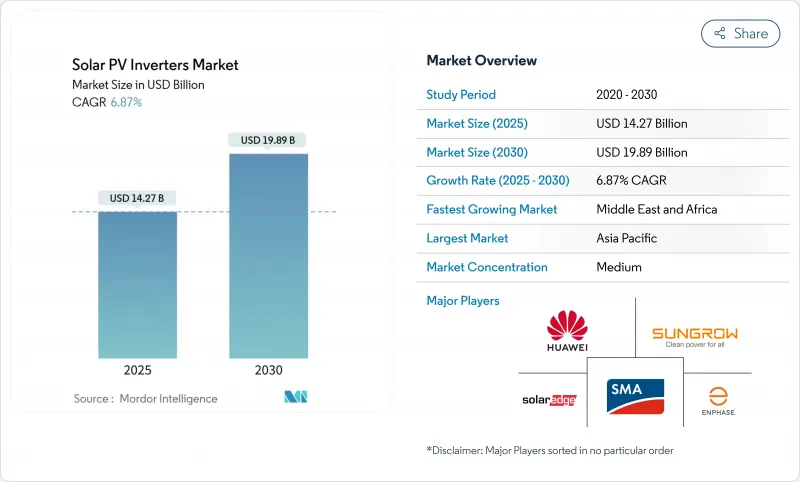

태양광 발전 인버터 시장 규모는 2025년에 142억 7,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 6.87%로, 2030년에는 198억 9,000만 달러에 달할 것으로 예상됩니다.

시장 확대는 단순한 DC에서 AC로의 전환으로부터 전력 품질을 보호하고 소유자의 새로운 수익원을 풀어주는 스마트 그리드 형성 솔루션으로의 전환에 뒷받침됩니다. 아시아태평양이 세계 수요를 지지하고 있지만, 대규모 유틸리티 프로젝트와 그리드 근대화의 과제가 교차하고 있는 중동이 현재 가장 급성장하고 있는 지역입니다. 일본의 견조한 교체 사이클, 인도의 옥상 설치 의무, 미국과 유럽의 고전압 설계가 당면의 유닛 수량을 증가시키는 한편, 중국에서 SiC/IGBT의 지속적인 부족과 억제 증가가 확대 페이스를 약화시키고 있습니다. 이러한 역풍에도 불구하고 첨단 그리드 지원 기능에 비해 가격이 비싸기 때문에 태양광 발전용 인버터 시장의 총 수익은 계속 상승하고 있습니다.

유틸리티 개발자는 밸런스 오브 시스템 비용을 낮추고 전력 밀도를 높이기 위해 1,500V DC 아키텍처를 지정하는 것이 증가하고 있으며, 2,000V DC 아키텍처도 시험적으로 도입하고 있습니다. GE Vernova의 2,000V 플랫폼은 평준화 에너지 비용을 절감하는 30%의 출력 향상을 보여줍니다. 이 전압의 전환은 특히 토지와 그리드의 헤드룸에 의해 더 큰 블록 크기를 가능하게 하는 경우, 신축 사이트에서는 1,000V 어레이를 경제적으로 진부화시켜 리노베이션 프로젝트에 박차를 가합니다. 반도체 수요가 증가함에 따라 SiC 디바이스공급을 가속화하고 주요 브랜드의 열 설계 전문 지식의 전략적 중요성을 높이고 있습니다.

인도 정책은 신규 및 기존 상업시설에 옥상 어레이를 설치해야 하며 100kW 미만의 인버터에 대한 지속적인 요구가 커지고 있습니다. 2024년도에는 4GW라는 기록적인 증설이 예정되어 있어 기회의 크기를 이야기했습니다. 국내 제조업체는 2026년까지 110GW의 셀과 모듈을 건설할 계획에 포함된 수입 대체 목표로부터 혜택을 받아 국내 밸류체인을 강화하고 있습니다.

SiC 웨이퍼공급 부족은 고효율 인버터를 계속 제약하고 재료비를 증가시키고 있습니다. 웨이퍼의 재정난은 위험 인지를 높이고 있지만, 인피니언은 비용 효율적인 200mm SiC 웨이퍼로 전환함으로써 2026년 이후의 구제를 시사하고 있습니다.

