한편, 차세대 시퀀싱(NGS) 비용은 꾸준히 저하되고 있어, 학술·상업 유저 양쪽의 액세스가 더욱 넓어지고 있습니다. 라이브 바이오테라피 제품, 동반진단제, 국립 바이오뱅크 개념에 대한 투자의 기세는 샘플 양 증가와 정기적인 분석 계약에 직접 연결되어 있습니다. 경쟁사와의 차별화는 순수한 시퀀싱 능력에서 통합 바이오인포매틱스, 규제 등급 품질 시스템, 멀티오믹 데이터 분석으로 이동하고 있습니다. 동시에, 데이터 주권에 관한 규칙과 멀티오믹스 바이오인포마티션의 지속적인 부족은 당분간 시장 성장의 가능성을 약화시키고, 대기업 공급자가 컴플라이언스 인프라와 자동화에 적극적으로 투자하도록 촉구하고 있습니다.

제약 개발 회사는 복잡한 마이크로바이옴 연구 작업 스트림을 CRO로 이전합니다. CRO는 사내에 적은 전문적인 샘플링, 생착, 바이오인포매틱스의 전문 지식을 보유하고 있기 때문입니다. 미국 FDA가 REBYOTA와 VOWST를 승인함으로써 약사 규제의 패스웨이가 확립되어 후기 파이프라인이 확대되었습니다. 스폰서간에 프로젝트를 풀어 스케일 메리트를 활용할 수 있는 CRO는 2030년까지의 CAGR이 7.55%로 현재 가장 빠르게 성장하고 있는 최종 사용자 집단입니다. 샘플 물류, 습식 실험실 워크플로우, 제출 준비된 보고서 등 통합 서비스를 제공하는 CRO는 속도와 재현성이 물량을 절감하는 비용이 많이 드는 2상 및 3상 시험에서 특히 매력적입니다. 주요 CRO와 시퀀싱 기술 벤더의 전략적 제휴는 시장 도달범위를 확대하고 아웃소싱 사이클을 강화함으로써 마이크로바이옴 시퀀싱 서비스 시장 전체의 CAGR을 1.8% 밀어 올립니다.

인간 유전체의 시퀀싱 비용은 2001년 1억 달러에서 2023년 500달러 가까이 떨어졌으며 전문 연구 개발 환경에서 10달러 이하의 예측도 가능해졌습니다. 이러한 감소로 샷건과 긴 리드의 메타유전체 연구가 민주화되었고, 중소 바이오 기술 기업과 대규모 학술 컨소시엄도 마찬가지로 마이크로바이옴 시퀀싱 서비스 시장에 접근할 수 있게 되었습니다. 그러나 원시 시퀀싱가 상품화되고 마진이 엄격해짐에 따라 공급자는 고급 분석, 품질 관리 및 엔드 투 엔드 워크플로우 통합을 통한 차별화를 촉구하고 있습니다. 멀티오믹스 해석과 임상 등급 리포팅에 중점을 둔 공급자는 프리미엄 가격을 유지하는 반면 순수한 'Gb 당' 공급자는 가격 압력에 노출됩니다. 그 결과 비용 디플레이션은 시장의 CAGR에 1.5% 포인트 플러스의 영향을 미치지만, 저비용 생성과 부가가치 해석을 결합한 벤더만이 상승을 완전히 포착할 수 있을 것으로 보입니다.

개인과 관련된 미생물 유전 물질이 생물 의학 개인 정보 보호법의 대상이되는 개인 데이터에 해당하는지 여부는 관할 지역에 따라 다릅니다. 중국의 인간 유전 자원에 관한 규칙은 국내에서의 처리를 요구하고 있지만, 나고야 의정서는 국경을 넘어 출소할 가능성이 있는 미생물에 대한 액세스와 이익 공유를 확대하고 있습니다. 미국 사법부는 마이크로바이옴 데이터를 관리 카테고리로 분류할 것을 제안하고 있으며 잠재적으로 적대국과의 클라우드 처리를 제한할 수 있습니다. 각각의 괴리는 로컬 서버부터 섬세한 동의서에 이르기까지 중소규모의 프로바이더에게 불균형한 부담을 강하게 하는 컴플라이언스 오버헤드를 부과합니다. 국경을 넘어서는 임상시험에서는 샘플이 여러 규제당국의 규제를 통과하기 때문에 지연과 법적 비용 증가가 발생하고, 마이크로바이옴 시퀀싱 서비스 시장의 CAGR은 추정 1.2포인트 떨어집니다.

