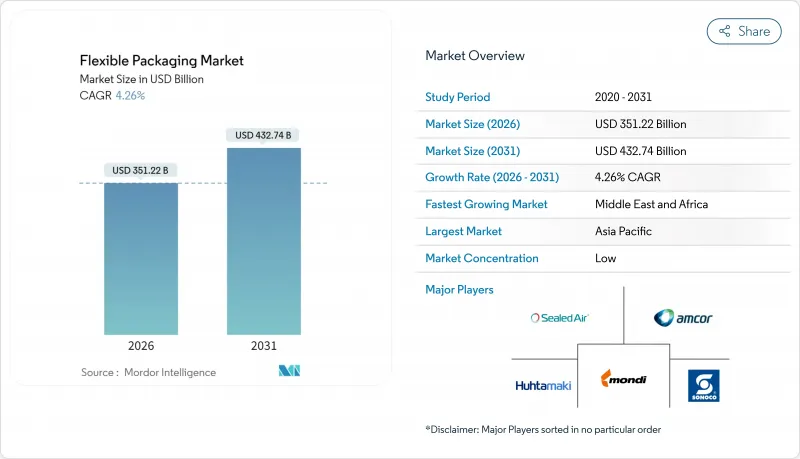

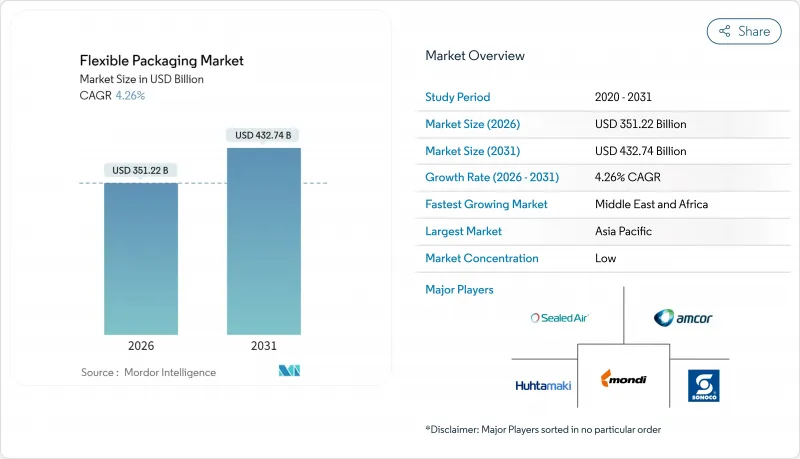

연포장 시장은 2025년 3,368억 7,000만 달러에서 2026년에는 3,512억 2,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 4.26%를 나타낼 전망입니다. 2031년까지 4,327억 4,000만 달러에 달할 것으로 예상됩니다.

지속가능성에 대한 요구가 늘어나고, 전자상거래의 급속한 확대, 경량의 고배리어 형식에 대한 브랜드 측 수요가 연포장 업계의 기회를 확대하고 있습니다. 재료 과학의 발전, 특히 단일 소재 구조의 혁신은 매립지 부담을 줄이고 가공업자에게 새로운 순환 수익원을 개척하고 있습니다. 디지털 인쇄는 틈새 제품의 출시 주기를 단축하고 Just-in-Time 워크플로우는 폴리올레핀 가격 변동으로 인한 수익 변동을 완화합니다. 지역별로는 아시아태평양의 중산계급 확대와 제조규모 확대가 그 주도적 지위를 뒷받침하고 있는 한편, 중동 및 아프리카의 포장 인프라 정비의 급성장은 이 지역의 추진 성장을 가속시키고 있습니다.

북미의 온라인 판매는 2024년에 15.4% 확대되었으며, 소매업체는 용적 중량 요금을 최대 30% 절감할 수 있는 유연한 기포 완충 봉투의 채용을 추진했습니다. 아마존이 인도에서 9,100미터톤의 플라스틱 삭감을 실현하고 재생지 쿠션 봉투의 보급을 확대하고 있는 사례는 기업의 탄소 삭감 공약이 조달을 섬유와 필름의 하이브리드 제품에 인도하고 있다는 것을 보여줍니다. 컨버터 각사의 수주 상황은 현재, 고재활용 플라스틱 함유 필름을 사용한 가정 쓰레기로서 회수 가능한 메일 봉투를 우선하고 있어 미국과 멕시코 전역에서 생산 능력의 증강이 진행되고 있습니다. 유럽에서도 적정 사이즈화 규제의 강화에 따라 수요가 확대되고, 아시아의 소포 네트워크도 같은 비용 효율형 포맷을 도입하고 있습니다. 이러한 시너지 효과로 인해 폴리코팅 봉투에 대한 수요가 지속적으로 증가하고, 연포장 산업은 기존의 FMCG 용도를 넘어 성장하고 있습니다.

