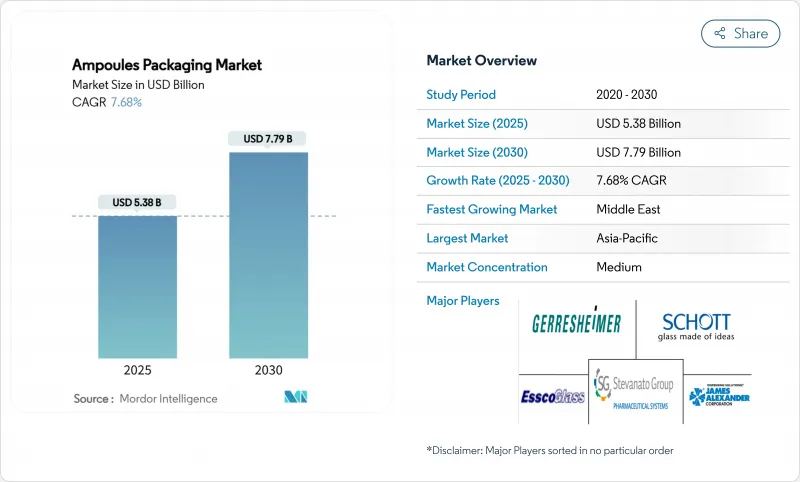

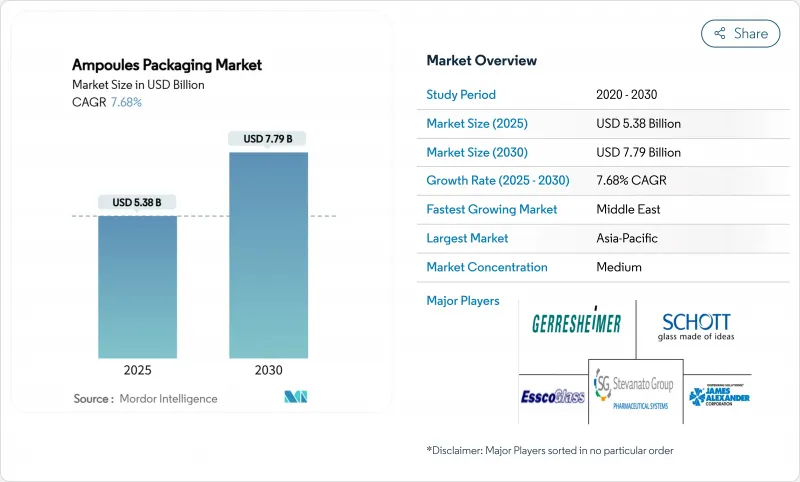

앰풀 포장 시장은 2025년에 53억 8,000만 달러로 추정되고, 2030년에는 77억 9,000만 달러로 확대될 것으로 예측되며, 예측 기간 CAGR 7.68%로 성장할 전망입니다.

확대는 생물 제제의 성장과 변조 방지 및 연속 용기를 우선하는 세계적인 규제에 의해 추진되는 의약품 분야의 단회 투여 주사제 포맷으로의 축족이 되고 있습니다. 유리 앰풀은 화학적 불활성 및 확립된 규제 수용성을 결합하여 현재 주류가 되고 있지만, Blowfill Seal(BFS) 플랫폼이 무균성과 비용 이점을 입증함에 따라 플라스틱 형식도 빠르게 확대되고 있습니다. 중국과 한국이 2024년 보툴리눔툭신(보톡스)의 새로운 적응증을 승인했기 때문에 아시아태평양이 수요를 선도하고 있으며, AI 대응의 육안 검사 라인이 대량 생산업체의 품질 보증 향상을 가속화하고 있습니다. 경쟁의 심각성은 여전히 완만합니다. 주요 공급업체는 단가가 아니며 브레이크 시스템 설계, 추적성 기능 및 지속가능성 프로그램으로 차별화를 도모하고 에너지 관련 비용이 변동하더라도 이익을 완화하고 있습니다.

의약품 제조업체는 FDA 21 CFR 211.132 및 EU의 위조 의약품 지침의 요구 사항을 충족하기 위해 눈에 띄는 탬퍼 증거에 많은 투자를 하고 있으며, 앰풀 사양의 방향성을 간섭할 수 없는 지표를 생성하는 브레이크 링 및 스코어 라인 기술로 이끌고 있습니다. SCHOTT Pharma의 One-Point-Cut 시스템은 2024년까지 세계 브레이크 시스템 서브마켓의 62%를 차지했으며, 환자 안전 기능이 프리미엄에서 표준 기대로 전환되었음을 보여줍니다. 무결성이 손상되면 치료 효과가 직접 위협을 받기 때문에 탬퍼 증거는 고가치 생물 제제의 법적 책임 위험도 감소시킵니다. 병원은 점점 더 조달 기준으로 단순화된 진정성 점검을 제시하고 있으며, 공급업체는 견고한 브레이크 설계를 선호하도록 촉구되고 있습니다. 그 결과 대체 재료의 인증 기준이 엄격해지고 치명타 관리 제형에서 유리의 우위가 강화되었습니다.

