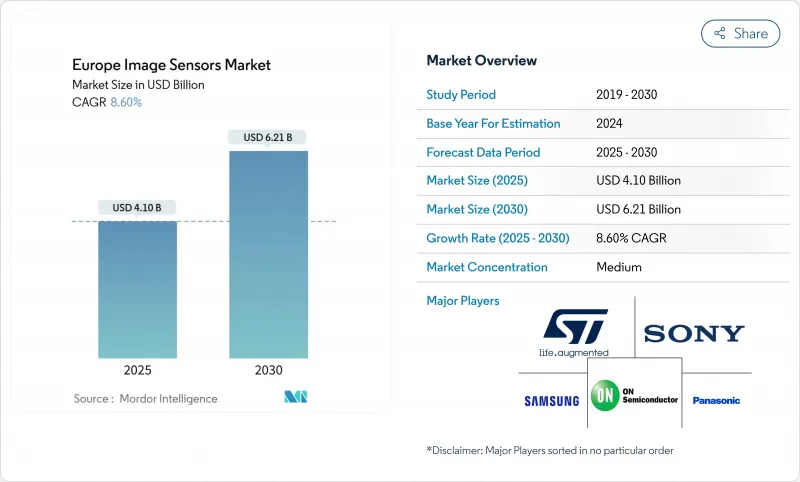

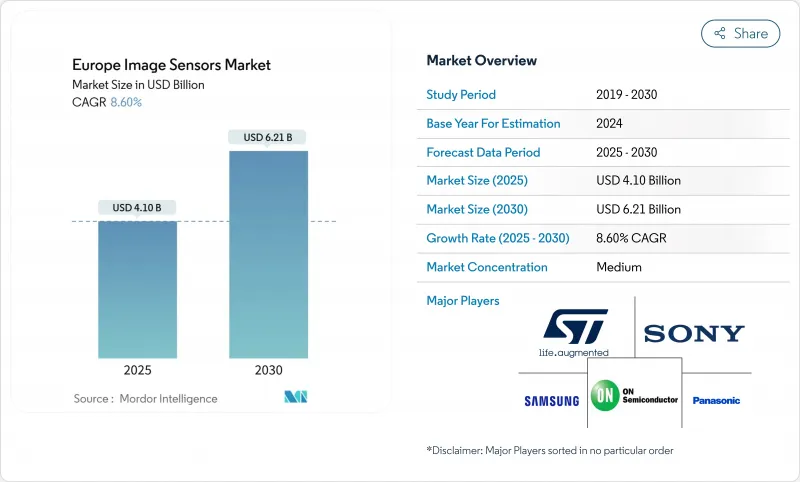

유럽의 이미지 센서 시장은 2025년에 41억 달러, 2030년에는 62억 1,000만 달러에 이를 것으로 예측되며 CAGR은 8.66%를 나타낼 전망입니다.

자동차 안전성에 대한 수요 증가, 스마트폰 카메라 기술 혁신, EU의 반도체 재쉐어링 정책이 결합되어 가치창조는 소비자용 전자기기에서 고신뢰성 자동차 및 산업용 틈새 시장으로 전환하고 있습니다. 웨이퍼 레벨 광학 적층 CMOS 이미징 센서(CIS) 아키텍처와 양자점 재료는 폼 팩터를 슬림하게 유지하면서 성능의 상한을 높입니다. 지역 기업은 자동차 제조업체 및 산업용 OEM에 가깝다는 장점을 활용하여 먼 공급업체보다 신속하게 기능 안전 요구 사항을 검증할 수 있습니다. 동시에 리소그래피 툴을 둘러싼 수출 규제의 불확실성과 유럽의 에너지 가격 상승이 당면 생산능력 확대를 억제하고 기술적 리더십이 비용을 능가하는 프리미엄 부문을 우선시합니다.