인도의 2025년도 플라스틱 폐기물 관리규칙에서는 브랜드 소유자가 포장재료의 정량적인 재활용 실적을 증명할 의무가 있으며, 주요 식품·구강 케어 기업은 다층 라미네이트에서 폴리올레핀 단일 소재 필름으로의 전환을 강요받고 있습니다. Wipf AG의 PP 기반 "WICOFILM"과 같은 솔루션은 산소와 향기 장벽을 유지하면서 기존 재활용 공정에 원활하게 통합됩니다. ASEAN 지역의 퍼스널케어 브랜드도 같은 전환을 진행하고 있어, 단일 소재의 파우치를 활용하는 것으로 소매점의 회수 제도를 채우면서, 매장에서의 소구력을 확보하고 있습니다. 공급 측의 혁신은 아시아태평양 전체에 퍼져, 이 지역이 연포장 업계에서 45.24%의 점유율을 유지하는 데 도움이 되고 있습니다. EPR(확대 생산자 책임) 비용의 대부분이 해마다 상승하는 가운데, 단일 소재의 생산 능력을 확대하는 컨버터는 고수익 계약의 획득과 이익률의 안정화를 도모할 수 있는 입장에 있습니다.

원료가격의 변동폭은 2024년 두 자릿수에 달했고, 분기별 가격계약에 묶인 컨버터의 EBITDA를 압박했습니다. 아시아에서 PE&PP공급과잉과 수송장애가 변동폭을 확대하고 있습니다. 이익률에 대한 충격을 완화하기 위해, 주요 컨버터는 얇은 필름의 채용, 재고 계획의 디지털화, 바이오매스 유래 나프타 계약의 검토를 통해 리스크 분산을 도모하고 있습니다. 이 억제책은 일시적인 것이지만, 가격 안정성과 재생재 함유율이 높은 소재로의 이행을 가속화해, 간접적으로 연포장 업계공급 기반을 근대화하고 있습니다.

폴리에틸렌은 2025년 시점에서 연포장 업계의 34.12%를 차지했으며 저비용성과 방습 특성에 따라 식품 포장의 기간 용도를 지원했습니다. 수지의 입수 용이성과 확립된 리사이클 시스템에 의해 시리얼용 라이너, 냉동 식품용 필름, 세제용 파우치에 있어서 표준 소재로서의 지위를 유지하고 있습니다. 그러나 소매업체가 가정용 퇴비화 가능한 프라이빗 브랜드 제품을 도입하고 지자체에서는 유기폐기물 처리 프로그램을 확충하는 가운데 생분해성·퇴비화가능 폴리머는 2026년부터 2031년에 걸쳐 7.65%라는 가장 빠른 CAGR을 나타낼 전망입니다. 이 기세에 의해 연구개발 예산은 LDPE의 강도를 모방하면서 산업용 퇴비화 사이클 내에서 분해되는 PLA(폴리유산) 및 PHA(폴리히드록시알칸산) 기반의 공압출 기술로 재분배되고 있습니다. 종이 라미네이트는 수증기 투과성이 중간 정도로 요구되는 분야에서 재흥하고, 알루미늄박은 산소 투과성이 거의 제로인 것이 요구되는 틈새 역할을 유지합니다. EVOH는 마이크로 레이어 형태로 사용되지만, 멸균 배양액과 영양 보충제 젤에는 여전히 필수적입니다. 종합적으로 소재 포트폴리오는 가공성을 손상시키지 않고 범위 3 배출량을 줄이는 솔루션으로 전환하여 연포장 시장의 순환형 경제로의 전환을 강화하고 있습니다.

생분해성 소재의 연포장 시장 규모는 FMCG(일용소비재)의 탈탄소화 로드맵과 매립 처분 회피 비용을 배경으로 2026년 336억 달러에서 2031년에는 486억 달러로 확대될 것으로 전망됩니다. 폴리에틸렌은 여전히 사용량으로 선두를 유지하고 있지만, 소비자 범주에서 재생재 함량의 최소 기준이 설정됨에 따라 그 이점은 점차 감소할 것으로 예측됩니다. BOPP의 투명성과 강성은 스낵 식품 분야에서의 존재감을 유지하고 CPP의 히트 씰 신뢰성은 레토르트 포장이나 트위스트랩 포장에서의 채용을 보증하고 있습니다. 수지 제조업체는 화학적 리사이클 기술에 대한 투자를 확대해, 폴리프로필렌(PP)이나 폴리에틸렌(PE)의 단량체를 회수. 이것은 재료 성능을 유지하는 진정한 폴리머 투 폴리머 순환을 실현하고 있습니다. 이러한 노력이 확대됨에 따라 가공업자는 기계적, 화학적, 생분해 적 재활용 경로가 공존하는 혼합 포트폴리오를 예측합니다. 각 기술은 연포장 산업 내의 다른 채널 요구에 대응할 것으로 예측됩니다.

