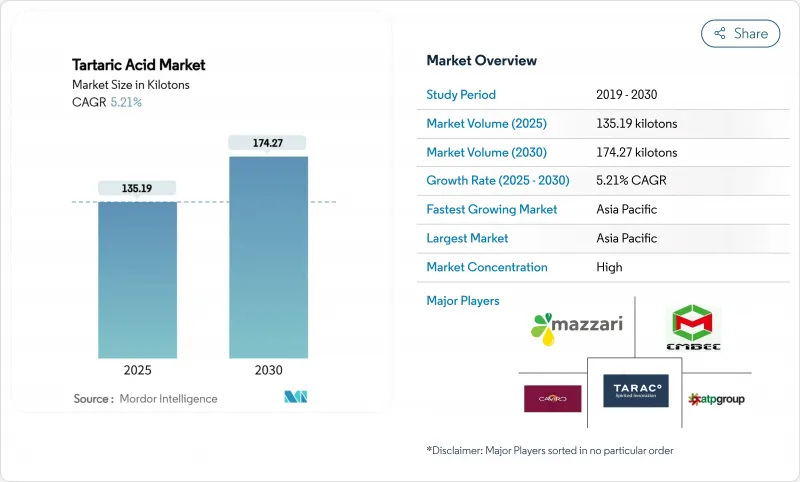

주석산 시장 규모는 2025년에 135.19킬로톤으로 추정되고, 2030년에는 174.27킬로톤에 달할 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 5.21%를 나타낼 전망입니다.

이 성장은 와인 안정화에서 고급 의약품 부형제에 이 화합물의 광범위한 유용성을 반영합니다. 생산자는 포도 유래의 회수와 무수 말레산 합성을 전환할 수 있기 때문에 원재료의 충격을 완화하고 공급의 탄력성이 주석산 시장을 지원하고 있습니다. 와인 양조에 있어서 순도 규격의 인상, 클린 라벨 식품에의 기호의 높아짐, 안정된 의약품 처방등이 더해져, 상업 기반이 확대하고 있습니다. 동시에 지속가능성에 대한 압력은 전기투석 및 기타 에너지 절약 프로세스에 대한 투자에 박차를 가하여 천연 등급의 품질 우위를 저해하지 않고 합성 등급의 생산 비용을 절감하고 있습니다.

세계 와인 생산량은 감소하고 2024년에는 2억 2,600만 헥토리터까지 떨어졌지만, 역설적으로 생산자가 자사에서 포도 폐기물 회수에 의존하지 않게 되었기 때문에 외부로부터의 주석산 공급에 대한 수요가 높아지고 있습니다. 희귀 가치 프리미엄을 통해 유럽의 천연 포도 생산자는 합성 포도보다 15-20% 높은 가격을 확보할 수 있습니다. 버지니아주에서 실시한 시험은 발효 전에 칼륨계 주석산을 첨가함으로써 발효 후 첨가하는 것보다 우수한 관능적 점수를 얻을 수 있음을 보여주었습니다. 기후에 의한 포도의 칼륨의 상승은 일상적인 산성화의 필요성을 더욱 증가시킵니다. 국제 포도 와인기구(International Organisation of Vine and Wine)는 현재 순도 99.5%를 규정하고 있으며, 이 기준치는 확립된 내추럴 공급업체에게 유리합니다. 생산자는 또한 전기투석에 의해 순도 69.7%에 달하는 증류소 비니너스를 높이 평가하고 품질목표를 순환형 경제의무에 합치시키고 있습니다.

주석산 시장은 약물의 용해, 정제의 붕괴, 생체이용률을 돕는 화합물의 키랄 특성으로부터 이익을 얻고 있습니다. 바나너 전분 복합체는 붕괴 시간에 표준 초붕해제보다 우수합니다. FDA 지침에서 주석산은 GRAS로 취급되며 규제상의 장애물이 감소합니다. 메탈로프로테아제 억제 및 항균 활성에 대한 특허 출원은 치료 가능성을 강조합니다. 고령화 사회에 따라 완하제 제제의 CAGR 성장률이 6.06%를 나타낼 전망입니다. 미국과 유럽 연합(EU)의 1일당 섭취 한도량 240mg/kg의 조화는 세계적인 제품 전개를 간소화합니다.