샷건 메타유전체 시퀀싱은 2024년 마이크로바이옴 시퀀싱 서비스 시장 점유율의 43.43%를 차지하여 균주 수준 및 기능적 특성 분석의 주요 기법으로서의 지위를 명확히 했습니다. 이 접근법은 내성 유전자, 병원성 인자 및 대사 경로를 밝히는 엄청난 데이터 세트를 생성하므로 신약 개발 스크리닝과 바이오 마커 식별을 지원할 수 있습니다. 지속적인 비용 절감과 자동화로 납기가 개선되고 탐색 및 규제 프로젝트 모두에서 산탄총의 매력이 증가하고 있습니다. 그러나, 표적 16S rRNA 시퀀싱은 분류학적 폭이 있으면 충분한 비용-중심 진단 및 대규모 역학적 스크리닝에서 스캐폴드를 굳힙니다. 따라서 공급자가 첫 번째 16S 스크리닝에 전체 샷건 프로파일링을 중첩하는 서비스 번들로 성장을 실현합니다.

모든 유전체 및 메타트란스크립트 시퀀싱은 치료 설계 및 약사 신청에서 기능성 오믹스 수요에 견인되며 CAGR 7.67%를 나타낼 것으로 예상됩니다. 스폰서가 분류학적 지식에 그치지 않고 메커니즘적인 지견을 요구하는 가운데, DNA/RNA와 대사물을 조합한 워크플로우를 제공하는 프로바이더는 보다 이익률이 높은 계약을 획득하고 있습니다. 표적 패널 순서는 항균제 저항성 감시와 같은 특별한 필요를 수용하고 공간 마이크로바이오믹스와 같은 다른 혁신적인 서비스는 수술 종양학 및 피부과학에서 상승합니다. 이러한 동향은 마이크로바이옴 시퀀싱 서비스 시장의 꾸준한 다양화를 지원하며, 공급자는 단일 양식으로 인한 이익률의 감소를 확실히 회피할 수 있습니다.

Sequencing By Synthesis는 2024년 매출의 41.21%를 차지하며 대규모 임상 코호트에 적합한 높은 정확도와 처리량을 제공하는 확립된 화학의 혜택을 받았습니다. 이 플랫폼을 활용하는 공급자는 성숙한 시약 공급망과 소프트웨어 에코시스템을 즐길 수 있으며, 합성은 규제 대상 업무의 사실상 표준이 되고 있습니다. 하지만 리가이션 기반 시퀀싱이 CAGR 가장 빠른 7.56%를 나타낼 것으로 예상되는 이유는 주로 그 화학물질이 대변이나 환경 샘플에서 많이 보이는 단편화된 DNA나 손상된 DNA를 처리하기 때문입니다. 라이게이션 기반 플랫폼이 속도와 출력을 개선함에 따라 공급자는 높은 정확도의 요구에 대응하는 합성과 보다 어려운 매트릭스에 대응하는 라이게이션을 결합한 하이브리드 플릿을 채용하고 있습니다.

나노포어 시퀀싱은 병원체의 신속한 검출 및 구조 변형 분석을 가능하게 하는 실시간 긴 리드 기능으로 주목받고 있습니다. 정확도의 장애물에 여전히 직면하고 있는 것, 반복적인 포어 디자인과 머신러닝에 의한 염기 콜에 의해 그 차이는 줄어들고 있습니다. 다른 분야에서는 1분자법이나 반도체 검출기가 진보를 계속하고 있지만, 마이크로바이옴에의 응용은 틈새에 그치고 있습니다. 공급업체는 경쟁이 치열해지는 시장에서 고객 유지를 유지하기 위해 각 샘플 유형에 가장 적합한 플랫폼을 선택하고 멀티 기술 실험실을 운영합니다.

북미는 2024년에 42.87%의 매출 리드를 유지해 FDA가 승인한 규제 패스웨이, 밀집한 제약 클러스터, 오랜 NIH의 자금원에 지지를 받았습니다. 바이오 치료제의 승인, 벤더와의 제휴, 벤처 캐피탈의 유입은 비용 압력이 전문 CRO 허브에 아웃소싱을 촉진하는 중에도 샘플 양을 많이 유지하기 위해 집계되어 있습니다. 미생물학적 데이터를 기밀 정보로 분류하는 미국 규정은 해외 분석에 제약을 줄 수 있지만, 국내 공급자가 안전한 클라우드 환경과 FedRAMP 준수 파이프라인에 투자하도록 촉구하고 현지 능력을 더욱 강화하고 있습니다.

유럽에서는 범 EU 규제의 조화와 국가 수준의 바이오뱅크 프로그램이 결합되어 학술, 임상, 상업 분야에서 다양한 수요가 유지되고 있습니다. 인간 유래 물질에 대한 새로운 규제에는 인간 마이크로 바이옴도 포함됨이 명시되어 있으며 ISO20387 바이오 뱅크 인증을 취득한 공급자에게는 컴플라이언스 업무와 시장 기회가 모두 창출됩니다. 이 지역의 전통인 엄격한 데이터 보호 프레임워크는 GDPR(EU 개인정보보호규정)을 준수하는 시설과 견고한 동의 관리 시스템을 갖춘 공급업체에게 유익하며 지역 내 분석의 인센티브가 되었습니다.

