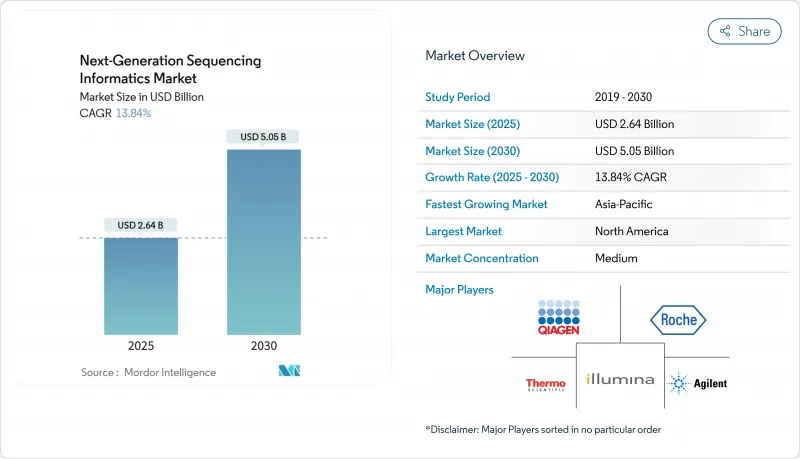

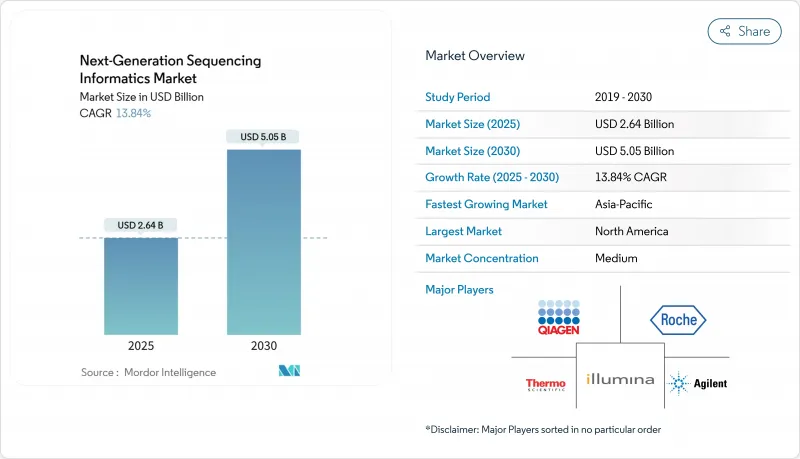

차세대 시퀀싱 인포매틱스 시장 규모는 2025년에 26억 4,000만 달러에 이르고, CAGR 13.84%를 나타내 2030년에는 50억 5,000만 달러에 달할 것으로 예상되고 있습니다.

시퀀싱 비용은 급속히 떨어지고 현재는 샘플당 USD 100의 범위에 있으며 해석해야 할 유전체 데이터의 양이 확대되고 있습니다. 클라우드 및 하이브리드 컴퓨팅 모델은 이미 매년 480 페타베이스를 넘는 원시 출력을 처리하며, 이는 총 50만 유전체에 해당하는 양입니다. Illumina DRAGEN과 NVIDIA Clara와 같은 소프트웨어에 내장된 인공지능 파이프라인은 변형 호출의 정확성을 향상시키면서 분석 실행 시간을 2자리 단축하고 있으며, 이 조합이 종양학, 희귀질환 진단, 집단 건강 프로그램에서의 임상 채용을 가속화하고 있습니다. AI/ML 대응 의료기기에 관한 FDA의 2025년 3월의 지침에 나타낸 바와 같이, 규제의 명확화가 진행됨으로써 상업화 리스크가 경감되고, 차세대 시퀀싱 인포매틱스 시장에의 새로운 툴의 진입이 가속될 것으로 예측됩니다.

암 치료 프로그램은 현재 환자를 표적 요법에 적합시키는 종합적인 패널에 의존하고 있으며, 이 변화가 정밀의료 수익을 2030년까지 연평균 복합 성장률(CAGR) 16.4%를 나타낼 전망입니다. 프레드릭 헬스는 제노몬콜로지 플랫폼을 Expanse Genomics에 통합하여 96명의 환자를 치료하고 6개월 만에 28배의 임상시험을 소개했습니다. 희귀질환 진단은 긴 리드 시퀀싱의 혜택을 받았으며, Azenta의 임상적으로 검증된 테스트는 대부분의 짧은 리드 워크플로우가 놓치는 구조 돌연변이를 발견했습니다. 학술 컨소시엄도 규모를 확대하고 있습니다. Alliance for Genomic Discovery는 25만 건의 전체 유전체을 완료했으며, 의약품 타겟팅을 위한 훈련 세트를 확대했습니다. 이와 같은 프로그램이 확대됨에 따라 병원과 바이오파마는 복잡한 데이터세트를 침대 측의 의사결정으로 변환하는 인포매틱스 플랫폼을 요구하고 있으며 차세대 시퀀싱 인포매틱스 시장 전체에서 리커런트 리비뉴 모델을 강화하고 있습니다.

