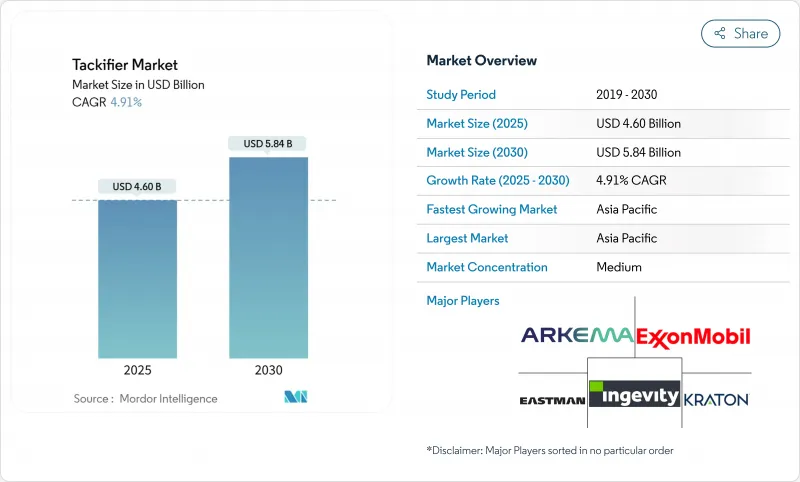

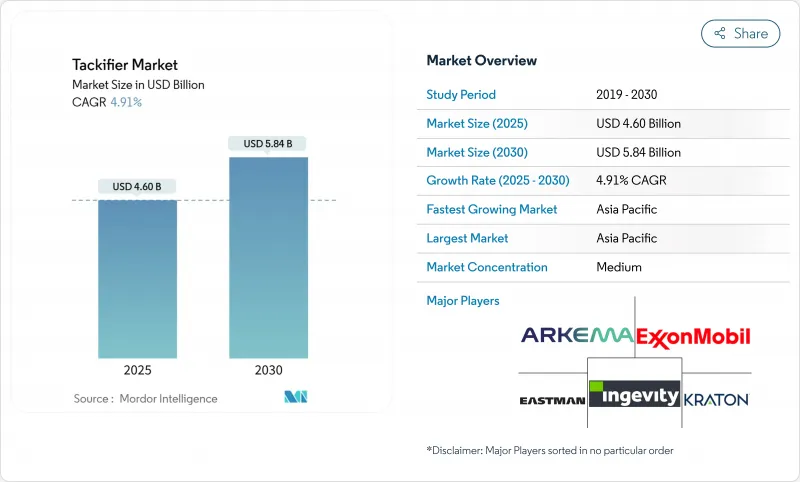

태키파이어 시장 규모는 2025년에 46억 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 4.91%로, 2030년에는 58억 4,000만 달러에 달할 것으로 예상됩니다.

포장 및 위생 제품에서 감압 접착제와 핫멜트 접착제의 지속적인 수요가 현재 수익을 뒷받침하고 있는 반면, 전기자동차 배터리 조립, 특수 건축, 낮은 VOC 식품 포장에서의 사용 확대는 향후 성장 경로를 확대하고 있습니다. 아시아태평양의 급속한 인프라 투자, 북미와 유럽의 엄격한 배출 규제, 바이오 재료에 대한 브랜드 소유자의 헌신 등이 시장의 기세를 강화하고 있습니다. 초저 VOC 등급, 고열 탄화수소 수지, 로진 유래 분배 등의 혁신을 통해 공급업체는 접착 성능을 희생하지 않고 식품 접촉 규제 및 환경 규제 강화에 대응할 수 있습니다. 태키파이어 프리 반응성 핫멜트 및 역동적인 폴리우레탄 화학으로의 기술 이동은 원유 가격의 변동과 함께 수익성을 저하시키면서도 연구 개발의 다양화에 박차를 가할 수 있는 종합적인 리스크로 남아 있습니다.

전자상거래의 소포량과 고급 위생 용품의 조합으로 핫멜트 접착제와 감압 접착제의 소비가 계속 증가하고 있습니다. 탁 파이어 수지는 이러한 고속 생산 라인이 필요로 하는 중요한 초기 잡기 강도와 지속적인 박리 강도를 제공합니다. HBFuller사의 Full-Care 6217은 처방의 미세 조정으로 박리성을 향상시키면서 접착제 사용량을 20% 삭감할 수 있음을 보여줍니다. 생분해성 로진 수지는 브랜드의 지속가능성의 맹세에 따라 종이를 뒷받침한 테이프로 인기를 끌고 있습니다. 여성 관리용 패드의 수분 관리 기능을 통해 공급업체는 고습도를 견디면서도 냄새를 억제하는 점착제를 요구하게 됩니다. 엑손 모빌의 Escorez 포트폴리오는 투명성이 가장 중요하게 여겨지는 투명 포장 필름에 희미하고 열 안정성이 높은 등급이 요구됨을 보여줍니다. 이러한 복합적인 요구에 따라 태키파이어 시장은 2030년까지 소비재의 성장과 밀접하게 연관되어 있습니다.

