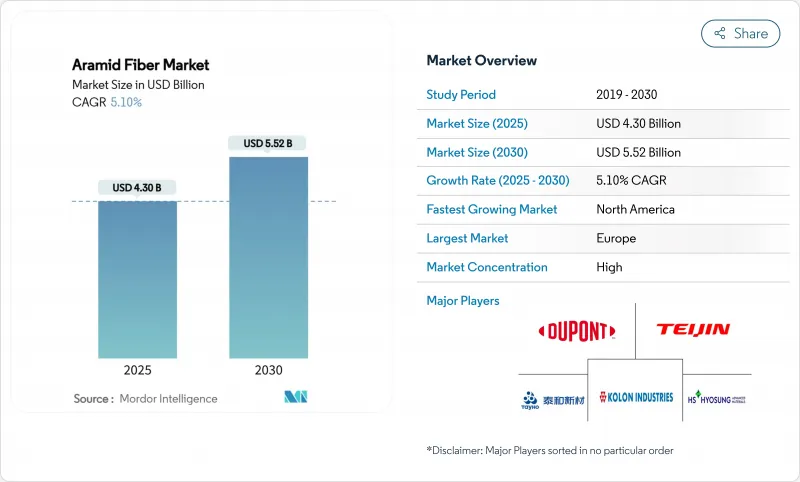

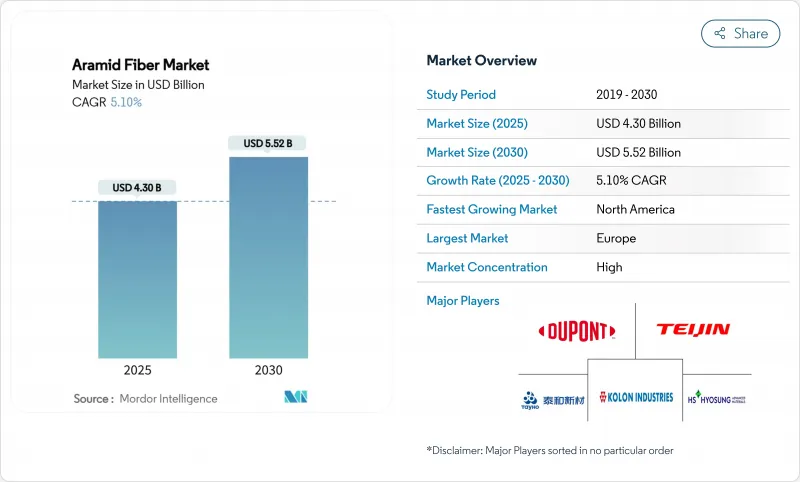

아라미드 섬유 시장 규모는 2025년에 43억 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 5.10%로, 2030년에는 55억 2,000만 달러에 달할 것으로 예상됩니다.

자동차, 항공우주, 전기통신, 고급 개인보호구의 보급이 수요를 높이는 한편, 섬유의 강도 대 중량비와 열안정성이 장기적인 관련성을 지원하고 있습니다. 전기 모빌리티의 재료 경량화 목표, 5G 네트워크 구축, 극초음속 및 우주 프로그램에 대한 투자 증가는 지속적으로 사업 기회를 확대합니다. 동시에, 주로 MPD와 PPD의 원료가격 변동이 금리를 압박하고, 선도적인 제조업체에 의한 수직통합의 움직임을 촉구하고 있습니다. 지적재산의 제약이 더욱 경쟁의 역학을 형성하고, 연구개발에 자금을 공급하고, 크로스 라이선스의 틀을 잘 이용할 수 있는 기존 기업의 지위를 확고하게 하고 있습니다.

중국, 인도, 동남아시아의 신흥경제권에서 산업안전규칙 시행이 진행됨에 따라 아라미드 강화장갑, 헬멧, 내열작업복 주문이 증가하고 있습니다. 아라미드 복합재료로 만들어진 산업용 헬멧은 ABS제의 것보다 내충격성이 37% 높고, 이 성능 차이가 공장에서의 채용을 가속시키고 있습니다. 파라계 아라미드를 사용한 내절창성 장갑은 레벨 5의 보호 성능을 30%의 경량화로 실현해, 연속 착용시의 쾌적성을 향상시키고 있습니다. 메타계 아라미드를 사용한 난연성 작업복은 425℃에서도 구조적 무결성을 유지하며, 보다 엄격한 주조 및 석유화학 안전 기준에 적합합니다. 이러한 이유로 이 지역에 제품을 공급하는 제조업체는 아라미드 원사와 직물 할당을 늘리고 아라미드 섬유 시장의 성장 프로파일을 강화하고 있습니다.

