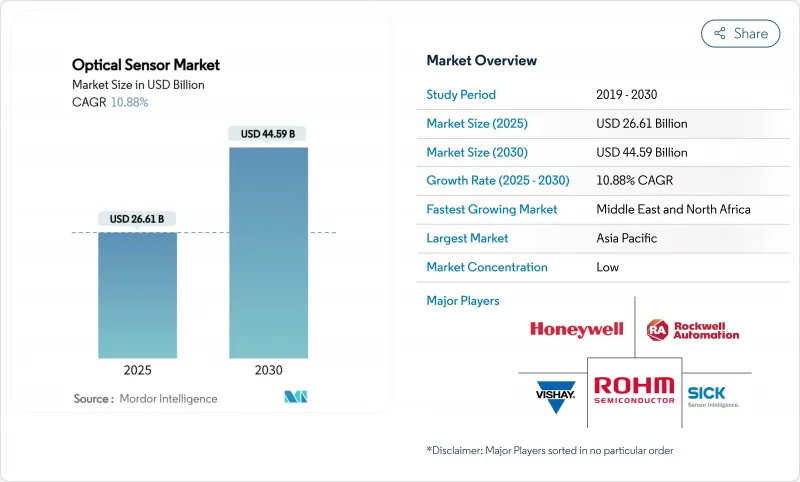

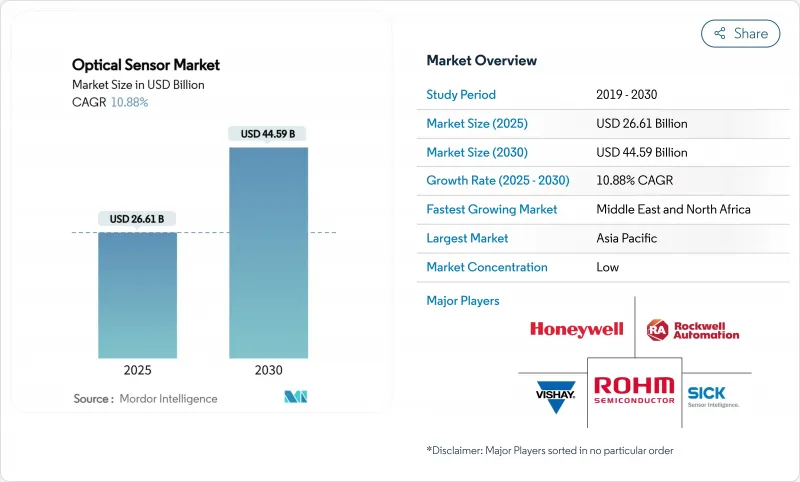

광센서 시장은 2025년에 266억 1,000만 달러, 2030년에는 CAGR 10.88%로, 445억 9,000만 달러에 달할 것으로 예측됩니다.

자동차 안전, 환경 모니터링 및 데이터 프라이버시에 대한 일관된 규제 압력은 통합되고 비용 효율적인 실리콘 포토닉스 기반 설계에 대한 수요를 유도하고 있습니다. 웨이퍼 레벨 포토닉스의 가격 하락과 네트워크 에지에서의 AI 워크로드의 보급으로 5G 인프라, 자율주행차, 분산형 광섬유 모니터링에서의 센서 채택이 가속화되고 있습니다. 고순도 실리카와 게르마늄을 둘러싼 재료 공급 리스크는 다양한 조달의 필요성을 부각시키고 있으며, 웨어러블과 스마트폰의 소형화 요건은 대량 생산을 아시아태평양으로 옮겨가고 있습니다. 중소기업이 포토닉 인테그레이션을 전개해 노포 반도체 제조업체에 대항하기 때문에 경쟁의 치열해지고 있습니다.