파우치는 2025년 수익의 46.05%를 차지했고 유리병과 캔을 70% 경량 형태로 대체하고 운송시 배출량을 삭감하는 능력이 주목받았습니다. 스탠드업 파우치는 광고 공간을 확장하여 조미료와 반려동물 먹이에서 충동 구매를 촉진합니다. 고화질 잉크젯 인쇄기의 등장에 의해 준비 공정의 폐기물이 대폭 삭감되어, 계절 한정 풍미의 SKU 확충이 가능하게 되었습니다. 이에 따라 D2C 브랜드와 프라이빗 브랜드의 리뉴얼이 지원되고 있습니다. 필름이나 랩은 매장에서의 존재감은 낮은 것, 내천자성을 손상시키지 않고 두께를 삭감한 것으로, 5.61%라고 하는 가장 높은 CAGR을 기록하고 있습니다. 나노클레이나 산화규소 배리어 코팅이 알루미늄층 대신, 선별성과 재활용성을 향상시키고 있습니다.

한편, 가방·자루 분야의 연포장 시장 규모는 비료·시멘트·독 푸드 수요에 지지되어 안정을 유지합니다. 사쉐와 스틱팩은 특히 외출처에서의 소비가 증가하는 동남아시아를 중심으로 단회용 영양보조식품과 인스턴트 음료시장에 침투를 계속하고 있습니다. 향후 5년간 디지털 인쇄기의 가동 시간, 무용제 라미네이션, 전자빔 경화 기술의 상호작용으로 리드 타임이 몇 주에서 며칠로 단축될 것으로 예측됩니다. 이로 인해 컨버터는 공장 레이아웃의 재고를 강요받을 것입니다. 궁극적으로는 대규모 외식 산업용 생산과 인플루언서와의 협업을 위한 소량 생산을 유연하게 전환할 수 있는 민첩한 운영을 가능하게 하는 제품 구성이 요구됩니다.

연포장 시장 보고서는 소재 유형(플라스틱, 종이, 알루미늄박, 생분해성 소재), 제품 유형(파우치, 가방, 필름, 기타), 최종 이용 산업(식품, 음료, 의약품, 화장품, 공업, 기타), 유통 채널(직접, 간접), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 예측은 금액(달러)으로 표시됩니다.

아시아태평양은 도시화, 가처분 소득 증가, 제조업 지원 정책을 통해 2025년에도 연포장 업계의 44.70%라는 압도적인 점유율을 유지했습니다. 중국의 스마트 공장 투자와 인도의 식품 가공용 생산 연동형 장려 제도(PLI)가 국내의 수지·필름 생산 능력을 지지하고 있습니다. UFlex는 폴리에스터 칩의 생산량을 두 배로 늘리고, 사용한 원료를 통합하는 PCR 플랜트를 가동시켜, 순환형 공급 제안을 강화했습니다. 지역 컨버터 각사도 향후 도입되는 EPR(확대생산자책임)제도에 따른 비용부담에 대비하여 단일소재제품의 전개를 주도하고 있으며, 이 지역의 성장궤도를 더욱 강화하고 있습니다. 한편 동남아 국가들은 면세 무역 클러스터를 활용하여 스탠드업 파우치 수출을 확대하고 역내 무역 흐름을 활발히 하고 있습니다.

북미는 제2의 중요한 거점으로 전자상거래용 봉투의 채용 확대와 의약품 콜드체인의 성장에 견인되고 있습니다. 소매업체는 How2Recycle 인증된 파우치의 채용을 추진하고 PE 필름의 재활용성 향상을 촉진하고 있습니다. OEM 제조업체는 디지털 검사를 통합하고 FDA 기준의 추적성을 보장함으로써 시장의 건전성을 강화하고 있습니다. 유럽은 EU 플라스틱 폐기물 지침(PPWR)을 전략의 핵으로 삼아 화학적 재활용 시험 플랜트와 섬유계 연포장에 자금 투입을 진행하고 있습니다. 몬디사와 후타마키사는 각각 리사이클 가능한 레토르트 라인과 블루루프사의 포트폴리오를 확대하여 대규모 리사이클 설계 원칙의 통합을 추진하고 있습니다.

