인도의 풍력에너지 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

India Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1851488

리서치사:Mordor Intelligence

발행일:2025년 07월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

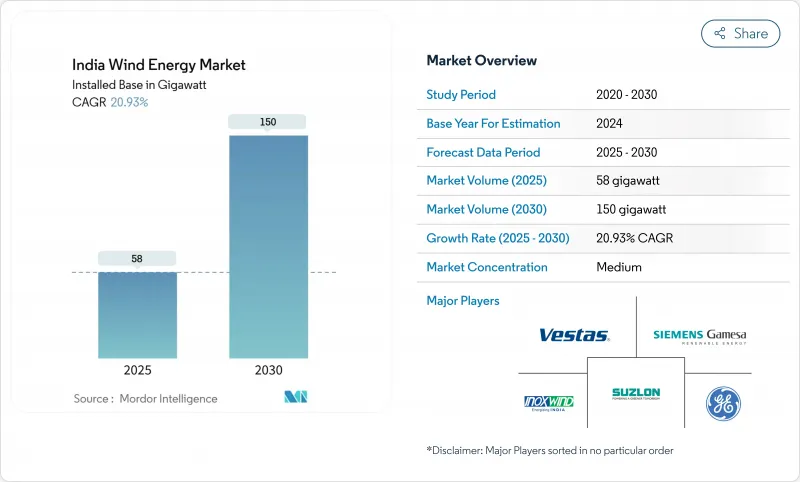

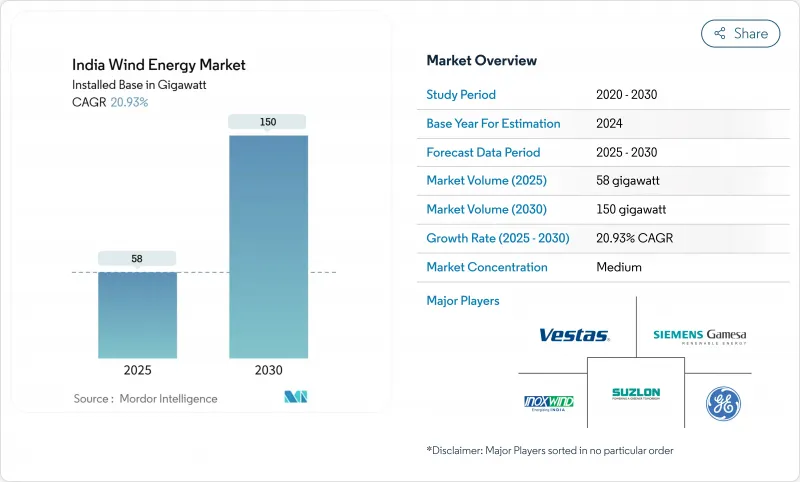

인도의 풍력에너지 시장 규모는 2025년 58기가와트에서 2030년에는 150기가와트로 확대되며, 예측 기간(2025-2030년)의 CAGR은 20.93%를 나타낼 것으로 예상됩니다.

이 기세를 뒷받침하는 것은 500GW 비화석 목표에 따른 정책 지원, 기업의 전력 구매 계약 증가, 풍력과 햇빛의 하이브리드 경임베디드니다. 데이터센터 사업자에 의한 송전망 규모의 조달 증가, 노후화된 터빈의 리파워링의 부활, 최초의 해외 바이어빌리티 갭 자금 조달이 성장 전망을 더욱 강화합니다. 2025년 6월의 주간 송전 면제 만료와 주 수준의 토지 제약에 의한 비용면의 역풍은 단기적인 과제였지만, 국내 제조업의 두께와 그린 수소 수요가 구조적인 업사이드를 만들어 내기 때문에 장기적인 전망을 미치게 하지 않습니다.