지속가능성의 의무화로 인해 이해관계자들은 품질 저하 없이 생산 루프에 재참가할 수 있는 용기를 선호하게 되었습니다. SCHOTT 파마, Corplex, 다케다 약품에 의한 2024년의 클로즈드 루프 파일럿 시험에서는 USP'660'의 내약품성 벤치마크를 충족하면서 버진 유리에 비해 온실가스 배출량을 50% 삭감했습니다. 유럽의 규제 당국은 현재 조달 인센티브를 재활용 가능성 점수와 연결하고 있으며 지역 의료 시스템이 칼렛 스트림 유래 유리를 선호하도록 장려하고 있습니다. SGS의 감사는 재활용된 Type-I가 동일한 가수분해 안정성을 유지하는 것으로 확인되었으며, 의약품 품질 기준값은 그대로 유지됩니다. 브랜드 오너가 스코프 3의 탈탄소화를 목표로 하는 가운데, 트레이서블한 재활용 함량을 보증하는 앰풀 제조업체는 공급 계약 상의 우위성을 확보하고 있습니다. 다국적 기업이 EU의 ESG 기준을 아시아태평양의 입찰 프로세스에 도입하고 있기 때문에 이러한 움직임은 아시아태평양에도 미치고 있습니다.

소매 지향적인 생물학적 제제와 자가 투여형 치료제는 투여 정확성과 환자 편의성을 제공하는 즉시 주사기로 전환하고 있습니다. Stevanato Group이 2024년에 주사기 매출을 15% 급증시킨 것은 바이알병의 매출이 34% 감소한 것과 동시기이며, 주사기 대체 압력을 예증하고 있습니다. 주사기는 금리가 크기 때문에 생산자는 앰풀에서 퍼니스 시간을 돌립니다. 이 시프트는 자가주사의 어드히어런스가 지불자 선호의 원동력이 되는 블록버스터의 GLP-1 작용제에 의해 가속됩니다. 그럼에도 불구하고 주사기 마개와 관련된 실리콘 오일과 텅스텐 잔류물에 민감한 약물에는 앰풀이 필수적인 것은 아닙니다. 수요 프로파일이 세분화되어 있기 때문에 앰풀 제조업체는 틈새 시장에서 안정성이 중요한 분자를 타겟으로 하고, 유리 순도의 우위성을 강조하는 마케팅에 투자할 수밖에 없습니다.

2024년 앰풀 포장 시장에서 유리제는 87%의 점유율을 유지했으며, 규제 당국의 신뢰성 정착과 비교할 수 없는 화학적 내구성을 반영하고 있습니다. 그러나 플라스틱은 무균 검증 단계를 줄이고 인건비를 줄이는 BFS 라인을 통해 2030년까지 연평균 복합 성장률(CAGR) 9.78%로 성장할 전망입니다. 유리 제제에서는 생물 제제, 암치료제, 반응성이 높은 화합물에는 i형 붕규산염이 주류입니다. 코닝의 Valor 조성은 가수분해성 클래스 i의 특성을 유지하면서 층간 박리를 없애고, 고스트레스한 콜드체인 환경에 유리의 적용 범위를 넓혀줍니다.

제조업체는 다양한 비즈니스 모델을 채용하고 있습니다. SCHOTT Pharma의 2024년 매출의 55%는 프리미엄 가격으로 고가치 유리 제품에 의한 것에 반해, 폴리머의 스페셜리스트는 백신이나 제네릭 의약품의 판매량을 추구하고 있습니다. 용기의 성형, 충전, 밀봉을 원패스로 할 수 있기 때문에 2차 포장의 필요성이 줄어들고, 공급망이 단순하게 됨으로써, 플라스틱의 경제성이 강화됩니다. 그럼에도 불구하고, 유리 기반 솔루션 시장 규모는 2025년에 46억 9,000만 달러가 되어, 플라스틱의 6억 9,000만 달러를 능가했습니다. 이 궤적은 치료 위험 허용도, 필요한 보존 가능 기간 및 지속가능성 계산에 따라 달라지며 대체 대신 공존을 나타냅니다.