유럽 자동차 제조업체가 전기자동차의 항속 거리를 연장하기 위해 차체 질량을 줄이는 타이어 재 설계 프로그램을 가속. 아라미드로 강화된 타이어 카커스는 최대 25%의 경량화를 실현하고 그린딜의 운송의 탈탄소화 목표에 직결합니다. 1kg 삭감할 때마다 0.7km의 항속 거리 연장이 가능하기 때문에 OEM은 폴리에스터와 스틸 코드 대신 아라미드를 사용하게 됩니다. 컴파운드 제조업체는 구름 저항을 낮추면서도 내구성을 유지하는 아라미드 들어간 고무 믹스를 제품화하고 있어 유럽이나 곧 북미에서도 아라미드 섬유 시장 수요를 강화하고 있습니다.

원유 가격 상승과 지역 공급의 혼란은 MPD와 PPD의 비용 곡선을 상승시키고 생산자 마진을 압박하며 장기 계약을 불안하게 합니다. 미국 상무부는 방향족 디아민을, 지정학적으로 생산이 집중하는 화학적으로 중요한 원료의 하나로 꼽고 있어, 공급 안보상의 리스크를 높이고 있습니다. 제조업체는 바이오 중간체와 아라미드 스크랩의 폐쇄 루프 회수를 모색함으로써 대항하고 있지만, 눈앞의 변동이 여전히 아라미드 섬유 시장의 성장세를 깎고 있습니다.

2024년 아라미드 섬유 시장 점유율은 파라계 아라미드가 65%를 차지해 방탄, 항공우주, 마찰재 수요에 지지되었습니다. 파라계 아라미드 원사는 3.8GPa에 가까운 인장 강도를 가지며, 방호복이나 항공 벌집에서의 지위를 유지하고 있습니다. 미국의 국방 예산 증가와 경량 자동차 복합재료에 대한 새로운 관심으로 파라 계열 아라미드는 아라미드 섬유 시장에서 안정적인 수량 파이프라인을 확보하고 있습니다. 도레이의 한국 거점에서 3,000톤의 생산 능력 증강 등 대규모 투자는 이 섬유 클래스에 대한 자본 배분의 규모를 뒷받침하고 있습니다.

메타계 아라미드는 베이스는 작은 것, 2030년까지의 CAGR이 5.42%로 가장 빠른 궤도를 그리고 있습니다. 첨단 습식 방사 필라멘트는 현재 인장 강도가 1,255MPa에 이르며, 장시간의 자외선 노출 후에도 90% 이상의 강도를 유지하므로 송전선 커버와 같은 옥외 용도의 가능성이 넓어지고 있습니다. 메타계 아라미드는 난연성 직물, 절연지, 여과 백에 사용되어 전자, 산업 안전, 환경 보호에 있어서 열안정성의 요구에 부응하고 있습니다. 메타계 아라미드 섬유 시장 규모는 아시아 전역에서 반도체 생산 능력 확대와 EU의 녹색 전환 프로젝트에 의해 견조하게 확대될 것으로 예측되며 가격뿐만 아니라 소재의 특성이 고객의 전환을 결정한다는 경쟁력학이 형성되고 있습니다.

습식 방사는 2024년에 아라미드 섬유 시장 점유율의 60%를 차지했고, CAGR 5.87%로 계속해서 주요 시장을 상회합니다. 이 공정은 균질한 고분자 응고를 제공하고 전기 종이 및 여과 매체의 필수 조건인 높은 유전 안정성을 달성하는 균일한 밀도의 섬유를 생산합니다. 업그레이드된 솔벤트 재활용 모듈은 배출량과 비용을 절감하고 지속가능성을 중시하는 최종 사용자에게도 채택되었습니다. 습식 방적품의 아라미드 섬유 시장 규모는 전자화 및 필터 미디어 수요 증가에 따라 확대될 것으로 예측됩니다.

