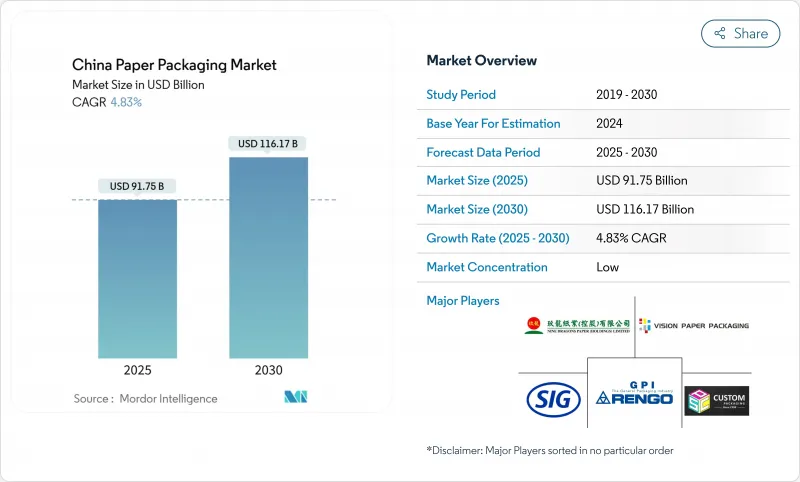

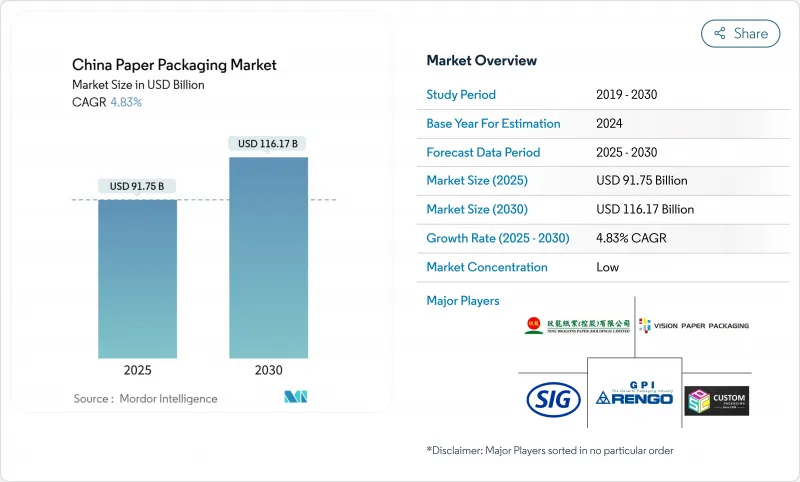

중국의 종이 포장 시장 규모는 2025년에 917억 5,000만 달러, 2030년에는 1,161억 7,000만 달러에 이를 것으로 예측되며, 이 기간의 CAGR은 4.83%를 나타낼 전망입니다.

펄프 가격주기에도 불구하고 확대가 계속되고 있는 이유는 전자상거래의 소포량, 정부의 플라스틱 감축 의무, 외식산업의 성장 등 모든 신규 수요가 골판지와 접이식 판지 형식으로 흐르고 있기 때문입니다. 재생 섬유의 채용은 중국의 국가적인 탄소 신용 제도가 회수율 향상에 공헌한 제조업체에 보답하는 것으로 가속하는 한편, 선진적인 디지털 인쇄에 의해 브랜드는 재고를 낭비하지 않고 단기간에 커스터마이즈된 캠페인을 실시할 수 있습니다. 나인드 래곤스 페이퍼와 선페이퍼 그룹과 같은 국내 대기업은 고속 콜게이터와 보드 머신을 통해 생산 능력을 확대하고 있지만 수입 목재 섬유와 동적 전력 가격의 변동으로 인해 비용 압력이 높아지고 있습니다. 녹색 포장의 시행이 지역에 따라 다르기 때문에 기업은 제형을 현지화하고 GB 43352-2023의 중금속 및 규제 물질 제한을 충족하는 품질 관리 시스템에 투자해야 합니다.

익스프레스 편의 2024년 취급 개수는 1,745억 개로, 골판지 포장이 상자 재료의 96.17%를 차지해, 중국 종이 포장 시장의 베이스라인 소비의 탄력성을 확보했습니다. 베이징과 상하이의 지하철 기반 물류 허브는 라스트 원 마일의 비용을 절감하고 배송 시간을 단축하고 있지만, 다수의 취급 사이클을 견뎌야 하는 2차 상자의 성능 요건도 강화하고 있습니다. 알리바바가 시험적으로 실시하고 있는 세계 각지로의 1시간 이내의 배달을 목표로 한 로켓 배송의 대처는 얼마나 극한의 스피드가, 내충격성을 유지하면서 중량 대 강도비를 최적화하도록 포장 설계자에게 육박하고 있는지를 증명하고 있습니다. QR 코드 직렬화 및 RFID 삽입은 재고 시각화 및 반품 자동화를 가능하게 하며 배송 판지에 점점 나타납니다. 이 시장 개척은 전자상거래를 중국 종이 포장 시장의 구조적인 백본으로 확고하게 하고 있습니다.

