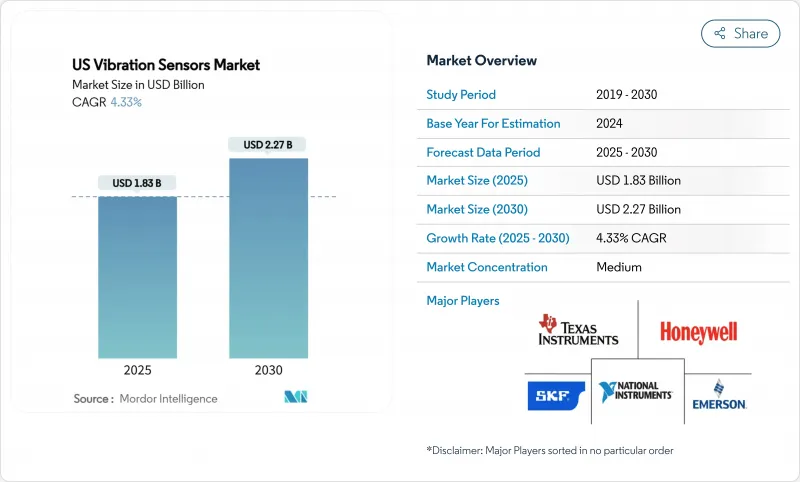

미국의 진동 센서 시장 규모는 2025년에 18억 3,000만 달러로 추정되고, CAGR 4.33%로 성장할 전망이며, 2030년에는 22억 7,000만 달러에 달할 것으로 예측되고 있습니다.

미국의 진동 센서 시장은 최종 사용자가 엣지 AI, 무선 연결 및 인더스트리 4.0을 채택함에 따라 양적 확장에서 기술 중심의 가치 창출로 전환하고 있습니다. 예측 분석의 채택, OSHA 및 API 표준에 따른 컴플라이언스 압력, 예기치 않은 다운타임을 제한할 필요성이 꾸준한 수요 증가를 지원합니다. 무선 노드, 에너지 수확 설계, MEMS 기반 가속도계는 노후화된 산업 자산에 대한 도입 옵션을 확대합니다. 공급업체는 하드웨어와 클라우드 분석을 번들로 제공하는 통합 솔루션을 통해 차별화를 도모하고 생태계 파트너십을 형성하여 사이버 보안 및 레거시 시스템 통합 문제를 해결합니다.

미국 제조업에서는 계획되지 않은 다운타임 비용이 매년 500억 달러를 초과하고 있으며, 시간 기반 유지보수 전략에서 상태 기반 유지보수 전략으로의 전환이 촉구되고 있습니다. 많은 공장에서는 현재 베어링의 마모와 미스 얼라인먼트를 조기에 검출해, 예비 부품의 재고를 삭감하면서 자산 수명을 30%까지 연장하는 지속적인 진동 모니터링을 도입하고 있습니다. 스펙트럼 데이터에 적용되는 머신러닝은 특히 상호 작용하는 기계가 있는 설비에서 인간 분석가가 놓칠 수 있는 이상을 식별합니다. 이러한 도구를 사용하는 풍력 발전소 운영자는 기어박스 고장을 예측하여 400만-500만 유로(430만-540만 달러)의 생산 손실을 피하고 있습니다. 조기 도입 성공으로 자동차, 금속, 식품 가공 현장에서의 폭넓은 전개가 가속화되고 있습니다.

무선 모니터링은 케이블 라우팅을 필요로 하지 않으며, 이전에는 도달할 수 없는 것으로 간주되었던 자산을 커버할 수 있습니다. LoRaWAN 네트워크는 15km 이상의 거리를 데이터 전송하며 원격 환경 감지에서 입증되었습니다. 주변의 진동과 열을 동력원으로 하는 에너지 수확 장치는 배터리 교체의 번거로움을 없애고 지금까지의 비용 장벽을 해결합니다. 베이커 퓨즈의 Ranger Pro 센서는 세계 위험 지역에서의 사용이 승인되었으며 기업 전체의 상태 모니터링을 추구하는 석유 및 가스 사업자에게 템플릿을 제공합니다. 짧은 도입 시간은 예정된 유지보수 창에 적합하며 신속한 ROI 계산을 지원합니다.