니트가 55%의 수익 리드를 유지했지만, 모듈형 전자 제품이 조기 어댑터의 틈새 시장을 넘어감에 따라 마이크로 인버터는 CAGR 8.1%를 나타낼 것으로 예측됩니다. Enphase는 2025년에 650만 대 이상의 국내용 마이크로 인버터를 출하하여 미국 현지화 기준을 충족하고 이 분야의 상업 규모를 입증했습니다. 태양광 발전 인버터 시장은 ASIC 설계, 무선 데이터, 열공학을 소형 실적에 통합한 기업에 보상을 주고 있습니다. 중앙 아키텍처는 현재 중국에서 전력 억제로 인한 수요 측면에 직면하고 있지만, 다른 지역에서는 특히 공장 수준의 제어와 경쟁력 있는 설비 투자가 최우선 과제인 전력 사업 프로젝트에 뿌리를 내리고 있습니다.

경쟁의 심각성은 마이크로 일렉트로닉스에서 두드러지며 하드웨어 비용보다 펌웨어의 고급화와 안전 인증이 장벽입니다. 그 결과, 저가의 진출기업은 급속 셧다운이나 배터리 인터페이스 모드 등의 급속한 기능 전개를 따라잡는데 고생하고 있습니다. 견고한 수량 성장에도 불구하고 마이크로 인버터는 향후 10년 이내에 스트링 플랫폼을 구축하지 않을 것으로 보입니다.

2024년 출하량의 63%는 전력회사가 차지했는데, 이는 장기 PPA로 고정된 대규모 프로젝트 파이프라인을 반영하고 있습니다. 그럼에도 불구하고 그리드 서비스 및 인터넷 요금 프레임 워크가 가정의 경제성을 향상시키기 때문에 주택 시스템은 연간 7.6%를 나타낼 것으로 보입니다. 인도의 Pradhan Mantri Surya Ghar 프로그램은 2027년 3월까지 30GW의 옥상 어레이를 설치하는 것을 목표로 하고 있으며, 호주는 배터리 부가 기능의 동향에 따라 설치율이 상승하고 있습니다. 상업용 옥상은 인도의 옥상 의무화 파도를 타고 있지만, 다른 지역에서는 투자 회수 기간을 연장하는 신중한 대출 조건에 직면하고 있습니다.

프로슈머는 양방향 기능과 아일랜드 모드의 탄력성을 더욱 강조하고 있으며, 인버터 OEM은 배터리 제어 로직의 통합을 촉구하고 있습니다. 그 결과, 태양광 발전 인버터 시장의 총 매출이 늘어나고 있는 거시적인 설치 대수의 성장을 보완하는 형태로 ASP가 상승하고 있습니다. 한편, 유틸리티 사업자는 1,500V와 2,000V의 플랫폼에 주력하고, 보다 엄격한 그리드 코드를 준수하기 위해 STATCOM과 같은 기능을 탑재하고 있습니다.

태양광 발전 인버터 시장 보고서는 인버터 유형(중 인버터, 스트링 인버터, 마이크로 인버터, 하이브리드/배터리 레이디 인버터), 위상(단상, 삼상), 접속 유형(온그리드, 오프 그리드), 용도(주택, 상업 및 산업, 유틸리티 스케일), 지역(북미, 유럽, 아시아태평양, 남미,

아시아태평양은 중국의 수직 통합 공급망과 인도의 정책 주도형 옥상 녹화 추진에 힘입어 2024년 출하량의 55%를 차지했습니다. 중국의 새로운 시장 기반 관세 제도는 그린필드의 설치를 감속시킬 수 있지만, 출하량의 복원력은 스토리지와 고전압 스트링을 통합한 리노베이션에 기인합니다. 2026년까지 110GW에 이르는 인도의 제조 능력은 국내 조달 루프를 강화하고 국내 태양광 발전 인버터 시장을 수입 변동으로부터 보호하지만 규제 집행의 지역 격차가 당면의 이익을 억제합니다.