Ultima Genomics와 Roche SBX 플랫폼은 각각 샘플당 비용을 100달러로 끌어올리고 처리량을 시간당 730X 유전체까지 늘립니다. 진입 비용이 낮아 집단 규모의 프로젝트가 활성화되고 싱가포르의 국가 정밀의료 로드맵과 인도의 GenomeIndia의 노력이 수만 개의 새로운 유전체을 위탁하게 되었습니다. 일루미나의 MiSeq i100 시스템은 콜드체인 물류가 없는 실험실용으로 개발된 것으로, 신흥국에서의 도입이 확대되고 있습니다. 시퀀서의 자본 집약도가 떨어짐에 따라 리드 생성보다 데이터 분석 능력이 주요 병목 현상이 되고 있으며 차세대 시퀀싱 인포매틱스 시장의 소프트웨어 구독 및 관리 서비스로 예산 배분이 이동하고 있습니다.

미국 사법부는 현재 지정된 '우려 국가'로의 유전체의 대량 수출을 제한하고 있으며, 2025년 10월 이후 기업에 기술적 안전 가드를 설치하고 연차 감사를 제출하도록 의무화하고 있습니다. 유럽의 GDPR(EU 개인정보보호규정)은 이미 2차 이용을 위한 명시적인 동의를 의무화하고 있으며, APAC의 일부 국가들은 다기능 연구를 복잡하게 하는 데이터 현지화 조항을 도입하고 있습니다. 따라서 제공업체는 지역별로 클라우드를 구축하거나 협력 학습 모델을 추구해야 합니다. 이러한 조치는 컴플라이언스 오버헤드를 두 자리로 부풀려 차세대 시퀀싱 인포매틱스 시장의 배포주기를 지연시킬 수 있습니다.

NGS 인포매틱스 소프트웨어는 2024년 차세대 시퀀싱 인포매틱스 시장 점유율의 58.12%를 유지하며 대부분의 1차 및 3차 워크플로우를 지원했습니다. 커스텀 플러그인 생태계, 시맨틱 검색 모듈, AI 지원 큐레이션 엔진은 정적 변형 파일을 몇 분 안에 대화형 임상 보고서로 변환합니다. 클라우드 네이티브 플랫폼은 현재는 소규모이지만 CAGR 15.8%를 나타내 있으며, 워크플로우 관리, 컴플라이언스 대시보드, 종량 과금의 계산을 통합 작업 공간에 번들해, 사내의 바이오인포매틱스 스탭이 한정되어 있는 검사실에 어필하고 있습니다.

서비스 제공업체(관리 분석 사이트에서 맞춤형 파이프라인 개발자까지)는 내부에 전문가가 없는 검사 기관에 필수적인 존재로 남아 있습니다. Clinical and Laboratory Standards Institute(임상 검사 표준 협회)의 구조화된 워크시트는 현재 밸리데이션의 지침이 되고 있지만, 많은 병원 실험실은 아직도 3차 해석 작업을 외주하고 있습니다. 플랫폼이 드래그 앤 드롭 인터페이스와 컨테이너 오케스트레이션을 통합함에 따라 기존의 사일로가 더욱 침식되어 시장 세분화 시장의 대응 가능한 전체 부문이 확대되고 있습니다.

2024년 차세대 시퀀싱 인포매틱스 시장의 64.21%는 클라우드 설치가 차지했으며, 자본 지출 없이 수만 CPU 아워를 스핀업시킬 필요성에 몰두했습니다. Google Cloud와 같은 공급업체는 페타바이트 규모의 객체 저장소와 통합 AI 모델 허브를 갖춘 턴키 게노믹 워크벤치를 제공하여 멀티오믹스 쿼리의 평균 응답 시간을 단축합니다.

On-Premise 클러스터는 데이터가 방화벽을 떠날 수 없는 곳에 존재하지만, 장비의 감가상각이 꾸준히 진행되고 에너지 비용이 상승하고 있기 때문에 하이브리드 설정으로의 전환이 진행되고 있습니다. 하이브리드 모델은 원시 읽기 데이터를 위한 사내 보안 스토리지와 클라우드 기반 2차 분석을 결합하여 탄력성을 유지하면서 새로운 주권 관련 법규를 준수할 수 있습니다. 이러한 구성은 2030년까지 연평균 복합 성장률(CAGR)이 15.41%를 나타낼 것으로 예상되며, 배포 솔루션의 차세대 시퀀싱 인포매틱스 시장 규모는 세계적으로 확대됩니다.

