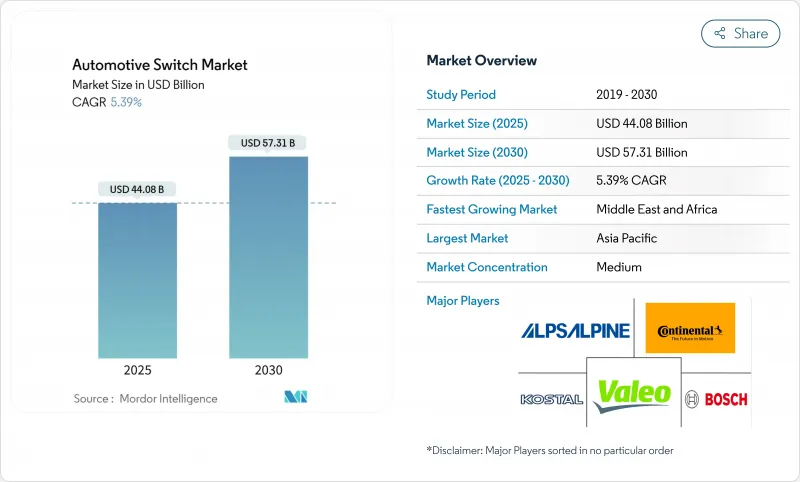

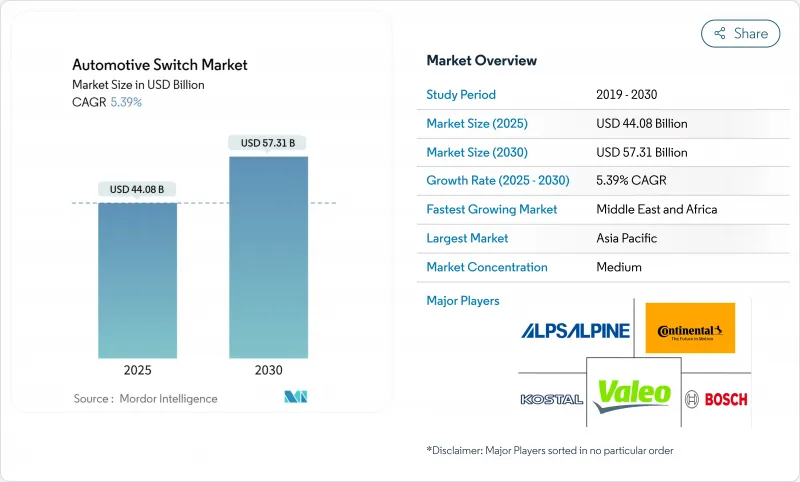

자동차 스위치 시장 규모는 2025년에 440억 8,000만 달러, 2030년에는 573억 1,000만 달러에 이르고, CAGR 5.39%로 성장할 것으로 예측됩니다.

이 성장은 기계적 감각과 전자적 인텔리전스를 연결하는 최전선의 휴먼 머신 인터페이스로 스위치가 작동하는 소프트웨어 정의 자동차로의 광범위한 전환을 반영합니다. 배터리 전기자동차는 연소식에 비해 구리와 고전압 회로를 훨씬 많이 필요하기 때문입니다. 인포테인먼트와 ADAS 내용의 충실, 화려한 일루미네이션 캐빈의 추진, ISO 26262의 안전 규칙의 엄격화, 이들 모두가, 모든 스위치에 요구되는 기능적인 기대를 높이고 있습니다. 경쟁 기업간 경쟁 관계는 촉각 기술과 정전 용량 기술이 기계적인 현상에 과제함에 따라 격화하고, 구리와 희토류를 둘러싼 공급 체인 충격은 제조 업체에 조달, 비용 헤지, 생산 지역의 풋 프린트의 재고를 강요합니다.

배터리 관리, 회생 브레이크, 열 최적화 등 전동 파워트레인에는 독자적인 제어 요구가 있으며, 촉각적인 반응을 유지하면서 고전압을 견디는 전용 스위치가 필요합니다. 파나소닉 오토모티브의 중앙 집중식 ECU 아키텍처는 연소 하드웨어를 제거하면 전자 제품의 내용이 어떻게 부풀어 오르는지를 보여줍니다. 브라질의 플러그인 판매량은 2024년 90% 증가한 17만 7,360대로 급증하여 수요 패턴의 변화가 얼마나 빠른지 밝혀졌습니다. 2026년까지 100% 국산 칩을 사용한 자동차를 출시하는 중국의 계획은 부품 조달 경로를 더욱 재구축할 것으로 보입니다. 이러한 힘은 수량과 스위치 기능의 다양성을 모두 확대하여 자동차 스위치 시장을 밀어 올립니다.