중동은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.4%를 기록해 기가와트 규모의 프로젝트를 경제다양화의 청사진에 맞추고 있습니다. 엄격한 사막 조건은 고열 설계에 대한 수요를 높여 밀폐형 큐비클 솔루션에 특화된 유럽 OEM에 틈새 시장을 엽니다. 사우디아라비아와 아랍에미리트(UAE)의 송전망 강화 노력은 저전압 라이드스루와 무효 전력 관리의 사양을 끌어올렸으며, 벤더는 보다 엄격한 유틸리티 벤치마크에 비추어 제품을 인증하도록 강요받고 있습니다.

북미와 유럽은 교체 및 리노베이션 사이클이 증가 수요를 지배하는 성숙한 설치 기반에서 운영되고 있습니다. 미국에서는 인플레이션 억제법의 국내 전력량 공제로 현지 생산이 가속화되고 있으며, 텍사스주, 사우스캐롤라이나주, 애리조나주 시설은 2026년까지 연간 생산량이 30GW를 크게 웃도는 것을 목표로 하고 있습니다. 유럽에서는 독일, 스페인 등 시장에서 재생에너지의 보급률이 50%를 넘어 그리드 형성 기능의 가치가 높아지고, 신규 건설량이 두드러지더라도 벤더는 보다 높은 ASP를 통과할 수 있습니다.

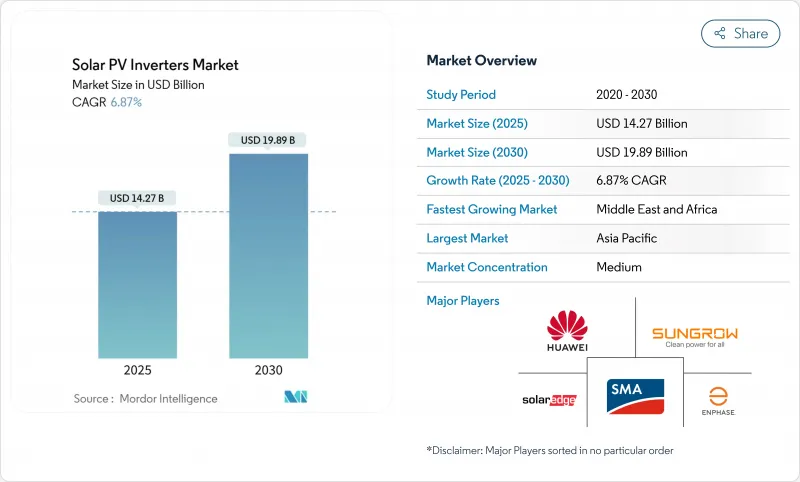

The Solar PV Inverters Market size is estimated at USD 14.27 billion in 2025, and is expected to reach USD 19.89 billion by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

The market's expansion is underpinned by a move from simple DC-to-AC conversion toward smart, grid-forming solutions that safeguard power quality and unlock new revenue streams for owners. Asia-Pacific anchors global demand, yet the Middle East is now the fastest-growing territory as large utility projects intersect with grid-modernization agendas. Robust replacement cycles in Japan, rooftop mandates in India, and higher-voltage designs across the United States and Europe amplify near-term unit volumes, while persistent SiC/IGBT shortages and rising curtailment in China temper the pace of expansion. Despite those headwinds, premium pricing for advanced grid-support functions keeps aggregate revenue upward in the solar PV inverter market .

Utility developers increasingly specify 1,500 V-and pilot 2,000 V-DC architectures to lower balance-of-system costs and boost power density. GE Vernova's 2,000 V platform showcases a 30% output gain that decreases levelized energy costs. This voltage migration renders 1,000 V arrays economically obsolete on new-build sites and spurs retrofit projects, especially where land and grid headroom allow bigger block sizes. Heightened semiconductor demand follows, tightening the supply of SiC devices and elevating the strategic importance of thermal design expertise among leading brands.

