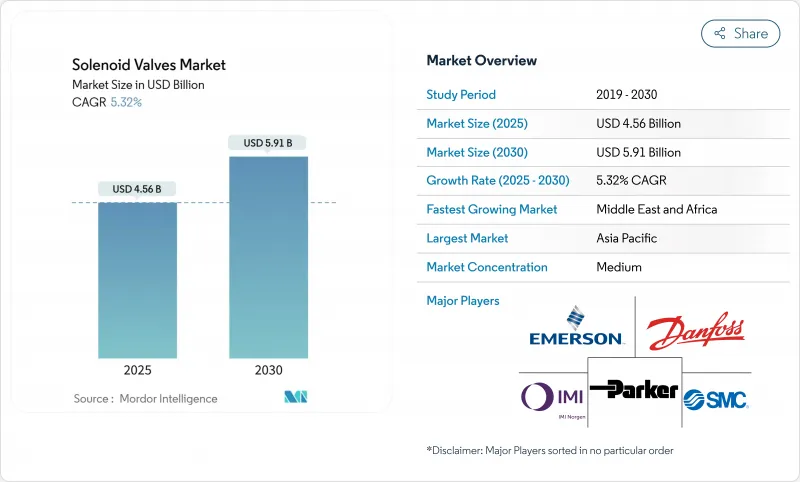

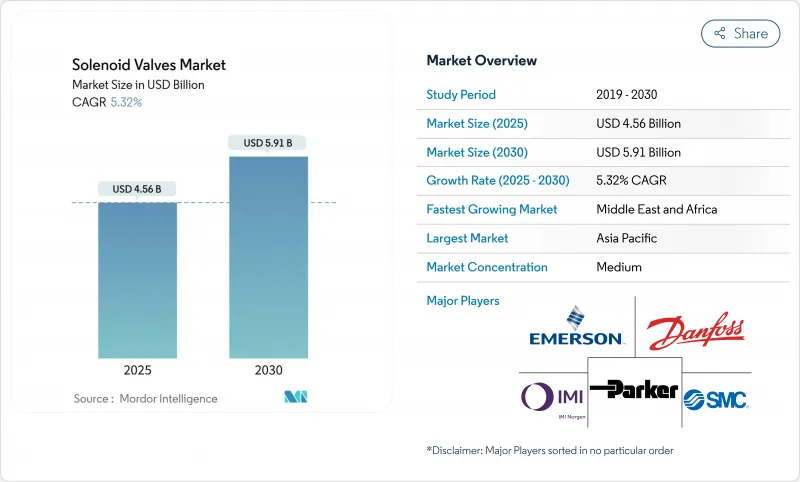

세계의 솔레노이드 밸브 시장 규모는 2025년 45억 6,000만 달러, 2030년까지 59억 1,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 5.32%로 예상됩니다.

수요는 물 재사용, 혈암 가스 갱구, 수소 전해조, 소형 전기자동차(EV) 열 루프의 자동화 프로젝트에 기인합니다. 아시아태평양이 양의 주도권을 유지하는 반면 중동 및 아프리카은 경제 다양화 계획을 위해 가장 빠르게 확대되고 있습니다. 기술 차별화는 제로 에미션 액추에이션, IO 링크 대응 진단, 자동차의 항속 거리 목표를 충족하는 경량 엔지니어링 플라스틱으로 이동하고 있습니다. 저비용 아시아 제조업체와의 가격 경쟁 격화와 합금 비용 변동에도 불구하고 OEM은 계속 가동 중지 시간을 제한하고 예지 보전을 가능하게 하는 스마트하고 서비스하기 쉬운 솔레노이드 아키텍처를 선호합니다.

유럽연합(EU)의 순환형 경제 지령과 걸프 협력 회의(GCC)의 물 부족 지령에 의해 자동 약액 주입, 백플러시 제어, 스테이지 전환을 필요로 하는 고도 처리 플랜트에 대한 투자가 가속화되고 있습니다. 솔레노이드 밸브는 특히 공급수의 변동에 따라 치료 레시피가 변할 때 수동 장치로는 대응할 수 없는 정확하고 낮은 누설 작동을 가능하게 합니다. 중동에서 폐수 무방류 플랜트를 채택한 석유 제조업체는 환경 감사를 지원하기 위해 스테인레스 스틸 또는 이중 구조 바디와 디지털 위치 피드백을 선호합니다.