북미는 2024년 매출의 42.12%를 차지하며, 풍부한 연구 예산, 성숙한 지급자의 틀, 임상 유전체학에서 적응형 AI를 장려하는 FDA의 자세에 지지를 받았습니다. 엔비비아, IQVIA, 메이요 클리닉은 페타바이트급 멀티모달 환자 데이터를 분석하는 기초모델을 공동으로 훈련하여 임상시험의 매칭을 가속화하고 있습니다. 한편 벤더는 구조화된 체세포 돌연변이의 결과를 Epic의 Genomics 모듈에 직접 피드하는 최초의 실험실이 되어 3,000개 이상의 시설에서 국내 분석 벤더에 크게 의존하는 임상 워크플로우를 확고히 하고 있습니다.

아시아태평양은 싱가포르의 10년간 정밀의료 로드맵, 호주 PrOSPeCT 암 프로그램, 한국의 K-MASTER 이니셔티브에 힘입어 2030년까지 연률 14.51%를 나타낼 것으로 예상되고 있으며, 각각 수만 유전체의 시퀀싱을 실시했습니다. 인도의 위탁 연구 부문은 10.75%로 성장하고 있으며, 장치의 도입을 보완하고 있습니다. 일루미나의 MiSeq i100은 콜드체인 선적이 부족한 실험실을 정면으로 겨냥하여 Tier 2 도시에서 지역화된 워크플로우를 가능하게 합니다. 이러한 움직임은 총체로서 차세대 시퀀싱 인포매틱스 시장 규모에서 이 지역의 슬라이스를 확대하고 주권 데이터법을 존중한 클라우드 네이티브 콜라보레이션의 기반을 구축하는 것입니다.

유럽은 Horizon의 자금 지원과 2025년부터 병원체 감시에 전체 유전체 시퀀싱을 채택할 것을 공중 위생 연구소에 의무화하는 유럽 위원회의 새로운 규제를 배경으로 확고한 발판을 유지하고 있습니다. 일루미나와 Sequentia Biotech와 같은 파트너십은 식품 안전의 트랜스레이셔널 섭취를 보여줍니다. 중동, 아프리카와 남미는 아직 개발 도상이지만 유망합니다. Quad Cancer Moonshot과 같은 이니셔티브는 유전체 인프라를 주입하고 차세대 시퀀싱 인포매틱스 시장 전체에서 프론티어 시장의 성장을 목표로 하는 벤더의 조기 발판을 구축합니다.

The next-generation sequencing informatics market size touched USD 2.64 billion in 2025 and, on the strength of a 13.84% CAGR, is forecast to reach USD 5.05 billion by 2030.

Rapid declines in sequencing costs, now in the USD 100-per-sample range, are expanding the volume of genomic data that must be interpreted, which in turn is stimulating fresh demand for scalable analytics solutions across the next-generation sequencing informatics market. Cloud and hybrid compute models already handle more than 480 petabases of raw output each year, a volume equivalent to 5 million whole genomes. Artificial-intelligence pipelines embedded in software such as Illumina DRAGEN and NVIDIA Clara are shortening analysis run-times by double-digit percentages while improving variant-calling accuracy, a combination that is accelerating clinical adoption in oncology, rare-disease diagnostics and population health programs. Greater regulatory clarity-illustrated by the FDA's March 2025 guidance on AI/ML-enabled medical devices-reduces commercialization risk and is expected to speed the entry of new tools into the next-generation sequencing informatics market.

Oncology programs now rely on comprehensive panels that match patients to targeted therapies, a shift that is propelling precision-medicine revenues at a 16.4% CAGR through 2030. In Frederick Health, embedding GenomOncology's platform inside Expanse Genomics triggered therapy adjustments for 96 patients and multiplied clinical-trial referrals by 28-fold within six months. Rare-disease diagnostics are benefiting from long-read sequencing, and Azenta's clinically validated test is uncovering structural variants most short-read workflows miss. Academic consortia are also scaling: the Alliance for Genomic Discovery has completed 250,000 whole genomes, enlarging training sets for drug-target identification. As these programs expand, hospitals and biopharma alike demand informatics platforms that translate complex datasets into bedside decisions, reinforcing recurrent-revenue models across the next-generation sequencing informatics market.