India's policy obliges new and existing commercial structures to install rooftop arrays, driving the sustained need for <=100 kW inverters. Record additions of 4 GW in fiscal 2024 signal the scale of the opportunity . Domestic manufacturers benefit from import-substitution targets embedded in the country's 110 GW cell-and-module build-out by 2026, reinforcing the local value chain. While implementation gaps remain across several states, standardized installation practices create a template for broader residential uptake.

SiC wafer supply tightness continues to constrain high-efficiency inverters and amplify bill-of-material costs. Wolfspeed's financial distress heightens risk perceptions, whereas Infineon's switch to cost-effective 200 mm SiC wafers signals relief from 2026 onward . European and North American producers, dependent on advanced semiconductors for grid-forming functionality, experience sharper margin compression than vertically integrated Chinese peers able to fall back on silicon alternatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Central units retained a 55% revenue lead in 2024, yet microinverters are forecast to grow at an 8.1% CAGR as module-level electronics move beyond the early-adopter niche. Enphase shipped more than 6.5 million domestic microinverters in 2025, satisfying US localization criteria and underlining the segment's commercial scale . The solar PV inverter market rewards firms that combine ASIC design, wireless data, and thermal engineering in a miniature footprint. Central architectures now confront flattish demand in China due to curtailment but remain anchored in utility projects elsewhere, especially where plant-level controls and competitive capex remain priorities.

Competitive intensity is pronounced in microelectronics; barriers arise from firmware sophistication and safety certifications rather than raw hardware cost. Consequently, low-price entrants struggle to keep pace with rapid feature rollouts such as rapid shutdown and battery interface modes. Despite robust volume growth, microinverters are not likely to eclipse string platforms before the next decade, keeping the solar PV inverter market diversified by architecture.

Utility plants captured 63% of 2024 shipments, reflecting large project pipelines locked under long-term PPAs. Even so, residential systems should expand by 7.6% annually as grid services and net-billing frameworks enhance household economics. India's Pradhan Mantri Surya Ghar program targets 30 GW of rooftop arrays by March 2027, while Australia's battery add-on trend lifts attachment rates. Commercial rooftops ride India's rooftop mandate wave but face cautious finance terms in other regions that stretch payback timelines.

Prosumers increasingly value bidirectional capability and island-mode resilience, prompting inverter OEMs to integrate battery control logic. The resulting ASP uplift compensates for slower macro installation growth, supporting aggregate revenue progression inside the solar PV inverter market. Utility developers, meanwhile, focus on 1,500 V and 2,000 V platforms, coupling them with STATCOM-like functionalities to meet stricter grid-code compliance.

The Solar PV Inverter Market Report is Segmented by Inverter Type (Central Inverters, String Inverters, Micro Inverters, and Hybrid/Battery-Ready Inverters), Phase (Single-Phase and Three-Phase), Connection Type (On-Grid and Off-Grid), Application (Residential, Commercial and Industrial, and Utility-Scale), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Asia-Pacific generated 55% of 2024 shipments, underpinned by China's vertically integrated supply chain and India's policy-driven rooftop push. While China's new market-based tariff regime may slow greenfield installations, volume resilience stems from retrofits that embed storage and higher-voltage strings. India's manufacturing capacity, set to reach 110 GW by 2026, tightens domestic procurement loops and shields the local solar PV inverter market from import volatility, although regional disparities in regulatory execution temper immediate gains.

The Middle East, clocking the quickest 9.4% CAGR through 2030, aligns gigawatt-scale projects with economic diversification blueprints. Harsh desert conditions drive demand for high-derating-temperature designs, opening niches for European OEMs specializing in sealed cubicle solutions. Grid-reinforcement efforts in Saudi Arabia and the United Arab Emirates elevate low-voltage ride-through and reactive-power management specifications, pressing vendors to certify products against stricter utility benchmarks.

North America and Europe operate in a mature install base where replacement and retrofit cycles dominate incremental demand. The US Inflation Reduction Act's domestic content credits accelerate localized production, with Texas, South Carolina, and Arizona facilities targeting annual output well above 30 GW by 2026. Europe's renewable penetration surpassing 50% in markets such as Germany and Spain raises the value of grid-forming features, allowing vendors to pass through higher ASPs even as new-build volumes plateau.