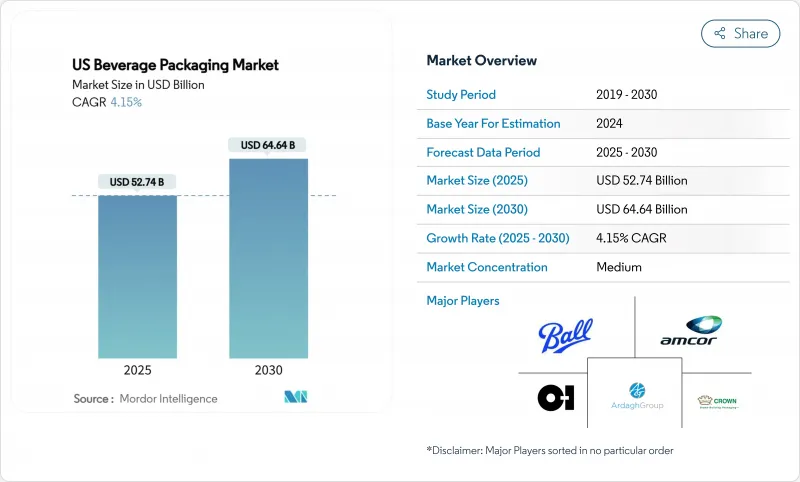

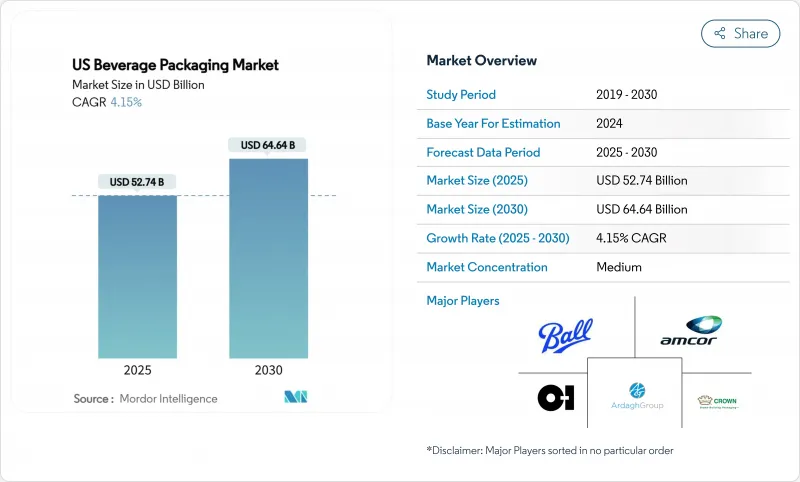

미국의 음료 포장 시장은 2025년에 527억 4,000만 달러에 이르고, 2030년에는 646억 4,000만 달러로 확대되어 CAGR 4.15%를 나타낼 것으로 예상됩니다.

꾸준한 가치 성장은 지속가능성 규제의 강화, 재활용 함량의 의무화, 재활용이 용이한 형식으로 소비자의 선호에 따른 알루미늄 중심의 전략에 의해 뒷받침됩니다. 브랜드 소유자는 포장을 이산화탄소 삭감 목표를 위한 비용 효과적인 테코로 취급하고 있으며, 경량 금속 용기와 고 배리어성 플렉서블 필름에 대한 수요를 촉진하고 있습니다. 볼사가 2025년 1월에 12온스 캔에 부과한 급여와 같은 공급업체의 가격 대책과 최소 주문량 인상은 공예 맥주 생산자의 비용 곡선의 형태를 계속 변화시켜 주요 음료 제조업체와 소규모 음료 제조업체 간의 격차를 넓히고 있습니다. RTD(즉석 음용) 커피, 에너지 음료, 기능성 음료의 병행 확대로 다층 플라스틱 병에서 알루미늄 캔과 고급 그래픽의 슬림 병으로의 전환이 가속화되고 있습니다. 마지막으로 전자상거래의 성장으로 2차 골판지를 제거하고 파손을 줄이고 새로운 프리미엄화의 길을 여는 '쉽 인 오운 컨테이너' 형식의 설계가 뒷받침되고 있습니다.

캘리포니아의 AB793은 2022년 PET 음료 용기의 재생 이용률을 15%, 2030년까지 50%로 끌어올리기로 결정했으며, 뉴욕, 뉴저지, 매사추세츠 주 의원이 적극적으로 검토하고 있는 청사진을 보여주었습니다. 재생 PET는 버진 수지에 비해 15-25%의 비용 프리미어가 있어, 각 브랜드는 용기 1개당 8-12%의 폴리머 사용량을 삭감하는 경량화에 대한 투자를 강요하고 있습니다. PepsiCo는 일부 물 라인에서 100% rPET로 전환하여 선반의 무결성을 유지하면서 이산화탄소 배출량을 31% 줄였습니다. 컴플라이언스 주도의 라인 리노베이션은 물류 및 가공 오버헤드를 1개당 0.03-0.08달러 추가하지만, 브랜드는 저탄소 포장을 팔아 5-8%의 가격 상승을 획득하고 있습니다.