중국, 인도 및 ASEAN 국가의 대량 운송 노선, 공항, 저렴한 주택 계획은 바닥재, 지붕재 및 패널 접착제의 장기 수요를 지원합니다. 습기 경화형 시스템은 열대 습도에서 우수하며, 태키파이어 수지의 초기 습윤에 대한 의존은 판매량을 증가시킵니다. Master Builders Solutions사는 이러한 제품을 강점으로 2028년까지 인도에서 500캐롤 루피의 매출을 목표로 하고 있습니다. 경량 복합 외관과 샌드위치 패널을 추진하는 건축 기준법은 열 안정성을 제공하는 합성 탄화수소계 점착제의 성능 창을 확대하고 있습니다. 중국 접착 테이프 협의회(China Adhesive Tape Council)는 건축용 테이프의 수량 증가를 보고하고 인프라와 내구 소비재가 어떻게 교차하는지를 강조합니다. 이러한 투자는 APAC의 태키파이어 시장 성장의 리더십을 유지하고 있습니다.

탄화수소의 튀르키예 파이어 라인은 C5와 C9 스트림이 나프타 크래커의 제품별이기 때문에 원유 가격의 변동을 반영합니다. 가격 상승은 마진을 악화시키고 설비투자를 정체시키고 연구개발예산을 제약합니다. 2021년 유럽의 물류 급박 시에는 접착제 수요가 5% 감소하여 공급 중단에 대한 취약성이 부각되었습니다. Speciality Chemical Planner는 현재 위험 회피와 민첩한 가격 결정 수단을 강조하고 있지만 소규모 독립 수지 제조 업체는 여전히 위험에 처해 있습니다. 석유수지 점유율은 65.45%를 차지하고 있으며, 변동이 확대되면 경쟁 구도를 재구성하고 바이오 베이스 등급으로 바이어를 유도할 가능성이 있습니다.

석유수지는 2024년 매출의 65.45%를 차지하며 신뢰할 수 있는 품질과 가격 성능의 균형으로 태키파이어 시장을 지원했습니다. C5-C9 하이브리드는 자동차 인테리어와 산업용 테이프의 탁과 내열성을 보장합니다. 반면 로진 등급은 컨버터가 친환경 라벨 및 공인 컴포스터블 파우치를 위해 재생할 수 있는 함량을 추구함에 따라 CAGR 5.15%를 나타낼 전망입니다. 톨유 로진공급은 바이오연료 정제업자가 같은 원료 풀에서 조달하기 때문에 희박해 2030년까지 8% 공급 부족이 예측됩니다. 성공적인 공급업체는 탄화수소 및 로진계를 다양화하고 가격 변동을 헤지하면서 브랜드의 지속가능성 목표를 달성하고 있습니다. 테르펜 수지는 틈새이지만 천연 고무 및 탄성 기재와의 접착력을 향상시키는 극성의 장점이 있습니다. 태키파이어 시장은 혼합이 원료 접근법에서 이익을 얻고, 배합자가 비용, 성능 및 녹색 함량의 균형을 맞출 수 있습니다.

석유 생산자는 안정성을 유지하기 위해 장기 계약을 맺는 것을 목표로 하지만, 고객이 바이오 함량에 중점을 두면 그러한 계약은 유연성을 저하시킵니다. 반대로, 로진의 혁신자는 투명 포장 필름에 요구되는 색상과 냄새의 기준을 충족시키기 위해 수소 첨가 개선을 활용합니다. 비용 변동과 지속가능성에 관한 법률의 상호작용은 향후 10년간 원료 전략을 결정할 것입니다.