유럽 브랜드는 아시아 라이벌에 대응하기 때문에 센서 해상도를 200MP 이상으로 늘립니다. 픽셀 비닝에 의해 파일 사이즈를 증대시키는 일 없이 저조도로의 촬영 결과를 개선해, 웨이퍼 레벨의 광학계에 의해 카메라의 단차를 억제. 옴니비전의 0.56µm 픽셀은 기술적 실현 가능성을 증명하고 열 관리의 절충을 강조합니다. 디바이스 제조업체는 현재 까다로운 폼 팩터로 광학, DSP 및 AI 파이프라인을 공동 설계하는 유럽 패키징 전문가를 높이 평가했습니다. 알고리즘이 성숙하고 비용 곡선이 구부러짐에 따라 2026년부터 채용이 확대됩니다.

유로 NCAP의 별 평가 시스템의 갱신에 의해 2026년 이후에 발매되는 신형차에서는 자동 긴급 브레이크에 전방 카메라의 탑재가 의무화됩니다. 이 규칙은 자전거 및 보행자 감지에도 적용되며 센서 해상도와 동적 범위의 목표 값을 높입니다. OnSemi의 Hyperlux 제품군은 눈부신 도로 장면에 맞게 조정된 150dB HDR을 제공하여 독일과 이탈리아의 OEM 검증 시간을 단축하고 있습니다. 유럽의 Tier-1 공급업체는 테스트 트럭과 규제 기관에 지리적으로 가깝다는 장점이 있어 프로토타입에서 대량 생산까지의 루프 시간을 단축할 수 있습니다.

유럽의 전기 요금과 초순수 요금은 아시아 평균을 30-50% 웃돌고 있습니다. 탄소 중립성의 서약으로 인해 공장은 재생 가능 전력 계약과 HVAC 업그레이드 선불을 강요합니다. 2027년까지 탄소 중립을 달성하는 ST 마이크로 일렉트로닉스의 로드맵은 자본의 발판을 보여줍니다. 이러한 오버헤드를 채우기만 하는 생산량이 없는 소규모 주조소는 철수하거나 패브라이트 모델로 축발을 옮기는 것입니다. 유럽의 이미지 센서 시장 기업은 단기 마진 압박을 목격하면서도 ESG를 중시하는 구매자로부터의 평판을 높여가고 있습니다.

CMOS 센서는 저소비 전력과 로직의 통합을 배경으로 2024년 유럽의 이미지 센서 시장 점유율의 86.30%를 획득했습니다. 움직임이 많은 자동차와 로봇에 필수적인 세계 셔터형은 CAGR 9.30%로 추이하고 있으며, 2030년까지 유럽의 이미지 센서 시장에서 큰 점유율을 차지합니다. 롤링 셔터 CMOS는 가격에 민감한 휴대폰과 노트북에 적합하지만 CCD는 초저잡음이 중요한 과학적 틈새 시장으로 물러났습니다.

유럽 기업은 자동차 제조업체와의 긴밀한 관계를 활용하여 ASIL-B 인증을 받은 세계 셔터 부품을 공동 설계하고 Euro NCAP의 2026년 모델로 조기 설계 승리를 획득합니다. 웨이퍼 레벨 광학 부품 및 딥 트렌치 절연은 다이 크기를 증가시키지 않고 양자 효율을 향상시킵니다. 그 결과, 세계 셔터 디바이스의 유럽의 이미지 센서 시장 규모는 견조하게 확대되고, 소비자 사이클이 연화해도 지역의 수익 회복력을 높일 것으로 예측됩니다.

25-64MP 클래스가 2024년에 28.44%의 점유율로 매출을 이끌어, 파일 사이즈의 경제성과 계산 워크로드의 밸런스를 취했습니다. 그러나 200MP를 초과하는 부품은 CAGR 12.33%로 증가하고 무손실 디지털 줌과 8K 비디오 자르기를 판매하는 플래그쉽 휴대폰에 의해 뒷받침됩니다. 이러한 초해상도 디바이스의 유럽 이미지 센서 시장 규모는 픽셀 비닝 알고리즘의 성숙과 함께 2025-2030년에 가장 빠르게 확대됩니다.

웨이퍼 레벨의 광학 부품과 서브 μm 픽셀을 정합시키는 첨단 패키징이 렌즈 수차를 억제해, 유럽의 모듈 제조업체가 프리미엄 핸드셋 SKU에 진입할 수 있게 됩니다. 유럽의 이미지 센서 시장에서는 OEM 제조업체가 특수 유리와 IR 필터를 국내에서 조달하고 아시아 공급 충격에 대비하는 것으로 관측되고 있습니다. 엔트리 레벨 모바일 단말기는 여전히 8MP 미만의 칩에 의존하고 있으며, 롤링 셔터의 대량 생산의 밑바닥이 되고 있습니다.