Qualcomm의 Snapdragon 플랫폼으로 구축된 클라우드 링크 조종석은 차량 외부 센서, 음성 어시스턴트, 무선 업데이트 백엔드와 통신할 수 있는 다기능 컨트롤러가 필요합니다. 콘티넨탈의 프로그래머블 햅틱 노브는 하나의 다이얼로 다양한 디텐트를 모방할 수 있으므로 차세대 대시보드의 공간과 스타일링 목표를 충족할 수 있습니다. 안전한 ADAS 레이어는 ISO 26262 인증을 받은 스위치를 요청하여 레인 유지와 같은 기능의 중복 작동을 보장합니다. 개조된 ADAS 애프터마켓은 10억 달러에 가까워지고 있으며, 새로운 안전 기능을 요구하는 낡은 자동차들 사이에서 대응할 수 있는 수요를 확대하고 있습니다.

구리 가격은 2024년 2월 이후 20% 가까이 상승했으며, 2025년에는 1톤당 1만 5,000달러를 초과하려고 하며, 고순도 접점을 사용하는 모든 기계식 스위치의 재료비를 밀어 올리고 있습니다. 중국의 희토류 수출의 병행 규제로 스즈키와 포드와 같은 OEM은 이미 단기간의 생산 중단을 강요하고 있습니다. 스위치 제조업체는 자동차 스위치 시장의 마진을 보호하기 위해 재료 비용을 헤지하고, 접점 레이아웃을 재설계하며, 저질량 합금을 평가합니다.

기계 설계는 2024년 매출의 93.82%를 유지하여 극단적인 온도, 먼지, 진동에 대한 신뢰성이 입증되었습니다. 버튼은 빈도가 높은 사용자 작업을 처리하고, 로커 장치는 바이너리 기능을 제어하며, 패들은 스티어링에 설치된 명령을 관리합니다. 기계식 스위치의 자동차 스위치 시장 규모는 디스플레이가 성장하더라도 꾸준히 확대될 것으로 예측됩니다.

터치식 스위치 시장 규모는 현재 미미하지만, 고급차나 매스 프리미엄의 트림이 플래시 라이트식 패널로 이행함에 따라, 2030년까지의 CAGR은 8.17%가 됩니다. 콘티넨탈 정전 피드백 노브는 기어 없이 기계적인 디텐트를 재현하며, 스냅트론의 납땜 가능한 촉각 돔은 연간 생산 능력을 두 배로 할 수 있습니다. 하이브리드 모듈은 얇은 플라스틱 캡 아래에 정전용량식 감지를 번들하면서도 클릭감을 발생시켜 OEM에 스타일링의 자유를 주면서 자동차 스위치 시장에서 기대되는 기존 느낌을 유지합니다.

인디케이터 컨트롤은 2024년 매출의 25.11%를 차지했는데, 이는 모든 사법 관할구에서 턴, 위험, 경고 기능을 위한 견고한 신호 전달이 의무화되어 있기 때문입니다. 인디케이터 용도의 자동차 스위치 시장 규모는 완전 디지털화된 조종석에서도 스크린이 고장날 때 외부 조명 명령이 작동해야 하기 때문에 안전합니다.

HVAC 인터페이스는 전기자동차의 레인지 센시브 서멀 로직 덕분에 가장 빠른 5.57%의 CAGR을 달성합니다. Tokai Rika의 인몰드 도장 프로세스는 이미 도요타의 하이에이스에 채택되고 있어 제조시의 에너지 사용량을 삭감하는 동시에, 흠집이 생기기 어려운 외관을 실현합니다. 기후 제어는 터치스크린에 완전히 사라지지 않으며, 사용자는 탈습 및 서리 제거를 위해 즉시 촉각으로 접근해야 하며 자동차 스위치 시장 전체 수요를 지원합니다.

아시아태평양이 자동차 스위치 시장의 선진을 끊고 있으며, 2024년 매출은 49.88%로 현재 최대 시장이 되었습니다. 중국, 일본, 한국, 인도에 견고한 공급 클러스터가 형성되고 EV에 대한 인센티브가 충실하기 때문에 세계 OEM이 현지 생산을 확대하는 가운데 이 지역은 항상 선두를 달리고 있습니다. 태국 최초의 전동 픽업 프로그램과 인도네시아의 니켈 풍부한 배터리 회랑은 APAC의 리더십을 강화하고 있습니다.

중동 및 아프리카는 규모가 작고 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 7.58%를 나타낼 전망입니다. 사우디아라비아에서는 2025년까지 계획된 50,000대의 공공충전기가 걸프 경제 전체의 스위치 수요를 가속화하고 있습니다. 2030년까지 4만 2,000대의 EV를 도입하는 두바이의 목표는 성장 격차를 더욱 넓히고 있습니다.

북미와 유럽은 프리미엄 명판을 고 컨텐츠 ADAS 및 인포테인먼트 시스템과 결합하여 강력한 포지션을 유지하고 있습니다. 남미는 브라질의 300억 레알(60억 달러)의 Stellantis 프로그램이 지역 제조를 확보함으로써 꾸준한 지보를 굳히고 있습니다. 최종 조립 거점에 가까운 곳에서 생산이 가능한 공급업체는 진화하는 무역과 컴플라이언스의 압력에 대응할 수 있는 최상의 입장에 있습니다.

