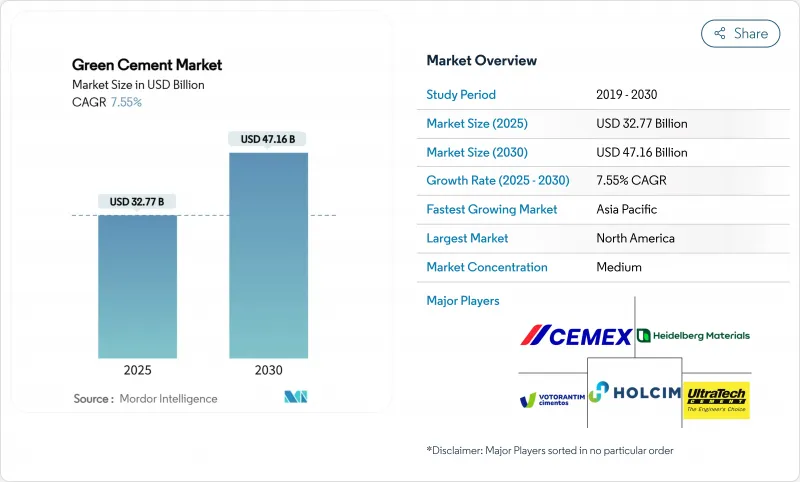

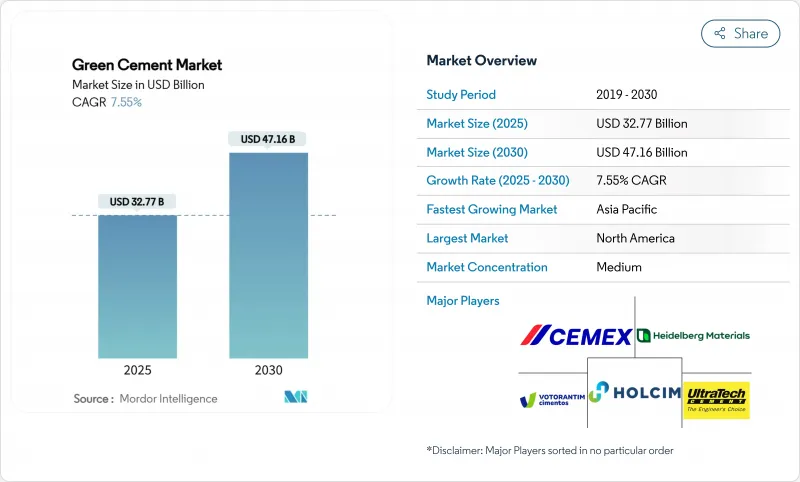

세계의 그린 시멘트 시장 규모는 2025년 327억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 7.55%로 확대되어, 2030년에는 471억 6,000만 달러에 달할 것으로 예측됩니다.

규제의 의무화, 탄소가격 상승, 저탄소재료를 우월하게 하는 조달규칙에 따라 그린 시멘트 시장은 틈새 상황에서 공공 프로젝트와 민간 프로젝트에서 주류의 선택으로 전환하고 있습니다. 비산회 기반의 배합이 최대 매출 점유율을 차지하는 한편, 인프라 지출과 ESG 연동 대출이 비주택 공사에서의 채용을 가속화하고 있습니다. 아시아태평양이 가장 급성장하고 있는 반면 북미는 조기 정책 도입과 성숙한 공급망을 통해 판매량의 주도권을 유지하고 있습니다. 경쟁의 격렬함은 기존 시멘트 메이저가 그린 포트폴리오를 확대하고 전문 제조업체가 확보한 원료 계약을 활용하기 때문에 완만한 것에 그칩니다.