유럽 의회가 폭로한 추적 가능성의 갭이 중국산 합성 식물에 대한 컴플라이언스 비용을 끌어올리는 감시 강화에 박차를 가합니다. EFSA의 2024년 견해에서 도입된 중금속 규제치는 보다 비용이 많이 드는 정화를 요구합니다. 동위원소검사와 함께 규제당국은 발효 유래와 석유화학 유래를 확인할 수 있게 되어 수입검사가 엄격화됩니다.

주석산 시장의 내추럴 그레이드는 포도 폐기물의 종합적 처리의 강점을 살려 2024년에는 72.19%의 점유율을 차지했습니다. 천연 회수는 유럽에서 번성하고 와인 생산자는 제품별로 산을 추출하여 원료 비용을 절감하고 있습니다. 합성 능력은 중국에 집중되어 있으며, 말레산 무수물이 농업 사이클에 의존하지 않는 경로를 제공하기 때문에 CAGR 5.91%의 속도로 증가하고 있습니다. 지속 가능한 막 전기 투석은 에너지 사용량을 30% 줄이고 비용 격차를 줄입니다.

합성 제조업체 각사는 균일한 순도와 연간을 통한 이용가능성을 판매하고, 예측 가능한 사양에 중점을 두는 바이어를 매료하고 있습니다. 천연 공급업체는 유기 인증의 우위와 깨끗한 라벨 식품에서 프리미엄 포지셔닝으로 대응합니다. 칠레와 아르헨티나에서 알비네사 인수는 반구를 넘어서는 지속적인 포도 폐기물의 흐름을 지원합니다. 규제기관이 유기농 표시에 있어서 식물 유래의 산을 지지하기 때문에 합성 물질이 주석산 시장 내에서 많은 점유율을 획득하고 있다고 해도, 천연 물질의 양은 과반수를 차지한다고 생각됩니다.

주석산 시장 보고서는 유형별(천연 주석산, 합성 주석산), 용도별(방부제·첨가제, 완하제, 중간체, 기타 용도), 최종사용자 산업별(음식, 의약품, 화장품, 건설, 기타 최종사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되고 있습니다.

아시아태평양은 2024년 점유율 46.52%에 달했고, 2030년까지 연평균 복합 성장률(CAGR) 전망 5.88%로 주석산 시장의 최전선에 서 있습니다. 중국의 석유화학 콤비나트는 경쟁가격의 말레산 무수물을 공급하고 있으며, 합성수지는 유럽 제품을 15-20% 밑돌 수 있습니다. 인도와 동남아시아의 의약품 생산은 고순도 등급 수요를 더욱 높이고 있습니다. 일본, 한국, 싱가포르 당국은 저탄소 제조업을 장려하고 에너지 사용을 억제하는 전기화학 합성 시험에 박차를 가하고 있습니다.

유럽은 와인 부문과 연관된 천연 추출에 지원되는 강력한 지위를 유지하고 있습니다. 이탈리아, 스페인 및 프랑스의 포도 가공 허브는 지속적인 원료 접근을 가능하게 하며 99.5% 순도 기준을 준수합니다. 동위원소 분석을 이용한 EU 인증 규칙은 합성 수입품에 대응하여 국내 공급업체를 강화합니다. 독일과 북유럽의 다운스트림 식품 및 음료 브랜드는 유기 인증을 받은 원료를 중시해 지역내 흐름을 강화하고 있습니다.

북미는 주석산 시장의 성숙하지만 안정된 부분을 형성합니다. 미국은 제네릭 의약품 생산과 클린 라벨 제제를 통해 소비를 견인하고 캐나다는 조리된 식품의 천연 소재를 중시하고 있습니다. 멕시코에서는 과자류와 음료 수출이 확대되고 수요가 증가하고 있습니다. 식물 유래 산을 의무화하는 USDA의 유기 기준은 구매자를 포도 폐기물 가산업자로 향하게 합니다. 지역 연구는 벌새 생물 방제와 같은 기술 혁신을 촉진하고 생산량 다양화의 새로운 길을 제시합니다.

The Tartaric Acid Market size is estimated at 135.19 kilotons in 2025, and is expected to reach 174.27 kilotons by 2030, at a CAGR of 5.21% during the forecast period (2025-2030).