2024년 앰풀 포장 시장 점유율에서는 스트레이트 스템 앰풀이 63%로 선두에 올랐지만, 원포인트 컷(OPC), 스코어링, 컬러 브레이크 링 디자인 등 사용하기 쉬운 포맷이 CAGR 9.21%로 증가하고 있습니다. 의료 제공자는 조달 기준으로 바늘 찌르기 손상 및 파손 불만을 줄이는 경향이 강해지고 있으며 간편한 개방 옵션이 간호 및 재택 케어 현장에서 필수적입니다. 이와 병행하여, 깔때기 형 앰풀은 넓은 목이 효율적인 충전을 가능하게 하는 점성 제제 및 현탁 제제와 관련성을 유지합니다.

Easy Open은 백신과 뷰티에서 자가 투여의 추세에도 도움이 됩니다. SCHOTT Pharma의 easyOPC 설계는 개전력 변동을 60% 줄이고 준비 시 유출 위험을 줄입니다. 브레이크 시스템의 특허가 끊어지면, 중견 제조업체도 이러한 기능을 모방할 수 있게 되어, 이익률이 낮은 치료 클래스에서의 가격 경쟁이 격화합니다. 그럼에도 불구하고 고급 생물 제제는 무균성 및 추적성을 보장하는 독자적인 브레이크 기술을 계속 지지하고 있으며, 혁신 리더의 마진 회복력이 강화되고 있습니다. Easy Open Variant의 앰풀 포장 시장 규모는 인체공학적 가치의 차별화에 힘입어 2030년까지 21억 달러 이상에 달할 것으로 예측됩니다.

아시아태평양은 2024년에는 세계 매출의 39%를 차지했으며, 중국, 인도, 한국에서 각국 정부의 주사제 공급망 현지화에 따른 생산 능력 확대가 뒷받침하고 있습니다. 중국의 바이오 의약품 생산량은 2024년에 5,653억 위안(784억 달러)에 이르렀으며, 2029년에는 1조 4,000억 위안(1,940억 달러)을 초과할 전망입니다. 한국에서는 강남의 미학 클러스터가 일관된 소량 생산 유리의 수주를 촉진하고 인도에서는 '메이크 인 인디아'의 인센티브가 백신용 BFS의 능력 증강을 지지하고 있습니다. 동시에 ASEAN 국가들은 세제 우대 조치와 GMP 승인의 합리화를 통해 CDMO를 유치하여 지역 경쟁력을 높이고 있습니다.

북미는 생물 제제의 상업화 파이프라인과 연속적인 1차 용기를 필요로 하는 DSCSA의 준수 기한에 지지되어 안정적인 성장을 보이고 있습니다. 미국에서는 비경구용 육안 검사에 관한 USP '1790'의 권장 사항을 충족하는 Type-I 유리와 AI 대응 검사 라인의 고액 수주가 견인하고 있습니다. 캐나다에서는 미국의 추적성 기준을 충족하기 위해 공급업체에게 이중 언어 패키징 및 GS1 호환 코드를 제공하도록 권고합니다. 특필해야할 것은 제초제 소송과 공급망 쇼크가 의약품 제조업체에 멕시코로부터의 앰풀 이중 조달을 촉구하고 북미 역내 무역을 확대하고 있다는 것입니다.

유럽은 지속가능성과 서큘러 순환경제의 목표가 구매를 좌우하는 풍부한 가치를 가지고 있는 성숙한 지역입니다. EU의 포장 및 포장 폐기물 규제의 개정으로 2030년까지 재활용률 70% 이상이 의무화되어, 폐쇄 루프의 Type-I 유리에 대한 수요가 높아지고 있습니다. 독일 병원은 2024년에 구매 컨소시엄을 결성하여 50% 이상의 칼렛 함량을 가진 공급업체와 5년간 계약을 맺게 되었습니다. 한편, 가스 공급 감소에 따른 에너지 가격 변동은 퍼니스 다운타임에 대한 우려를 높였으며 일부 기업은 붕규산염 튜브를 비축하도록 촉구했습니다. 그러나 생명 과학 인프라에 충당되는 EU 부흥 기금이 차세대 검사 장비에 보조금을 내고 비용 우려를 일부 상쇄하게 됩니다.