저탄소 조달의 의무화 정책은 일반적으로 포틀랜드 시멘트에서 검증된 녹색 배합으로 수요 이동을 즉시 촉구합니다. 캘리포니아는 2035년까지 시멘트 부문 배출량을 40% 절감하고 2045년까지 넷 제로화하는 것을 목표로 하고 있으며, 미국의 다른 주에서도 비슷한 노력을 하고 있습니다. EU의 개정 건설 제품 규칙은 2024년부터 콘크리트의 디지털 여권과 CO2 정보 공개를 의무화하고, 이미 라이프 사이클 문서를 갖춘 생산자를 입찰 목록의 최전선으로 밀어 올리고 있습니다. 프랑스, 덴마크, 아일랜드, 뉴욕은 각각 점진적인 배출량 한도 또는 Buy Clean 규칙을 도입하여 적합 재료를 비싼 옵션이 아닌 기본 옵션으로 사용합니다. 각 주가 선구적인 법령을 복제함에 따라, 그린 시멘트 시장은 전통적인 생산자가 가마 개수 및 전문업체와의 제휴에 의해서만 대응 가능한 정책 주도형의 성장 플로어를 획득하고 있습니다.

탄소 비용은 CO2를 직접적인 비용으로 바꾸어 클링커의 경제성을 변화시킵니다. EU의 배출권 거래제도는 무료 배출량을 서서히 삼키고 시멘트 제조업체에 저탄소 대체를 가속화하거나 마진 압축의 위험을 촉구합니다. 중국의 국가 거래 플랫폼이 시멘트를 커버하게 되어 세계 최대의 생산국에 대한 비용 압력이 높아지고 있습니다. 더 많은 지역이 탄소 가격을 결정함에 따라 보완적인 시멘트 재료는 상대적인 경쟁력을 얻고 있으며, 그린 시멘트 시장은 기존 제품보다 구조적 비용 우위를 누리고 있습니다.

일부 건설업자들은 양생시간의 연장, 한랭지에서의 경화의 지연, 보조재료의 입수 가능한 지역이 일정하지 않음 등을 이유로 사양 변경에 저항하고 있습니다. 표준화 단체는 규정 배합 제한을 성능 기반 지침으로 대체하기 위해 노력하고 있지만, 특히 중소기업에서는 지식의 격차가 여전히 남아 있습니다. 주류에 채택되기 위해서는 실증 프로젝트와 목표를 세운 훈련이 여전히 필수적입니다.

비산회 기반 제제는 2024년 그린 시멘트 시장 점유율에서 44.22%를 차지했으며 석탄 연소 잔류물이 풍부하게 남아 있는 지역에서는 저탄소 대용품으로 기본 지위를 차지하고 있음이 밝혀졌습니다. 생산자는 성숙한 물류와 충분한 성과를 활용하여 대규모 인프라 계약 및 정부 입찰을 지원합니다. 그러나 석탄 발전량이 감소함에 따라 미래의 원료 풀은 좁아지고 기업은 기존 애쉬 파운드를 채취하거나 석회석과 소성 점토의 혼합으로 이동해야합니다. 배출량을 최대 40% 절감할 수 있는 LC3 기술은 보통 포틀랜드 시멘트와의 기계적 동등성을 실험실이 검증함에 따라 인지도를 높이고 있습니다. 실리카 흄을 주성분으로 하는 콘크리트는 해양 구조물과 화학물질 봉쇄 구조물에 적합한 불침투성 콘크리트를 제공하며, 고규격의 틈새를 차지하고 있습니다. 슬래그를 주성분으로 하는 대체 재료는 임박한 공급 시프트에 고전을 겪고 있지만, 일관제철소 근처에서는 관련성을 유지하고 있습니다. 지오폴리머 콘크리트를 포함한 새로운 바인더 화학물질은 파일럿 프로젝트를 통해 발전하고 있으며, 규모의 경제성이 개선되면 녹색 시멘트 시장을 다양화할 수 있습니다.