운송 주문은 핵심 상업 그리드에서 고밀도 폐기물을 발생시키고 상위 10%의 구역은 포장 폐기물의 64%를 차지합니다. Sumkoka와 같은 국내 공급업체가 개발 한 재사용 가능한 Bagas 성형 트레이는 고급 프랜차이즈 중 인기를 얻고 있으며 신선도를 추적하는 바이오 센서 라벨은 안전성을 손상시키지 않고 더 긴 배달 반경을 지원합니다. 다국적 퀵 서비스 체인은 세척 가능한 다인 용기를 시험적으로 도입하고 있으며, 각 국가의 규제 당국이 일회용 플라스틱에 대한 기준치를 엄격하게 유지하는 동안 미래의 컴플라이언스 방향을 보여줍니다. 이러한 요인은 종합적으로 중국의 종이 포장 시장에 기세를 주고 있습니다.

중국은 2023년 시장 펄프를 2,800만 톤 수입했지만, 이는 24% 증가했으며 공장은 운임 혼란과 관세 변동에 노출되었습니다. 소비 후 섬유의 수입 금지에 의해 국내의 리사이클 업자는 풀 가동에 가까운 상태로 조업하고 있기 때문에 폐지 가격이 상승해, 때로는 컨버터가 그램수를 낮출 수밖에 없는 경우도 있습니다. 완성지의 관세 인하는 ASEAN 공장과의 경쟁을 격화시키고 가격 계곡에 국내 마진을 침식합니다. 이러한 역학으로 중국 종이 포장 시장의 성장 기대가 줄어들고 있습니다.

골판지 상자는 2024년 중국의 종이 포장 시장 규모의 36.24%를 차지했습니다. 동광 Huangshi Jinhui의 분당 352m의 콜게이터는 전자상거래 기지에 저스트 인 타임 공급을 보장하는 능력 향상의 예입니다. 그러나 화장품의 프리미엄화에 뒷받침된 종이기는 2030년까지 연평균 복합 성장률(CAGR) 7.84%로 골판지의 우위성을 침식해 나갈 것으로 보입니다. 멀티패스 디지털 프린팅 머신은 니스 효과와 스폿 포일의 악센트를 긴 준비 시간을 강력하게 지원하고 부티크 미용 라벨이 높은 마진을 얻는 한정판을 인쇄할 수 있도록 하고 있습니다. 액체 포장용 카톤은 SIG의 알루미늄층을 사용하지 않는 기술을 활용하여 틈새 관련성을 유지하고 있습니다. 변조 방지 슬리브와 같은 특수 서브 라인은 도시 지역의 건강 관리 지출이 증가함에 따라 꾸준히 성장하고 있습니다.

2024년 중국의 종이 포장 시장 점유율의 41.32%는 식품이었습니다. 식용 도시락의 밀도는 그리드의 핫스팟에서 급상승하고 지방 자치 단체가 재활용 섬유 공장에 공급하는 폐쇄 루프 회수를 시도하도록 촉구하고 있습니다. 퍼스널케어 및 화장품은 규모가 작은 것, 온라인 미용 인플루언서와 가처분 소득 상승을 배경으로 연간 8.21% 확대됩니다. Amcor 재활용 파우치와 리필 포드는 1급 쇼핑몰의 샴푸 리필 스테이션에서 사용되며 기능성과 지속가능성의 융합을 보여줍니다. 일렉트로닉스 브랜드는 정전기 방지 및 방습 라이너를 요구하고 있으며, 골판지 공급업체는 프루팅에 나노 클레이 코팅을 그래프트 겹치는 것으로, 이 유리한 크로스 오버에 대응하고 있습니다. 건강 관리 포장은 온도 로깅을 위한 스마트 라벨을 통합하여 지역 콜드체인 전반에 걸쳐 의약품의 무결성을 보장합니다.

중국의 종이 포장 시장 보고서는 제품 유형(폴딩 판지, 골판지 상자, 종이 봉지 및 가방, 액체 포장 판지 등), 최종 사용자 산업(식품, 음식, 건강 관리, 개인 관리, 가정 용품, 전자 제품 등), 재료 유형(처녀 섬유 기반, 재생 섬유 기반), 포장 수준(1차, 2차, 시장 예측은 금액(달러)입니다.