중동 및 아프리카는 2031년까지 연평균 복합 성장률(CAGR) 6.03%로 가장 높은 성장이 예측되며, 사우디아라비아나 이집트에서 외국 직접투자(FDI) 지원 식품허브가 이를 뒷받침합니다. 아프리카 포장 시장은 2031년까지 560억 2,000만 달러 규모에 이를 것으로 예측되며, 그중 연포장은 2033년까지 33억 8,000만 달러를 초과할 수 있습니다. 건조 기후 하에서 장기 보존을 가능하게 하는 파우치가 현대 소매 체인에 요구되고 있어, 고차단성 필름의 수입을 촉진하고 있습니다. 남미의 스페셜티 커피 붐은 탈기 밸브가 있는 파우치 수요를 강화하는 한편, 통화 변동에 의해 경량인 연포장 산업이 경질 유리나 금속보다 매력적으로 비치고 있습니다. 지역을 불문하고 공통되는 경향으로서, 규제 주도의 리사이클 목표가 컨버터의 연구 개발을 통일해, 단일 소재화를 위한 로드맵을 추진하고 있습니다.

The Flexible Packaging market is expected to grow from USD 336.87 billion in 2025 to USD 351.22 billion in 2026 and is forecast to reach USD 432.74 billion by 2031 at 4.26% CAGR over 2026-2031.

Rising sustainability mandates, rapid e-commerce expansion, and brand demand for lightweight, high-barrier formats are widening the flexible packaging industry opportunity. Material science breakthroughs, particularly in mono-material structures, are reducing landfill pressure and unlocking new circular revenue streams for converters. Digital printing is compressing launch cycles for niche products, while just-in-time workflows mitigate the earnings volatility caused by polyolefin price swings. Regionally, Asia Pacific's expanding middle class and manufacturing scale underpin its leadership, whereas the Middle East and Africa's packaging infrastructure boom is accelerating its catch-up growth.

North American online sales expanded by 15.4% in 2024, pushing retailers to adopt flexible bubble mailers that cut dimensional-weight fees up to 30%. Amazon's removal of 9,100 metric tons of plastic in India and its wider rollout of recyclable paper padded bags illustrate how corporate carbon pledges are steering procurement toward fiber-and-film hybridsConverter order books now favor curbside-recyclable mailers with high recycled-content films, spawning capacity additions across the United States and Mexico. Volumes are also spilling into Europe as right-sizing mandates tighten, while Asian parcel networks replicate these cost-efficient formats. The net effect is a sustained uplift in poly-coated mailer demand that lifts the flexible packaging industry beyond traditional FMCG end uses.

India's Plastic Waste Management Rules in FY 2025 require brand owners to demonstrate quantifiable recycling of their packaging footprints, compelling leading food and oral-care players to replace multilayer laminates with polyolefin-only films. Solutions such as PP-based WICOFILM from Wipf AG preserve oxygen and aroma barriers yet flow seamlessly through existing recycling streams. ASEAN personal-care brands echo this switch, leveraging mono-material pouches to secure shelf appeal while satisfying retailer take-back schemes. Supply-side innovation is spreading across Asia Pacific, helping the region reinforce its 45.24% hold on the flexible packaging industry. With most EPR fees escalating annually, converters that scale mono-material capacity are positioned to secure premium contracts and margin resilience.

Feedstock volatility reached double-digit spreads in 2024, eroding EBITDA for converters locked into quarterly price agreements. Asian PE and PP oversupply and shipping disruptions amplify the swings. To blunt margin shocks, leading converters deploy thinner gauge films, digitalize inventory planning, and explore biomass-based naphtha contracts to diversify risk exposure. This restraint remains transitory yet accelerates the shift toward materials that provide price stability and recycled content, indirectly modernizing the flexible packaging industry supply base.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyethylene underpinned 34.12% of flexible packaging industry share in 2025, leveraging its low cost and moisture barrier attributes to anchor core food applications. Its wide resin availability and established recycling streams keep it the default choice for cereal liners, frozen food films, and detergent pouches. However, biodegradable and compostable polymers exhibit the fastest 7.65% CAGR from 2026-2031 as retailers introduce home-compostable private-label lines and municipalities upgrade organic waste programs. This momentum realigns R&D budgets toward PLA- and PHA-based coextrusions that mimic LDPE toughness yet break down within industrial composting cycles. Paper laminates also resurge where water vapor requirements are moderate, while aluminum foil defends niche roles that demand near-zero oxygen transmission. EVOH, albeit used in microlayer form, remains critical for aseptic broths and nutraceutical gels. Collectively, the material portfolio is pivoting toward solutions that reduce Scope 3 emissions without forfeiting machinability, reinforcing the flexible packaging market's pivot to circularity.