The automotive switch market size stands at USD 44.08 billion in 2025 and is forecast to reach USD 57.31 billion by 2030, advancing at a 5.39% CAGR.

The upswing reflects a wider transition to software-defined vehicles where switches act as frontline human-machine interfaces that connect mechanical feel with electronic intelligence. Electrification now shapes material demand and cost structures, as each battery-electric vehicle needs far more copper and high-voltage circuitry than its combustion counterpart. Greater infotainment and ADAS content, the push for luxurious illuminated cabins, and stricter ISO 26262 safety rules all raise the functional expectations placed on every switch. Competitive rivalry intensifies as haptic and capacitive technologies challenge the mechanical status quo, while supply-chain shocks surrounding copper and rare-earths force manufacturers to rethink sourcing, cost hedging, and regional production footprints.

Electric powertrains introduce unique control needs-battery management, regenerative braking, and thermal optimization all require purpose-built switches that tolerate higher voltage while preserving tactile response. Panasonic Automotive's centralized ECU architecture shows how electronics content balloons once combustion hardware is removed. Brazil's plug-in sales jumped 90% in 2024 to 177,360 units, underscoring how quickly demand patterns shift. China's plan to launch cars using 100% domestically sourced chips by 2026 will further reshape component procurement paths . These forces collectively lift the automotive switch market by broadening both unit volumes and the variety of switch functions.

Cloud-linked cockpits built on Qualcomm's Snapdragon platforms require multifunction controllers able to talk to exterior sensors, voice assistants, and over-the-air update back-ends. Continental's programmable haptic knob enables a single dial to mimic many different detents, satisfying space and styling goals in next-generation dashboards . Safety-critical ADAS layers demand switches certified to ISO 26262, ensuring redundant actuation for features such as lane-keeping. The retrofit ADAS aftermarket, approaching USD 1 billion, expands addressable demand among older vehicles seeking new safety functions.

Copper prices climbed nearly 20% after February 2024 and are on track to top USD 15,000 per ton in 2025, inflating the bill-of-materials for every mechanical switch that uses high-purity contacts. Parallel restrictions on Chinese rare-earth exports have already forced short production pauses at OEMs, including Suzuki and Ford. Switch makers are hedging material costs, redesigning contact layouts, and evaluating lower-mass alloys to protect margins inside the automotive switch market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Mechanical designs retained 93.82% of 2024 revenue, proving their reliability in temperature, dust, and vibration extremes. Buttons handle high-frequency user tasks, rocker units govern binary functions, and paddles manage steering-mounted commands. The automotive switch market size for mechanical variants is projected to expand steadily even as displays grow, because safety codes continue to demand tactile backup controls.

Touch-based switches hold modest volume today but carry an 8.17% CAGR to 2030 as luxury and mass-premium trims migrate to flush lit panels. Continental's electrostatic feedback knob reproduces mechanical detents without gears, and Snaptron's solderable tactile domes can double annual output capacity. This convergence blurs the line: hybrid modules bundle capacitive sensing beneath a thin plastic cap yet still generate a click, giving OEMs styling freedom while maintaining the legacy feel expected in the automotive switch market.

Indicator controls owned 25.11% of 2024 revenue because every jurisdiction mandates robust signaling for turn, hazard, and warning functions. The automotive switch market size for indicator applications remains secure even in fully digital cockpits, as external lighting commands must work when screens fail.

HVAC interfaces earn the fastest 5.57% CAGR thanks to range-sensitive thermal logic in electric cars. Tokai Rika's in-mold-painting process, already used on Toyota's Hiace, slashes energy use during manufacturing while delivering scratch-resistant fascias. Climate controls cannot disappear into touchscreens entirely; users need immediate tactile access to demist or defrost, sustaining demand across the automotive switch market.

The Automotive Switch Market Report is Segmented by Switch Type (Mechanical Switches, Touch-Based Switches, and More), Application (Indicator System Switches, HVAC Controls, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia Pacific spearheads the automotive switch market with 49.88% revenue in 2024, making it the largest market today. Entrenched supply clusters in China, Japan, South Korea, and India, plus robust EV incentives, keep the region in front as global OEMs scale local production. Thailand's first electric pickup program and Indonesia's nickel-rich battery corridor reinforce APAC's leadership.

The Middle East & Africa, while smaller, posts the fastest 7.58% CAGR through 2030. Saudi Arabia's USD 2.9 billion pipeline of automotive projects, including Ceer's USD 1.3 billion EV complex, alongside 50,000 public chargers planned by 2025, accelerates switch demand across Gulf economies. Dubai's target of 42,000 EVs by 2030 further widens the growth gap.

North America and Europe retain strong positions by marrying premium nameplates with high-content ADAS and infotainment systems. South America gains steady ground as Brazil's R$30 billion (USD 6.0 billion) Stellantis program secures regional manufacturing. Suppliers able to locate production close to final assembly sites remain best placed to navigate evolving trade and compliance pressures.