차세대 EV 배터리 냉각, 파워 일렉트로닉스 냉각기 및 캐빈 HVAC는 빠르고 에너지 효율적인 마이크로 솔레노이드에 의존하는 다중 루프 회로를 통합합니다. Sanhua Automotive와 같은 공급업체는 제한된 배터리 팩 내에서 작동하면서 수백만 번의 사이클을 반복할 수 있는 냉매 버전을 제품화합니다. 경량 PEEK 바디와 저전력 코일이 주행 거리를 늘리고, 이 분야를 솔레노이드 밸브 시장의 핵심 성장 엔진으로 하고 있습니다.

증기 라인과 고온 반응기에서 솔레노이드 코일은 가속 절연 파괴에 노출됩니다. 프리미엄 고내열 구리 권선과 퍼플로로 엘라스토머 씰을 사용할 수 있지만, 재료비가 높아지고 가격에 민감한 프로젝트에서의 채용이 억제됩니다. 유지 보수 간격 연장에 직면한 유틸리티 회사는 고밀도 권선으로 교체할 위험을 느끼고 있으며 솔레노이드 밸브 시장의 성장을 늦추고 있습니다.

직동식 밸브는 2024년 점유율 42%로 솔레노이드 밸브 시장을 선도하고, 2025년 시장 수익 추정치는 19억 달러에 이릅니다. 간단한 아키텍처, 최소 압력 손실, 고속 사이클은 유틸리티 수도관과 OEM 기계에 적합합니다. 그러나 CAGR 6.9%로 진보하는 파일럿식 기구는 25mm를 넘는 포트와 100bar를 넘는 압력을 필요로 하는 갱이 헤드, 전력 보일러, 대형 화학 반응기에 대한 서비스가 늘고 있습니다. Emerson의 셰일 가스 솔루션은 시간당 수천 입방 미터의 표준 압력을 공급할 수 있는 피스톤 다이어프램과 미세한 전자기 조종사를 결합하여 이 시프트를 부각시키고 있습니다. 예측 유지 보수 플랫폼으로 업그레이드하는 업계는 파일럿 작동 장치에 전형적인 낮은 돌입 전류와 조용한 폐쇄 프로파일을 높이 평가합니다.

코일은 변동하는 업스트림 압력을 견뎌야 하며, 다이어프램은 내마모성 엘라스토머를 요구하며 하우징은 PLC에 공급하는 나사식 센서를 통합하는 경우가 많습니다. 아시아 제조업체들은 현재 고전적인 조종사 운영의 형태를 대규모로 재현하고 있으며 가격 압력을 강화하고 있지만 신흥 경제 지역에서의 가용성도 확대됨에 따라 솔레노이드 밸브 시장이 확대되고 있습니다.

양방향 셧오프 밸브는 여전히 주력 제품으로 2024년 매출의 55%, 솔레노이드 밸브 시장 규모의 약 23억 달러를 차지합니다. 이들은 관개, 압축 공기, 기본 공정의 분리를 지배합니다. 그러나 식음료와 바이오테크놀러지가 SKU의 신속한 전환을 요구하고 있기 때문에 삼방 전환 밸브는 연률 6.4%의 성장을 보이고 있습니다. 이 밸브는 수동 스풀 교환없이 생산, CIP 및 멸균 흐름을 번갈아 전환하고 위생 지침에 부합합니다. 일부 제약용 스키드에서는 20대 이상의 3방 유닛을 1개의 디지털 매니폴드에 번들함으로써 설치 면적을 30% 삭감하고 설치 시간을 단축하고 있습니다.