AR 유리와 스마트 웨어러블에는 발광 효율 목표를 충족하는 서브 mm 광학 스택이 필요합니다. ST 마이크로 일렉트로닉스가 도입한 단층 메타옵틱스는 렌즈의 높이를 70% 삭감하여 플래그쉽 스마트폰의 언더 디스플레이 근접 감지를 가능하게 합니다. 인듐 인화 VCSEL은 GaAs 이미 터를 대체하고 공간에 제약이있는 장치에 엄격한 빔 발산을 실현합니다. APAC의 수탁 제조 업체는 이러한 개발을 활용하여 구미 브랜드로부터 설계 수주를 획득하여 이 지역의 수익 점유율 33%의 지위를 강화하고 있습니다.

분산형 광섬유 감지는 전자기 간섭의 영향을 받지 않는 킬로미터 단위의 온도와 스트레인 데이터를 제공하여 정유소, 파이프라인 및 고압 변전소의 사전보호를 가능하게 합니다. 로크웰 오토메이션은 이러한 데이터의 조기 경고 분석을 통해 공정 산업에서 예정되지 않은 다운타임의 30%를 줄일 수 있다고 지적합니다. AI 기반 패턴 인식과 지속적인 광학 피드백의 조합은 북미와 유럽 인더스트리 4.0 전략의 핵심이 되고 있습니다.

2024년 허리케인을 통한 가동 중단은 단일 지역이 광섬유공급력을 압박하는 방법을 드러냈습니다. 중국의 게르마늄 수출 규제와 더불어 제조업체 각 사는 비싼 가격으로 장기 계약을 협상하고 있으며 분산형 섬유 솔루션의 대량 도입을 늦추고 있습니다. 합성 실리카의 신흥 기업이 대두하고 있지만, 상업적인 스케일링은 2-3년 후에도 유지됩니다.

이미지센서는 멀티카메라 스마트폰과 ADAS의 전개에 힘입어 2024년 광센서 시장에서 42%의 점유율을 유지했습니다. Sony의 적층 CMOS 기술은 120fps의 4K 캡처를 추진하고 공장 자동화를 위한 머신 비전 공차를 충족합니다. 광섬유 센서는 절대 수익으로는 작지만 인프라 사업자가 킬로미터 규모의 구조 건전성 모니터링으로 이동하기 때문에 CAGR은 최대 12.7%를 보일 것으로 예측됩니다. 이 견인력으로 인해 광섬유 솔루션의 광센서 시장 규모는 2025년 47억 달러에서 2030년 86억 달러로 확대될 것으로 예상됩니다. 분산 음향 감지, 파이프라인 보안, 경계 침입 시스템이 주요 양적 촉진요인입니다.

광전 센서, 환경 광센서, 근접 센서의 다양화는 견고하지만, ASP의 저하는 부품 제조업체를 압박하고 있습니다. Vishay의 0.5mm 두께 장치와 같은 초소형 근접 모듈은 베젤리스 휴대폰 설계를 지원하며 세계 셔터 산업용 카메라는 로봇의 픽앤플레이스로 모션 블러를 제거합니다. 기타”의 멀티스펙트럼 이미저는 정밀 농업 및 식품 안전 형광 분석을 지원하여 두 자리 성장을 이루고 있습니다.

단일 광자 애벌란시 다이오드(SPAD) 및 애벌란시 포토다이오드(APD)와 같은 최첨단 광검출기는 표준 포토다이오드보다 출하량이 적음에도 불구하고 프리미엄 가격으로 판매되고 있습니다. SPAD 어레이는 피코초 레벨의 비행 시간 데이터를 제공하며, LiDAR 시스템은 자율주행 차량의 정확한 거리 측정에 활용됩니다. 이미 터 측에서 설계 팀은 LED에서 VCSEL 및 단면 발광 레이저로 이동하여 더 높은 광 출력과 더 엄격한 스펙트럼 제어를 획득했습니다.

광학 부품과 필터는 정밀한 코팅과 엄격한 공차가 신규 진출기업에 어려우므로 그램당 가장 큰 가치에 기여하고 있습니다. 메타옵틱스는 다중 요소 스택을 단일 패터닝된 레이어로 대체하여 성능을 유지하면서 크기와 무게를 줄이고 렌즈 설계를 크게 바꿉니다. 가공 전자도 같은 길을 따릅니다. 더 많은 기능이 센서 다이에 탑재되어 에지 AI를 로컬로 실행할 수 있으므로 대기 시간이 단축되고 대역폭 요구가 완화됩니다.