RTD 에너지 음료는 편의점의 RTD 매출의 37%를 차지하며 2020년의 28%에서 증가했으며 거의 모든 주요 신제품이 알루미늄 형식을 사용합니다. 몬스터 비벌리지는 세계 판매량의 97%를 알루미늄 용기에서 얻고 있으며, 프리미엄 가격 설정에 의해 상품 인플레이션을 상쇄하면서 2025년 순매출 71억 달러를 가능하게 하고 있습니다. 알루미늄의 빛과 산소를 차단하는 특성은 커피의 아로마와 기능성 성분의 안정성을 유지하고, 냉각 유통 없이 유통 기한을 연장하고, 콜드체인 비용을 최대 30% 삭감하는 데 도움이 됩니다. 2018년부터 2023년까지 새로운 RTD 커피의 스톡 유지 유닛(SKU)은 73% 증가했으며, 그중 60%는 풍미 유지와 장식의 다양성에서 캔을 사용했습니다.

단량체 가격 변동, 특히 에틸렌과 파라크실렌은 멕시코 걸프 스팟 시장에서 정기적으로 25-30 c/lb에 이르며, 병 식수 및 탄산음료(CSD) 제조업체의 PET 비용 구조를 불안정하게 만듭니다. 포워드 헤지가 제한되어 있기 때문에 소규모 보틀러의 경우 분기별로 마진이 압축됩니다.

2024년에는 플라스틱이 45.3%로 최대의 점유율을 유지했지만, 금속 패키징의 CAGR은 6.2%로 전 소재 중에서 가장 빠른 것을 기록할 것으로 예측됩니다. 금속 용기의 미국의 음료 포장 시장 규모는 2030년까지 270억 달러 이상에 달할 것으로 예상됩니다. 이는 제한 없이 재활용 가능한 형식에 대한 소비자 선호도와 높은 소비자 재사용(PCR) 함량에 대한 규제 신용을 반영합니다. 알루미늄의 장벽 특성은 에너지 음료 및 RTD 커피의 풍미 변화를 방지하고 단가 상승을 상쇄하는 프리미엄 선반 분할을 지원합니다.

볼사는 2030년까지 재활용률 90%, 재활용률 85%를 목표로 하고 있으며, 스코프 3 배출감축을 추구하는 소매업체와 공명하는 클로즈드 루프의 이야기를 창조하고 있습니다. 유리는 노의 폐쇄와 에너지 다소비용의 용융에 의한 역풍에 직면하고 있지만, 판지 카톤은 97% 재생 가능한 Elopak Pure-Pak 구조에 의해 대량 생산으로 PET와 동등한 비용에 도달해, 기세를 늘리고 있습니다. 재생 PET의 부족은 폴리머 함량을 최대 15%까지 줄이는 적극적인 경량화에도 불구하고 플라스틱의 보급을 여전히 억제하고 있습니다.

병은 2024년에 미국 음료 포장 시장의 27.8%를 차지했지만, 캔은 휴대성, 냉장 효율, 사용자 정의 가능한 인쇄에 견인되어 CAGR 7.1%를 나타낼 전망입니다. 캔의 쌓을 수 있는 형상은 유리병에 비해 20-25%의 운임 절약으로 이어져 크래프트 맥주, 맛 탄산음료, 비타민 강화수 제조업체의 전환을 촉진하고 있습니다.

Can Manufacturers Institute의 데이터에 따르면, 2025년에 출시된 음료의 70% 이상이 통조림입니다. 디지털 인쇄 기술은 리드 타임을 몇 주에서 며칠로 단축함으로써 SKU의 보급을 가속화합니다. 병의 기술 혁신의 중심은 경량 리필 PET와 유리이며, 파우치와 카톤은 어린이용 음료나 무균 유제품의 대체품 등 틈새 이용 사례에 어필하고 있습니다.

미국의 음료 포장 시장은 소재(플라스틱, 금속, 유리, 판지), 제품 유형(병, 캔, 파우치, 카톤, 맥주통), 용도(알코올 음료, 우유·유제품 대체 음료, 에너지·기능성 음료, 탄산 음료·물, 기타 음료), 포장 형태(경질, 연질)로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

The US beverage packaging market reached USD 52.74 billion in 2025 and is forecast to expand to USD 64.64 billion in 2030, registering a 4.15% compound annual growth rate (CAGR).