The Europe image sensors market stands at USD 4.1 billion in 2025 and is projected to reach USD 6.21 billion by 2030, reflecting an 8.66% CAGR.

Pent-up automotive safety demand, smart-phone camera innovation and EU semiconductor re-shoring policies combine to move value creation from consumer electronics toward high-reliability automotive and industrial niches. Wafer-level optics stacked CMOS imaging sensor (CIS) architectures and quantum-dot materials increase performance ceilings while keeping form factors slim. Regional players leverage proximity to automakers and industrial OEMs to validate functional-safety requirements faster than distant suppliers can. At the same time, export-control uncertainty around lithography tools and high European energy prices temper near-term capacity expansion, pushing firms to prioritize premium segments where technical leadership outweighs cost.

European brands escalate sensor resolution beyond 200 MP to counter Asian rivals. Pixel-binning improves low-light results without ballooning file sizes, while wafer-level optics keeps camera bumps in check. OmniVision's 0.56 µm pixels prove technical feasibility and highlight thermal-management trade-offs. Device makers now value European packaging specialists that co-design optics, DSP and AI pipelines in tight form factors. Adoption is set to widen from 2026 as algorithms mature and cost curves bend.

Euro NCAP's updated star-rating system makes forward-facing cameras compulsory for Automatic Emergency Braking across new models launched from 2026. The rule extends to cyclist and pedestrian detection, increasing sensor resolution and dynamic-range targets. OnSemi's Hyperlux family delivers 150 dB HDR tuned for glare-filled road scenes, lowering validation time for German and Italian OEMs. European tier-1 suppliers benefit from geographical proximity to test tracks and regulatory bodies, shortening loop times between prototype and series production.

Electricity and ultra-pure water bills in Europe sit 30-50% above Asian averages. Carbon-neutrality pledges force fabs to pre-pay for renewable power contracts and HVAC upgrades. STMicroelectronics' roadmap to reach carbon neutrality by 2027 exemplifies the capital drag. Smaller foundries lacking volume to offset these overheads either exit or pivot to fab-lite models. Europe image sensors market players see near-term margin squeeze yet gain reputational leverage with ESG-focused buyers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

CMOS sensors captured 86.30% of Europe image sensors market share in 2024 on the back of lower power draw and logic integration. Global-shutter variants, vital for motion-heavy automotive and robotics tasks, are pacing at 9.30% CAGR and will command a larger slice of the Europe image sensors market by 2030. Rolling-shutter CMOS stays relevant for price-sensitive phones and laptops, while CCD retreats into scientific niches where ultra-low noise still matters.

European firms exploit close ties with automakers to co-design ASIL-B qualified global-shutter parts, gaining early design-wins for Euro NCAP 2026 models. Wafer-level optics and deep-trench isolation raise quantum efficiency without inflating die size. Consequently, Europe image sensors market size for global-shutter devices is projected to climb steadily, lifting regional revenue resilience even if consumer cycles soften.

The 25-64 MP class led revenue with 28.44% share in 2024, balancing file-size economy and computational workload. However, >200 MP parts rise at 12.33% CAGR, fuelled by flagship phones that tout lossless digital zoom and 8K video crops. Europe image sensors market size for these ultra-resolution devices will expand fastest in 2025-2030 as pixel-binning algorithms mature.

Packaging advances that align wafer-level optics with sub-µm pixels curb lens aberration, letting European module makers enter premium handset SKUs. The Europe image sensors market observes OEMs procuring specialty glass and IR filters domestically to hedge against Asian supply shocks. Entry-level handsets still rely on <=8 MP chips, keeping a floor under high-volume rolling-shutter production.

The Europe Image Sensors Market is Segmented by Type (CMOS, CCD), Resolution (<= 8 MP, 9 - 24 MP and More), Spectrum (Visible (RGB), Near-Infrared (NIR) and More), Shutter Technology, End-User Industry (Consumer Electronics, Healthcare, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).