Platforms from Ultima Genomics and Roche SBX are pushing per-sample costs toward USD 100 and raising throughput to seven 30X genomes per hour, respectively. Lower entry costs have unlocked population-scale projects, leading Singapore's national precision-medicine roadmap and India's GenomeIndia effort to commission tens of thousands of new genomes. Illumina MiSeq i100 systems, tailored for laboratories that lack cold-chain logistics, are widening uptake in emerging economies. As sequencing capital intensity wanes, data-analysis capacity rather than read generation is becoming the primary bottleneck, shifting budget allocations toward software subscriptions and managed services inside the next-generation sequencing informatics market.

The U.S. Department of Justice now restricts bulk genomic exports to designated "countries of concern," compelling enterprises to install technical safeguards and submit annual audits starting October 2025. Europe's GDPR already mandates explicit consent for secondary use, and several APAC nations have introduced data-localization clauses that complicate multi-center studies. Providers must therefore build region-segregated clouds or pursue federated-learning models, steps that inflate compliance overheads by double digits and may slow deployment cycles inside the next-generation sequencing informatics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

NGS informatics software maintained 58.12% of next-generation sequencing informatics market share in 2024 and anchors most primary and tertiary workflows, with Illumina DRAGEN and Emedgene Explainable AI driving incremental accuracy gains. Custom plug-in ecosystems, semantic-search modules and AI-assisted curation engines transform static variant files into interactive clinical reports within minutes. Cloud-native platforms, though smaller today, are expanding at a 15.8% CAGR, bundling workflow management, compliance dashboards and pay-as-you-go compute into unified workspaces that appeal to laboratories with limited in-house bioinformatics staff.

Service providers-ranging from managed-analysis shops to bespoke pipeline developers-remain indispensable for organizations lacking internal specialists. The Clinical and Laboratory Standards Institute's structured worksheets now guide validation, yet many hospital labs still outsource tertiary-interpretation tasks. As platforms integrate drag-and-drop interfaces and container orchestration, they further erode traditional silos and enlarge the total addressable segment of the next-generation sequencing informatics market.

Cloud installations accounted for 64.21% of the next-generation sequencing informatics market in 2024, fueled by the need to spin up tens of thousands of CPU-hours without capital expenditure. Providers such as Google Cloud offer turnkey genomics workbenches with petabyte-scale object stores and integrated AI model hubs that reduce the mean time-to-answer for multi-omics queries.

On-premise clusters persist where data cannot leave firewalls, but steady equipment depreciation and rising energy costs are prompting a migration to hybrid set-ups. The hybrid model combines in-house secure storage for raw reads with cloud-based secondary analysis, allowing compliance with emerging sovereignty statutes while maintaining elasticity. These configurations are expected to post a 15.41% CAGR to 2030, expanding the footprint of the next-generation sequencing informatics market size for deployment solutions worldwide.

The Next-Generation Sequencing Informatics Market Report is Segmented by Offering (NGS Informatics Software, NGS Informatics Services, and NGS Informatics Platforms), Deployment Mode (Cloud-Based, and More), Application (Drug Discovery, and More), End User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 42.12% of 2024 turnover, underpinned by deep research budgets, mature payer frameworks and an FDA stance that encourages adaptive AI in clinical genomics. Technology alliances are flourishing: NVIDIA, IQVIA and Mayo Clinic jointly train foundation models that crunch petabytes of multimodal patient data to accelerate trial matching. Tempus, meanwhile, became the first laboratory to feed structured somatic-variant results directly into Epic's Genomics module across more than 3,000 institutions, cementing clinical workflows that lean heavily on domestic analytics vendors.

Asia Pacific is projected to compound at 14.51% a year to 2030, propelled by Singapore's 10-year precision-medicine roadmap, Australia's PrOSPeCT cancer program and South Korea's K-MASTER initiative, each sequencing tens of thousands of genomes. India's contract-research sector, growing at 10.75%, complements device uptake; Illumina's MiSeq i100 aims squarely at labs lacking cold-chain shipping, enabling localized workflows in tier-2 cities. These moves collectively enlarge the region's slice of the next-generation sequencing informatics market size and lay a foundation for cloud-native collaborations that respect sovereign data laws.

Europe retains a solid foothold on the back of Horizon funding and a new European Commission regulation that obliges public-health labs to adopt whole-genome sequencing for pathogen surveillance starting 2025. Partnerships like Illumina-Sequentia Biotech showcase translational uptake in food safety. Middle East & Africa and South America remain nascent but promising; initiatives such as the Quad Cancer Moonshot inject genomic infrastructure and establish early footholds for vendors courting frontier-market growth across the next-generation sequencing informatics market.