제조업체는 구멍이 없는 내부와 FDA 인가의 씰로 대응해, 오염 물질이 축적하는 데드 레그를 배제하고 있습니다. 제어 소프트웨어는 각 포트를 PLC 태그에 매핑하여 레시피 구동 흐름 경로를 허용합니다. 멀티포트 혁신은 화학제품이 여러 린스 에칭 탱크를 밀리초 단위로 통과해야 하는 반도체 습식 벤치에도 파급되어 솔레노이드 밸브 시장 전체에서 3방향 채용이 강화되고 있습니다.

아시아태평양은 2024년 매출의 34%를 차지하며 중국의 방대한 전자제품 생산, 일본 정밀로봇공학, 인도의 의약품 수출 확대를 활용하고 있습니다. 국내 반도체 공장과 배터리 공장을 지원하는 정부는 매니폴드 채용에 박차를 가하고 있으며, 일본과 한국의 수소 파일럿 통로에서는 700bar의 기체 사용을 견디는 고신뢰성 밸브가 요구되고 있습니다. 또한 중국 해안부에서는 물 재사용이 의무화되어 새로운 지자체 수요가 증가하고 있습니다.

중동 및 아프리카에서는 CAGR이 7.50%로 예측되어 사우디아라비아의 비전 2030 다각화 프로젝트와 UAE의 석유화학 메가사이트로부터 혜택을 받고 있습니다. 오만과 사우디 NEOM의 수소 및 암모니아 수출 계획에는 극저온 및 고압 의무에 대응하는 특수한 파일럿 조작 밸브가 필요합니다. 아프리카에서는 남아프리카의 광업 탈수와 이집트의 식품 가공업의 확대가 성장의 중심이며 완만하면서도 다양한 흡수를 추진하고 있습니다.

북미는 셰일가스, LNG, 제약으로 안정적인 애프터마켓 매출에 기여하고 있습니다. 콜로라도 주와 텍사스 주에서는 제로 방출 갱도구 밸브가 급속히 전개되었고, 규제 주도의 설비 투자에 의해 설치 베이스가 리프레시되었습니다. 캐나다에서는 탄소 포획 시연 플랜트가 CO2 혼합 흐름을 다루는 내식성 솔레노이드를 찾습니다. 성숙하면서도 혁신 주도의 지역인 유럽은 그린 수소와 디지털화된 제조업에 축족을 옮기고 있습니다. 이 피벗은 헤드라인의 성장이 둔화되고 있음에도 불구하고 스마트 IO-Link 대응 밸브의 가치를 확보하고 솔레노이드 밸브 시장에 프리미엄 가격대가 정착하고 있습니다.

The solenoid valves market size is valued at USD 4.56 billion in 2025 and is forecast to reach USD 5.91 billion by 2030, reflecting a 5.32% CAGR over the period.

Demand stems from automation projects in water reuse, shale-gas wellheads, hydrogen electrolyzers, and compact electric-vehicle (EV) thermal loops. Asia-Pacific retains volume leadership, while the Middle East and Africa exhibits the fastest expansion because of economic diversification programs. Technology differentiation is shifting toward zero-emissions actuation, IO-Link-enabled diagnostics, and lightweight engineering plastics that satisfy automotive range targets. Despite growing price competition from low-cost Asian producers and alloy cost swings, OEMs continue to prioritize smart, service-friendly solenoid architectures that limit downtime and enable predictive maintenance.

Circular-economy directives in the European Union and water-scarcity mandates in the Gulf Cooperation Council are accelerating investments in advanced treatment plants that need automated chemical dosing, back-flush control, and stage switching. Solenoid valves enable precise, low-leak actuation that manual devices cannot match, especially when treatment recipes shift with feed-water variability. Oil producers adopting zero-liquid-discharge plants in the Middle East prefer stainless-steel or duplex bodies coupled with digital position feedback to meet environmental audits.

Battery cooling, power-electronics chillers, and cabin HVAC in next-generation EVs integrate multi-loop circuits that depend on fast, energy-efficient micro-solenoids. Suppliers such as Sanhua Automotive have commercialized refrigerant versions able to cycle millions of times while operating inside constrained battery packs. Lightweight PEEK bodies and low-power coils extend driving range, making the segment a core growth engine for the solenoid valves market.