중동에서는 사우디아라비아와 UAE가 공중 보건 예산을 현지 제조업으로 돌이키기 위해, 2030년까지 연평균 복합 성장률(CAGR) 9.03%로 지역 최고를 기록할 전망입니다. 리야드의 '비전 2030' 제약 프로그램은 무균 주사제 플랜트에 공동 출자하여 BFS와 튜블러 라인의 그린 필드 수요를 창출합니다. 걸프 협력 회의 입찰 규칙은 비용 효과를 우선하므로 인도와 유럽의 중견 기업이 점유율을 얻습니다. 그러나 숙련 노동자가 제한되어 있기 때문에 장비 공급과 장기 서비스 계약을 포함한 기술 이전 파트너십이 필요합니다.

라틴아메리카에서는 거시경제의 불안정성이 보급을 방해하고 있지만, 브라질의 ANVISA는 EU-FMD의 요건에 따른 직렬화를 추진하고 있으며, 추적성 대응 앰풀의 가능성이 넓어지고 있습니다. 그러나 아프리카 연합(AU)의 2040년 목표인 백신 제조의 60% 국산화는 예측 기간 후반에 BFS 투자를 촉진할 수 있습니다.

The ampoules packaging market reached USD 5.38 billion in 2025 and is projected to climb to USD 7.79 billion by 2030, translating to a 7.68% CAGR over the forecast period.

Expansion is anchored in the pharmaceutical sector's pivot toward single-dose injectable formats, propelled by biologics growth and global regulations that prioritize tamper-evident, serialised containers. Glass ampoules currently dominate because they combine chemical inertness with established regulatory acceptance, yet plastic formats are scaling quickly as blow-fill-seal (BFS) platforms prove their sterility and cost benefits. Asia-Pacific leads demand after China and South Korea approved new botulinum toxin indications in 2024, while AI-enabled visual inspection lines accelerate quality-assurance gains for high-volume producers. Competitive intensity remains moderate: leading suppliers differentiate on break-system design, traceability features and sustainability programs instead of unit price, cushioning margins even as energy-related costs fluctuate.

Drug manufacturers are investing heavily in visible tamper-evidence to satisfy FDA 21 CFR 211.132 and EU Falsified Medicines Directive requirements, steering ampoule specifications toward break-ring and score-line technologies that produce unmistakable indicators of interference. SCHOTT Pharma's One-Point-Cut system captured 62% of the global break-system sub-market by 2024, demonstrating how patient-safety features have moved from premium to standard expectation. Tamper-evidence also lowers liability risk for high-value biologics because compromised integrity directly threatens therapeutic efficacy. Hospitals increasingly cite simplified authenticity checks as a procurement criterion, encouraging suppliers to prioritise robust break designs. The resulting shift tightens qualification windows for alternative materials, reinforcing glass dominance in critical-care formulations.

Sustainability mandates push stakeholders to prefer containers that can re-enter production loops without downgrading quality. Type-I borosilicate satisfies this need: a 2024 closed-loop pilot by SCHOTT Pharma, Corplex and Takeda trimmed greenhouse-gas emissions by 50% versus virgin glass while meeting USP <660> chemical resistance benchmarks. European regulators now tie procurement incentives to recyclability scores, encouraging local health systems to favour glass derived from cullet streams. SGS audits confirm recycled Type-I maintains identical hydrolytic stability, so pharmaceutical-quality thresholds remain intact. As brand owners target Scope 3 decarbonisation, ampoule producers that guarantee traceable recycled content secure supply-agreement advantages. These developments extend to Asia-Pacific as multinationals transplant EU ESG criteria into regional tender processes.

Retail-oriented biologics and self-administered therapies are migrating to ready-to-inject syringes that offer dosing accuracy and patient convenience. Stevanato Group's 15% surge in syringe revenue in 2024 coincided with a 34% slump in vial sales, exemplifying format substitution pressure. Syringes carry superior margins, prompting producers to reallocate furnace hours away from ampoules. The shift is accelerated by blockbuster GLP-1 agonists, where self-injection adherence drives payer preference. Nevertheless, ampoules remain vital for drugs sensitive to silicone oil or tungsten residue associated with syringe stoppers. The segmented demand profile obliges ampoule suppliers to target niche, stability-critical molecules and invest in marketing that highlights glass purity advantages.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Glass maintained an 87% share of the ampoules packaging market in 2024, reflecting entrenched regulatory confidence and unmatched chemical durability. Plastic formats, however, are logging a 9.78% CAGR through 2030, powered by BFS lines that cut sterility validation steps and shrink labor outlays. Within glass, Type-I borosilicate remains the default for biologics, oncology drugs and highly reactive compounds. Corning's Valor composition eliminates delamination while retaining hydrolytic class I properties, widening glass's applicability to high-stress cold-chain environments.