하이브리드 입찰은 2020년의 16%에서 2024년에는 재생에너지 입찰 전체의 43%를 차지했습니다. 구자라트 주와 타밀 나두 주에서는 2.58-2.67루피/kWh의 요금 설정이 비용 경쟁력을 보여줍니다. 가동중인 하이브리드 발전 용량은 2025년에는 770만kW에 이르며 30만kW의 파이프라인이 있습니다. 이 접근법은 보완적인 발전 프로파일을 매칭시켜 그리드의 안정성을 향상시키고 인도의 풍력에너지 시장이 불안정한 도로 곡선 전체에 걸쳐 견고한 수요를 유지할 수 있도록 합니다.

구자라트 주 최초의 4GW 해상 풍력 발전 라운드에 대한 바이어빌리티 갭 자금 공급 공급 공급 투자 기폭제

항만용 60억 루피를 포함한 연방 내각의 745억 3,000만 루피 패키지는 육상 프로젝트와 해상 프로젝트 간의 관세 격차를 줄입니다. 구자라트의 캄밧 만과 타밀 나두의 해안은 공동으로 7,000만kW의 기술적 잠재력을 제공하며 해상 풍력 발전을 장기적인 다양화 기둥으로 자리잡고 있습니다. 항구 업그레이드 및 전용 피난 통로는 모노 파일, 트랜지션 피스, HVDC 수출 라인공급망 현지화를 가속화합니다. 그 결과 인도의 풍력에너지 시장은 태양광 발전이 많은 주간 발전을 보완하는 고용량 인자 자산의 기반을 확보하게 됩니다.

카르나타카와 마하라슈트라의 토지 할당 동결이 육상 파이프라인을 지연

카르나타카는 2024년에 1,135MW의 발전 용량을 추가했지만, 주 레벨의 토지 뱅크의 고갈이 프로젝트 실행 스케줄을 제약했습니다. 오픈 액세스에 관한 규제 개혁은 강하의 오프 테이크를 개선하지만, 토지 전환을위한 여러 부처의 클리어런스는 여전히 장기화되고 있습니다. 태양광 발전 입찰 경쟁은 적절한 구획을 더욱 좁히고 있습니다. 이러한 병목 현상은 추가 토지 임대 체제가 완성될 때까지 인도의 풍력에너지 시장의 건설 속도를 지연시킬 수 있습니다.

부문 분석

2024년 인도의 풍력에너지 시장 점유율은 육상 용량이 100%를 차지했는데, 이는 18GW의 연간 국내 터빈 제조 능력과 2.68-3.6루피/kWh의 경쟁가격에 의해 지원되고 있습니다. 해상 풍력은 아직 시작되었지만, 745.3억 루피의 자금 조달 방식과 40% 이상의 뛰어난 가동률에 힘입어 CAGR 35%를 나타낼 것으로 예상되고 있습니다. 그 결과 인도의 해상 풍력 발전 프로젝트 시장 규모는 2030년까지 2자리 기가와트 수준까지 매우 적은 베이스에서 확대될 수 있습니다.

보다 높은 자본 집약도와 특수 로지스틱스로 인해 해외 평준화 비용은 보조금 없이 INR 9-12/kWh에 가깝게 유지됩니다. 국산 비율 64% 규칙 초안은 해외 기초와 어레이의 지역 공급망을 육성하면서 온쇼어 경제성을 강화합니다. 시간이 지남에 따라 규모의 경제와 항만 주도 제조 클러스터가 비용 격차를 줄이고, 인도의 풍력에너지 시장은 향후 10년간 육상과 육상 사이의 균형 잡힌 구성으로 전환될 것으로 기대됩니다.

