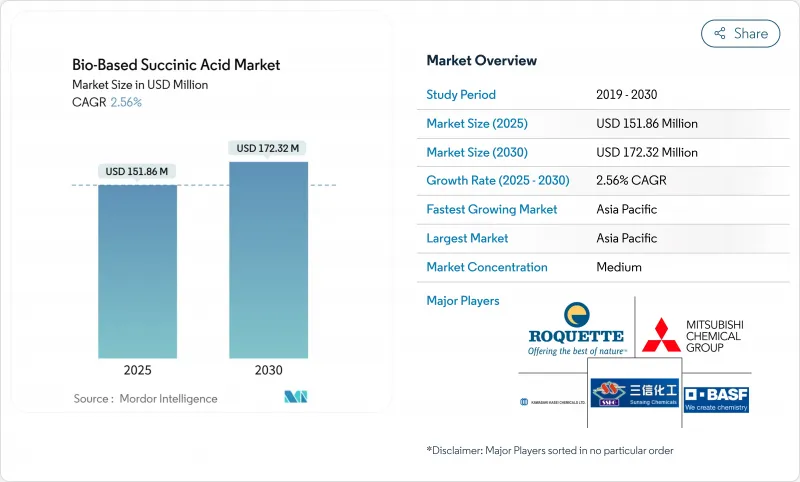

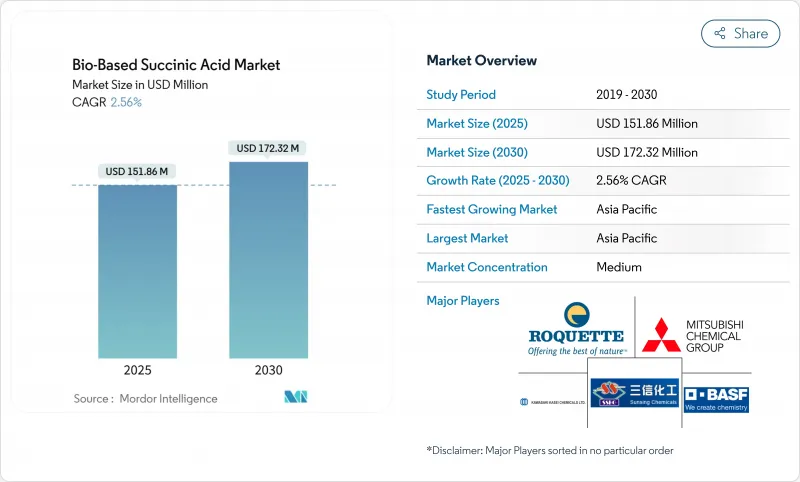

바이오 기반 숙신산 시장 규모는 2025년에 1억 5,186만 달러로 추정되고, 2030년에는 1억 7,232만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 2.56%를 나타낼 전망입니다.

바이오 기반 숙신산 시장은 발효 효율의 향상, 원료 옵션의 다양화, 강하 용도의 확대에 의해 석유 루트와의 가격 갭은 여전히 존재하는 것, 수요는 전진을 계속하고 있습니다. 폴리부틸렌 석시네이트(PBS)와 폴리우레탄 체인에는 이 분자가 대량으로 사용되기 때문에 산업용 고분자 제조업체는 여전히 중심적인 구매자입니다. 지역 확대는 정책과 밀접하게 관련되어 있습니다. 아시아태평양은 중국의 바이오 제조업 투자와 일본의 탈탄소화 로드맵을 배경으로 가속화되고 있는 한편, 유럽의 성장은 낮은 실적 중간체에 보상하는 탄소 가격 제도에 기인하고 있습니다. 경쟁의 치열성은 모든 생산자들이 결정적인 비용 우위를 아직 지배하지 않았기 때문에 스케일업 협력, 원료 헤지, 지속가능성 주장을 검증하기 위한 엄격한 인증 캠페인을 촉구하고 있기 때문에 멈추고 있습니다.