The China paper packaging market size stands at USD 91.75 billion in 2025 and is forecast to climb to USD 116.17 billion by 2030, registering a 4.83% CAGR over the period.

Expansion continues despite pulp-price cycles because e-commerce parcel volumes, government plastic-reduction mandates, and food-service growth all channel fresh demand into corrugated and folding-carton formats. Recycled fiber adoption accelerates as China's national carbon-credit scheme rewards manufacturers that raise recovered-content ratios, while advanced digital printing lets brands run short, customized campaigns without inventory waste. Domestic leaders such as Nine Dragons Paper and Sun Paper Group extend capacity through high-speed corrugators and board machines, yet volatility in imported wood fiber and dynamic electricity pricing keeps cost pressure high. Provincial variability in green-packaging enforcement adds complexity, prompting firms to localize formulations and invest in quality-control systems that meet GB 43352-2023 limits on heavy metals and restricted substances.

Express delivery handled 174.5 billion items in 2024, with corrugated packaging accounting for 96.17% of box material, ensuring resilient baseline consumption for the China paper packaging market. Metro-based logistics hubs in Beijing and Shanghai compress last-mile costs and shorten delivery times, but they also intensify performance requirements for secondary boxes that must survive multiple handling cycles. Alibaba's pilot rocket-delivery initiative, targeting one-hour global drop-offs, exemplifies how extreme speed pushes packaging designers to optimize weight-to-strength ratios while preserving shock resistance. QR-code serialization and RFID inserts increasingly appear on shipping cartons, enabling inventory visibility and returns automation. Together these developments cement e-commerce as the structural backbone for the China paper packaging market.

Takeaway orders generate high-density waste in core commercial grids where the top 10% of zones account for 64% of packaging discards, driving restaurants to switch to lighter, fiber-based solutions. Reusable, bagasse-molded trays developed by domestic suppliers such as Sumkoka gain traction among premium franchises, while biosensor labels that track freshness support longer delivery radii without safety compromises. Multinational quick-service chains pilot washable dine-in containers, indicating the direction of future compliance as provincial regulators tighten thresholds on single-use plastics. These factors collectively add momentum to the China paper packaging market.

China imported 28 million tons of market pulp in 2023, a 24% rise that exposes mills to freight disruptions and tariff shifts. The ban on post-consumer fibre imports keeps domestic recyclers running near full capacity, raising recovered-paper prices and occasionally forcing converters to down-spec grammage. Tariff cuts on finished paper boost competition from ASEAN mills, eroding domestic margins during price troughs. These dynamics trim growth expectations for the China paper packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Corrugated boxes generated 36.24% of China paper packaging market size in 2024 as express freight required light, crush-resistant formats. Dongguan Huangshi Jinhui's 352 m-per-minute corrugator exemplifies capacity build-out that secures just-in-time supply for e-commerce hubs. Yet folding cartons, buoyed by cosmetics premiumisation, are pacing a 7.84% CAGR that will erode corrugated dominance through 2030. Multi-pass digital presses support varnish effects and spot-foil accents without forcing long makeready times, letting boutique beauty labels print limited editions that fetch high margins. Liquid packaging cartons maintain niche relevance by leveraging SIG's alu-layer-free technology, which cuts carbon footprints by 61% while safeguarding dairy shelf life. Speciality sub-lines, including tamper-evident pharma sleeves, grow steadily as healthcare spending rises in urban markets.

Food products held 41.32% of China paper packaging market share in 2024 because takeaway dining dominates urban consumption. Meal-box density spikes in grid hotspots, prompting municipalities to trial closed-loop collection that feeds recycled-fibre mills. Personal-care and cosmetics, though smaller, expand 8.21% yearly on the back of online beauty influencers and rising disposable income. Amcor's recycle-ready pouches and refill pods serve shampoo refill stations in tier-one malls, illustrating how functionality merges with sustainability. Electronics brands demand anti-static, moisture-barrier liners, a lucrative cross-over that corrugated suppliers address by grafting nanoclay coatings onto fluting. Healthcare packaging integrates smart labels for temperature logging, ensuring drug integrity across regional cold chains.

The China Paper Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Boxes, Paper Bags and Sacks, Liquid Packaging Cartons, and More), End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, Electronics, and More), Material Type (Virgin Fibre-Based, Recycled Fibre-Based), Packaging Level (Primary, Secondary, Tertiary), and Geography (China). Market Forecasts are in Value (USD).