인도의 풍력에너지 시장 보고서는 분야별(육상 및 해상)으로 분류됩니다. 시장 규모 및 예측은 설치용량(GW)으로 제공됩니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

시장 개요

시장 성장 촉진요인

풍력과 태양광을 번들로 한 하이브리드 재생에너지 경매의 가속 타밀·나두주와 구자라트주에 있어서 용량 이용률의 향상

구자라트 주 최초 4GW 해상풍력 프로젝트에 대한 생존성 격차 자금 지원, 공급망 투자 촉매제 역할

리파워링 계획에 의해 5-15GW의 노후풍력 발전소가 고용량 터빈용으로 개방

그린 수소 정책이 산업 클러스터에 있어서 고부하율 풍력 발전 수요를 촉진

ISTS 차지 면제가 자원 풍부한 서부주의 풍력 프로젝트 IRR 촉진

풍력과 태양광의 RTC 믹스를 요구하는 데이터센터 사업자로부터 기업용 PPA가 급증

시장 성장 억제요인

카르나타카주와 마하라슈트라주 토지 할당 동결이 육상 파이프라인을 지연

캄밧 만에서 해상 풍력 발전을위한 송전망 대피 통로 지연

터빈 부품의 GST 상승으로 태양광 발전과의 비용 경쟁이 격화

주 DISCOM에 의한 은행 규제(30% 미만의 에너지)가 축소 리스크를 증대

공급망 분석

규제 전망

기술 전망

Porter's Five Forces

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 관계

PESTEL 분석

제5장 시장 규모와 성장 예측

섹터별

육상

터빈 용량별

2MW 미만

2-3.5MW

3.5MW 이상

용도별

유틸리티 스케일

자체 소비 산업용

상업 및 기관용

해상

설치 유형별

고정식 해저 설치

부유식

수심별

얕은 수심(30m 미만)

과도 수심(30-60m)

심해(60m 이상)

제6장 경쟁 구도

시장 집중도

전략적 움직임(M&A, 파트너십, PPA)

시장 점유율 분석(주요 기업의 시장 순위/점유율)

기업 프로파일

Inox Wind Limited

Suzlon Energy Limited

Siemens Gamesa Renewable Energy SA

Vestas Wind Systems A/S

General Electric Company

Envision Energy

Wind World(India) Ltd

Tata Power Renewable Energy Ltd

Enercon GmbH

Senvion India

ReNew Power(ReNew Energy Global PLC)

Adani Green Energy Ltd

JSW Energy-Mytrah Cluster

Amp Energy India Pvt Ltd

Greenko Group

Siemens Energy AG

Mingyang Smart Energy

Nordex SE

Leitwind Shriram Manufacturing Ltd

GE T&D India Ltd

SKF India

Hitachi Energy India Ltd

Bharat Heavy Electricals Ltd

LM Wind Power(India)

제7장 시장 기회와 향후 전망

KTH

영문 목차

영문목차

The India Wind Energy Market size in terms of installed base is expected to grow from 58 gigawatt in 2025 to 150 gigawatt by 2030, at a CAGR of 20.93% during the forecast period (2025-2030).

Policy support under the 500 GW non-fossil target, rising corporate power-purchase agreements, and hybrid wind-solar auctions underpin this momentum. Increased grid-scale procurement by data-centre operators, resurgence in repowering of aging turbines, and the first offshore viability-gap funding tranche further strengthen growth prospects. Cost headwinds from the June 2025 expiry of interstate-transmission waivers and state-level land constraints pose near-term challenges but do not derail the long-term outlook, as domestic manufacturing depth and green-hydrogen demand create structural upside.

India Wind Energy Market Trends and Insights

Accelerated Hybrid Renewable Auctions Bundling Wind with Solar Enhancing Capacity Utilisation in Tamil Nadu & Gujarat

Hybrid tenders accounted for 43% of all renewable auctions in 2024, up from 16% in 2020. Tariffs of INR 2.58-2.67 / kWh in Gujarat and Tamil Nadu demonstrate cost competitiveness, while capacity-utilisation factors above 60% meet round-the-clock requirements for commercial consumers. Operational hybrid capacity stood at 7.7 GW in 2025 with a 30 GW pipeline, and NTPC's recent 1.2 GW award signals strong institutional backing. The approach enhances grid stability by matching complementary generation profiles, ensuring that the India wind energy market maintains robust demand across volatile load curves.