The flexible packaging industry size for biodegradable materials is projected to climb from USD 33.6 billion in 2026 to USD 48.6 billion in 2031, fueled by FMCG decarbonization roadmaps and landfill diversion fees. Polyethylene still commands the volume crown, yet its dominance is expected to edge down as consumer-facing categories impose minimum recycled-content thresholds. BOPP's clarity and stiffness uphold its presence in snack foods, while CPP's heat-seal reliability ensures its inclusion in retort and twist-wrap packs. Resin makers are investing in chemical recycling to recapture PP and PE monomers, enabling true polymer-to-polymer loops that preserve material performance. As these initiatives scale, converters foresee a blended portfolio where mechanical, chemical, and bio-degradation pathways coexist, each serving distinct channel needs within the flexible packaging industry.

Pouches generated 46.05% of 2025 revenue, spotlighting their ability to replace glass jars and tins with 70% lighter formats that lower freight emissions. Stand-up pouches enhance billboard space, driving impulse purchases in condiments and pet food. The advent of high-definition inkjet presses slashes make-ready waste and enables SKU proliferation for seasonal flavors, supporting D2C brands and private-label refreshes. Films and wraps, while less visible on shelf, register the sharpest 5.61% CAGR by trimming gauge thicknesses without sacrificing puncture resistance. Nanoclay and silicon oxide barrier coatings now substitute aluminum layers, improving sortability and stream recyclability.

Meanwhile, the flexible packaging industry size for bags and sacks holds steady, buoyed by fertilizer, cement, and dog-food demand. Sachets and stick packs continue to penetrate single-serve nutraceuticals and instant beverages, particularly in Southeast Asia where on-the-go consumption is rising. Over the next five years the interplay between digital press uptime, solvent-less lamination, and e-beam curing is expected to compress lead times from weeks to days, pushing converters to rethink plant layouts. The end result is a product mix that rewards agile operations able to toggle between long food-service runs and micro batches for influencer collaborations.

The Flexible Packaging Market Report is Segmented by Material Type (Plastic, Paper, Aluminum Foil, Biodegradable Materials), Product Type (Pouches, Bags, Films, Others), End-Use Industry (Food, Beverage, Pharmaceutical, Cosmetics, Industrial, Others), Distribution Channels (Direct, Indirect), and Geography (North America, Europe, Asia Pacific, South America, MEA). Market Forecasts are in Value (USD).

Asia Pacific retained a commanding 44.70% share of the flexible packaging industry in 2025 due to urbanization, rising disposable incomes, and pro-manufacturing policies. China's smart-factory investments and India's Production Linked Incentive scheme for food processing underpin domestic resin and film capacity. UFlex doubled polyester chip output and commissioned a PCR plant to integrate post-consumer feedstock, fortifying a circular supply proposition. Local converters also spearhead mono-material rollouts to comply with forthcoming EPR fees, reinforcing the region's trajectory. Meanwhile, Southeast Asian nations leverage duty-free trade clusters to export stand-up pouches, lifting intraregional trade flows.

North America is the second-largest node, propelled by e-commerce mailer adoption and pharmaceutical cold-chain growth. Retailers press for How2Recycle-certified pouches, prompting PE film recyclability upgrades. OEMs integrate digital inspection to guarantee FDA-grade traceability, reinforcing market integrity. Europe anchors its strategy around the EU PPWR, channeling funds into chemical-recycling pilot plants and fiber-based flexibles. Mondi and Huhtamaki expand recyclable retort lines and blueloop portfolios, respectively, embedding design-for-recycling principles at scale.

The Middle East & Africa is forecast to post the fastest 6.03% CAGR to 2031, aided by FDI-backed food hubs in Saudi Arabia and Egypt. Africa's packaging sector is on course to hit USD 56.02 billion by 2031, of which flexible formats could surpass USD 3.38 billion by 2033. Modern retail chains require extended-shelf-life pouches for arid climates, stimulating imports of high-barrier films. South America's specialty coffee boom strengthens demand for degassing valve pouches, while currency volatility makes the lighter flexible packaging industry more attractive than rigid glass or metal. Across regions, a common thread is regulatory-driven recycling targets that unify converter R&D roadmaps toward mono-materials.