많은 시설들은 표준화된 센서 마운트나 통신 포트가 없는 수십년전에 제조된 장비에 의존합니다. 레트로핏은 새로운 자산에 센서를 설치하는 것보다 3배에서 5배 더 많은 비용이 듭니다. 오래된 프레임의 공진 효과는 신호의 충실도를 복잡하게 하고 노동 시간을 추가하는 사용자 정의 픽스처를 요구합니다. 여러 세대의 독자적인 프로토콜은 자본 투자 및 사이버 보안 위험을 증가시키는 게이트웨이를 필요로 합니다. 아날로그 디바이스의 Voyager4 플랫폼은 적응형 마운트와 온노드 AI를 제공해 이러한 장애물에 대항하고 있지만, 가격 감응도가 채용을 늦추고 있습니다.

가속도계는 2024년 출하의 45.1%를 차지했으며, 주파수 대역을 불문하고 범용성을 보여줍니다. 속도 센서는 대형 회전 기기의 저주파 고장을 조기에 파악하기 때문에 CAGR 7.81%로 가장 높을 전망입니다. 멀티파라미터 디바이스는 가속도, 속도, 온도를 결합하여 설치를 간소화하여 총 소유 비용을 절감합니다. 아날로그 디바이스는 이러한 패키지에 엣지 AI를 통합하여 네트워크 대역폭을 줄이는 온노드 고장 분류를 가능하게 합니다. 수력 발전소 및 종이 펄프 공장에서 속도 감지의 활용 확대는 미국의 진동 센서 시장의 다양성을 지원합니다.

두 번째 성장 인자는 3축 가속도계가 복합 동적 하중을 추적하는 타이어 및 기어박스 시험의 확대에 있습니다. 프록시미티 프로브는 틈새이지만 비접촉 터빈 용도에 필수적인 것은 아닙니다. 타코미터는 가변 속도 드라이브의 주문 분석을 위한 기준 계기로서의 가치를 유지합니다. 플랜트의 디지털화와 함께 자산 건강 플랫폼은 모든 제품 유형에서 데이터를 캡처하고 미국의 진동 센서 시장에서 하드웨어 마진을 확대하고 공급업체와 고객의 연결을 강화하는 서비스 수수료를 창출하고 있습니다.

유선 디지털 시스템은 입증된 신뢰성과 기존 케이블 트레이로 2024년 매출의 61.3%를 차지했습니다. 그러나 무선 노드는 배터리 수명과 무선 복원력 향상으로 매년 9.23% 성장합니다. LoRaWAN은 단일 게이트웨이로 킬로미터 규모의 도달 거리를 달성하고 분산형 태양광 발전소를 지원합니다. 하이브리드 파워 플러스 무선 아키텍처는 가동 시간과 오염 제어가 가장 중요한 제약 클린룸에서 등장합니다. 에너지 수확은 유지 보수 문제를 해결하고 슬립 링이 비용과 복잡성을 증가시키는 회전 킬른과 같은 이용 사례를 확대합니다.

데이터 다이오드 기능과 AES-256 암호화는 한때 유선 설정이 선호되었던 사이버 보안 문제를 완화합니다. 펌웨어 오버에어 업데이트를 통해 운영자는 물리적 액세스 없이 취약점을 패치할 수 있습니다. ISA100과 IEC 62938의 표준화는 공급업체 간의 상호 운용성을 촉진하고 미국의 진동 센서 시장 생태계를 확장합니다.

The United States vibration sensors market size reached USD 1.83 billion in 2025 and is forecast to reach USD 2.27 billion by 2030, reflecting a 4.33% CAGR.