Steady value growth is underpinned by aluminum-centric strategies that align with tightening sustainability regulations, rising recycled-content mandates, and consumer preference for easily recyclable formats. Brand owners increasingly treat packaging as a cost-effective lever for carbon-reduction targets, fostering demand for lightweight metal containers and high-barrier flexible films. Supplier price actions-such as Ball Corporation's January 2025 surcharge on 12-ounce cans-and minimum-order hikes continue to reshape cost curves for craft producers, widening the gap between large and small beverage companies. Parallel expansion of ready-to-drink (RTD) coffee, energy, and functional beverages is accelerating the migration from multilayer plastic bottles toward aluminum cans and slim bottles with premium graphics. Finally, e-commerce growth is nudging the design of "ship-in-own-container" formats that eliminate secondary corrugate, reduce breakage, and create new premiumization avenues.

California's AB 793 set a 15% recycled-content floor for PET beverage containers in 2022 that rises to 50% by 2030, providing a blueprint that New York, New Jersey, and Massachusetts lawmakers are actively considering. Recycled PET carries 15-25% cost premiums over virgin resin, compelling brands to invest in lightweighting that reduces polymer usage by 8-12% per container. PepsiCo's 100% rPET shift on select water lines trimmed carbon emissions by 31% while retaining shelf integrity. Compliance-driven line retrofits add USD 0.03-0.08 per unit in logistics and processing overhead, yet brands are capturing 5-8% price lifts by marketing lower-carbon packaging.

RTD energy beverages now account for 37% of convenience-store RTD sales, up from 28% in 2020, and nearly every major launch uses aluminum formats. Monster Beverage derives 97% of its global volume from aluminum containers, enabling USD 7.1 billion in 2025 net sales while offsetting commodity inflation through premium pricing. Aluminum's light- and oxygen-barrier attributes help maintain coffee aromatics and functional ingredient stability, extending shelf life without chilled distribution and lowering cold-chain costs by up to 30%. New RTD coffee stock-keeping units (SKUs) rose 73% from 2018-2023, and 60% of those used cans because of flavor preservation and decoration versatility.

Monomer price swings-particularly ethylene and paraxylene-regularly reach 25-30 c/lb in Gulf Coast spot markets, destabilizing PET cost structures for bottled water and carbonated soft drink (CSD) producers. Forward hedging is limited, causing quarterly margin compression for small bottlers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic kept the largest share at 45.3% in 2024, yet metal packaging is projected to post a 6.2% CAGR, the fastest among all materials. The US beverage packaging market size for metal containers is forecast to exceed USD 27 billion by 2030, reflecting consumer preference for infinitely recyclable formats and regulatory credit for higher post-consumer recycled (PCR) content. Aluminum's barrier properties guard flavor volatility in energy drinks and RTD coffee, supporting premium shelf pricing that offsets higher unit costs.

Ball Corporation targets 90% recycling rates and 85% recycled content by 2030, creating a closed-loop narrative that resonates with retailers pursuing Scope 3 emission cuts. Glass faces headwinds from furnace closures and energy-intensive melting, while paperboard cartons gain momentum through 97% renewable Elopak Pure-Pak structures that reach cost parity with PET at high volume. Recycled PET shortages still restrain plastic penetration despite aggressive lightweighting that cuts polymer content by up to 15%.

Bottles commanded 27.8% of the US beverage packaging market in 2024; however, cans are pacing at a 7.1% CAGR, driven by portability, refrigeration efficiency, and customizable printing. Cans' stackable geometry yields 20-25% freight savings over glass bottles, encouraging conversion among craft beer, flavored seltzer, and vitamin-enriched water producers.

Over 70% of 2025 beverage launches are in cans compared with 45% five years earlier, according to Can Manufacturers Institute data. Digital-print technology accelerates SKU proliferation by shrinking lead times from weeks to days, vital for limited edition RTD coffee collaborations. Bottle innovation centers on lightweight refillable PET and glass, while pouches and cartons appeal to niche use cases such as children's beverages or aseptic dairy alternatives.

US Beverage Packaging Market is Segmented by Material (Plastic, Metal, Glass, Paperboard), Product Type (Bottles, Cans, Pouches, Cartons, Beer Kegs), Application (Alcoholic Beverages, Milk and Dairy Alternatives, Energy and Functional Drinks, Carbonated Soft Drinks and Water, Other Beverages), Packaging Format (Rigid, Flexible). The Market Forecasts are Provided in Terms of Value (USD).