엔지니어링 플라스틱, 열경화성 수지 및 엘라스토머 제조업체는 화석 원료를 인증된 바이오 대체품으로 계속 전환하고 있습니다. BASF는 60개 이상의 포트폴리오 제품으로 ISCC 인증을 받았으며 재생가능 성분을 40% 함유하는 바이오 아크릴산에틸을 발표했습니다. 폴리우레탄 체인에서는 숙신산 발효로부터 직접 얻은 바이오-1,4-부탄디올을 이용하는 노력이 병행하여 진행되고 있습니다. 이 경로는 제노마티카사가 개척하여 중국 제조업자에게 기술공여를 통해 더욱 규모를 확대한 것입니다. PBS 수지는 이미 숙신산과 1,4-부탄디올로부터 합성되었기 때문에 숙신산의 생산량이 증가할 때마다 포장, 멀티필름, 일회용 가전 부품에 파급됩니다. 브랜드 소유자가 스코프 3의 탈탄소화 목표를 확대함에 따라 조달팀은 온실가스 감축을 문서화할 수 있는 공급업체를 선호하고 있으며, 바이오 기반 숙신산 시장이 대량 생산 폴리머 용도에 끌리는 경향이 커지고 있습니다.

원유가격 변동이 배럴당 80달러를 초과하면 석유화학제품인 숙신산의 비용 우위성이 정기적으로 손상되기 때문에 컨버터 각사는 원료가격 변동으로부터 면한 바이오루트의 인수계약을 체결할 수밖에 없게 됩니다. 유럽위원회의 산업 탄소 관리 계획은 자본 보조금과 세액 공제를 화석 중간체를 대체하는 프로젝트에 맞추어 이 경제적 뒷받침을 보완합니다. 일본의 대기업인 미쓰비시화학, 미쓰이화학, 아사히카세이는 바이오매스나프타를 나프타 크래커로 시용함으로써 변동성을 경감하면서 각국의 넷 제로 서약을 달성함으로써 대응하고 있습니다. 원유안의 국면에서는 일시적으로 기세가 약해질 수도 있지만, 구매부문은 확률가중의 원유궤도를 할당한 총소유비용 시나리오를 모델화하는 것이 늘어나고 있으며, 원유가 약한 예측이라도 바이오 기반 숙신산 시장의 전략적 쐐기를 유지할 수 있습니다.

기술경제모델에서는 상업용 바이오 기반 숙신산의 가격 하한을 현재의 공공요금으로 킬로그램당 2.5-2.7달러 사이로 하고 있으며 이는 원유안 시나리오에서 석유 유래 동등품의 스팟 가격을 아직 웃도는 대역입니다. 이 델타는 살균 에너지 수요, 다단계 침전 및 스테인레스 스틸 발효조의 자본 집약도에서 비롯됩니다. 탄소 부과금과 프리미엄 틈새는 스프레드를 부분적으로 상쇄하는 것, 수지와 코팅의 대용량 사용자는 여전히 가격에 민감합니다. 공정 강화 - 연속 발효, in-situ 생성물 제거, 낮은 pH 내성 미생물은 유망하지만, 동등하게 하기 위한 스케줄은 이러한 기술을 파일럿으로부터 50킬로톤의 명판 능력까지 가속시키는지에 달려 있습니다.

2024년의 바이오 기반 숙신산 시장 점유율의 43.18%는 산업 용도이며, PBS 포장용 필름, 생분해성 멀티, 폴리우레탄 중간체 등이 그 중심이 되었습니다. 컨버터 각 회사는 플랜트 부하율을 뒷받침하는 다년간의 테이크 오어 페이 계약을 맺고 있기 때문에 이러한 채널 수요는 예측대로 확대되어 바이오 기반 숙신산 시장 전체를 안정시키고 있습니다. 예측 기간 동안 퍼스널케어는 CAGR 3.79%와 가장 날카로운 성장 곡선을 그려 리브 온 여드름 치료, 내추럴 데오도란트, 마일드 익스포리언트 등의 특수 포맷이 공헌합니다. 피부과학 연구에서는 1% 숙신산 겔이 자극을 일으키지 않고 프로피오니박테리움 아크네스의 증식을 억제하는 것으로 확인되었으며, 브랜드는 기존의 β-하이드록시산과 함께 보다 친환경적인 활성제를 위치시킬 수 있습니다. 한편, 코팅제 제조업체는 고고형분이면서 생분해성을 확보할 수 있는 숙신산계 폴리올을 시험하고 있습니다.