건조 제트 습식 방사는 연쇄 배향이 극단적인 인장 지표를 구동하는 파라계 아라미드에 여전히 필수적입니다. 폴리이미드 유사체의 실험은 최대 2.72GPa의 인장 강도와 114GPa를 초과하는 탄성률을 나타내며, 미래의 파라계 아라미드 강화를 위한 경로가 확인되었습니다. 전반적인 점유율은 작지만이 프로세스는 하이 엔드 발리 스틱 원사 공급을 지원하며 방위성과 고급 스포츠 용품 브랜드의 요구에 부합합니다. 처리량 효율과 용매 포착 기술을 목표로 한 지속적인 라인 업그레이드는 아라미드 섬유 시장에 대한 틈새 공헌을 보호할 것입니다.

2024년 아라미드 섬유 시장의 35%는 유럽이 차지했습니다. 엄격한 근로자 안전법, ISO에 준거한 화염 규격, 유럽 연합의 그린·딜이, 자동차나 산업 현장에서의 고가치 채용을 뒷받침하고 있습니다. 수출 지향 자동차 기반을 가진 독일이 이 지역의 수량 확대를 이끌고 프랑스와 네덜란드는 고도 여과와 항공우주용 라미네이트에 특화하고 있습니다. 전기자동차 배터리 공장에 대한 정부의 우대 조치는 고분자 복합재의 채택을 더욱 자극합니다.

북미는 2025-2030년의 CAGR이 5.34%로 가장 빠릅니다. 연방 국방 예산은 파라계 아라미드 탄도탄 재료의 지속적인 수요로 이어지는 반면, NASA와 민간 발사 공급자는 메타계 아라미드 열 차폐에 투자를 돌이킵니다. 미국의 통신 사업자는 허리케인의 영향을 받기 쉬운 복도를 가로지르는 항공 섬유 백본을 업데이트하고 폭풍우로 인한 손상을 줄이기 위해 아라미드 강도 부재를 지정합니다. 캐나다는 광업과 에너지 인프라를 중심으로 공공 안전에 중점을 둔 유사한 동향을 보여줍니다.

아시아태평양은 아라미드 섬유 시장의 다음 프론티어가 될 것입니다. 중국은 수입 의존도를 줄이기 위해 국내 생산을 확대하고 10년대 중반까지 파라아라미드 자급을 목표로 하고 있습니다. 스마트 공장, EV 배터리 공장 및 재생 가능 인프라의 대량 건설은 가볍고 내열성이 높은 소재에 대한 수요를 증가시킵니다. 일본과 한국은 반도체와 5G 하드웨어의 하이테크 전개에 연마를 가해 아라미드가 제공하는 유전 안정성과 기계적 탄력성이 필요합니다. 인도의 Make-in-India 방어 프로그램과 노동 안전 규범의 업데이트는 지역 PPE와 방어구 소비를 확대하고 지역 성장에 두께를 추가합니다.

The Aramid Fiber Market size is estimated at USD 4.30 billion in 2025, and is expected to reach USD 5.52 billion by 2030, at a CAGR of 5.10% during the forecast period (2025-2030).

Increasing penetration in automotive, aerospace, telecom, and advanced personal protective equipment elevates demand, while the fiber's strength-to-weight ratio and thermal stability anchor long-term relevance. Material-lightweighting targets in electric mobility, the build-out of 5G networks, and rising investment in hypersonic and space programs continuously widen commercial opportunities. At the same time, feedstock price swings, mainly for MPD and PPD, keep margins under pressure, prompting vertical-integration moves by large producers. Intellectual-property constraints further shape competitive dynamics, cementing the position of incumbents that can finance R&D and navigate cross-licensing frameworks.

Growing enforcement of industrial-safety rules in China, India, and emerging Southeast Asian economies is lifting orders for aramid-reinforced gloves, helmets, and heat-resistant workwear. Industrial helmets made with aramid composites show 37% higher impact resistance than ABS counterparts, a performance gap that accelerates factory adoption. Cut-resistant gloves incorporating para-aramid deliver Level 5 protection with 30% less weight, improving comfort for continuous wear. Fire-retardant workwear formulated with meta-aramid maintains structural integrity at 425 °C, aligning with stricter foundry and petrochemical safety codes. Manufacturers supplying this region therefore raise allocation for aramid yarns and fabrics, strengthening the growth profile of the aramid fiber market.

European automakers accelerate tire redesign programs that shave vehicle mass to extend electric-car range. Aramid-reinforced tire carcasses cut weight by up to 25%, a saving directly linked to the Green Deal's transport decarbonization targets . Every kilogram trimmed offers a 0.7 km range gain, motivating OEMs to substitute polyester or steel cords with aramid. Compounders are commercializing aramid-filled rubber mixes that lower rolling resistance yet keep durability, reinforcing demand for the aramid fiber market in Europe and soon North America.