Viability-Gap Funding for Initial 4 GW Offshore Wind Round in Gujarat Catalyst for Supply-Chain Investments

The Union Cabinet's INR 74.53 billion package, including INR 6 billion for ports, narrows the tariff gap between onshore and offshore projects. Gujarat's Gulf of Khambhat and Tamil Nadu's coast jointly offer 70 GW technical potential, positioning offshore wind as a long-term diversification pillar. Port upgrades and dedicated evacuation corridors accelerate supply-chain localisation for monopiles, transition pieces, and HVDC export lines. As a result, the India wind energy market secures a foundation for high-capacity-factor assets that complement solar-heavy daytime generation.

Land Allotment Freeze in Karnataka & Maharashtra Slowing Onshore Pipeline

State-level land-bank depletion constrains project execution timelines despite Karnataka adding 1,135 MW in 2024. Regulatory reforms around open access improve downstream offtake, yet multi-agency clearances for land conversion remain protracted. Competing solar bids further tighten suitable parcels. These bottlenecks could slow the build rate for the India wind energy market until additional land-leasing frameworks are finalised.

Other drivers and restraints analyzed in the detailed report include:

Repowering Scheme Opening 5-15 GW of Ageing Wind Farms for High-Capacity Turbines

Green Hydrogen Policy Driving Demand for High-Load-Factor Wind Power in Industrial Clusters

Delayed Grid Evacuation Corridors for Offshore Wind at Gulf of Khambhat

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore capacity accounted for 100% India's wind energy market share in 2024, supported by 18 GW of annual domestic turbine manufacturing capacity and competitive tariffs between INR 2.68-3.6/kWh. Offshore wind, although at a nascent stage, is forecast to expand at a 35% CAGR, underpinned by the INR 74.53 billion funding scheme and superior capacity factors exceeding 40%. As a result, the India wind energy market size for offshore projects could rise from a negligible base to a double-digit gigawatt level by 2030.

Higher capital intensity and specialised logistics keep offshore levelised costs near INR 9-12/kWh without subsidies. The draft 64% domestic-content rule strengthens onshore economics while seeding local supply chains for offshore foundations and arrays. Over time, scale economies and port-led manufacturing clusters are expected to narrow cost gaps, allowing the India wind energy market to transition toward a balanced onshore-offshore mix in the next decade.

India Wind Energy Market Report is Segmented by Sector (Onshore and Offshore). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

Inox Wind Limited

Suzlon Energy Limited

Siemens Gamesa Renewable Energy SA

Vestas Wind Systems A/S

General Electric Company

Envision Energy

Wind World (India) Ltd

Tata Power Renewable Energy Ltd

Enercon GmbH

Senvion India

ReNew Power (ReNew Energy Global PLC)

Adani Green Energy Ltd

JSW Energy - Mytrah Cluster

Amp Energy India Pvt Ltd

Greenko Group

Siemens Energy AG

Mingyang Smart Energy

Nordex SE

Leitwind Shriram Manufacturing Ltd

GE T&D India Ltd

SKF India

Hitachi Energy India Ltd

Bharat Heavy Electricals Ltd

LM Wind Power (India)

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 Introduction

1.1 Study Assumptions & Market Definition

1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

4.1 Market Overview

4.2 Market Drivers

4.2.1 Accelerated Hybrid Renewable Auctions Bundling Wind with Solar Enhancing Capacity Utilisation in Tamil Nadu & Gujarat

4.2.2 Viability-Gap Funding for Initial 4 GW Offshore Wind Round in Gujarat Catalyst for Supply-Chain Investments

4.2.3 Repowering Scheme Opening 5-15 GW of Ageing Wind Farms for High-Capacity Turbines

4.2.4 Green Hydrogen Policy Driving Demand for High-Load-Factor Wind Power in Industrial Clusters

4.2.5 ISTS Charge Waivers Boosting Wind Project IRRs in Resource-Rich Western States