양적 확대와 병행하여 가격도 최종 시장에 따라 크게 다릅니다. 산업용 수지의 바이어는 톤당의 관세를 낮추는 협상을 실시하면서도, 안정된 인수를 실시했습니다. 개인 관리 및 의약품 사용자는 미생물 학적 순도 및 추적 가능성 요구 사항에서 할인을 받아들이고 생산자에게 마진 위험 회피를 제공합니다. 이러한 역학은 조기 채용자가 기준 생산 능력을 폴리머에 할당하고 특수 배치를 위해 업그레이드 된 발효기를 소비하는 듀얼 채널 모델을 촉진합니다. 각 다운스트림 섹터가 라이프사이클 평가 지표를 선호하기 때문에 부문 교차 시너지 효과가 발생합니다. 예를 들어, 의약품으로 검증된 증명서는 화장품의 주장에 신뢰성을 부여하고, 포장의 기계적 재활용성 시험은 소비재의 소유자에게 라이프사이클 종료시의 결과가 순환형 경제의 공약에 따른 것임을 안심시킵니다. 이러한 패턴을 종합하면 바이오 기반 숙식산 시장 전체의 수익 안정성을 확대하는 데 있어서 용도의 다양성이 중심적인 역할을 하고 있음을 확인할 수 있습니다.

아시아태평양이 가장 규모가 큰 지역 슬라이스를 차지하고, 2024년에는 바이오 기반 숙신산 시장의 32.75%를 차지했고, 2030년까지의 CAGR은 3.70%를 나타낼 전망입니다. 중국의 정부는 저이자 대출을 산업 바이오 파크에 흘려 석신산과 1,4-부탄디올 전용 50킬로톤 발효기의 신속한 규모를 높일 수 있습니다. 국가발전개혁위원회는 바이오케미칼을 5개년 계획의 우대조치에 통합하고 현금비용의 손익분기점을 낮추는 세제우대조치를 추가하고 있습니다. 일본에서는 탄소중립을 위한 녹색성장 전략으로 바이오매스나프타 공처리에 보조금이 할당되어 미쓰비시화학, 미쓰이화학, 아사히카세이가 숙신산 기반 폴리에스터에 공급하는 파일럿 크래커에 공동 투자하도록 촉구하고 있습니다. 한국은 바이오전략기술청사진을 통해 비슷한 야심을 지원하고 있으며 인도는 당화 스트림을 화학발효조로 전환할 수 있는 파쇄미 에탄올 프로그램을 확대함으로써 원료 공급에 중점을 두고 있습니다. 이러한 이니셔티브를 종합하면 정책 지원과 규모의 경제성을 결합하여 아시아태평양의 바이오 기반 숙식산 시장에서의 리더십을 강화할 것입니다.

북미는 첨단 합성 생물학 클러스터, 고위험 벤처 자금, 주 수준의 청정 연료 장려책을 통해 견조한 활동을 유지하고 있습니다. 미국 농무부는 2025년 바이오매스 연구개발 아젠다에서 숙신산을 우선도가 높은 제품으로 자리매김하고 균주공학과 폐기물류의 가치화를 위한 보조금 풀을 개방하고 있습니다. 캘리포니아의 저탄소 연료 기준은 생물 기원의 CO2 이용에 대한 신용 배율을 부여하는 것으로, 발효 공장이 탄소 포집 장치를 통합할 때 추가 수입을 얻기 위해 활용할 수 있는 구조입니다. 그린 플레인즈의 클린 슈가 자회사가 네브라스카의 계약 발효자가 현재 시험하고 있는 원료인 포도당의 이산화탄소 배출량을 40% 삭감할 수 있음을 실증했습니다. 캐나다에서는 바이오케미칼에 사용되는 설비에 가속상각이 적용되고, 멕시코에서는 북부의 산업회랑을 촉진하기 위해 바이오중간체에 대한 이권이 평가되고 있습니다. 이러한 정책과 인프라를 종합하면 이 지역 내에서 바이오 기반 숙식산 시장의 꾸준한 확대를 지원하는 비옥한 생태계가 형성됩니다.

유럽의 궤도는 석유화학제품 생산량 1톤당 탄소 비용을 통합하는 규제 강화에 달려 있습니다. 유럽 위원회의 2040년 기후 중립 로드맵은 탄소 포집 및 이용 제품을 공공 조달의 우선적인 대상으로 삼고 있습니다. 독일의 국가 바이오 이코노미 전략은 로이나와 같은 화학 공원에 사탕수수 잔여물을 통합하기 위해 R&D 보조금과 원료 물류 프로그램을 보완합니다. 프랑스에서는 소비재의 탄소 실적 표시를 시험적으로 실시하여 검증된 저배출 중간체에 대한 수요를 높이고 있습니다. 영국의 차금 결제 제도(Contracts for Difference) 스타일의 산업용 탄소 제거를 위한 메커니즘은 지불 플로어를 보장하고 발효 공장이 북해의 격리 우물과 함께 거주하도록 장려하고 있습니다. 생산 비용은 아시아의 평균을 초과하지만 브랜드 소유자의 압력과 녹색 금융 수단에 대한 접근이 경쟁력을 유지하고 있습니다. 그 결과 유럽은 바이오 기반 숙식산 시장의 주요 프리미엄 시장으로 운영되어 고순도 등급과 특수 수량을 흡수하고 높은 가격 설정을 정당화하고 있습니다.