Surging crude-oil swings and regional supply disruptions elevate MPD and PPD cost curves, compressing producer margins and unsettling long-term contracts. The U.S. Department of Commerce lists aromatic diamines among chemically critical inputs subject to geopolitically concentrated production, heightening supply-security risks . Manufacturers counter by exploring bio-based intermediates and closed-loop recovery of aramid scrap, yet near-term volatility still shaves growth momentum within the aramid fiber market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The para-aramid segment held a commanding 65% aramid fiber market share in 2024, supported by ballistic protection, aerospace, and friction-material demand. Para-aramid yarns deliver tensile strength near 3.8 GPa, sustaining their position in body armor and aviation honeycombs. Defense-budget uplifts in the United States and renewed interest in lightweight automotive composites ensure stable volume pipelines for para-aramid within the aramid fiber market. Significant investments, such as a 3,000-ton capacity addition at Toray's South Korea site, underscore the scale of capital allocation toward this fiber class.

Meta-aramid, while smaller in base, stages the fastest trajectory at a 5.42% CAGR through 2030. Advanced wet-spun filaments now reach 1,255 MPa tensile strength and retain over 90% strength after prolonged UV exposure, unlocking outdoor applications like transmission-line covers. Embedded in fire-retardant fabrics, insulation papers, and filtration bags, meta-aramid addresses thermal stability demands in electronics, industrial safety, and environmental protection. The aramid fiber market size for meta-aramid is forecast to expand steadily because of expanding semiconductor capacity across Asia and EU green-transition projects, setting a competitive dynamic where material attributes, not only price, decide customer conversion.

Wet spinning captured 60% of aramid fiber market share in 2024 and continues to out-pace the headline market with a 5.87% CAGR. The process offers homogeneous polymer coagulation, producing uniformly dense fibers that achieve high dielectric stability, a prerequisite for electrical papers and filtration media. Upgraded solvent-recycling modules reduce emissions and cost, supporting adoption even among sustainability-minded end-users. The aramid fiber market size for wet-spun output is projected to widen in line with electrification and filter-media demand growth.

Dry-jet wet spinning remains indispensable for para-aramid where chain orientation drives extreme tensile metrics. Lab runs of polyimide analogues display tensile strength up to 2.72 GPa and modulus above 114 GPa, confirming pathway headroom for future para-aramid enhancement. Although overall share is smaller, the process anchors high-end ballistic yarn supply, aligning with the needs of defense ministries and premium sports-equipment brands. Continuous line upgrades aimed at throughput efficiency and solvent-capture technology will safeguard its niche contribution to the aramid fiber market.

The Aramid Fiber Market Report Segments the Industry by Product Type (Para-Aramid, Meta-Aramid), Spinning Process (Wet Spinning, Dry Wet Spinning), Application (Security and Protection Equipment, Frictional and Brake Materials, and More), End-User Industry (Safety and Protection Equipment, Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe anchors the global aramid fiber market with 35% revenue in 2024. Stringent worker-safety laws, ISO-aligned flame standards, and the European Union's Green Deal propel high-value adoption in automotive and industrial settings. Germany, with its export-oriented automotive base, leads regional volume expansion, while France and the Netherlands specialize in advanced filtration and aerospace laminates. Government incentives for electric-vehicle battery plants further stimulate polymer-composite uptake.

North America posts the fastest CAGR at 5.34% for 2025-2030. Federal defense appropriations feed continuous demand for para-aramid ballistic materials, whereas NASA and private launch providers channel investments into meta-aramid thermal shields. U.S. telecom carriers renew aerial fiber backbones across hurricane-prone corridors, specifying aramid strength members to mitigate storm damage. Canada follows similar trends with a public-safety focus, particularly in mining and energy infrastructure.

Asia-Pacific represents the next frontier of scale for the aramid fiber market. China escalates domestic output to cut reliance on imports and targets self-sufficiency in para-aramid by mid-decade. Massive construction of smart factories, EV battery plants, and renewable infrastructure multiplies demand for lightweight, heat-resistant materials. Japan and South Korea refine high-tech deployment in semiconductors and 5G hardware, requiring dielectric stability and mechanical resilience that aramid delivers. India's Make-in-India defense program and updated occupational-safety codes build local PPE and armor consumption, adding depth to regional growth.