광센서 시장은 센서 유형(이미지 센서, 광섬유 센서, 기타), 센싱 기술(진성 센서, 기타), 구성요소(수광 소자, 광원, 기타), 파장(자외선, 가시광 등), 출력 최종 사용자용도(소비자용 전자기기, 산업용 오토메이션 및 로봇 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 매출의 33%를 차지했고 부품 공장, 모듈 조립 및 가전 브랜드가 긴밀하게 협력하고 있음을 반영합니다. 중국과 베트남 계약 제조업체는 현재 근접 센서 다이를 ASP 0.09USD 이하로 생산하고 있으며 이 지역의 비용 리더십을 강화하고 있습니다. 일본의 정밀 광학 에코시스템은 AEC-Q102 등급에 맞는 차량용 LiDAR 모듈을 지원하며, 한국의 파운드리은 적층형 이미지 센서의 수율 한계에 도전하고 있습니다.

유럽 전망의 중심은 규제 중심의 애플리케이션입니다. 독일 Tier-1 공급업체는 Euro NCAP 비전 시스템 지침을 준수하는 NIR 이미징 어레이의 장기 계약을 맺고 있습니다. 북해 플랫폼 주변에서는 EU의 메탄 배출 규제 강화에 따라 광섬유에 의한 가스 누출 감시가 확대되고 있습니다. GDPR(EU 개인정보보호규정)에 대응함으로써 OEM은 온 디바이스 생체 인증 분석으로 방향타를 끊고 고유 센서의 채택을 뒷받침하고 있습니다.

북미는 다른 지역에 앞서 새로운 개념을 계속 테스트하고 있습니다. 포토닉 신흥 기업에 대한 벤처 자금 조달은 2024-2025년에 7억 달러를 넘어, 엣지 AI 광 링크에 주목. 환경기관은 메탄 정량화를 위한 분산 섬유 네트워크를 도입하고 있으며, 종종 그린본드 발행으로 자금을 조달하고 있습니다. 한편 사우디아라비아와 UAE는 스마트시티 프로젝트에 하이퍼스펙트럼 카메라 어레이를 도입해 중동 CAGR 전망 13.6%를 견인하고 있습니다.

The optical sensors market reached USD 26.61 billion in 2025 and is projected to climb to USD 44.59 billion by 2030, advancing at a 10.88% CAGR.

Consistent regulatory pressure on automotive safety, environmental monitoring, and data privacy is steering demand toward integrated, cost-efficient silicon-photonics-based designs. Price drops in wafer-level photonics and the proliferation of AI workloads at the network edge are accelerating sensor adoption in 5G infrastructure, autonomous vehicles, and distributed fiber-optic monitoring. Material-supply risks around high-purity silica and germanium underscore the need for diversified sourcing, while miniaturization requirements in wearables and smartphones continue to shift volume production to Asia-Pacific. Competitive intensity is rising as smaller firms deploy photonic integration to rival long-established semiconductor players.

AR glasses and smart wearables now require sub-millimeter optical stacks that still meet luminous-efficiency targets. Single-layer meta-optics introduced by STMicroelectronics cut lens height by 70%, permitting under-display proximity sensing in flagship smartphones. Indium-phosphide VCSELs are replacing GaAs emitters, delivering tighter beam divergence for space-constrained devices. APAC contract manufacturers leverage these developments to secure design wins from Western brands, reinforcing the region's 33% revenue share position.

Distributed fiber sensing provides kilometre-scale temperature and strain data immune to electromagnetic interference, enabling predictive maintenance across refineries, pipelines, and high-voltage substations. Rockwell Automation notes that early-warning analytics on such data can eliminate 30% of unplanned downtime in process industries. Coupling AI-based pattern recognition with continuous optical feedback is becoming a cornerstone of Industry 4.0 strategies in North America and Europe.