다양화의 발전은 단일 보조 흐름에 대한 과도한 의존성을 줄이고 생산자를 원료의 충격으로부터 보호합니다. 벌채회가 미국 비산회 재사용량의 10%를 차지하고 공급 안정성은 향상되지만 처리 비용은 상승합니다. 그러므로 시멘트 제조업체와 석탄재 재생 사업체 간의 전략적 합의는 최근의 거래 흐름에서 두드러지게 특징적입니다. 슬래그 분쇄 파트너십과 점토 소성 합작투자는 기업이 기술적 실현 가능성, 배출 목표, 원재료의 경제성의 균형을 잡는 데 마찬가지로 중요합니다.

북미는 2024년 판매의 37.88%를 차지하고, 연방과 국가 바이클린 규칙, 초기 탄소 포집 시험, 혼합 시멘트에 익숙한 계약자에 의해 지원됩니다. Heidelberg Materials의 Mitchell CCS 프로젝트는 30년 동안 5,000만 톤 이상의 CO2 지중 저류를 목표로 하고 있으며, 장기적인 양적 헌신을 지원하는 인프라를 시사하고 있습니다. 공급의 가용성은 지역에 따라 다릅니다. 중서부의 국가는 석탄재의 유역에 가깝다는 이점을 활용하고, 해안부는 슬래그와 소성 점토를 수입하여 사양을 충족합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 8.22%를 기록하며, 이는 인도의 여러 해에 걸친 인프라 파이프라인과 동남아시아 전역에서 점차 엄격해지는 법규제에 힘쓰고 있습니다. 중국의 통합 노력은 부동산 부문의 역풍이 부는 동안 허가를 유지하기 위해 저탄소 노선에서 공장을 업그레이드하는 것을 선도하는 그룹에게 촉구합니다. 세계의 고속철도망의 3분의 2가 이 지역에 있으며, 배출규제 강화에 대응한 콘크리트가 필요하며, 궤도나 역의 스톡을 보충하는 프로젝트로서 그린 시멘트 시장에 혜택을 가져옵니다.

유럽은 견고한 기후 변화 정책과 성숙한 산업 능력을 융합시키고 있습니다. 아일랜드의 2024년 전주 프로젝트에서 저탄소 시멘트 의무화, 덴마크의 2025년 7.1kg-CO2e/m2/년 배출 상한은 영향력 있는 벤치마크를 설정했습니다. CO2 비용이 낮은 클링커 믹스에 대한 입찰 평가를 기울이기 때문에 탄소 가격은 건설량의 변화에도 불구하고 녹색 시멘트 시장 규모를 확실히 확대합니다. 중동 및 아프리카에서는 수소 허브와 대규모 유틸리티을 계획하고 있는 걸프 국가를 중심으로 새로운 수요가 태어나고 있지만, 통일된 가이드라인이 성숙할 때까지 단편적인 기준과 한정된 현장 전문 지식에 의해 보급이 지연됩니다.

The Green Cement Market size is estimated at USD 32.77 billion in 2025, and is expected to reach USD 47.16 billion by 2030, at a CAGR of 7.55% during the forecast period (2025-2030).

Regulatory mandates, rising carbon prices, and procurement rules that favor low-carbon materials move the green cement market from niche status to mainstream selection in public and private projects. Fly-ash-based formulations command the largest revenue share, while infrastructure spending and ESG-linked financing accelerate uptake across non-residential works. Asia-Pacific provides the fastest growth, whereas North America retains volume leadership because of early policy adoption and mature supply chains. Competitive intensity stays moderate as incumbent cement majors scale green portfolios and specialized producers leverage secured feedstock contracts.

Mandatory low-carbon procurement policies drive immediate demand shifts from ordinary Portland cement to verified green formulations. California targets a 40% emissions cut for its cement sector by 2035 and net-zero by 2045, anchoring similar actions in other U.S. states. The EU's revised Construction Products Regulation obliges digital passports and CO2 disclosure for concrete from 2024, pushing producers already equipped with life-cycle documentation to the front of tender lists. France, Denmark, Ireland, and New York State have each introduced progressive emissions ceilings or Buy Clean rules that make compliant materials the default choice rather than a premium option. As jurisdictions replicate pioneering statutes, the green cement market gains a policy-driven growth floor that traditional producers can meet only by retrofitting kilns or partnering with specialized suppliers.