This progression mirrors the compound's broad utility, stretching from wine stabilization to advanced pharmaceutical excipients. Supply resilience anchors the tartaric acid market because producers can toggle between grape-derived recovery and maleic anhydride synthesis, cushioning raw-material shocks. Elevated purity specifications in wine making, rising clean-label food preferences, and steady pharmaceutical formulations are together widening the commercial base. At the same time, sustainability pressures spur investment in electrodialysis and other energy-saving processes that trim production costs for synthetic grades without eroding the quality edge held by natural variants.

Lower global wine output, which fell to 226 million hectoliters in 2024, has paradoxically lifted demand for external tartaric acid supplies as producers rely less on in-house grape waste recovery. Scarcity premiums enable European natural producers to secure 15-20% higher prices over synthetic offerings. Trials in Virginia show that potassium-based tartaric additions before fermentation deliver superior sensory scores versus post-fermentation use. Climate-driven rises in grape potassium further increase routine acidification needs. The International Organisation of Vine and Wine now stipulates 99.5% purity, a threshold favoring established natural suppliers. Producers also valorize distillery vinasses, reaching 69.7% purity via electrodialysis, aligning quality goals with circular-economy mandates.

The tartaric acid market benefits from the compound's chiral properties that aid drug dissolution, tablet disintegration, and bioavailability. Banana-starch complexes outperform standard super-disintegrants in disintegration time. FDA guidance treats tartaric acid as GRAS, lowering regulatory hurdles. Patent filings for metalloproteinase inhibition and antimicrobial actives underscore therapeutic potential. Growth in laxative formulations accelerates at 6.06% CAGR as aging populations seek gentle natural options. Harmonized daily-intake limits of 240 mg/kg in the United States and European Union streamline global product rollouts.

Traceability gaps exposed by the European Parliament spur stricter oversight that raises compliance outlays for Chinese synthetic plants. Heavy-metal limits introduced in EFSA's 2024 opinion require costlier purification. Coupled with isotope testing, regulators can now discern fermentation-derived and petrochemical origins, tightening import inspections.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The natural grade of the tartaric acid market commanded 72.19% share in 2024 on the strength of integrated grape-waste processing. Natural recovery thrives in Europe, where wine producers extract acid as a byproduct, slashing feedstock costs. Synthetic capacity, concentrated in China, is gaining pace at a 5.91% CAGR because maleic anhydride furnishes an agricultural-cycle-free route. Sustainable membrane electrodialysis cuts energy use by 30%, narrowing cost gaps.

Synthetic producers tout uniform purity and year-round availability, attracting buyers focused on predictable specifications. Natural suppliers counterbalance with organic certification advantages and premium positioning in clean-label foods. Alvinesa's acquisitions in Chile and Argentina underpin continuous grape-waste flows across hemispheres. As regulatory bodies favor plant-origin acids in organic labeling, natural volumes are likely to hold majority share even as synthetics gain numerical ground within the tartaric acid market.

The Tartaric Acid Market Report is Segmented by Type (Natural Tartaric Acid, Synthetic Tartaric Acid), Application (Preservative and Additive, Laxative, Intermediate, and Other Applications), End-User Industry (Food and Beverage, Pharmaceutical, Cosmetics, Construction, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific stands at the forefront of the tartaric acid market with 46.52% share in 2024 and a 5.88% CAGR outlook to 2030. China's integrated petrochemical complexes supply competitively priced maleic anhydride, allowing synthetics to undercut European offers by 15-20%. Pharmaceutical production in India and Southeast Asia further bulks demand for high-purity grades. Authorities in Japan, South Korea, and Singapore encourage low-carbon manufacturing, spurring trials in electrochemical synthesis that curb energy use.

Europe upholds a strong position anchored in natural extraction linked to its wine sector. Grape-processing hubs in Italy, Spain, and France enable continuous raw-material access and ensure compliance with the 99.5% purity threshold. EU authentication rules using isotope analysis strengthen domestic suppliers against synthetic imports. Downstream food and beverage brands within Germany and the Nordics value organically certified inputs, bolstering intra-regional flows.

North America forms a mature yet steady slice of the tartaric acid market. The United States drives consumption through generic drug production and clean-label formulations, while Canada emphasizes natural ingredients in ready meals. Mexico's expanding confectionery and beverage exports add incremental demand. USDA organic standards, which mandate plant-derived acids, direct buyers toward grape-waste processors. Regional research fosters innovations such as bee-mite biocontrol, hinting at fresh avenues for volume diversification.