The Bio-Based Succinic Acid Market size is estimated at USD 151.86 million in 2025, and is expected to reach USD 172.32 million by 2030, at a CAGR of 2.56% during the forecast period (2025-2030).

The bio-based succinic acid market has entered a measured maturation phase in which incremental fermentation efficiencies, diversified feedstock options, and expanding downstream uses keep demand advancing even though price gaps versus petro-routes persist. Industrial polymer makers remain the anchor buyers because polybutylene succinate (PBS) and polyurethane chains incorporate high volumes of the molecule, while personal-care and pharmaceutical formulators are scaling adoption to capture its multifunctional antimicrobial and pH-buffer benefits. Regional expansion is tied closely to policy: Asia-Pacific accelerates on the back of China's biomanufacturing investments and Japan's decarbonization roadmap, whereas Europe's growth stems from carbon-pricing schemes that reward low-footprint intermediates. Competitive intensity stays elevated because no producer yet controls a decisive cost advantage, prompting scale-up collaborations, feedstock hedging, and rigorous certification campaigns to validate sustainability claims.

Manufacturers of engineering plastics, thermoset resins, and elastomers continue to swap fossil building blocks for certified bio-alternatives. BASF secured ISCC+ certification for more than 60 portfolio products and introduced a bio-based ethyl acrylate featuring 40% renewable content that cuts cradle-to-gate emissions by 30%. Parallel initiatives in polyurethane chains rely on bio-1,4-butanediol derived directly from succinic acid fermentations, a pathway pioneered by Genomatica and scaled further through technology licensing to Chinese producers. Because PBS resin is already synthesized from succinic acid and 1,4-butanediol, every incremental gain in succinate output ripples through packaging, mulch film, and single-use appliance parts. As brand owners escalate scope-3 decarbonization targets, procurement teams favor suppliers able to document greenhouse-gas savings, reinforcing the pull on the bio-based succinic acid market toward high-volume polymer applications.

Oil-price swings above the USD 80 per-barrel threshold regularly erode the cost advantage enjoyed by petrochemical succinic acid, nudging converters to lock in offtake agreements for bio-routes that insulate them from feedstock shocks. The European Commission's industrial carbon-management plan complements this economic push by aligning capital grants and tax credits with projects that displace fossil intermediates. Japanese majors Mitsubishi Chemical, Mitsui Chemicals, and Asahi Kasei have responded by trialing biomass naphtha in naphtha crackers to derisk volatility while meeting national net-zero pledges. Although low oil phases can stall momentum temporarily, purchasing departments increasingly model total-cost-of-ownership scenarios that assign probability-weighted oil trajectories, keeping a strategic wedge for the bio-based succinic acid market even under bearish crude forecasts.

Techno-economic models place the price floor for commercial bio-based succinic acid between USD 2.5 and 2.7 per kilogram at today's utility tariffs, a band still above the spot price of petro-derived equivalents in low-oil scenarios. The delta stems from sterilization energy demand, multi-step precipitation, and the capital intensity of stainless-steel fermenters. While carbon levies and premium niches partially offset the spread, large-volume users in resins and coatings remain price sensitive. Process intensification-continuous fermentation, in-situ product removal, and low-pH tolerant microbes-holds promise, but the timeline for parity hinges on accelerating these technologies from pilot to 50 kiloton nameplate capacity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Industrial uses captured 43.18% of the bio-based succinic acid market share in 2024, anchored by PBS packaging films, biodegradable mulch, and polyurethane intermediates that together consume multi-kiloton volumes. Demand in these channels scales predictably because converters sign multi-year take-or-pay contracts that underpin plant-load factors, thereby stabilizing the overall bio-based succinic acid market. Over the forecast horizon, personal care presents the sharpest growth curve at a 3.79% CAGR, lifting contribution from specialty formats such as leave-on acne treatments, natural deodorants, and mild exfoliants. Dermatology studies confirm that 1% succinic acid gels diminish Propionibacterium acnes proliferation without triggering irritation, which allows brands to position greener actives alongside existing beta-hydroxy acids. Pharmaceutical uptake continues steadily as formulators incorporate succinate buffers to maintain pH in controlled-release matrices, while coatings makers experiment with succinate-based polyols that give high-solids content yet ensure biodegradability.