Steam lines and high-temperature reactors expose solenoid coils to accelerated insulation breakdown. Premium high-temp copper windings and perfluoro-elastomer seals are available but raise bill-of-material cost, curbing adoption in price-sensitive projects. Utilities facing extended maintenance intervals perceive risk in swapping to higher-density windings, moderating growth for the solenoid valves market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Direct-acting valves led the solenoid valves market with 42% share in 2024, translating to an estimated USD 1.9 billion of 2025 revenue. Their simple architecture, minimal pressure drop, and fast cycling suit utilities water lines and OEM machinery. Yet pilot-operated mechanisms, advancing at 6.9% CAGR, increasingly service wellheads, power boilers, and large chemical reactors that require ports above 25 mm and pressures exceeding 100 bar. Emerson's shale-gas solution highlights the shift, pairing a minute electromagnetic pilot with a piston diaphragm able to pass thousands of standard cubic meters per hour. Industries upgrading to predictive maintenance platforms value the lower inrush current and quieter closing profile typical of pilot-operated units.

The move alters supply-chain needs: coils must tolerate fluctuating upstream pressures, diaphragms demand abrasion-resistant elastomers, and housings often integrate threaded sensors that feed PLCs. Asian fabricators now replicate classic pilot-operated geometries at scale, intensifying price pressure but also expanding availability across emerging economies, thereby broadening the solenoid valves market.

Two-way shut-off valves remain the workhorse, holding 55% revenue in 2024, roughly USD 2.3 billion of solenoid valves market size. They dominate irrigation, compressed-air, and basic process isolation. However, as food, beverage, and biotech adopters demand rapid SKU changeovers, three-way diverter designs grow 6.4% annually. These valves alternate between production, CIP, and sterilization streams without manual spool changes, aligning with hygienic directives. Certain pharmaceutical skids now bundle twenty or more three-way units on a single digital manifold, trimming footprint by 30% and slashing install time.

Manufacturers respond with cavity-free internals and FDA-approved seals that eliminate dead legs where contaminants accumulate. Control software maps each port to PLC tags, enabling recipe-driven flow paths. Multi-port innovations bleed into semiconductor wet benches, where chemistries must route through multiple rinse and etch tanks in milliseconds, reinforcing three-way adoption across the solenoid valves market.

The Solenoid Valves Market Report is Segmented by Operating Principle (Direct-Acting, Pilot-Operated), Port Configuration (Two-Way, Three-Way, and Four-Way), Material (Brass, Steel, Aluminum, and Plastics), Size (Micro, Sub, Mini, Small, and Large), End-User (Food, Automotive, Chemical, Oil and Gas, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific, home to 34% of 2024 revenue, leverages China's vast electronics output, Japan's precision robotics, and India's expanding pharma exports. Governments supporting domestic semiconductor fabs and battery plants fuel manifold adoption, while hydrogen pilot corridors in Japan and Korea demand high-integrity valves able to tolerate 700 bar gaseous service. Additionally, rising water-reuse mandates in coastal Chinese provinces add fresh municipal demand.

The Middle East and Africa, posting a projected 7.50% CAGR, benefits from Vision 2030 diversification projects in Saudi Arabia and petrochemical mega-sites in the UAE. Hydrogen-ammonia export plans from Oman and Saudi NEOM require specialized pilot-operated valves compatible with cryogenic and high-pressure duty. African growth centers on South African mining dewatering and Egyptian food-processing expansion, driving moderate yet diverse uptake.

North America contributes steady aftermarket turnover in shale gas, LNG, and pharma. The rapid rollout of zero-emissions wellhead valves across Colorado and Texas showcases regulatory-driven capex that refreshes installed bases. In Canada, carbon-capture demonstration plants call for corrosion-proof solenoids handling CO2 mixed streams. Europe, a mature yet innovation-led region, pivots to green hydrogen and digitalized manufacturing. That pivot secures value for smart IO-Link-ready valves despite slower headline growth, anchoring premium price bands within the solenoid valves market.