아시아태평양은 CAGR 7.76%로 가장 빠른 성장을 보이고 있지만, 이는 중국의 대규모 유전체학 투자와 일본의 구조화된 국가 마이크로바이옴 데이터베이스를 반영하고 있습니다. 데이터 주권에 대한 제약이 국경을 넘어 시퀀싱을 복잡하게 하고 있지만, BGI, MGI, 지역 CRO에 의한 국내 능력에 대한 투자가 프로젝트의 기세를 강하게 유지하고 있습니다. 한국, 싱가포르, 호주 정부도 정밀의료 예산을 확대하고 지역 시퀀싱 센터로 작업을 돌리는 종단 마이크로 바이옴 프로젝트를 맡고 있습니다. 공급자는 이질적인 규정을 극복해야 하지만 현지화 전략의 성공으로 인해 충분한 서비스를 받지 못한 대규모 샘플 풀이 해제됩니다.

중동, 아프리카, 남미는 아직 막 시작되었지만 유망한 지역입니다. 시퀀싱의 인프라와 자금이 제한되어 있기 때문에 곧바로 도입할 수는 없지만, 시험적인 국가 마이크로바이옴 이니셔티브와 테크놀로지 파크에 대한 투자는 관심의 고조를 시사하고 있습니다. 제공업체가 현지 대학 및 공중보건기구와 제휴함으로써 조기에 발판을 구축하고 미래의 규제 기준을 형성할 수 있습니다. 이 지역은 세계의 마이크로바이옴 시퀀싱 서비스 시장을 다양화하고 장기적인 지속적인 성장을 향한 수량 증가에 기여하고 있습니다.

The microbiome sequencing services market is valued at USD 1.82 billion in 2025 and is forecast to advance to USD 2.52 billion by 2030, registering a 6.72% CAGR throughout the period.

Consistent adoption of microbiome profiling in clinical trials, therapeutic discovery, and precision-medicine workflows underpins this expansion, while steadily falling next-generation sequencing (NGS) costs further widen access for both academic and commercial users . Investment momentum around live-biotherapeutic products, companion diagnostics, and national biobank initiatives is translating directly into higher sample volumes and recurring analytical contracts. Competitive differentiation is shifting from pure sequencing capacity toward integrated bioinformatics, regulatory-grade quality systems, and multi-omic data interpretation. At the same time, data-sovereignty rules and a persistent shortage of multi-omic bioinformaticians moderate the market's growth potential in the near term, prompting larger providers to invest aggressively in compliance infrastructure and automation.

Pharmaceutical developers are transferring complex microbiome workstreams to contract research organizations because CROs retain specialized sampling, engraftment, and bioinformatic expertise that remains scarce in-house. The U.S. FDA's approvals of REBYOTA and VOWST validated regulatory pathways and unlocked bigger late-phase pipelines, encouraging further outsourcing to firms that can compress timelines and manage protocol standardization. CROs, able to pool projects across sponsors and leverage economies of scale, now represent the fastest-rising end-user cohort at a 7.55% CAGR to 2030. Their integrated offerings-spanning sample logistics, wet-lab workflows, and submissions-ready reporting-are particularly attractive during costly Phase 2 and Phase 3 studies, where speed and reproducibility translate into material savings . Strategic alliances between big CROs and sequencing technology vendors also amplify market reach, reinforcing the outsourcing cycle that underpins a +1.8% boost to the overall microbiome sequencing services market CAGR.

The cost of sequencing a human genome has collapsed from USD 100 million in 2001 to near-USD 500 by 2023, with sub-USD 10 projections now credible in specialized R&D environments . Such decline democratizes shotgun and long-read metagenomic studies, making the microbiome sequencing services market accessible to smaller biotechnology firms and large academic consortia alike. Yet as raw sequencing becomes commoditized and margins tighten, providers are compelled to differentiate via advanced analytics, quality management, and end-to-end workflow integration. Those focusing on multi-omic interpretation and clinical-grade reporting sustain premium pricing, whereas pure "per-Gb" providers encounter mounting price pressure. Consequently, cost deflation contributes a positive 1.5 percentage-point effect on the market CAGR, but only vendors that couple low-cost generation with value-added interpretation will fully capture the upside.