고형 칩과 펠릿은 2024년 매출의 81.56%를 차지했는데, 이는 컨버터가 공급이 용이하고 분진이 적고, 확립된 핫멜트 장치와의 적합성을 선호하기 때문입니다. 150℃를 넘는 용융 피크에도 산화 열화 없이 견딜 수 있기 때문에 카톤 및 실링 라인이나 목공 라인에는 빠뜨릴 수 없습니다. 수지 분배는 CAGR 5.32% 이상으로 라벨 및 유연한 라미네이트에서 수성 접착제의 성장을 지원합니다. 이러한 분배는 VOC 배출량을 줄이고 라인 정리를 간소화합니다. 액체 유형은 상온 점도가 필요한 리본 코트 및 솔벤트 시스템에 사용되지만 솔벤트 절감 비용으로 시장 점유율이 부진합니다. 제조업체의 경우 멀티 폼 포트폴리오를 제공하면 스위칭 장벽을 높이고 맞춤형 점도 프로파일을 필요로 하는 특수 최종 용도에서 점유율을 확보할 수 있습니다.

아시아태평양은 2024년 매출의 36.25%를 차지했으며 인프라 투자, 상거래 급증, 종이 기저귀의 보급 확대에 힘입어 CAGR 5.50%를 나타낼 전망입니다. 중국의 점착 테이프 생산은 차별화된 점착제를 지정하는 건설 및 전자 제품의 수직 분야와 연계하여 한 자릿수의 높은 성장을 보였습니다. 2025년 2만 캐롤 루피가 되는 인도의 건설 화학 시장은 건축 주기를 가속화하는 접착제에 대한 지역적 수요를 뒷받침하고 있습니다. 생분해성 포장을 지지하는 정부의 정책이 로진 기반 수요를 끌어올리는 한편, 토르유공급이 불안정하기 때문에 현지의 배합업자가 안정된 원료를 확보하는 것이 과제가 되고 있습니다.

북미는 엄격한 VOC 규제와 FDA 식품 접촉 규칙을 통해 초저 냄새 등급의 구매를 향하고 있으며 혁신의 주도권을 유지하고 있습니다. 미국과 멕시코에서는 자동차의 전동화가 진행되어 배터리 셀 스택을 보호하는 고열 합성 수지 수요가 높아지고 있습니다. 유럽은 순환형 경제 목표와 REACH 준수를 중시하고, 비용 상승에도 불구하고 바이오 함유 점착 부여제로 축발을 옮기고 있습니다. 유럽 건축용 접착제의 2025년 회복은 규제로 인한 역풍이 지속 가능한 대체 기회와 공존할 수 있음을 시사합니다.

남미와 중동 및 아프리카는 규모가 작은 것, 물류 회랑, 소비재의 성장, 제조업에 대한 해외 직접 투자와 관련된 상승 여지가 있습니다. 산고반에 의한 FOSROC의 10억 2,500만 달러의 인수는 GCC 국가와 인도에서 건축용 접착제의 유통을 강화하는 것으로, 세계 기업이 신흥 수요 센터에 전략적 베팅을 하는 예입니다. 환율 변동과 현지 수지 생산 능력의 한계는 당면 성장을 억제하지만 완만한 산업화로 향후 10년간의 태키파이어 보급의 기반이 갖춰집니다.

The Tackifier Market size is estimated at USD 4.60 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 4.91% during the forecast period (2025-2030).

Sustained demand for pressure-sensitive and hot-melt adhesives in packaging and hygiene products anchors current revenue, while widening use in electric vehicle battery assembly, specialty construction, and low-VOC food packaging broadens future growth pathways. Rapid infrastructure spending across Asia Pacific, stringent emission norms in North America and Europe, and brand owner commitments to bio-based materials collectively reinforce market momentum. Innovation in ultra-low-VOC grades, high-heat hydrocarbon resins, and rosin-derived dispersions allows suppliers to address tightening food-contact and environmental regulations without sacrificing bond performance. Technology shifts toward tackifier-free reactive hot melts and dynamic polyurethane chemistries, alongside crude-oil price swings, remain overarching risks that could temper profitability yet also spur R&D diversification.

E-commerce parcel volume, combined with premium hygiene products, continues to lift hot-melt and pressure-sensitive adhesive consumption. Tackifier resins provide the critical early-grab and sustained peel strength these fast-running production lines require. H.B. Fuller's Full-Care 6217 shows how formulation tweaks can cut adhesive usage by 20% while improving peel, a direct cost-and-performance benefit to diaper makers. Biodegradable rosin resins gain traction in paper-backed tapes, aligning with brand sustainability pledges. Moisture-management features in feminine care pads push suppliers toward tackifiers that tolerate high humidity yet keep odor low. ExxonMobil's Escorez portfolio illustrates the push for light-color, thermally stable grades serving transparent packaging films where clarity is paramount. These combined needs ensure that the tackifier market remains firmly linked to consumer goods growth through 2030.