Parallel to volume expansion, price realization differs widely among end markets. Industrial resin buyers negotiate lower per-tonne tariffs yet provide consistent offtake. Personal care and pharmaceutical users accept a premium due to microbiological purity and traceability requirements, creating a margin hedge for producers. These dynamics encourage a dual-channel model in which early adopters allocate baseline capacity to polymers and consume upgraded fermenter runs for specialty batches. Because each downstream sector prioritizes life-cycle-assessment metrics, cross-segment synergies emerge: credentials validated in medicine lend credibility to cosmetic claims, while mechanical recyclability tests in packaging reassure consumer-goods owners that end-of-life outcomes align with circular-economy pledges. Together, these patterns affirm the central role of application diversity in extending revenue stability across the bio-based succinic acid market.

The Bio-Based Succinic Acid Market Report is Segmented by Application (Industrial, Pharmaceuticals, Personal Care, Paints and Coatings, Other Applications), Feedstock Source (Corn-Derived Glucose, Sugarcane & Beet Sucrose, Lignocellulosic Biomass, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific owned the largest regional slice, representing 32.75% of the bio-based succinic acid market in 2024 and cruising toward a 3.70% CAGR through 2030. China's provincial governments funnel low-interest loans into industrial-biotech parks, enabling rapid scale-up of 50 kiloton fermenters dedicated to succinic acid and 1,4-butanediol. The National Development and Reform Commission integrates bio-chemicals into its Five-Year Plan incentives, adding tax holidays that lower cash-cost breakevens. In Japan, the Green Growth Strategy for Carbon Neutrality allocates subsidies for biomass naphtha co-processing, prompting Mitsubishi Chemical, Mitsui Chemicals, and Asahi Kasei to co-invest in pilot crackers that will feed succinate-based polyesters. South Korea supports similar ambitions through its Bio-Strategic Technology blueprint, while India focuses on feedstock supply by expanding broken-rice ethanol programs that could divert saccharified streams into chemical fermenters. Altogether, these initiatives compound policy support with scale economies, reinforcing Asia-Pacific's leadership in the bio-based succinic acid market.

North America sustains robust activity through advanced synthetic-biology clusters, risk-tolerant venture funding, and state-level clean-fuel incentives. The United States Department of Agriculture frames succinic acid as a high-priority product in its 2025 Biomass Research and Development Agenda, unlocking grant pools for strain engineering and waste-stream valorization. California's Low Carbon Fuel Standard awards credit multipliers to biogenic CO2 utilization, a mechanism that fermentation plants leverage for additional revenue when they integrate carbon capture units. Green Plains' clean-sugar subsidiary demonstrated 40% lower carbon footprint dextrose, a feedstock now trialed by contract fermenters in Nebraska. Canada provides accelerated depreciation for equipment deployed in biochemicals, and Mexico evaluates concessions for bio-intermediates to spur northern industrial corridors. Collectively, these policy and infrastructure elements create a fertile ecosystem that underpins steady expansion of the bio-based succinic acid market within the region.

Europe's trajectory hinges on regulatory stringency that embeds carbon costs into every tonne of petrochemical output. The European Commission's 2040 climate-neutral roadmap positions carbon-capture-and-utilization products for priority offtake in public procurement. Germany's National Bioeconomy Strategy supplements R&D grants with feedstock logistics programs to integrate sugar-beet residues into chemical parks such as Leuna. France pilots carbon-footprint labeling on consumer goods, elevating demand for verified low-emission intermediates. The United Kingdom's Contracts for Difference-style mechanism for industrial carbon removal assures payment floors, encouraging fermentation plants to co-locate with sequestration wells in the North Sea. While production costs exceed Asian averages, brand-owner pressure and access to green-finance instruments maintain competitive momentum. Consequently, Europe operates as the principal premium market within the bio-based succinic acid market, absorbing high-purity grades and specialty volumes that justify elevated pricing.