The United States vibration sensors market is moving from volume expansion toward technology-driven value creation as end users adopt edge AI, wireless connectivity, and Industry 4.0 practices. Uptake of predictive analytics, compliance pressures from OSHA and API standards, and the need to limit unplanned downtime underpin steady demand growth. Wireless nodes, energy-harvesting designs, and MEMS-based accelerometers broaden deployment options across aging industrial assets. Suppliers differentiate through integrated solutions that bundle hardware with cloud analytics while forming ecosystem partnerships to address cybersecurity and legacy-system integration challenges.

Unplanned downtime costs exceed USD 50 billion each year across U.S. manufacturing, prompting a shift from time-based to condition-based maintenance strategies. Many plants now deploy continuous vibration monitoring that detects bearing wear and misalignment early, extending asset life by as much as 30% while cutting spare-parts inventory. Machine learning applied to spectral data identifies anomalies that human analysts can miss, especially in facilities with interacting machines. Wind-farm operators using these tools have avoided lost production valued at EUR 4-5 million (USD 4.3-5.4 million) by predicting gearbox failures. Early adoption success is accelerating broader rollouts across automotive, metals, and food-processing sites.

Wireless monitoring eliminates cable routing and allows coverage of assets once considered unreachable. LoRaWAN networks transmit data more than 15 kilometers, proven in remote environmental sensing. Energy-harvesting devices powered by ambient vibration or heat remove battery-change labor, addressing previous cost barriers. Baker Hughes' Ranger Pro sensor, approved for global hazardous areas, provides a template for oil and gas operators pursuing enterprise-wide condition monitoring. Short deployment times fit scheduled maintenance windows, supporting rapid ROI calculations.

Many facilities rely on equipment built decades ago without standardized sensor mounts or communication ports. Retrofitting can cost three to five times more than installing sensors on new assets. Resonance effects in older frames complicate signal fidelity and demand custom fixtures that add labor hours. Multiple generations of proprietary protocols require gateways that increase capex and cybersecurity exposure. Analog Devices' Voyager4 platform offers adaptive mounting and on-node AI to counter these hurdles, though price sensitivity slows adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Accelerometers represented 45.1% of 2024 shipments, underlining their versatility across frequency ranges. Velocity sensors post the highest 7.81% CAGR as they capture low-frequency faults earlier in large rotating equipment. Multi-parameter devices combine acceleration, velocity, and temperature to simplify installation and reduce total cost of ownership. Analog Devices integrates edge AI in such packages, allowing on-node fault classification that trims network bandwidth. Growing use of velocity sensing in hydropower and pulp-and-paper plants supports revenue diversity within the United States vibration sensors market.

The second growth driver lies in expanding tire and gearbox testing where triaxial accelerometers track compound dynamic loads. Proximity probes, though niche, remain indispensable in non-contact turbine applications. Tachometers retain value as reference instruments for order analysis in variable-speed drives. As plants digitize, asset-health platforms ingest data from all product types, creating service fees that augment hardware margins and strengthen supplier-customer ties within the United States vibration sensors market.

Wired digital systems delivered 61.3% of 2024 revenue thanks to proven reliability and existing cable trays. However, wireless nodes grow 9.23% annually as battery life and radio resilience improve. LoRaWAN achieves kilometer-scale reach on single gateways, supporting distributed solar farms. Hybrid power-plus-wireless architectures appear in pharmaceutical cleanrooms where uptime and contamination control are paramount. Energy harvesting addresses maintenance pain points and expands use cases such as rotating kilns where slip rings add cost and complexity.

Data-diode features and AES-256 encryption mitigate cybersecurity concerns that once favored wired setups. Firmware-over-air updates let operators patch vulnerabilities without physical access. Standardization under ISA100 and IEC 62938 promotes interoperability across vendors, broadening the ecosystem for the United States vibration sensors market.

The United States Vibration Sensors Market Report is Segmented by Product Type (Accelerometers, Proximity Probes, Tachometers, Velocity Sensors, Others), Sensor Technology (Wired, Wireless), Sensing Material/Principle (Piezoelectric, MEMS, Magnetostrictive, Fiber-Optic), End-User Industry (Automotive, Aerospace and Defense, Oil and Gas, Metals and Mining, and More). The Market Forecasts are Provided in Terms of Value (USD).