Jurisdictions differ on whether microbial genetic material associated with a person constitutes personal data subject to biomedical privacy laws. China's human-genetic resource rules demand in-country processing, while the Nagoya Protocol extends access-and-benefit-sharing to microorganisms whose provenance may span borders. The U.S. Department of Justice has proposed labeling microbiomic data as a controlled category, potentially limiting cloud processing with perceived-adversary nations. Each divergence imposes compliance overhead-from local servers to granular consent forms-that disproportionately burdens small and mid-size providers. Cross-border clinical trials, where samples traverse multiple regulatory regimes, now incur delays and incremental legal costs that subtract an estimated 1.2 percentage points from the microbiome sequencing services market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Shotgun metagenomic sequencing held 43.43% of the microbiome sequencing services market share in 2024, underscoring its status as the primary method for strain-level and functional characterization. The approach generates expansive datasets that reveal resistance genes, virulence factors, and metabolic pathways, thereby supporting drug-discovery screens and biomarker identification. Continued cost declines and automation improve turnaround times, reinforcing shotgun's appeal for both exploratory and regulated projects. Yet targeted 16S rRNA sequencing retains a foothold in cost-sensitive diagnostics and large epidemiological screens where taxonomic breadth suffices. Growth therefore materializes from service bundling, where providers layer full shotgun profiling onto initial 16S screens.

Whole-genome and metatranscriptomic sequencing is projected to rise at a 7.67% CAGR, driven by functional-omics demand in therapeutic design and regulatory submissions. As sponsors seek mechanistic insight beyond taxonomy, providers offering combined DNA/RNA and metabolite workflows capture higher-margin engagements. Targeted panel sequencing serves specialized needs such as antimicrobial-resistance surveillance, while other innovative services like spatial microbiomics emerge in surgical oncology and dermatology. Cumulatively, these trends support steady diversification of the microbiome sequencing services market, ensuring providers hedge against any single modality's margin erosion.

Sequencing-by-synthesis accounted for 41.21% revenue in 2024, benefiting from established chemistry that delivers high accuracy and throughput suitable for large clinical cohorts. Providers leveraging this platform enjoy mature reagent supply chains and software ecosystems, making synthesis a de-facto standard for regulated work. Nonetheless, sequencing-by-ligation is expected to record the fastest 7.56% CAGR, mainly because its chemistry handles fragmented or damaged DNA prevalent in fecal and environmental samples. As ligation-based platforms improve speed and output, providers are adopting hybrid fleets that pair synthesis for high-accuracy needs with ligation for more challenging matrices.

Nanopore sequencing gains mindshare for its real-time long-read capability, enabling rapid pathogen detection and structural-variant analysis. While still facing accuracy hurdles, iterative pore designs and machine-learning base-calling are narrowing the gap. Elsewhere, single-molecule methods and semiconductor detectors continue to advance, though their microbiome applications remain niche. Providers consequently operate multi-technology laboratories, selecting the optimal platform per sample type to sustain client retention amid an increasingly competitive microbiome sequencing services market.

The Microbiome Sequencing Services Market is Segmented by Sequencing Service Type (16S RRNA Gene Sequencing, and More), Technology (Sequencing by Ligation, and More), Application (Gastrointestinal Diseases, Infectious Diseases, and More), End User (Academic & Research Institutes and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America sustained its 42.87% revenue lead in 2024, anchored by FDA-recognized regulatory pathways, dense pharmaceutical clusters, and long-standing NIH funding streams. Live-biotherapeutic approvals, vendor collaborations, and venture-capital inflows all converge to keep sample volumes high, even as cost pressures encourage outsourcing to specialized CRO hubs. Proposed U.S. rules classifying microbiomic data as sensitive may constrain offshore analytics but are also prompting domestic providers to invest in secure cloud environments and FedRAMP-aligned pipelines, further entrenching local capacity.

Europe combines pan-EU regulatory harmonization with national-level biobank programs, sustaining diversified demand across academic, clinical, and commercial settings. New regulations on substances of human origin, which expressly include human microbiomes, create both compliance work and market opportunities for providers equipped with ISO 20387 biobank certification. The region's tradition of rigorous data-protection frameworks incentivizes in-region analysis, benefiting providers with GDPR-compliant facilities and robust consent-management systems.

Asia-Pacific offers the fastest growth at 7.76% CAGR, reflecting China's large-scale genomics investments and Japan's structured national microbiome databases. Although data-sovereignty constraints complicate cross-border sequencing, domestic capacity investments by BGI, MGI, and local CROs keep project momentum strong. Governments in South Korea, Singapore, and Australia also expand precision-medicine budgets, underwriting longitudinal microbiome projects that funnel work to regional sequencing centers. Providers must navigate heterogeneous regulations, but successful localization strategies unlock large, under-served sample pools.

The Middle East, Africa, and South America present nascent yet promising landscapes. Limited sequencing infrastructure and funding hamper immediate uptake; however, pilot national microbiome initiatives and technology park investments suggest growing interest. Providers partnering with local universities and public-health agencies can establish early footholds and shape future regulatory standards. Collectively, these geographies contribute incremental volumes that diversify the global microbiome sequencing services market and position it for sustained long-term growth.