Quartz mined from a handful of Appalachian deposits accounts for most global preform feedstock; Hurricane-induced outages in 2024 exposed how a single locale can squeeze optical-fiber availability. Coupled with China's export restrictions on germanium, manufacturers are negotiating long-term contracts at price premiums, delaying large-volume deployments of distributed fiber solutions. Synthetic-silica start-ups are emerging, but commercial scaling remains two to three years out.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Image sensors retained 42% share of the optical sensors market in 2024, buoyed by multi-camera smartphones and ADAS roll-outs. Sony's stacked CMOS technology pushes 120 fps 4-K capture, meeting machine-vision tolerances for factory automation. Fiber-optic sensors, while smaller in absolute revenue, are forecast to post the highest 12.7% CAGR as infrastructure operators shift toward kilometre-scale structural health monitoring. This traction lifts the optical sensors market size for fiber-optic solutions from USD 4.7 billion in 2025 toward USD 8.6 billion by 2030. Distributed acoustic sensing, pipeline security, and perimeter intrusion systems are the chief volume drivers.

Diversification across photoelectric, ambient light, and proximity sensors remains steady, although ASP erosion pressures component suppliers. Ultra-mini proximity modules like Vishay's 0.5 mm-thick device cater to bezel-less phone designs, while global-shutter industrial cameras eliminate motion blur in robotic pick-and-place. Multi-spectral imagers within the "Others" bucket are gaining double-digit growth, supporting precision agriculture and food-safety fluorescence assays.

Cutting-edge photodetectors such as single-photon avalanche diodes (SPADs) and avalanche photodiodes (APDs) sell at premium prices even though they ship in lower volumes than standard photodiodes. SPAD arrays deliver picosecond-level time-of-flight data that LiDAR systems rely on for accurate distance readings in self-driving cars. On the emitter side, design teams are moving from LEDs to VCSELs and edge-emitting lasers to gain higher optical power and tighter spectral control; VCSELs also couple easily into fiber while meeting consumer eye-safety rules.

Optics and filters contribute the most value per gram because their precision coatings and tight tolerances are hard for new entrants to match. Meta-optics is shaking up lens design by replacing multi-element stacks with single, patterned layers that keep performance but trim size and weight. Processing electronics are following the same path: more functions now sit on the sensor die, so edge AI can run locally, cutting latency and easing bandwidth demands.

Optical Sensors Market is Segmented by Sensor Type (Image Sensor, Fiber-Optic Sensor, and More), Sensing Technology (Extrinsic Optical Sensor and More), Component (Photodetectors, Light Sources, and More), Wavelength (Ultraviolet, Visible, and More), Output End-User Application (Consumer Electronics, Industrial Automation & Robotics and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 33% of 2024 revenue, reflecting its tight coupling of component fabs, module assembly, and consumer electronics brands. Contract manufacturers in China and Vietnam now produce proximity-sensor die at sub-USD 0.09 ASP, reinforcing the region's cost leadership. Japan's precision optics ecosystem supports automotive LiDAR modules meeting AEC-Q102 grade, while South Korea's foundries push the envelope on stacked-image-sensor yields.

Europe's outlook centers on regulatory-driven applications. German Tier-1 suppliers are booking long-term contracts for NIR imaging arrays that comply with Euro NCAP vision-system mandates. Fiber-optic gas-leak monitoring around North Sea platforms is expanding as EU methane-emissions rules tighten. GDPR compliance is steering OEMs toward on-device biometric analysis, supporting intrinsic sensor adoption.

North America continues to test emerging concepts ahead of other regions. Venture funding into photonic start-ups exceeded USD 700 million in 2024-2025, with a focus on edge-AI optical links. Environmental agencies deploy distributed fiber networks for methane quantification, often financed through green-bond issuances. Meanwhile, Saudi Arabia and the UAE are installing hyperspectral camera arrays across smart-city projects, driving the Middle East's 13.6% CAGR outlook.