Manufacturers adopt divergent business models: SCHOTT Pharma derived 55% of 2024 revenue from high-value glass offerings that command premium pricing, whereas polymer specialists chase volume in vaccines and generics. Supply-chain simplicity strengthens plastic economics because containers form, fill and seal in one pass, reducing secondary packaging needs. Still, the ampoules packaging market size for glass-based solutions stood at USD 4.69 billion in 2025, dwarfing plastic's USD 690 million contribution. The trajectory indicates coexistence rather than displacement, hinging on therapeutic risk tolerance, required shelf-life and sustainability calculus.

Straight-stem ampoules led with 63% of ampoules packaging market share in 2024, but user-friendly formats such as One-Point-Cut (OPC), score-ring and color-breakring designs are rising at 9.21% CAGR. Healthcare providers increasingly rank reduced needlestick injuries and breakage complaints as procurement criteria, making easy-open options indispensable for nursing and at-home care settings. In parallel, funnel-type ampoules retain relevance for viscous or suspension formulations where wider necks enable efficient filling.

Easy-open uptake is also fueled by self-administration trends in vaccines and aesthetics. SCHOTT Pharma's easyOPC design cuts opening force variability by 60%, thereby decreasing spillage risk during dose preparation. As break-system patents expire, mid-tier producers can emulate these features, intensifying price competition in lower-margin therapeutic classes. Nonetheless, premium biologics continue to favor proprietary break technologies that guarantee sterility and traceability, reinforcing margin resilience for innovation leaders. The ampoules packaging market size for easy-open variants is projected to surpass USD 2.1 billion by 2030, supported by differentiating ergonomic value.

The Ampoules Packaging Market Report is Segmented by Material Type (Glass, and Plastic), Ampoule Type (Straight-Stem, Funnel-Type, Closed Form D, and More), Capacity (<=2 ML, 3-5 ML, and Above 10 ML), End-User Industry (Pharmaceutical, and Personal Care and Cosmetics), Manufacturing Technology (Conventional Tubular Forming, Blow-Fill-Seal Plastic, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 39% of global revenue in 2024, buoyed by capacity expansions across China, India and South Korea as governments localise injectable drug supply chains. China's biopharmaceutical output hit CNY 565.3 billion (USD 78.4 billion) in 2024 and could eclipse CNY 1.4 trillion (USD 194 billion) by 2029, sustaining demand for ampoules despite sporadic API export restrictions tied to the 2024 Anti-Espionage Law. South Korea's aesthetics cluster in Gangnam fuels consistent small-volume glass orders, while India's "Make in India" incentives support BFS capacity additions for vaccines. Concurrently, ASEAN members court CDMOs by offering tax holidays and streamlined GMP approvals, amplifying regional competitiveness.

North America's growth is steadier, underpinned by biologics commercialisation pipelines and DSCSA compliance deadlines that require serialised primary containers. The United States drives high-value orders for Type-I glass and AI-enabled inspection lines that satisfy USP <1790> recommendations for parenteral visual inspection. Canada works to align with US traceability norms, spurring suppliers to provide bilingual packaging and GS1-compatible codes. Notably, herbicide litigation and supply-chain shocks have encouraged drug makers to dual-source ampoules from Mexico, broadening North American intra-regional trade.

Europe remains a value-rich but mature territory where sustainability and circular-economy targets dictate purchasing. The revised EU Packaging and Packaging Waste Regulation obliges recyclability scores above 70% by 2030, elevating demand for closed-loop Type-I glass streams. German hospitals formed a buying consortium in 2024 that gives 5-year contracts to vendors meeting >=50% cullet content, signalling future procurement norms. Meanwhile, energy-price volatility tied to gas supply cuts heightened concern over furnace downtime, prompting some firms to stockpile borosilicate tubing. Yet EU Recovery Funds earmarked for life-science infrastructure will subsidise next-generation inspection gear, partially offsetting cost fears.

The Middle East recorded the highest regional CAGR at 9.03% through 2030 as Saudi Arabia and the UAE channel public-health budgets into local manufacturing. Riyadh's Vision 2030 pharmaceutical programme co-funds sterile injectables plants, creating greenfield demand for BFS and tubular lines. Gulf Cooperation Council tender rules prioritize cost-effectiveness, positioning Indian and European mid-tier firms to capture share. However, limited skilled labour necessitates technology-transfer partnerships that intertwine equipment supply with long-term service contracts.

Latin America's uptake is hindered by macroeconomic instability, yet Brazil's ANVISA pushes serialization that mirrors EU-FMD requirements, opening opportunities for traceability-enabled ampoules. Africa remains nascent outside Egypt's vaccine complex; nonetheless, the African Union's 2040 target for 60% local vaccine manufacturing may catalyse BFS investments later in the forecast horizon.