Mass transit lines, airports, and affordable housing programs across China, India, and ASEAN nations underpin long-run demand for flooring, roofing, and panel bonding adhesives. Moisture-cure systems excel in tropical humidity, and their reliance on tackifier resins for initial wet-out drives incremental volumes. Master Builders Solutions targets INR 500 crore turnover in India by 2028 on the strength of such products. Building codes pushing lightweight composite facades and sandwich panels widen the performance window for synthetic hydrocarbon tackifiers that deliver thermal stability. The China Adhesive Tape Council reports volume gains in building tapes, highlighting how infrastructure and consumer durables intersect. These investments sustain APAC's leadership in tackifier market growth.

Hydrocarbon tackifier lines mirror crude-oil price swings because C5 and C9 streams are co-products of naphtha crackers. Spikes erode margins, stall expansion CAPEX, and constrain R&D budgets. During the 2021 European logistics crunch, adhesive demand slipped 5%, underscoring vulnerability to supply disruptions. Specialty chemical planners now emphasize hedging and agile pricing tools, yet smaller independent resin houses remain exposed. With petroleum resins occupying 65.45% share, extended volatility could redirect buyers toward bio-based grades, reshaping the competitive landscape.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Petroleum resins delivered 65.45% of 2024 revenue, anchoring the tackifier market with a reliable quality and price-performance balance. C5-C9 hybrids secure tack and heat resistance for automotive interiors and industrial tapes. Meanwhile, rosin grades expand at a 5.15% CAGR as converters pursue renewable content for eco-labels and certified compostable pouches. Tall-oil rosin supply tightens because biofuel refiners draw from the same feed pool, leading to a projected 8% deficit by 2030. Successful suppliers diversify between hydrocarbon and rosin lines, hedging price swings while meeting brand sustainability targets. Terpene resins, though niche, add polarity advantages that improve adhesion to natural rubber and elastic substrates. The tackifier market benefits from this blended feedstock approach, ensuring formulators can balance cost, performance, and green content.

Petroleum producers aim to lock in long-term contracts to preserve stability, but such commitments reduce flexibility when customers pivot to bio-content mandates. Conversely, rosin innovators exploit hydrogenated modifications to match color and odor standards demanded in transparent packaging films. The interplay between cost volatility and sustainability legislation defines feedstock strategy for the decade ahead.

Solid chips and pellets held 81.56% of 2024 sales because converters prefer easy feeding, low dust, and compatibility with established hot-melt equipment. They withstand melting peaks above 150 °C without oxidative degradation, making them indispensable for carton-sealing and woodworking lines. Resin dispersions outpace with 5.32% CAGR, meeting waterborne adhesive growth in labels and flexible laminations. These dispersions reduce VOC output and simplify line cleanup, critical under tighter plant-emission audits. Liquid forms serve ribbon-coating and solvent systems where room-temperature viscosity is needed, yet their market share lags amid solvent abatement costs. For manufacturers, offering multi-form portfolios elevates switching barriers and secures share in specialty end uses that demand customized viscosity profiles.

The Tackifier Market Report is Segmented by Feedstock (Rosin Resins, Petroleum Resins, Terpene Resins), Form (Solid, Liquid, Resin Dispersion), Type (Synthetic, Natural), Application (Tapes and Labels, Assembly, Bookbinding, and More), End-User Industry (Packaging, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific commanded 36.25% of 2024 revenue and rises at 5.50% CAGR, underpinned by infrastructure investment, surging e-commerce, and expanding diaper penetration. China's adhesive tape production grew at high single digits, aligned with construction and electronics verticals that specify differentiated tackifiers. India's construction chemicals market, sized at INR 20,000 crore in 2025, underscores regional appetite for adhesives that accelerate build cycles. Government policies favoring biodegradable packaging boost rosin-based demand, while volatile tall-oil supply challenges local formulators to secure consistent feedstock.

North America retains innovation leadership through tight VOC caps and FDA food-contact rules steering purchases toward ultra-low-odor grades. Automotive electrification in the United States and Mexico triggers demand for high-heat synthetic resins that secure battery cell stacks. Europe emphasizes circular economy targets and REACH compliance, prompting a pivot to bio-content tackifiers despite higher costs. The 2025 rebound in European construction adhesives signals that regulatory headwinds can coexist with sustainable substitution opportunities.

South America and Middle East & Africa, though smaller, offer upside tied to logistics corridors, consumer goods growth, and foreign direct investment in manufacturing. Saint-Gobain's USD 1.025 billion purchase of FOSROC bolsters distribution of construction adhesives in GCC states and India, an example of global firms placing strategic bets on emerging demand centers. Exchange-rate swings and limited local resin capacity temper immediate growth, but gradual industrialization sets a foundation for tackifier uptake over the next decade.