Carbon costs alter clinker economics by turning CO2 into a direct expense. The EU Emission Trading System gradually withholds free allowances, prompting cement manufacturers to accelerate low-carbon substitutions or risk margin compression. China's national trading platform now covers cement, expanding cost pressure to the world's largest producer. As more regions price carbon, supplementary cementitious materials gain relative competitiveness, and the green cement market benefits from a structural cost advantage over legacy products.

Some contractors resist specification changes, citing extended curing, cold-weather set delays, and inconsistent regional availability of supplementary materials. Standards bodies work to replace prescriptive mix limits with performance-based guidelines, yet knowledge gaps persist, especially in small and mid-size firms. Demonstration projects and targeted training remain essential for mainstream adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fly-ash-based formulations kept a 44.22% green cement market share in 2024, underscoring their status as the default low-carbon substitute where coal-combustion residues remain abundant. Producers leverage mature logistics and well-documented performance to serve large infrastructure contracts and government tenders. However, declining coal generation narrows future feedstock pools, prompting companies to harvest legacy ash ponds or shift toward limestone-calcined clay blends. LC3 technology, able to trim emissions by up to 40%, gains visibility as laboratories validate mechanical parity with ordinary Portland cement. Silica-fume-based variants occupy high-specification niches, delivering impermeable concrete suited to marine and chemical containment structures. Slag-based alternatives struggle with impending supply shifts but retain relevance near integrated steelworks. Novel binder chemistries, including geopolymer concretes, progress through pilot projects that could diversify the green cement market if scale economics improve.

Growing diversification reduces over-reliance on any single supplementary stream and insulates producers from raw-material shocks. With harvested ash constituting 10% of recycled U.S. fly ash, supply security improves, yet processing costs rise. Strategic agreements between cement makers and utility coal-ash reclamation entities therefore feature prominently in recent deal flow. Slag-grinding partnerships and clay-calcination joint ventures become equally critical as companies balance technical feasibility, emissions objectives, and raw-material economics.

The Green Cement Market Report is Segmented by Product Type (Fly-Ash-Based, Slag-Based, Limestone-Based, Silica-Fume-Based, Other Product Types), Construction Sector (Residential, Non-Residential), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 37.88% of 2024 revenues, anchored by federal and state Buy Clean rules, early carbon-capture pilots, and high contractor familiarity with blended cements. Heidelberg Materials' Mitchell CCS project alone targets geological storage for more than 50 million t of CO2 over 30 years, signaling infrastructure that can underpin long-run volume commitments. Supply availability differs by region: Midwest states leverage proximity to coal-ash basins, while coastal areas import slag or calcined clay to meet specifications.

Asia-Pacific registers the fastest 8.22% CAGR to 2030, fueled by India's multi-year infrastructure pipeline and progressively stricter codes across Southeast Asia. China's consolidation efforts prompt large groups to upgrade plants with low-carbon lines to retain permits amid property-sector headwinds. Two-thirds of global high-speed rail networks reside in the region, requiring concrete that satisfies tightening emissions caps and boon the green cement market as projects replenish track and station stock.

Europe blends robust climate policy with mature industrial capabilities. Ireland's 2024 mandate for low-carbon cement in all state projects and Denmark's 2025 emissions ceiling of 7.1 kg CO2e/m2/year set influential benchmarks. Carbon pricing ensures that the green cement market size expands despite construction-volume volatility, as CO2 costs tilt bid evaluations toward low-clinker mixes. The Middle East and Africa witness emerging demand, especially in Gulf economies planning hydrogen hubs and large-scale public works, yet fragmented standards and limited on-site expertise slow penetration until harmonized guidelines mature.